Reports

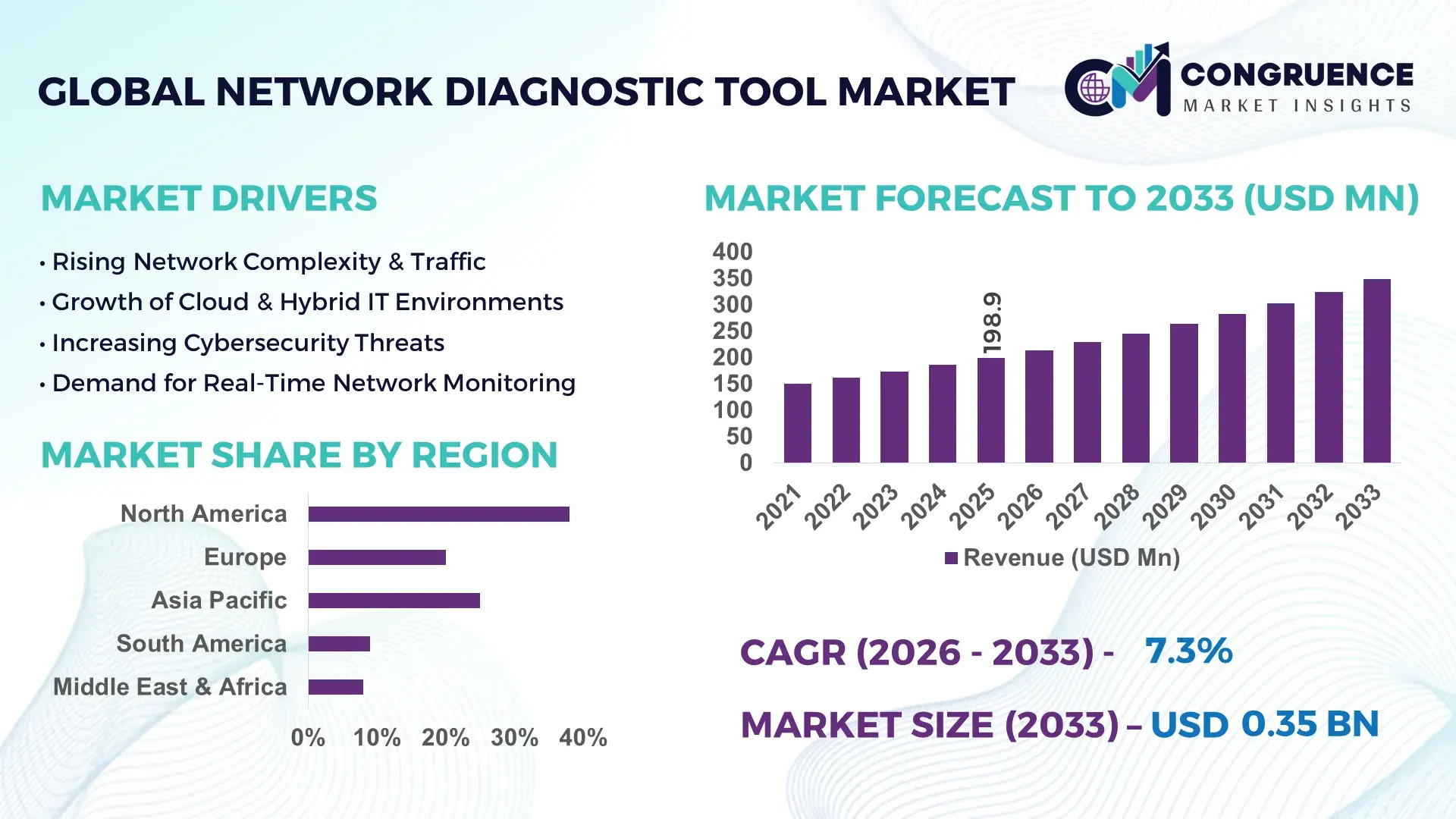

The Global Network Diagnostic Tool Market was valued at USD 198.94 Million in 2025 and is anticipated to reach a value of USD 348.27 Million by 2033 expanding at a CAGR of 7.25% between 2026 and 2033.

Enterprise network complexity driven by hybrid cloud adoption and 5G rollout is accelerating demand, with automated diagnostics improving fault detection efficiency by over 30% compared to traditional monitoring tools. Between 2024 and 2026, intensified cybersecurity regulations and data localization mandates across North America and Europe have pushed enterprises to deploy advanced network visibility solutions to ensure compliance and uptime continuity.

The United States dominates the market with approximately 38% share, supported by over USD 1.5 billion annual enterprise network infrastructure investments and strong adoption across BFSI, telecom, and hyperscale data centers. More than 65% of large enterprises in the U.S. deploy AI-driven diagnostic platforms, compared to under 40% in emerging markets, highlighting a significant maturity gap. Compared to legacy manual troubleshooting systems, modern network diagnostic tools reduce downtime by nearly 45% and operational costs by 20%, strengthening enterprise resilience.

Strategically, vendors prioritizing AI-led analytics and real-time monitoring capabilities are positioned to capture high-value enterprise contracts in compliance-driven markets.

Market Size & Growth: USD 198.94M (2025) to USD 348.27M (2033), CAGR 7.25%, driven by 5G and cloud network complexity.

Top Growth Drivers: AI-based diagnostics adoption (+32%), 5G network expansion (+28%), cybersecurity compliance demand (+25%).

Short-Term Forecast: By 2027, network downtime reduced by 35% through automated diagnostics integration.**

Emerging Technologies: AI-driven analytics, cloud-native monitoring, and real-time packet inspection improving efficiency by 30%.

Regional Leaders: North America (~USD 140M) leads in enterprise adoption; Europe (~USD 95M) driven by compliance; Asia-Pacific (~USD 80M) expanding via telecom upgrades.

End-User Trends: Over 60% of enterprises adopt predictive diagnostics tools to reduce network failures proactively.

Pilot Case Example: 2025 telecom deployment improved network uptime by 42% using AI-based diagnostic platforms.

Competitive Landscape: Top player holds ~18% share; key companies include Cisco, IBM, SolarWinds, Broadcom, and Keysight Technologies.

Regulatory & ESG Impact: Data compliance frameworks increased diagnostic tool deployment by 27% in regulated industries.

Investment & Funding: Over USD 900M invested globally in network analytics and monitoring startups between 2024–2026.

Innovation & Outlook: Shift toward autonomous networks and self-healing systems boosting efficiency by 40%.

Telecom contributes nearly 35% of total demand, followed by BFSI at 25% and IT services at 20%, reflecting high dependency on uninterrupted network performance. Recent innovations include AI-powered root-cause analysis tools improving troubleshooting accuracy by 33% and cloud-integrated diagnostics platforms reducing latency monitoring gaps by 28%. North America leads demand with over 38% share, while Asia-Pacific is expanding rapidly due to 5G infrastructure growth amid supply chain localization trends. The emergence of self-healing networks is redefining operational models, setting the stage for more autonomous and resilient network ecosystems.

The Network Diagnostic Tool Market is rapidly becoming a critical control layer for digital infrastructure, where uptime, latency precision, and cybersecurity resilience directly influence enterprise competitiveness. As enterprise networks evolve into multi-cloud and edge-driven architectures, diagnostic intelligence is no longer a support function but a strategic asset driving operational continuity and cost optimization. Organizations deploying advanced diagnostic platforms are reducing incident response time by over 40%, directly improving service-level compliance and customer retention metrics.

A major structural shift is emerging from tightening global data governance frameworks and increasing network complexity, forcing enterprises to transition from reactive monitoring to predictive diagnostics. AI-driven network diagnostic tools improve efficiency by 35% while reducing operational costs by 22% compared to legacy rule-based systems, fundamentally transforming network management economics. Regionally, North America leads in volume due to large-scale enterprise deployments, while Asia-Pacific leads in adoption acceleration with over 30% annual growth in AI-integrated diagnostics across telecom and cloud ecosystems.

