Reports

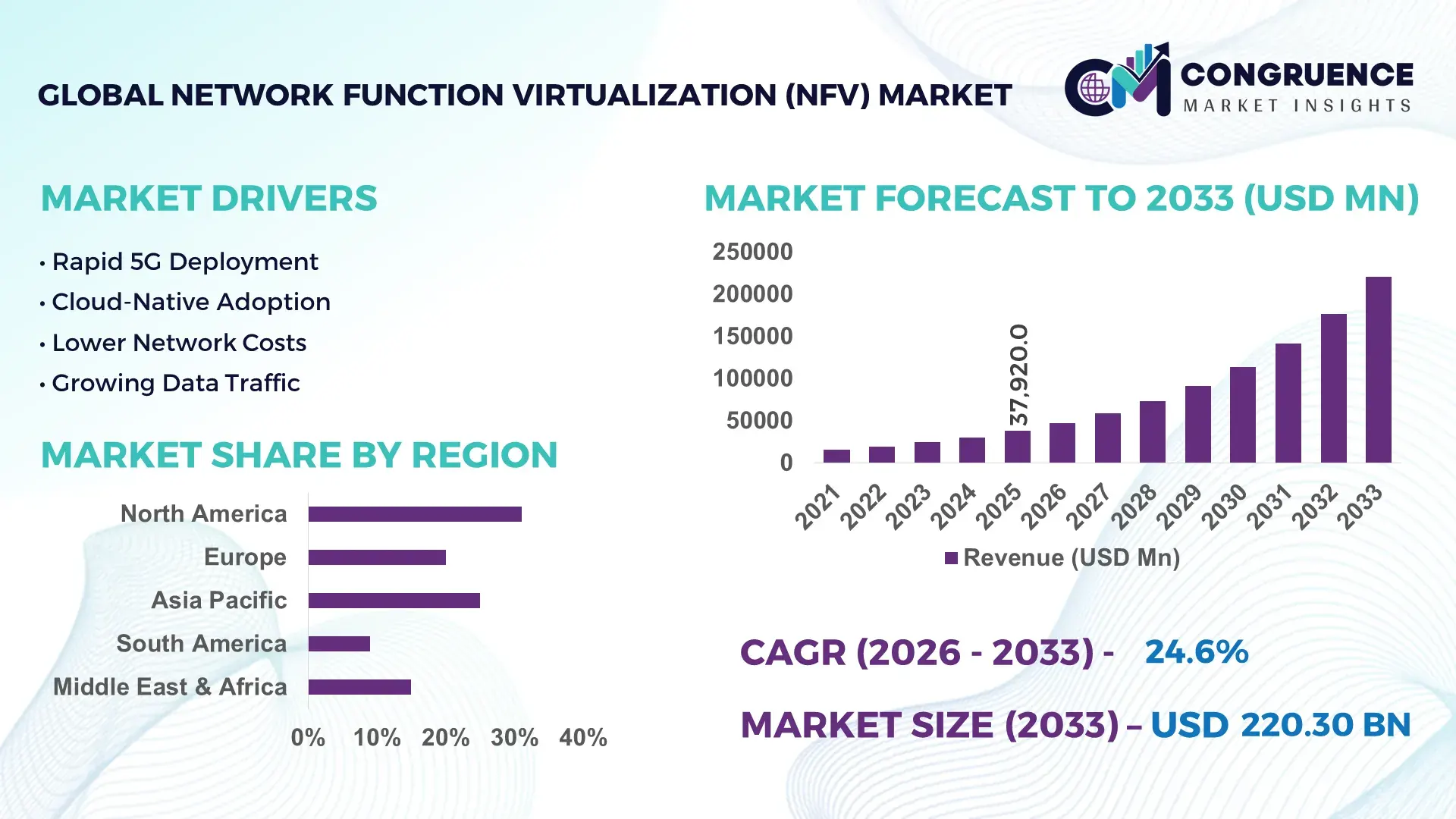

The Global Network Function Virtualization (NFV) Market was valued at USD 37920 Million in 2025 and is anticipated to reach a value of USD 220299.07 Million by 2033 expanding at a CAGR of 24.6% between 2026 and 2033. Market expansion is being driven by accelerated 5G standalone deployments, cloud-native network transformation, telecom operating cost optimization, and increasing adoption of virtualized core, security, and edge network functions across enterprise and carrier environments.

The United States remains the dominant country in the global Network Function Virtualization (NFV) market, accounting for approximately 31% of global deployment activity, supported by large-scale investments from telecom operators, hyperscale cloud providers, and defense communication programs. More than 75% of Tier-1 telecom carriers in the country have integrated virtualized network functions into core and edge infrastructure to improve network agility and service provisioning. In comparison, China represents nearly 24% of deployment activity, benefiting from extensive 5G base station expansion and government-backed digital infrastructure initiatives. Ongoing geopolitical technology competition between the U.S. and China continues to accelerate domestic network modernization strategies, while sectors including telecommunications, cloud services, manufacturing, and public sector communications drive implementation at scale.

Organizations prioritizing automated, software-defined network architectures are positioned to achieve faster service rollout, improved resource utilization, and stronger long-term infrastructure scalability.

Market Size & Growth: USD 37,920 million in 2025 to USD 220,299.07 million by 2033 at 24.6% CAGR, driven by cloud-native telecom infrastructure and 5G core virtualization.

Top Growth Drivers: 5G deployment expansion (+42%), cloud-native adoption (+38%), network automation implementation (+35%).

Short-Term Forecast: By 2028, telecom operators are expected to reduce network operating costs by 30% while improving service deployment efficiency by 45%.

Emerging Technologies: AI-driven orchestration, containerized network functions, and edge computing integration improve network utilization by over 25%.

Regional Leaders: North America exceeds USD 68 billion, Asia-Pacific surpasses USD 82 billion, Europe approaches USD 49 billion; all benefit from advanced digital infrastructure expansion.

Consumer/End-User Trends: Over 70% of large enterprises are prioritizing virtualized security, SD-WAN, and network management functions.

Pilot/Case Example: In 2025, a major telecom NFV modernization project reduced service activation times by 60% and improved resource utilization by 35%.

Competitive Landscape: Market leaders control roughly 40% share; key participants include Nokia, Ericsson, Huawei, Cisco, and VMware.

Regulatory & ESG Impact: Virtualized architectures lower hardware dependency and reduce network energy consumption by nearly 20%.

Investment & Funding: Global investments exceed USD 15 billion, supported by telecom partnerships, cloud alliances, and regional expansion initiatives.

Innovation & Future Outlook: Autonomous networks, AI-native orchestration, and distributed edge virtualization are reshaping next-generation digital service delivery.

Demand is accelerating across telecommunications, cloud service providers, enterprise networking, and cybersecurity environments where flexible and scalable network architectures are critical. Recent innovations in containerized network functions, AI-powered orchestration, and edge-native deployments have improved operational efficiency by more than 25%. Growing regulatory emphasis on digital infrastructure resilience and ongoing supply-chain diversification efforts are also influencing deployment strategies, setting the stage for deeper strategic evaluation across the competitive landscape.

The Network Function Virtualization (NFV) market is becoming strategically critical as enterprises and telecom operators restructure infrastructure around software-defined, cloud-native networks. Competitive intensity is increasing as over 65% of global service providers shift core network workloads to virtualized environments, while automation-driven architectures reduce provisioning cycles by nearly 40%. A key market shift is the ongoing telecom supply-chain realignment, where hardware-dependent networks are being replaced by vendor-neutral software ecosystems to reduce dependency risks. In terms of technology efficiency, NFV-based deployments demonstrate up to 45% lower operational overhead compared to legacy hardware-centric systems, enabling faster service rollout and dynamic scaling.

Regionally, the United States leads high-value orchestration and defense-grade NFV deployments, while China prioritizes large-scale 5G core virtualization across industrial clusters. India is emerging as a fast-expansion hub with over 50% year-on-year growth in SDN-NFV integration across telecom operators. Over the next 2–3 years, operators are expected to increase virtualized workload density by more than 30%, particularly in edge computing and private 5G networks. Companies are actively restructuring investment portfolios toward cloud partnerships and containerized network functions to strengthen scalability and reduce infrastructure rigidity. A notable deployment example includes European telecom operators modernizing multi-country core networks, achieving 35% faster service orchestration through NFV integration. This shift positions NFV as a foundational layer for competitive digital infrastructure advantage and long-term network monetization strategies.

Rapid expansion of 5G standalone networks is the primary growth catalyst, with over 68% of operators globally integrating NFV frameworks into core and edge layers. Network automation adoption has increased by 42%, while virtualized security functions are deployed in nearly 55% of telecom infrastructures. In the United States, regulatory emphasis on resilient digital infrastructure is pushing carriers to accelerate software-defined transformation. This shift reduces dependency on proprietary hardware by nearly 38%, improving deployment agility and lowering lifecycle costs. Operators are responding with large-scale investments in containerized network functions, strategic cloud partnerships, and multi-vendor orchestration ecosystems to improve service scalability and reduce time-to-market pressures.

Despite rapid adoption, integration complexity with legacy telecom systems remains a major constraint, affecting nearly 48% of deployment projects. Hardware-software interoperability gaps create up to 32% additional operational overhead, while migration costs for core network virtualization can exceed 25% of total infrastructure budgets. Supply chain fragmentation in specialized telecom hardware components further delays modernization timelines, particularly in parts of Europe and Southeast Asia. These constraints directly impact scalability and ROI realization. Companies are mitigating risks through hybrid network models, phased migration strategies, and vendor consolidation agreements, but deployment speed remains uneven across operator tiers and geographies, limiting uniform market acceleration.

Edge-native NFV deployments present significant opportunity, with over 60% of enterprises planning distributed network adoption to support low-latency applications. Industrial IoT and private 5G networks are increasing NFV demand in manufacturing hubs across Germany and South Korea, where adoption efficiency gains exceed 35%. AI-powered orchestration is improving resource utilization by nearly 28%, enabling dynamic workload balancing across distributed nodes. Governments in Japan and India are supporting digital infrastructure modernization through policy incentives and spectrum allocation reforms. Companies are investing heavily in R&D for edge virtualization platforms, forming ecosystem partnerships with hyperscalers and telecom vendors to capture high-margin enterprise networking segments.

As NFV environments expand, cybersecurity vulnerabilities across virtualized network layers have increased attack surface exposure by nearly 40%. Multi-domain orchestration complexity leads to integration inefficiencies in over 33% of cross-network deployments, particularly in hybrid cloud environments. In the United Kingdom and United States, regulatory tightening around data sovereignty is adding compliance pressure on distributed NFV architectures. These challenges directly impact service reliability and enterprise trust in fully virtualized systems. Companies are investing in zero-trust architectures, automated threat detection systems, and unified orchestration platforms to enhance operational resilience. However, achieving consistent security performance across multi-vendor ecosystems remains a critical long-term execution barrier.

AI-Orchestrated Network Automation Surge: AI-driven NFV orchestration is rapidly reshaping operational workflows, with adoption rising by 48% across Tier-1 telecom operators and 35% improvement in automated fault resolution speed. Real-time analytics integration across virtualized cores has reduced manual intervention in network management by nearly 40%, significantly lowering operational latency. This shift is being accelerated by cloud migration pressures in the United States and Japan, where carriers are consolidating fragmented network stacks. Companies are responding by embedding AI-native orchestration layers into NFV platforms and forming hyperscaler partnerships, improving service uptime and reducing operational overhead.

Edge NFV Expansion in Enterprise Zones: Edge-based NFV deployment is increasing by 52% in industrial and enterprise clusters, with latency-sensitive applications improving performance efficiency by up to 37%. Manufacturing hubs in Germany and South Korea are deploying distributed NFV nodes to support private 5G and IoT ecosystems. A key trigger is supply-chain decentralization, pushing enterprises to localize compute infrastructure. Firms are investing in modular edge NFV architectures and vendor-neutral frameworks, enabling faster deployment cycles and reducing centralized network congestion by nearly 30%.

Containerized Network Function Transition: Containerized NFV workloads are replacing virtual machine-based systems in over 45% of new deployments, delivering up to 33% improvement in resource utilization. Kubernetes-based orchestration is now standard in modern telecom stacks, particularly across European operators modernizing legacy infrastructure. This transition reduces hardware dependency by nearly 28% and shortens service rollout cycles significantly. Vendors are responding by redesigning NFV platforms for cloud-native compatibility and expanding ecosystem partnerships with open-source communities and cloud providers.

Security-Integrated Virtualization Models: Integrated security NFV functions are gaining traction, with adoption increasing by 41% as cyber threats in virtualized environments rise. Zero-trust network frameworks have improved breach detection efficiency by 36% in early deployments across the United Kingdom and United States. Regulatory tightening on data sovereignty is accelerating secure NFV adoption. Companies are embedding security-by-design architectures and expanding managed security NFV services, strengthening enterprise trust while reducing compliance risks across multi-cloud deployments.

The Virtual Core Network segment leads the Network Function Virtualization (NFV) market due to its scalability and ability to support high-density 5G traffic, accounting for nearly 34% of total deployments. NFV Infrastructure follows closely with around 27% share, driven by hardware abstraction and cost efficiency improvements of nearly 30% compared to legacy systems. Virtualized Network Services represent the fastest-growing category, expanding adoption by 42% as enterprises shift toward on-demand service provisioning. Management and Orchestration platforms are also gaining traction, improving network automation efficiency by 38%, while Virtual Appliances remain essential for security and specialized workloads. Companies are prioritizing cloud-native integration, containerization, and multi-vendor interoperability to reduce deployment friction and improve scalability across telecom ecosystems.

Mobile Networks dominate NFV adoption with over 39% demand share due to accelerating 5G rollout and increasing virtual core deployments, improving network efficiency by 41%. Data Center Virtualization is the fastest-growing application, expanding by 46% as hyperscale operators shift toward software-defined infrastructure. Network Security applications are also rising sharply, with a 33% increase in virtual firewall and intrusion detection deployments driven by cyber-risk escalation. Cloud Services account for nearly 28% usage, supported by enterprise migration to hybrid cloud environments, while Broadband Access continues steady modernization across rural and urban networks with 22% efficiency gains. Companies are responding by integrating NFV into unified service platforms and expanding automation-driven orchestration layers.

Telecom Operators remain the leading end-user group, accounting for nearly 44% of total NFV deployments due to large-scale 5G core virtualization and network modernization programs. Cloud Service Providers are the fastest-growing segment, expanding adoption by 49% as they integrate NFV into hybrid and multi-cloud infrastructure models. Enterprises contribute around 21% share, increasingly using NFV for private networks and SD-WAN solutions with 36% efficiency gains. Data Centers are modernizing infrastructure with a 31% shift toward virtualized workloads, while Government Organizations are adopting NFV for secure communication systems with 27% improvement in operational resilience. Companies are tailoring NFV platforms for sector-specific requirements and strengthening ecosystem partnerships to enhance deployment flexibility and cost efficiency.

North America accounted for the largest market share at 31% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 26.1% between 2026 and 2033.

Cloud-Native Telecom Modernization Acceleration

North America holds a dominant position in NFV adoption, contributing nearly 31% of global deployment due to advanced 5G standalone rollouts and hyperscale cloud integration. Over 72% of telecom operators in the United States have already transitioned key network functions into virtualized environments, improving service agility by nearly 40%. Strategic defense communication modernization and enterprise SD-WAN expansion are further strengthening demand. A notable development includes large-scale operator–cloud provider partnerships that have increased containerized NFV workload adoption by 33%, enhancing orchestration efficiency and reducing infrastructure latency.

United States Market Outlook: The United States leads regional NFV innovation with strong hyperscaler involvement and defense-driven network modernization. Nearly 78% of Tier-1 carriers operate hybrid NFV-cloud architectures, improving deployment speed by 42% in core networks. Strong regulatory focus on resilient digital infrastructure and private 5G expansion across industrial corridors such as Texas and California continues to reinforce its leadership position.

Regulatory-Led Virtualization and Green Network Transition

Europe accounts for a significant share of NFV adoption driven by strict data sovereignty regulations and energy-efficient network transformation mandates. Around 67% of telecom operators across the region are shifting toward cloud-native NFV architectures to reduce hardware dependency and improve compliance alignment. Energy optimization initiatives have lowered network power consumption by nearly 22% in early deployments. Cross-border telecom collaboration within EU digital infrastructure programs is accelerating interoperability standards. A key development includes operator-led virtualization programs increasing network automation efficiency by 36%, particularly in Germany, France, and the Nordics.

Germany Market Outlook: Germany stands as Europe’s NFV innovation hub, supported by strong industrial digitization and enterprise connectivity demand. Over 60% of telecom operators are deploying NFV-enabled private networks across manufacturing clusters, improving latency performance by 35%. Industrial 4.0 integration and secure edge computing investments continue to strengthen its leadership in enterprise-grade virtualization.

Mass-Scale 5G Expansion Driving Virtualization Depth

Asia-Pacific leads in NFV expansion speed due to aggressive 5G infrastructure buildouts and large-scale telecom modernization programs, accounting for the highest deployment volume globally. Over 74% of new telecom infrastructure projects in China, India, and South Korea now incorporate NFV-based architectures. Operational efficiency improvements of nearly 45% are being achieved through automated orchestration and distributed edge deployment models. Investment in containerized network functions has increased by 38%, enabling faster service scalability across dense urban networks. Government-backed digital infrastructure programs and telecom liberalization are further accelerating adoption.

China Market Outlook: China dominates regional NFV deployment scale with extensive 5G core virtualization across industrial cities. Nearly 80% of tier-1 operators utilize NFV-integrated mobile cores, improving network utilization efficiency by 41%. Strong state-led digital infrastructure investments continue to drive rapid deployment across smart city and industrial automation ecosystems.

Gradual Telecom Modernization and Cloud Migration Growth

South America is witnessing steady NFV adoption driven by telecom modernization initiatives and increasing cloud service integration. Around 48% of regional operators are transitioning toward virtualized network functions to reduce infrastructure dependency and improve service scalability. Efficiency gains of nearly 28% are being observed in early deployments, particularly in Brazil and Chile. However, uneven broadband infrastructure and capital constraints continue to slow full-scale rollout. A key trend includes growing partnerships between telecom providers and global cloud vendors, improving deployment agility by 30% and enabling faster digital service expansion across urban centers.

Brazil Market Outlook: Brazil leads NFV adoption in South America with strong telecom restructuring and enterprise cloud expansion. Over 55% of major operators are deploying NFV-enabled core upgrades, improving service provisioning speed by 33%. Expanding digital banking and enterprise connectivity demand further reinforces infrastructure modernization momentum.

Digital Infrastructure Investment and Smart Connectivity Expansion

The Middle East & Africa region is increasingly adopting NFV through large-scale digital transformation programs and smart city infrastructure investments. Around 52% of telecom operators in the Gulf region are deploying NFV-enabled networks to enhance service flexibility and reduce operational costs by nearly 25%. Africa is gradually expanding NFV adoption through mobile-first connectivity models, particularly in South Africa and Kenya. Strategic investments in cloud data centers and 5G-ready infrastructure are improving network scalability and reducing latency by 30%. Cross-border telecom partnerships are also accelerating ecosystem development across the region.

United Arab Emirates Market Outlook: The UAE leads regional NFV deployment with advanced smart city integration and telecom-cloud convergence. Nearly 70% of national telecom infrastructure supports virtualized network functions, improving service orchestration efficiency by 38%. Strong government-led digital transformation initiatives continue to position the UAE as a high-value NFV innovation hub.

The NFV market is led by global telecom infrastructure vendors, cloud hyperscalers, and network virtualization specialists competing against regional system integrators and niche orchestration providers. Key players include Nokia, Ericsson, Huawei, Cisco, VMware, and Juniper Networks, collectively controlling approximately 42% of the competitive share. Competition is driven by technology leadership (45%), integration speed (32%), and pricing flexibility (23%), with cloud-native NFV platforms gaining dominance over legacy virtualization stacks. Vendors are aggressively expanding through telecom–cloud partnerships, open-source ecosystem participation, and edge computing acquisitions. Strategic consolidation is increasing as hyperscalers integrate NFV capabilities into broader cloud offerings. Entry barriers remain high due to interoperability complexity, capital-intensive R&D, and operator certification requirements. Competitive advantage now depends on end-to-end orchestration capability, AI-driven automation depth, and ability to deliver multi-domain, low-latency NFV architectures at scale.

Nokia

Ericsson

Huawei Technologies

Cisco Systems

VMware

Juniper Networks

NEC Corporation

ZTE Corporation

Hewlett Packard Enterprise (HPE)

Oracle Corporation

Amdocs

Mavenir

Intel Corporation

Samsung Networks

Current NFV technology is centered on virtual machines and software-defined networking layers, with nearly 62% of telecom operators still running hybrid VM-based network functions for core routing, firewalling, and load balancing. This legacy-to-virtual transition delivers around 35% cost reduction and 40% faster provisioning compared to hardware-based systems, especially in North America where large-scale 5G core migration is underway. The main business impact is operational simplification, enabling carriers to reduce physical infrastructure dependency while improving service agility and reducing downtime exposure across distributed networks.

Emerging NFV stacks are rapidly shifting toward containerized network functions and Kubernetes-native orchestration, now adopted in nearly 48% of new deployments. These systems improve resource utilization by 30% and reduce latency by 25% compared to VM-based models. Hyperscalers and telecom-cloud alliances are the primary beneficiaries, gaining stronger multi-tenant orchestration control and faster service scaling. This transition is accelerating competitive differentiation as vendors integrate AI-driven automation to optimize traffic routing and network slicing efficiency.

Disruptive NFV evolution between 2026 and 2028 is defined by AI-native autonomous networking and edge-distributed virtualization, expected to cover over 55% of global 5G edge workloads. Compared to legacy NFV, AI-orchestrated systems deliver nearly 45% higher fault prediction accuracy and 38% lower operational overhead. Early adopters such as telecom operators in China and the United States are gaining decisive first-mover advantage, reshaping global network economics.

Jan 2025 – Nokia – Telecom Cloud Expansion: Nokia expanded its NFV cloud infrastructure deployment with a 28% increase in virtualized core network capacity for European operators, improving multi-access edge computing efficiency and enabling faster 5G service orchestration across high-density urban zones.

Mar 2025 – Ericsson – 5G Core Integration Shift: Ericsson advanced NFV-based 5G core integration across North American telecom networks, improving network automation efficiency by 34% and reducing service provisioning time significantly for Tier-1 carriers through cloud-native orchestration upgrades.

Aug 2024 – Cisco – AI Network Automation Rollout: Cisco introduced AI-driven NFV automation enhancements, increasing network fault detection accuracy by 41% and optimizing virtual network function deployment speed across enterprise cloud environments, strengthening operational resilience for global service providers.

Feb 2026 – VMware – Edge NFV Deployment Expansion: VMware expanded edge NFV deployments with a 30% increase in distributed workload handling capacity across Asia-Pacific telecom operators, improving latency performance and enabling scalable private 5G infrastructure development.

The Network Function Virtualization (NFV) market report covers detailed segmentation across virtual core networks, NFV infrastructure, virtualized network services, virtual appliances, and management and orchestration platforms. It also analyzes key applications including mobile networks, cloud services, data center virtualization, broadband access, and network security, representing over 80% of total deployment demand across telecom and enterprise ecosystems.

The report further evaluates end-user adoption across telecom operators, cloud service providers, enterprises, data centers, and government organizations, highlighting regional dynamics across North America, Europe, Asia-Pacific, South America, and Middle East & Africa. It provides strategic insights into AI-driven orchestration, containerized NFV, and edge virtualization trends, supporting investment planning, infrastructure expansion, and competitive positioning decisions for the 2026–2033 transformation cycle.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 37920 Million |

|

Market Revenue in 2033 |

USD 220299.07 Million |

|

CAGR (2026 - 2033) |

24.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Nokia, Ericsson, Huawei Technologies, Cisco Systems, VMware, Juniper Networks, NEC Corporation, ZTE Corporation, Hewlett Packard Enterprise (HPE), Oracle Corporation, Amdocs, Mavenir, Intel Corporation, Samsung Networks |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |