Reports

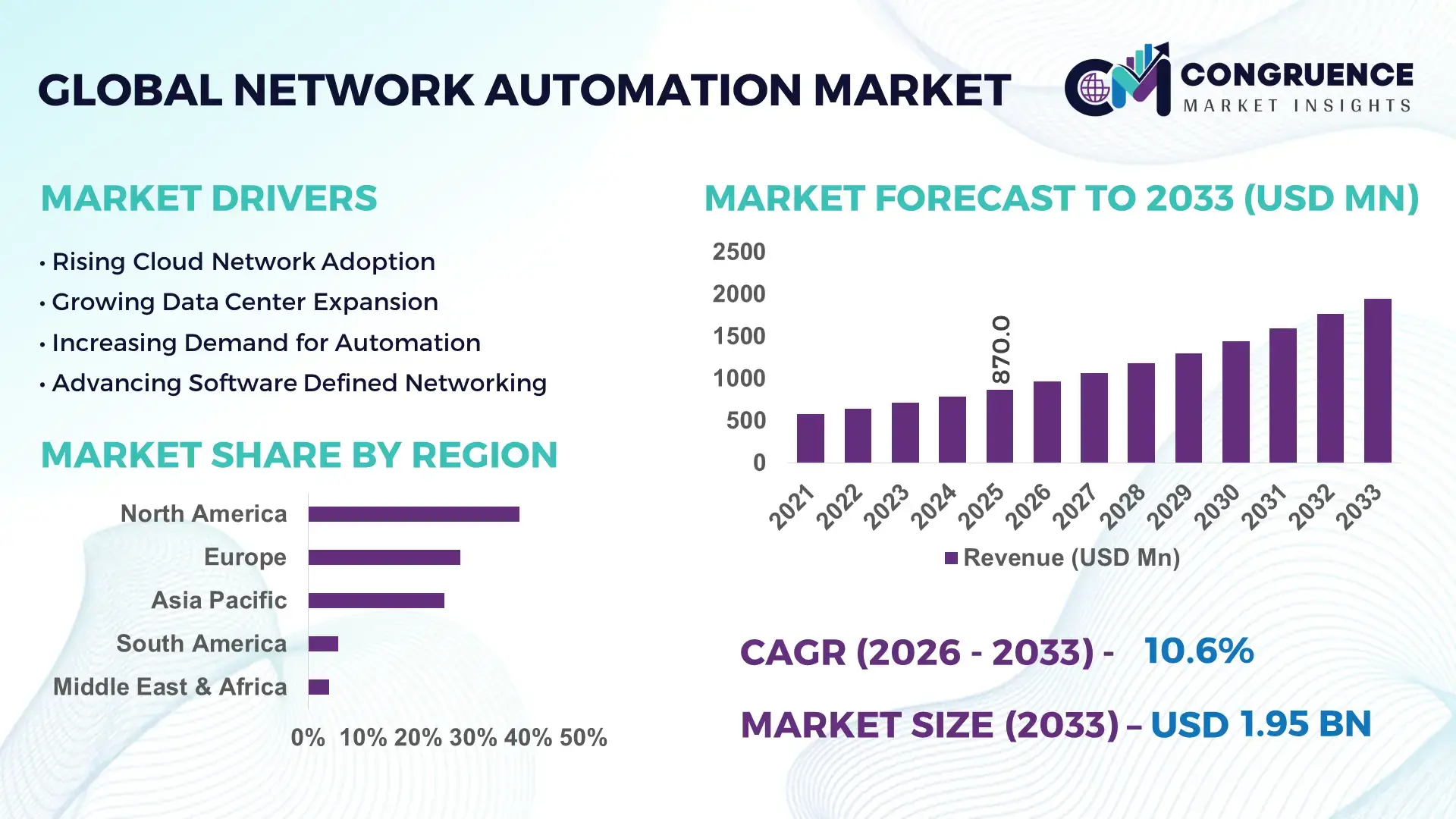

The Global Network Automation Market was valued at USD 870.0 Million in 2025 and is anticipated to reach a value of USD 1,947.9 Million by 2033 expanding at a CAGR of 10.6% between 2026 and 2033. Growth is being accelerated by large-scale deployment of AI-driven network orchestration platforms, 5G infrastructure expansion, and rising adoption of intent-based networking across enterprise and telecom environments.

The United States dominates the global network automation landscape with approximately 34% market share, supported by over 5.4 million enterprise network nodes and annual digital infrastructure investments exceeding USD 90 billion. Telecom operators and hyperscale cloud providers have automated nearly 68% of routine network management tasks, compared with around 52% in Germany. Ongoing infrastructure modernization initiatives and cybersecurity mandates have further strengthened automation adoption across critical industries including telecommunications, financial services, and data center operations.

Vendors that integrate AI-powered orchestration, security automation, and multi-cloud network visibility into unified platforms are positioned to secure long-term enterprise contracts and strengthen competitive differentiation.

Market Size & Growth: USD 870.0 Million in 2025 reaching USD 1,947.9 Million by 2033 at 10.6% CAGR, supported by accelerating AI-based network orchestration and 5G deployment programs.

Top Growth Drivers: Enterprise automation adoption +41%, cloud-network integration +38%, and intent-based networking deployment +35% across large organizations.

Short-Term Forecast: By 2028, automated network operations are expected to reduce configuration errors by 45% and improve service provisioning efficiency by 40%.

Emerging Technologies: Generative AI, intent-based networking, and autonomous closed-loop automation are enabling up to 60% faster network troubleshooting.

Regional Leaders: North America (USD 720 Million), Europe (USD 480 Million), and Asia Pacific (USD 410 Million) lead through cloud expansion, telecom modernization, and smart infrastructure deployment.

Consumer/End-User Trends: Nearly 64% of enterprises prioritize automated network monitoring to strengthen uptime, security, and operational agility.

Pilot/Case Example: In 2024, a leading telecom automation initiative reduced network provisioning time by 70% and operational workloads by 35%.

Competitive Landscape: Cisco holds approximately 19% share, alongside Juniper Networks, Huawei, IBM, Nokia, and HPE driving platform innovation.

Regulatory & ESG Impact: Digital resilience regulations and energy-efficiency initiatives have improved network resource utilization by nearly 22%.

Investment & Funding: More than USD 6 billion has been directed toward AI networking, cloud automation partnerships, and telecom transformation programs.

Innovation & Future Outlook: Autonomous networking, AIOps, and software-defined infrastructure are reshaping global network operations amid ongoing digital infrastructure expansion.

Network Automation Market is witnessing stronger demand from telecom operators, hyperscale data centers, financial institutions, and cloud service providers seeking greater network visibility and operational control. AI-assisted automation platforms now process up to 50% more network events than conventional systems while improving incident response accuracy. Growing adoption of software-defined networking, combined with stricter cyber-resilience requirements and expanding edge-computing deployments, is creating new opportunities for intelligent orchestration platforms, setting the stage for deeper strategic market evolution.

Network automation has become a strategic priority as enterprises seek to manage increasingly complex digital infrastructures while maintaining operational resilience. The convergence of cloud computing, 5G deployments, and distributed enterprise architectures is transforming network management from a manual process into an intelligent, software-driven function. Organizations are prioritizing automation to improve service reliability, strengthen cybersecurity readiness, and support large-scale digital transformation initiatives. Recent infrastructure modernization programs across the United States, India, and Japan are accelerating investment in automated network operations and orchestration capabilities.

Modern AI-enabled automation platforms can reduce network provisioning times by more than 70% compared with traditional manual workflows while lowering operational intervention requirements by approximately 40%. North America leads in enterprise-scale deployment and platform innovation, while Asia-Pacific demonstrates faster implementation across telecom and smart-city ecosystems. For example, major telecom operators are increasingly deploying closed-loop automation systems that automatically detect, diagnose, and remediate network issues without human intervention, significantly improving service continuity.

Over the next two to three years, adoption of intent-based networking, AIOps, and multi-domain orchestration is expected to expand across enterprise, telecom, and cloud environments. Vendors are strengthening partnerships with cloud providers, cybersecurity firms, and infrastructure specialists to create integrated automation ecosystems. Organizations that successfully combine automation, analytics, and security capabilities will gain stronger operational efficiency, improved service quality, and sustainable competitive positioning in increasingly digital business environments.

Enterprise networks are becoming significantly more complex as organizations adopt hybrid cloud, edge computing, and distributed work environments. Nearly 68% of large enterprises now operate multi-cloud infrastructures, while automated network operations can reduce configuration errors by over 45%. The rapid rollout of 5G infrastructure and software-defined networking architectures is creating strong demand for intelligent orchestration platforms capable of managing dynamic network environments. In the United States, telecom providers are expanding AI-powered automation capabilities to improve network reliability and reduce operational workloads. This shift is driving vendors to invest heavily in AIOps, intent-based networking, and autonomous management systems. A key strategic insight is that organizations deploying end-to-end automation achieve faster service activation cycles and stronger network resilience, creating measurable operational advantages over competitors relying on manual network management processes.

Despite growing adoption, interoperability challenges remain a significant barrier to network automation deployment. More than 55% of enterprise networks continue to rely on legacy infrastructure that lacks native compatibility with modern orchestration platforms. Multi-vendor environments further increase integration complexity, with enterprises reporting implementation timelines that are approximately 30% longer when managing heterogeneous network ecosystems. In sectors such as manufacturing and utilities, operational continuity requirements often limit rapid infrastructure replacement. The result is slower deployment, increased integration costs, and delayed realization of automation benefits. Companies are responding through vendor-neutral orchestration frameworks, API standardization initiatives, and phased modernization strategies. A notable operational insight is that organizations prioritizing architecture standardization before automation deployment experience substantially lower implementation disruptions and stronger long-term scalability.

The emergence of autonomous networking presents one of the most significant opportunities across the market. Edge computing deployments are projected to support more than 40% of enterprise-generated data processing workloads, creating demand for intelligent distributed network management. AI-enabled automation platforms can reduce fault-detection times by approximately 60%, improving service quality across mission-critical environments. India’s digital infrastructure expansion and Japan’s advanced industrial automation initiatives are creating favorable conditions for next-generation network orchestration solutions. Vendors are increasing R&D investments in self-healing networks, predictive analytics, and closed-loop automation ecosystems. A less obvious opportunity lies in energy optimization, where automated traffic management can improve network resource utilization by over 20%, providing both operational and sustainability benefits while supporting broader digital infrastructure modernization goals.

As automation becomes more sophisticated, ensuring secure and scalable deployment remains a major industry challenge. Approximately 43% of organizations identify cybersecurity concerns as a primary obstacle to expanding automated network operations. Automated environments process vast volumes of configuration and telemetry data, increasing exposure to misconfigurations and advanced cyber threats if governance frameworks are inadequate. At the same time, shortages of professionals skilled in AI networking, orchestration, and automation engineering continue to constrain deployment consistency. In countries such as Germany and the United States, demand for advanced networking specialists exceeds available talent supply in several technology sectors. Companies are addressing these issues through cybersecurity-focused automation frameworks, workforce upskilling programs, and strategic technology partnerships. Long-term competitiveness will depend on balancing automation scale, security assurance, and operational expertise across increasingly autonomous network environments.

AI-Native Network Operations Expansion Enterprises are rapidly shifting from rule-based automation to AI-native operations, with nearly 62% of large organizations integrating AIOps into network management workflows. Automated root-cause analysis has reduced incident resolution times by approximately 45%, while predictive maintenance capabilities have improved network availability by over 30%. Rising cybersecurity requirements and increasingly complex multi-cloud environments are accelerating deployment. Vendors are expanding AI partnerships and embedding machine learning engines directly into orchestration platforms to improve operational visibility and decision-making speed.

Intent-Based Networking Deployment Growth Intent-based networking adoption is accelerating across telecom, financial services, and cloud infrastructure environments, with automated policy enforcement improving configuration accuracy by nearly 50%. More than 55% of new enterprise network modernization projects now include intent-driven management capabilities. Organizations are transitioning away from device-centric administration toward business-outcome-based automation models. This shift enables faster service provisioning, reduces manual intervention, and strengthens compliance management. Leading providers are expanding software-defined architectures and developing centralized orchestration frameworks to support large-scale deployment requirements.

Multi-Cloud Automation Standardization The rapid expansion of hybrid and multi-cloud architectures has increased demand for unified network automation platforms. Approximately 68% of enterprises now operate workloads across multiple cloud environments, creating significant orchestration complexity. Automated cross-domain management has lowered operational overhead by nearly 35% while improving workload mobility and application performance. Companies are consolidating management tools, standardizing APIs, and investing in vendor-neutral automation frameworks to streamline operations and reduce infrastructure fragmentation.

Closed-Loop Autonomous Networking Adoption Telecom operators and hyperscale data center providers are accelerating deployment of closed-loop automation systems capable of detecting and correcting network anomalies without human intervention. Automated remediation processes have reduced service disruption events by approximately 40%, while network provisioning speeds have improved by nearly 60%. Labor shortages in advanced network engineering roles are reinforcing this transition. Companies are restructuring operational models around autonomous workflows, investing in self-healing infrastructure, and strengthening ecosystem partnerships to support increasingly intelligent network environments.

Physical Network Automation represents the leading segment, accounting for approximately 58% of overall deployments due to its critical role in managing routers, switches, data center infrastructure, and telecommunications networks. Large enterprises and telecom operators continue prioritizing physical infrastructure automation because of its ability to reduce manual configuration efforts by nearly 45% while improving network consistency and uptime. The segment benefits from established deployment frameworks, strong interoperability across enterprise environments, and direct operational impact on infrastructure reliability. Vendors are enhancing automation platforms with AI-assisted configuration management and predictive maintenance capabilities to strengthen enterprise adoption. Virtual Network Automation is emerging as the fastest-growing segment as organizations accelerate cloud migration and software-defined networking adoption. More than 64% of new digital infrastructure projects now incorporate virtualized network functions to improve scalability and workload flexibility. While physical automation remains foundational for mission-critical infrastructure, virtual automation enables faster provisioning and resource optimization across hybrid environments. Companies are increasing investment in cloud-native orchestration platforms, SDN ecosystems, and integrated management tools. This shift is reshaping investment priorities toward software-driven automation strategies capable of supporting increasingly distributed and dynamic network architectures.

Data Center Automation remains the leading application segment, supported by rapid expansion of hyperscale facilities, cloud computing infrastructure, and enterprise digital transformation programs. Approximately 60% of automation deployments are linked to data center operations where organizations seek improved workload orchestration, resource utilization, and network reliability. Automated provisioning processes have reduced deployment times by nearly 50%, allowing operators to manage increasingly complex infrastructure with greater efficiency. Major cloud providers continue expanding automation investments to support large-scale data processing and application delivery requirements. Cloud Network Automation is the fastest-growing application segment as enterprises expand multi-cloud and hybrid-cloud strategies. More than 68% of organizations now operate workloads across multiple cloud environments, creating demand for automated orchestration and policy management solutions. WAN Automation and Security Automation continue gaining importance as organizations strengthen connectivity and cyber resilience initiatives. Businesses are responding through broader deployment of centralized automation platforms, AI-powered analytics, and software-defined networking capabilities. Demand is increasingly shifting toward applications that deliver unified visibility, faster provisioning, and improved operational consistency across distributed environments.

Telecom Service Providers represent the dominant end-user segment due to extensive network infrastructure requirements, ongoing 5G deployments, and increasing pressure to improve service reliability. Telecom operators account for roughly 35% of total automation investments, leveraging advanced orchestration platforms to manage large-scale network environments. Automated network operations have reduced provisioning timelines by nearly 60% while supporting higher traffic volumes and improved customer experiences. Major operators continue investing in autonomous networking capabilities to strengthen operational efficiency and reduce manual intervention. Cloud Service Providers are the fastest-growing end-user segment as hyperscale infrastructure expansion and multi-cloud adoption increase network complexity. Nearly 70% of large cloud operators are expanding automation capabilities to support dynamic workload distribution and service scalability. Enterprises, BFSI organizations, healthcare institutions, and government agencies are also increasing deployment of automated network management tools to strengthen security, compliance, and operational resilience. Vendors are targeting these segments through customized automation platforms, strategic ecosystem partnerships, and industry-specific deployment models. Future demand is increasingly concentrated among organizations managing high-volume, mission-critical digital infrastructure.

North America accounted for the largest market share at 38.4% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12.8% between 2026 and 2033.

North America maintains its leadership position through extensive deployment of cloud infrastructure, advanced telecom networks, and enterprise digital transformation initiatives. The region accounts for approximately 38.4% of global market demand, supported by high concentrations of hyperscale data centers and software-defined networking deployments. More than 65% of large enterprises have integrated network automation into core IT operations, enabling faster provisioning and reduced operational complexity. Growing adoption of AIOps platforms, combined with expanding 5G infrastructure, is accelerating automation investments across telecommunications, financial services, and technology sectors. Strategic partnerships between cloud providers and network vendors continue to strengthen automation capabilities and enterprise-scale deployment readiness.

United States Market Outlook: The United States represents the largest national market due to its leadership in cloud computing, AI adoption, and digital infrastructure investment. More than 5,000 large-scale data centers and extensive enterprise network ecosystems create strong demand for automated orchestration and management platforms. Telecommunications operators continue expanding autonomous network capabilities to support increasing data traffic volumes. Enterprise adoption of intent-based networking and AI-driven operations is improving network efficiency while reducing manual intervention requirements across highly distributed digital environments.

Europe remains a strategically important market supported by industrial digitalization, cybersecurity mandates, and large-scale network modernization programs. The region accounts for approximately 27.6% of global adoption, with strong deployment activity across manufacturing, telecommunications, and public-sector infrastructure. Network automation adoption has increased significantly as enterprises seek to strengthen operational resilience and comply with evolving digital governance requirements. Investments in software-defined networking and cloud connectivity continue to expand across key industrial economies. Sustainability initiatives are also encouraging intelligent traffic management and network optimization solutions capable of reducing infrastructure energy consumption while maintaining service reliability.

Germany Market Outlook: Germany leads the European market through its advanced industrial base, Industry 4.0 initiatives, and enterprise digital transformation investments. More than 55% of large manufacturing organizations have incorporated automated network management capabilities into production and operational environments. The country's strong telecommunications infrastructure and industrial automation expertise support widespread adoption of AI-enabled networking solutions. Businesses are increasingly integrating automation with industrial IoT environments to improve operational visibility, security, and infrastructure performance.

Asia-Pacific represents the fastest-expanding market, driven by aggressive digital infrastructure development, cloud adoption, and telecommunications modernization. The region accounts for approximately 24.8% of global market activity and continues to gain share through large-scale enterprise digitization initiatives. Expanding 5G deployments, smart-city projects, and hyperscale data center construction are creating substantial demand for intelligent network orchestration solutions. Enterprises are increasingly implementing automated operations to manage growing network complexity and support distributed digital services. Regional governments are also prioritizing advanced connectivity infrastructure to strengthen economic competitiveness and digital transformation objectives.

China Market Outlook: China remains the most influential market in Asia-Pacific due to its extensive telecommunications infrastructure, cloud ecosystem expansion, and large-scale digital economy initiatives. The country operates one of the world's largest 5G networks, with millions of base stations supporting automation-intensive network management requirements. Major cloud providers and telecom operators are investing heavily in autonomous networking platforms to improve scalability and operational efficiency. Strong government-backed digital infrastructure programs continue supporting deployment of advanced automation technologies across enterprise and public-sector environments.

South America is experiencing growing demand for network automation as enterprises modernize infrastructure and expand cloud-based operations. The region contributes approximately 5.4% of global market activity, with adoption concentrated in telecommunications, financial services, and large enterprise environments. Increasing demand for secure connectivity and operational efficiency is encouraging deployment of software-defined networking and automated monitoring solutions. Infrastructure limitations and uneven digital maturity remain challenges in certain markets; however, ongoing investments in cloud infrastructure and broadband expansion are improving deployment conditions. Enterprises are prioritizing automation to manage network complexity while supporting digital transformation objectives.

Brazil Market Outlook: Brazil represents the largest market in South America due to its extensive telecommunications sector, growing cloud ecosystem, and expanding enterprise digitization efforts. Large enterprises are increasingly investing in automated network operations to improve service reliability and reduce operational workloads. Data center development activity continues to rise, supporting demand for advanced orchestration platforms. Financial institutions and telecom operators remain among the most active adopters as they seek improved scalability, security, and network performance across increasingly complex digital infrastructures.

The Middle East & Africa market is gaining momentum through national digital transformation programs, smart-city initiatives, and expanding telecommunications investments. The region accounts for approximately 3.8% of global market activity and is increasingly adopting automated network management technologies to support modern connectivity requirements. Large-scale infrastructure modernization projects are encouraging deployment of intelligent networking platforms across government, telecommunications, and enterprise sectors. Cloud adoption and advanced cybersecurity initiatives are further strengthening demand. Strategic investments in digital infrastructure are creating favorable conditions for broader automation deployment while improving operational efficiency across critical sectors.

Saudi Arabia Market Outlook: Saudi Arabia leads the regional market through ambitious digital transformation initiatives, next-generation connectivity projects, and substantial technology investment programs. National modernization efforts are accelerating deployment of cloud infrastructure, AI platforms, and advanced telecommunications networks. Enterprise organizations are increasingly implementing automation solutions to support large-scale digital operations and improve service delivery. The country's smart-city developments and expanding data center ecosystem continue generating demand for intelligent network orchestration technologies capable of supporting complex and highly connected digital environments.

The Network Automation Market is characterized by competition between global networking leaders such as Cisco Systems, Juniper Networks, Nokia, Huawei Technologies, and Hewlett Packard Enterprise (HPE) versus regional infrastructure vendors and specialized automation software providers. The top five participants collectively control approximately 58% of market activity, creating a moderately consolidated competitive structure. Competition increasingly centers on AI-driven automation, multi-cloud orchestration, and autonomous network operations rather than hardware pricing alone. AI-native platforms have reduced troubleshooting workloads by nearly 40%, while automated provisioning lowers deployment time by approximately 60%, making technology differentiation the primary battleground. Vendors are expanding through acquisitions, ecosystem partnerships, and integrated software portfolios that combine observability, security, and orchestration capabilities. The HPE–Juniper integration reflects ongoing consolidation, while AI-native networking is disrupting traditional hardware-led competition. High interoperability requirements and enterprise trust create significant entry barriers. Winning requires scalable automation, AI-powered operations, multi-vendor compatibility, and strong enterprise integration capabilities.

Juniper Networks, Inc.

Nokia Corporation

Hewlett Packard Enterprise (HPE)

Huawei Technologies Co., Ltd.

IBM Corporation

Extreme Networks, Inc.

Arista Networks, Inc.

VMware, Inc.

NetBrain Technologies, Inc.

Forward Networks, Inc.

SolarWinds Corporation

Gluware, Inc.

Riverbed Technology, LLC

Network automation technology is rapidly shifting from rule-based orchestration toward AI-native operations. AIOps platforms, intent-based networking, and closed-loop automation are becoming foundational technologies across enterprise and telecom environments. Nearly 62% of large organizations have deployed AI-assisted network management functions, while automated root-cause analysis reduces incident resolution times by approximately 45%. Businesses are integrating machine learning engines directly into orchestration platforms to improve network visibility, resilience, and operational consistency.

Emerging technologies include digital twins, autonomous network controllers, agentic AI frameworks, and predictive analytics. Compared with traditional manual network administration, AI-driven automation reduces configuration errors by nearly 50% and accelerates service provisioning by more than 60%. Intent-based networking platforms automatically translate business policies into network actions, significantly improving governance and compliance. Telecom operators, hyperscale cloud providers, and financial institutions are among the largest beneficiaries because of their highly complex network environments and continuous uptime requirements.

Between 2026 and 2028, autonomous networking and self-healing infrastructure are expected to become major competitive differentiators. Adoption of digital-twin-enabled automation is expanding across advanced data centers, while AI-driven observability platforms continue improving network utilization by approximately 20%. Organizations acting now gain operational agility, faster deployment cycles, and stronger cyber resilience. Vendors investing aggressively in AI-native networking ecosystems, automation intelligence, and multi-cloud orchestration are expected to strengthen their competitive positioning as network complexity continues increasing globally.

September 2024 – Nokia launched its Event-Driven Automation (EDA) platform for AI-era data centers, introducing intent-based automation, digital twins, and Kubernetes-native orchestration. The platform reduces operational effort by up to 40% while improving lifecycle management efficiency, strengthening Nokia’s position in autonomous networking. Source: www.nokia.com

February 2025 – Juniper Networks expanded its AI-Native Routing portfolio with Mist AI-powered automation, proactive troubleshooting, and closed-loop remediation capabilities. The solution significantly accelerates WAN deployment and optimization while improving energy efficiency through automated resource management across enterprise and service-provider environments.

January 2025 – ionstream.ai selected Juniper’s AI-Native Data Center solution to power AI managed-services infrastructure supporting GPU-as-a-Service workloads. The deployment strengthens high-throughput, low-latency networking while simplifying fabric management and reducing operational complexity for enterprise AI environments.

August 2025 – HPE introduced new Mist agentic AI innovations enabling autonomous network operations through AI-powered troubleshooting, expanded digital experience twinning, and self-driving workflows. The enhancements accelerate operational automation and improve visibility across client-to-cloud environments, supporting next-generation AI-native networking strategies.

The report provides comprehensive analysis of the Network Automation Market across key technology domains, deployment models, applications, and end-user industries. Coverage includes Physical Network Automation and Virtual Network Automation, along with major applications such as Data Center Automation, Cloud Network Automation, WAN Automation, and Security Automation. The assessment evaluates demand patterns across telecom service providers, cloud service providers, enterprises, government organizations, and industry-specific digital infrastructure environments. More than 60% of current deployments are concentrated within cloud, telecom, and data-center-driven use cases, reflecting the market’s operational transformation priorities.

The report further analyzes competitive positioning across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. It examines emerging technologies including AIOps, intent-based networking, autonomous operations, digital twins, and closed-loop automation. Strategic insights cover deployment trends, partnership activity, infrastructure modernization initiatives, enterprise adoption patterns, and innovation roadmaps. The analysis supports investment planning, market-entry evaluation, expansion strategy development, competitive benchmarking, and identification of high-opportunity automation segments expected to influence industry direction between 2026 and 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 870.0 Million |

| Market Revenue (2033) | USD 1,947.9 Million |

| CAGR (2026–2033) | 10.6% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Cisco Systems; Juniper Networks; Nokia Corporation; Hewlett Packard Enterprise (HPE); Huawei Technologies; IBM Corporation; Extreme Networks; Arista Networks; VMware; NetBrain Technologies; Forward Networks; SolarWinds; Gluware; Riverbed Technology |

| Customization & Pricing | Available on Request (10% Customization Free) |