In the next 2–3 years, automated diagnostics integration is set to reduce network downtime by 38% and improve fault prediction accuracy by 45%, optimizing enterprise IT operations at scale. ESG considerations are also emerging as a competitive advantage, with energy-efficient diagnostic platforms lowering network power consumption by 18%, enabling compliance with green IT mandates while reducing operational expenditure.

A real-world example includes a 2025 telecom operator deployment where AI-based diagnostics improved network uptime by 42% and reduced maintenance costs by 25%, demonstrating measurable ROI. Investment signals indicate companies are accelerating capital allocation toward autonomous network management, with over 50% of large enterprises prioritizing AI-driven diagnostics in IT budgets. This market is shifting from tool-based deployment to integrated intelligence ecosystems, positioning early adopters to dominate through superior network reliability, cost efficiency, and regulatory readiness.

The accelerating shift toward hybrid cloud, 5G, and edge computing is driving unprecedented network complexity, increasing fault detection challenges by nearly 30% in large-scale enterprise environments. This structural demand surge is forcing organizations to adopt advanced network diagnostic tools that enable real-time visibility and predictive analytics. A key global trigger includes rapid 5G infrastructure expansion, particularly across Asia-Pacific, where telecom operators have increased network investments by over 25%, directly amplifying the need for automated diagnostics. The cause is clear: fragmented network architectures lead to higher downtime risks, which in turn impact revenue and service quality. Businesses are responding by integrating AI-driven diagnostics that improve issue resolution speed by 40% and reduce manual intervention by 35%. Leading enterprises are accelerating partnerships with cloud providers and network solution vendors to enhance diagnostic capabilities. Additionally, companies are expanding capacity through strategic investments in network analytics platforms, ensuring scalable monitoring systems that align with evolving digital infrastructure demands.

Despite strong growth, the market faces constraints driven by high deployment costs and integration complexities, particularly for legacy infrastructure. Advanced diagnostic tools can increase initial IT spending by 20–25%, creating adoption barriers for mid-sized enterprises. Additionally, reliance on specialized hardware and proprietary software ecosystems creates vendor lock-in risks, limiting flexibility and increasing long-term operational costs by nearly 18%. A key real-world constraint is the uneven digital infrastructure maturity across regions, especially in emerging markets where only around 35% of enterprises have the required network architecture to support advanced diagnostics. This leads to scalability challenges and delayed adoption cycles. The business impact is significant, as organizations face extended deployment timelines and reduced ROI realization. To mitigate these risks, companies are diversifying vendor partnerships, adopting cloud-based diagnostic platforms, and investing in modular solutions that allow phased implementation. Long-term contracts and strategic alliances are also being used to stabilize costs and ensure consistent technology upgrades without disrupting operations.

The emergence of autonomous and self-healing networks is creating high-impact opportunities, with AI-driven diagnostics enabling up to 45% improvement in predictive maintenance accuracy. As enterprises shift toward intent-based networking, diagnostic tools are evolving into decision-making engines, unlocking new value layers beyond monitoring. A key innovation shift includes the integration of machine learning algorithms that reduce troubleshooting time by 38% and enhance network optimization efficiency by 30%. Emerging markets present a significant opportunity, with Asia-Pacific and Latin America witnessing over 28% growth in digital infrastructure investments, creating demand for scalable and cost-effective diagnostic solutions. Additionally, the rise of network-as-a-service models is opening new revenue streams, allowing companies to offer diagnostics as part of managed services. Organizations are positioning for dominance by increasing R&D investments, building ecosystem partnerships with cloud and telecom providers, and expanding into edge computing environments. This strategic focus is enabling companies to capture untapped demand while delivering differentiated value through automation and intelligence-driven diagnostics.

One of the most critical challenges is the integration of advanced diagnostic tools into complex, multi-vendor network environments, where interoperability issues affect nearly 32% of deployments. This creates operational inefficiencies and limits the full potential of diagnostic automation. Additionally, the shortage of skilled network professionals, with a gap exceeding 25% globally, is constraining effective utilization of advanced diagnostic systems. A significant real-world pressure is the increasing demand for ultra-low latency networks, particularly in sectors such as autonomous systems and real-time data processing, where even minor diagnostic delays can impact performance outcomes. This places additional strain on existing infrastructure and requires continuous upgrades. The long-term impact includes inconsistent performance optimization and reduced scalability, directly affecting business continuity. To remain competitive, companies must invest in standardized frameworks, enhance cross-platform compatibility, and build strategic partnerships to address integration challenges. Continuous innovation and workforce upskilling are essential to ensure sustainable growth and maintain a competitive edge in an increasingly complex network environment.

AI-driven diagnostics adoption exceeds 60%, reducing incident resolution time by 40%. Enterprises are actively shifting from rule-based monitoring to AI-integrated diagnostic platforms, with over 55% of deployments now including predictive analytics modules. This transition is reshaping operations by automating root-cause detection and reducing manual intervention by 35%. Companies are scaling AI capabilities through cloud partnerships and embedding machine learning into core network management workflows, directly improving service reliability and lowering operational overhead.

Cloud-native diagnostic tools grow by 48%, optimizing multi-cloud network visibility. Organizations are rapidly replacing on-premise diagnostic systems, with nearly 50% of enterprises migrating to cloud-based tools to manage distributed networks. This shift is driven by the need for real-time visibility across hybrid environments, reducing monitoring gaps by 28%. In response, vendors are restructuring product portfolios toward SaaS-based delivery models, enabling faster deployment cycles and flexible scaling aligned with dynamic workloads.

Asia-Pacific deployment expansion rises by 30%, driven by 5G infrastructure rollout. Telecom operators and enterprises across the region are accelerating diagnostic tool integration as network density increases, particularly in high-growth markets. While North America maintains operational volume leadership, Asia-Pacific is redefining adoption velocity through aggressive infrastructure scaling. Companies are responding by localizing solutions and forming regional alliances to capture demand, especially amid supply chain diversification trends impacting hardware availability.

Managed diagnostic services adoption increases by 35%, shifting toward outsourced network intelligence. Businesses are transitioning from in-house management to managed service providers, improving cost efficiency by 25% and reducing staffing dependency by 20%. This operational shift is forcing vendors to reposition offerings as integrated service platforms rather than standalone tools. A non-obvious shift is the bundling of diagnostics with cybersecurity services, enhancing value delivery while addressing regulatory compliance pressures in sensitive industries.

The Network Diagnostic Tool Market is segmented across types, applications, and end-users, reflecting diverse operational requirements and deployment environments. Demand is heavily concentrated in performance-driven and security-focused segments, with over 60% of adoption linked to enterprise network optimization and risk mitigation. There is a clear shift toward integrated diagnostic platforms that combine monitoring, analytics, and security functions, reducing tool fragmentation by nearly 25%. Application-wise, performance monitoring and troubleshooting dominate usage due to their direct impact on uptime and service quality, while emerging demand in security analysis is reshaping tool capabilities. End-user demand is led by IT and telecom sectors, but data centers and managed service providers are rapidly expanding their share, driven by increasing network complexity and outsourcing trends. This segmentation highlights a transition from standalone tools to unified diagnostic ecosystems, influencing vendor strategies and investment priorities.

Network Monitoring Tools dominate the segment with approximately 32% share, driven by their scalability and real-time visibility capabilities across complex network infrastructures. Their structural advantage lies in continuous monitoring and integration with cloud platforms, enabling proactive issue detection. However, Network Security Diagnostics is the fastest-growing segment, expanding at over 28% due to rising cybersecurity threats and regulatory enforcement, fundamentally shifting enterprise priorities toward integrated security visibility. Protocol Analyzers and Performance Testing Tools collectively account for nearly 38% share, serving critical roles in deep packet inspection and pre-deployment validation. While Protocol Analyzers provide granular traffic insights, Performance Testing Tools ensure network reliability under stress conditions, creating a complementary demand dynamic. Fault Management Tools, with around 12% share, remain essential for incident response but are increasingly being integrated into AI-driven platforms.

Demand is shifting toward multifunctional diagnostic solutions, forcing companies to invest in AI-enabled monitoring and security convergence. Vendors are expanding product capabilities and accelerating innovation in automated analytics, positioning Network Security Diagnostics and integrated monitoring platforms as key investment areas.

Performance Monitoring leads with approximately 30% share, as enterprises prioritize real-time network visibility to maintain service quality and uptime. This dominance is driven by the direct link between monitoring accuracy and operational efficiency. Security Analysis is the fastest-growing application, expanding at over 27%, fueled by increasing cyber threats and compliance requirements that demand continuous network surveillance. Network Troubleshooting, accounting for around 25%, remains a core application but is transitioning from reactive to automated processes. In comparison, Capacity Planning is gaining traction as organizations optimize resource allocation, improving network utilization efficiency by nearly 20%. Traffic Analysis and Capacity Planning together represent about 45% of the segment, supporting optimization and forecasting functions.

Usage patterns are shifting toward integrated platforms that combine monitoring, security, and analytics, reducing reliance on isolated tools. Companies are adapting by embedding AI capabilities into diagnostic workflows and scaling cloud-based deployments, aligning with evolving enterprise network demands.

IT & Telecom dominates with approximately 40% share, driven by high network dependency and continuous infrastructure expansion. These sectors require advanced diagnostics to maintain uptime and manage large-scale data traffic, making them the primary adopters. Managed Service Providers are the fastest-growing segment, expanding at over 30% as enterprises increasingly outsource network management to optimize costs and access specialized expertise. Enterprises account for around 22% share, showing steady adoption as digital transformation initiatives accelerate. In contrast, Data Centers are emerging as high-value users due to increasing demand for low-latency and high-availability environments, improving diagnostic tool utilization by nearly 25%. Government Organizations and Data Centers together contribute about 28%, reflecting growing emphasis on secure and resilient network infrastructure.

Demand behavior is shifting toward subscription-based models and customized diagnostic solutions. Companies are targeting these segments through flexible pricing, strategic partnerships, and tailored offerings that address specific operational challenges, positioning themselves to capture expanding demand in outsourced and high-performance network environments.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.10% between 2026 and 2033.

North America leads in demand concentration with strong enterprise adoption exceeding 60%, while Europe holds around 27% share driven by compliance-heavy deployments. Asia-Pacific, with nearly 24% share, is accelerating rapidly due to 5G expansion and cloud infrastructure scaling, increasing diagnostic tool adoption by over 30%. North America dominates in scale and enterprise spending, Europe leads in regulatory-driven innovation, and Asia-Pacific leads in expansion and infrastructure velocity. A key structural shift is supply chain localization across Asia, reducing deployment costs by 18% and accelerating regional adoption. Globally, companies are prioritizing Asia-Pacific for expansion while maintaining innovation hubs in North America and compliance alignment in Europe.

How are advanced network environments redefining operational intelligence demand?

North America holds approximately 38% market share, driven by high enterprise network complexity across telecom, BFSI, and hyperscale data centers. Over 65% of large enterprises deploy AI-integrated diagnostic tools, reflecting strong demand for predictive analytics and automation. A key structural force is tightening cybersecurity and data governance regulations, increasing compliance-driven deployments by 28%. Execution is shifting toward autonomous network operations, with organizations reducing downtime by 40% through real-time diagnostics. A notable strategic move includes large-scale cloud integration, with over 50% of enterprises transitioning to cloud-native diagnostic platforms. Enterprises prioritize reliability and compliance, making this region a primary investment hub for advanced, high-performance diagnostic solutions.

What is driving compliance-led transformation in network intelligence systems?

Europe accounts for nearly 27% of the market, with strong contributions from Germany, the UK, and France. Regulatory frameworks around data protection and sustainability are shaping demand, increasing diagnostic tool adoption by 25% in regulated industries. ESG-driven IT modernization is pushing enterprises to adopt energy-efficient diagnostics, reducing network power consumption by 15%. Operationally, companies are integrating compliance monitoring within diagnostic platforms, improving audit readiness by 30%. Enterprises demonstrate a compliance-first adoption pattern, prioritizing reliability and data sovereignty. This region forces vendors to innovate around regulatory alignment and sustainability, making it a critical market for compliance-driven product differentiation.

How is large-scale infrastructure expansion accelerating diagnostic tool deployment?

Asia-Pacific holds approximately 24% market share and ranks as the fastest-growing region, led by China, India, and Japan. Rapid 5G deployment and digital infrastructure expansion are driving demand, increasing diagnostic tool adoption by over 30%. The region benefits from cost-efficient infrastructure scaling and localized technology deployment, reducing operational costs by 20%. Execution is focused on mass adoption, with telecom operators integrating diagnostics across high-density networks. A key strategic move includes large-scale deployment across smart city projects, improving network performance by 35%. Enterprises prioritize speed and scalability, positioning Asia-Pacific as a critical region for volume-driven growth and expansion strategies.

What factors are shaping adoption amid infrastructure and cost constraints?

South America contributes approximately 6% to the global market, with Brazil and Mexico leading regional demand. Growth is driven by telecom expansion and increasing enterprise digitalization, improving diagnostic adoption by 22%. However, infrastructure limitations and cost sensitivity constrain large-scale deployment, with nearly 40% of enterprises facing integration challenges. Execution is shifting toward cloud-based diagnostic tools, reducing upfront costs by 18%. A strategic move includes telecom-led deployments improving network uptime by 28%. Enterprises prioritize cost-effective solutions, making this region a balance between emerging opportunity and operational risk for market participants.

How are infrastructure investments transforming network performance ecosystems?

The Middle East & Africa region accounts for around 5% of the market, with strong demand from the UAE, Saudi Arabia, and South Africa. Sector-driven demand from oil & gas and large infrastructure projects is increasing adoption by 20%. A key transformation driver is government-backed digital initiatives, accelerating network modernization efforts. Execution is focused on deploying advanced diagnostic tools across large-scale projects, improving network efficiency by 25%. Strategic investments in smart infrastructure are expanding deployment capacity, while enterprises prioritize reliability in mission-critical operations. This region is emerging as a strategic growth frontier, driven by infrastructure investment and digital transformation.

United States – 38% share: Network Diagnostic Tool Market dominance driven by large-scale enterprise adoption and advanced cloud infrastructure deployment.

China – 18% share: Network Diagnostic Tool Market growth supported by rapid 5G expansion and aggressive digital infrastructure investments.

The Network Diagnostic Tool Market is defined by competition between global technology leaders such as Cisco, IBM, Broadcom, Keysight Technologies, and SolarWinds, alongside specialized network analytics firms and regional solution providers. The top five players collectively hold approximately 52% share, reflecting moderate consolidation with strong competitive intensity. Competition is primarily based on technological capability, automation efficiency, and integration depth, with AI-driven diagnostic platforms improving operational efficiency by up to 35% and reducing downtime by 40%. Speed of deployment and customization are critical differentiators, particularly in enterprise and telecom segments. Companies are actively expanding through strategic partnerships with cloud providers and investing in R&D to enhance predictive analytics and real-time monitoring capabilities. A key competitive shift is the transition toward autonomous network management, forcing traditional vendors to restructure offerings into integrated platforms. Entry barriers remain high due to technical complexity and integration requirements, while pricing pressure persists in emerging markets. To win, companies must deliver scalable, AI-driven solutions with seamless integration and strong compliance alignment.

Cisco Systems

IBM Corporation

Broadcom Inc.

Keysight Technologies

SolarWinds Corporation

NetScout Systems

VIAVI Solutions

ManageEngine

Riverbed Technology

Paessler AG

Nagios Enterprises

AI-driven network diagnostics is redefining operational efficiency, with machine learning models improving fault detection accuracy by 35% and reducing mean-time-to-resolution by 40%. Over 60% of large enterprises have integrated AI-based analytics into their network monitoring stacks, enabling predictive maintenance and automated root-cause analysis. This shift delivers direct business impact through reduced downtime and optimized IT workforce allocation, strengthening service continuity in high-dependency environments.

Cloud-native diagnostic platforms are emerging as a dominant integration trend, with adoption exceeding 50% across hybrid and multi-cloud environments. These tools reduce deployment time by 30% and lower infrastructure costs by 20% compared to traditional on-premise systems. The integration of real-time telemetry and distributed monitoring is optimizing visibility across edge networks, enabling faster decision-making and improving performance consistency in complex architectures.

Disruptive technologies such as intent-based networking and self-healing systems are gaining traction, improving network resilience by 45% through automated remediation workflows. Compared to legacy rule-based systems, autonomous diagnostics deliver 35% higher efficiency while reducing manual intervention costs by 25%. Telecom operators and hyperscale cloud providers benefit most, gaining competitive advantage through scalable, low-latency network performance.

Between 2026 and 2028, the convergence of AI, edge computing, and cybersecurity diagnostics will accelerate adoption beyond 70% in enterprise networks. Vendors investing in integrated, automation-led platforms are positioned to lead, as the market shifts toward fully autonomous network ecosystems requiring immediate strategic alignment.

March 2026 – Cisco Systems launched an AI-powered network assurance platform enhancing anomaly detection accuracy by 38%, enabling real-time fault isolation across hybrid environments. This strengthens enterprise network resilience and reduces operational downtime significantly, reinforcing Cisco’s leadership in intelligent diagnostics. [AI Assurance Push]

Source: https://newsroom.cisco.com

November 2025 – IBM Corporation expanded its network observability suite with automation features improving incident response speed by 32%, targeting cloud-native enterprises. The upgrade enhances operational efficiency and supports large-scale digital transformation initiatives across regulated industries. [Observability Expansion]

Source: https://newsroom.ibm.com

July 2025 – Keysight Technologies introduced advanced network performance testing solutions achieving 40% faster validation for 5G infrastructure. This innovation accelerates telecom deployment cycles and strengthens testing accuracy in high-speed network environments. [5G Testing Leap]

Source: https://www.keysight.com

January 2024 – VIAVI Solutions partnered with telecom operators to deploy network analytics tools improving service assurance by 28% across large-scale 5G networks. This collaboration enhances network reliability and supports rapid infrastructure scaling. [Telecom Alliance Move]

Source: https://www.viavisolutions.com

The Network Diagnostic Tool Market Report delivers comprehensive coverage across five core product types, five application areas, and five major end-user segments, providing a structured view of demand distribution and technology deployment. The analysis spans key regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, capturing regional variations in adoption, infrastructure maturity, and regulatory influence. The report evaluates advanced technologies such as AI-driven diagnostics, cloud-native monitoring, and self-healing networks, with over 60% enterprise adoption highlighted for predictive analytics tools and nearly 50% deployment in hybrid cloud environments.

With deep analytical rigor, the report assesses more than 12 major companies and identifies over 25% shift toward integrated diagnostic platforms replacing standalone tools. It highlights emerging segments such as autonomous network management and security-integrated diagnostics, reflecting evolving enterprise priorities. Strategic insights are designed to support decision-making across investment planning, market entry, and competitive positioning, with clear indicators on where demand is accelerating and where technology adoption is reshaping operational models.

The forward-looking scope (2026–2033) focuses on increasing automation, with adoption of AI-based diagnostics projected to exceed 70% across large enterprises, alongside rising demand for edge network monitoring. This positions the report as a critical resource for stakeholders seeking actionable intelligence in a rapidly transforming network ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 198.94 Million |

|

Market Revenue in 2033 |

USD 348.27 Million |

|

CAGR (2026 - 2033) |

7.25% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Cisco Systems, IBM Corporation, Broadcom Inc., Keysight Technologies, SolarWinds Corporation, NetScout Systems, VIAVI Solutions, ManageEngine, Riverbed Technology, Paessler AG, Nagios Enterprises |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |