Reports

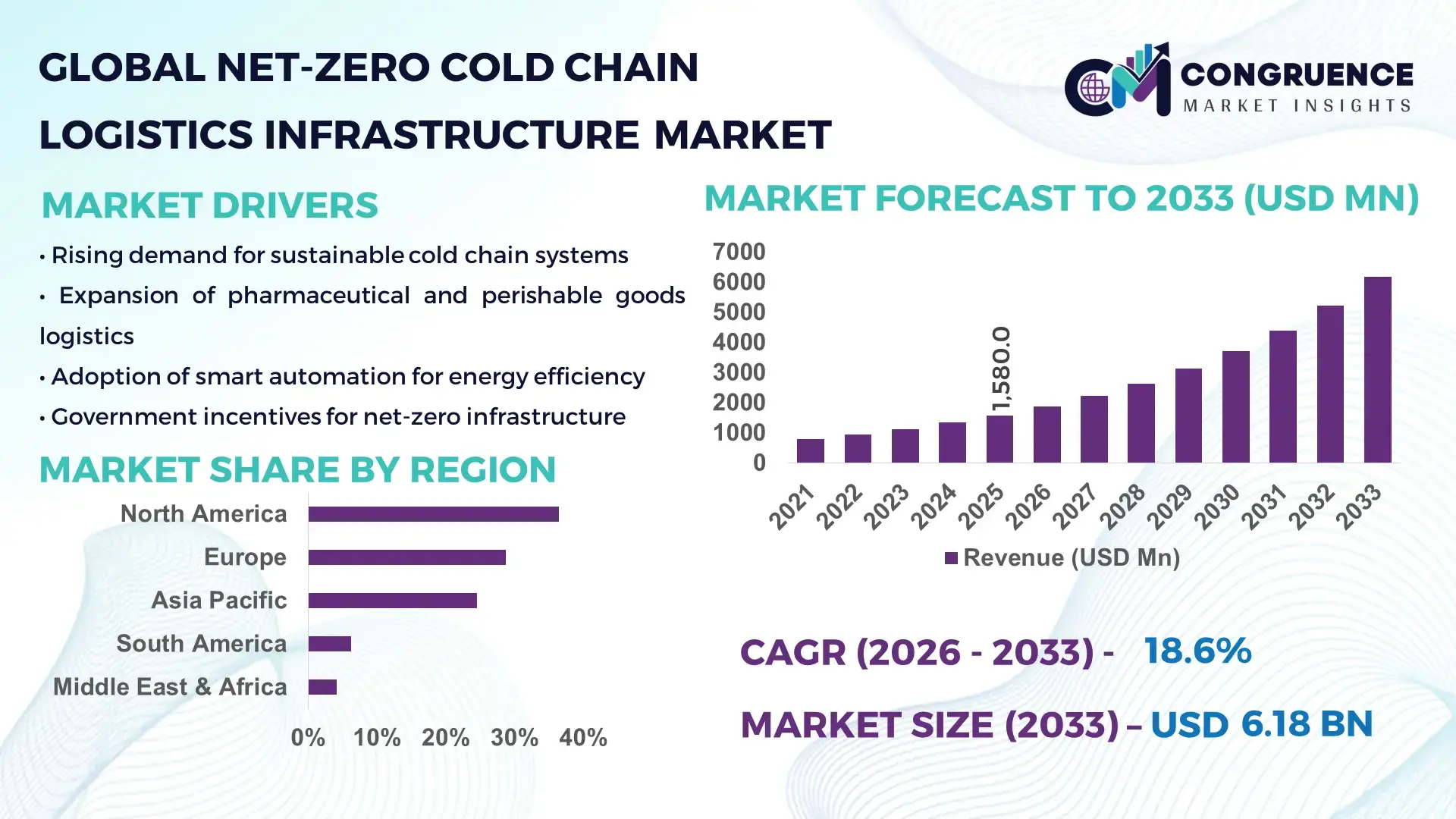

The Global Net-Zero Cold Chain Logistics Infrastructure Market was valued at USD 1,580.0 Million in 2025 and is anticipated to reach a value of USD 6,184.9 Million by 2033 expanding at a CAGR of 18.6% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is primarily driven by rising investments in sustainable refrigerated storage facilities, electrified refrigerated transportation fleets, and energy-efficient cooling technologies designed to reduce carbon emissions across food, pharmaceutical, and healthcare logistics networks.

The United States remains a central hub for net-zero cold chain logistics infrastructure development, supported by strong pharmaceutical distribution networks, advanced refrigeration technology manufacturing, and large-scale food logistics operations. The country operates over 3.7 billion cubic feet of refrigerated warehouse capacity, accounting for one of the largest cold storage infrastructures globally. More than 42% of newly commissioned cold storage warehouses since 2023 incorporate renewable energy systems, AI-enabled temperature monitoring, and low-GWP refrigerants. In addition, the U.S. pharmaceutical sector distributes over 65% of temperature-sensitive biologics through specialized cold logistics networks, while major logistics providers have committed to electrifying 30–40% of refrigerated truck fleets by 2030, accelerating the integration of net-zero cold chain infrastructure technologies across healthcare, food retail, and vaccine distribution systems.

Market Size & Growth: The market stood at USD 1,580.0 million in 2025 and is projected to reach USD 6,184.9 million by 2033, expanding at 18.6% CAGR due to increasing investments in low-emission refrigeration, electrified transport fleets, and renewable-powered cold storage infrastructure.

Top Growth Drivers: Approximately 47% growth impact from sustainable cold storage adoption, 38% from pharmaceutical cold chain expansion, and 32% from electrified refrigerated transport fleets accelerating net-zero infrastructure deployment.

Short-Term Forecast: By 2028, AI-enabled temperature monitoring and predictive refrigeration maintenance are expected to reduce cold chain energy consumption by nearly 18% while lowering operational losses by 12%.

Emerging Technologies: Adoption of solar-powered cold storage facilities, AI-driven energy optimization platforms, and low-GWP refrigerant systems such as CO₂ transcritical refrigeration is transforming infrastructure efficiency.

Regional Leaders:North America is projected to reach USD 2.1 billion by 2033 driven by pharmaceutical distribution networks; Europe is expected to approach USD 1.8 billion supported by green logistics regulations; Asia-Pacific could exceed USD 1.6 billion due to expanding food export cold chains.

Consumer/End-User Trends: More than 52% of global pharmaceutical manufacturers rely on temperature-controlled logistics, while food retailers account for nearly 40% of cold storage demand, emphasizing the shift toward sustainable infrastructure.

Pilot or Case Example: In 2024, a large European cold storage operator implemented renewable-powered refrigeration systems that reduced facility energy consumption by 26% and lowered carbon emissions by 31% across three logistics hubs.

Competitive Landscape: The market features a moderately consolidated structure led by Lineage Logistics (~14% share) followed by Americold Realty Trust, United States Cold Storage, Nichirei Logistics Group, and NewCold Advanced Cold Logistics.

Regulatory & ESG Impact: Governments across North America and Europe are enforcing low-GWP refrigerant mandates and carbon-neutral logistics targets, encouraging operators to cut refrigeration emissions by 30–50% by 2035.

Investment & Funding Patterns: Global investments exceeding USD 8 billion between 2022–2025 have been directed toward energy-efficient cold warehouses, smart refrigeration networks, and electrified logistics fleets.

Innovation & Future Outlook: The integration of IoT-based cold chain monitoring, AI energy analytics, and modular carbon-neutral warehouses is expected to significantly enhance operational sustainability and logistics resilience.

Net-zero cold chain logistics infrastructure is increasingly shaped by pharmaceutical distribution, food retail logistics, and global vaccine supply chains, which together contribute over 70% of cold chain demand. Innovations such as AI-enabled refrigeration monitoring, CO₂-based cooling systems, and solar-powered cold warehouses are improving operational efficiency. Strong regulatory frameworks targeting 40–60% emissions reduction in logistics operations by 2035, combined with rising demand for temperature-sensitive biologics and fresh food trade, are accelerating adoption across North America, Europe, and Asia-Pacific.

The Net-Zero Cold Chain Logistics Infrastructure Market has become strategically significant as global supply chains increasingly depend on temperature-controlled transportation and storage for pharmaceuticals, vaccines, biologics, seafood, dairy, and fresh produce. With global trade in temperature-sensitive pharmaceuticals exceeding USD 500 billion annually, the need for sustainable cold logistics infrastructure is intensifying. Governments and logistics operators are investing in carbon-neutral refrigeration technologies, energy-efficient warehouses, and electrified refrigerated fleets to meet sustainability goals while maintaining product integrity.

Technological modernization is a central strategic pathway for the sector. For example, AI-enabled refrigeration energy management delivers nearly 22% efficiency improvement compared to traditional fixed-temperature control systems. These advanced monitoring platforms analyze humidity, temperature fluctuations, and compressor load patterns to minimize energy consumption while maintaining precise temperature stability required for sensitive pharmaceuticals and biologics.

Regional dynamics also influence strategic development. North America dominates in cold storage volume due to its extensive food retail and pharmaceutical logistics networks, while Europe leads in sustainability adoption, with nearly 45% of logistics operators implementing low-GWP refrigeration technologies. Meanwhile, Asia-Pacific is witnessing rapid infrastructure expansion driven by food export industries and urban grocery distribution networks.

Short-term projections also highlight technology adoption trends. By 2028, AI-integrated cold storage automation systems are expected to reduce warehouse energy consumption by nearly 20% while improving operational uptime by 15%. Companies are simultaneously pursuing ESG commitments, with many logistics providers pledging 40% carbon emission reductions in refrigerated transport fleets by 2035.

Real-world implementation demonstrates measurable outcomes. In 2024, a large cold chain logistics operator in the Netherlands deployed solar-powered refrigeration warehouses that achieved a 28% reduction in grid electricity usage through integrated renewable energy systems and AI-based cooling optimization.

Looking ahead, the Net-Zero Cold Chain Logistics Infrastructure Market will remain a critical pillar of global supply chain resilience. Its integration of advanced refrigeration technology, sustainable logistics networks, and regulatory compliance initiatives positions it as a foundational element supporting climate-aligned trade, healthcare distribution, and sustainable food supply systems.

The Net-Zero Cold Chain Logistics Infrastructure Market is evolving rapidly as industries transition toward low-carbon logistics networks that maintain temperature stability while minimizing environmental impact. Demand for sustainable refrigerated warehouses, energy-efficient cooling systems, and electrified refrigerated transport fleets is increasing due to rising pharmaceutical distribution, vaccine logistics, and global food trade. Temperature-controlled supply chains are critical for products such as biologics, seafood, dairy, and fresh produce, which require strict thermal conditions during transportation and storage. Technological innovation is also influencing the market landscape. Advanced refrigeration systems using CO₂ transcritical cooling, ammonia-based refrigeration, and AI-driven energy management are enabling cold chain operators to reduce power consumption while maintaining precise temperature stability. Furthermore, IoT-based monitoring platforms allow real-time tracking of temperature conditions across warehouses and transport fleets, significantly reducing spoilage and logistics inefficiencies. Regulatory pressures and sustainability commitments are further shaping market dynamics. Several governments have introduced carbon reduction mandates targeting logistics and industrial refrigeration systems. Cold storage operators are therefore investing heavily in renewable-powered facilities, smart energy management systems, and low-emission refrigerants to comply with environmental regulations while improving operational efficiency.

The rapid expansion of biologics, vaccines, and temperature-sensitive medicines is significantly increasing the need for sustainable cold chain infrastructure. More than 70% of modern biologic medicines require temperature-controlled storage between 2°C and 8°C, while certain advanced therapies require ultra-low temperatures below -70°C during transportation. As pharmaceutical companies scale production of biologics and mRNA-based therapeutics, logistics providers must expand cold storage capacity while maintaining strict thermal stability. Additionally, global vaccine distribution networks depend heavily on reliable refrigerated logistics. During large-scale immunization campaigns, billions of vaccine doses must be transported under controlled temperatures to maintain efficacy. These requirements are encouraging logistics companies to adopt energy-efficient refrigeration units, real-time temperature monitoring systems, and renewable-powered cold storage warehouses to reduce emissions while maintaining product quality. Food logistics is another major contributor to demand. Nearly 30% of perishable food globally is lost due to inadequate cold chain infrastructure, encouraging governments and retailers to expand temperature-controlled storage networks. Sustainable cold warehouses and electric refrigerated vehicles are increasingly deployed to reduce food waste while improving supply chain efficiency.

Developing net-zero cold chain infrastructure requires substantial capital investment, particularly for energy-efficient refrigeration systems, renewable energy integration, and electrified transport fleets. Modern carbon-neutral cold storage facilities often incorporate advanced insulation materials, AI-driven refrigeration monitoring systems, and solar-powered cooling infrastructure, significantly increasing initial project costs compared to conventional cold warehouses. For example, implementing CO₂ transcritical refrigeration systems can increase installation costs by nearly 20–30% compared to traditional hydrofluorocarbon-based systems, even though they offer environmental benefits. Similarly, electrified refrigerated trucks require large battery systems capable of powering refrigeration units over long transport distances, raising vehicle acquisition costs for logistics operators. Infrastructure modernization also requires upgrading existing warehouses with high-efficiency compressors, thermal insulation systems, and automated energy management technologies. For small and medium-scale logistics operators, such investments can be difficult to justify without long-term regulatory incentives or financial support programs. Energy availability is another constraint. Renewable-powered cold storage facilities require large solar installations or energy storage systems to ensure uninterrupted refrigeration operations, particularly in remote logistics hubs where power reliability may be limited.

Digital transformation is creating significant opportunities for the Net-Zero Cold Chain Logistics Infrastructure Market by enabling smarter energy management, predictive maintenance, and real-time temperature monitoring. IoT-enabled sensors installed across refrigeration units, warehouses, and transport fleets allow logistics operators to track temperature fluctuations and equipment performance continuously. Advanced analytics platforms process this sensor data to identify inefficiencies in refrigeration systems. AI-based energy optimization software can automatically adjust compressor activity and airflow patterns, reducing energy consumption while maintaining precise thermal stability for sensitive products. These digital systems help cold chain operators reduce energy usage and minimize equipment downtime. Blockchain-based supply chain tracking is another emerging opportunity. By creating tamper-proof records of temperature data during transport and storage, logistics companies can enhance transparency and compliance with pharmaceutical quality standards. Such technologies are particularly important for global vaccine and biologics distribution networks. Additionally, smart warehouses equipped with automated pallet handling systems and robotics are improving cold storage efficiency. These facilities can reduce human intervention in refrigerated environments while optimizing storage capacity and lowering energy consumption.

Maintaining precise temperature conditions while minimizing energy consumption is one of the most complex challenges for net-zero cold chain infrastructure. Cold storage warehouses must maintain stable thermal environments even when external temperatures fluctuate significantly, particularly in regions with extreme climates. High-capacity refrigeration compressors and evaporators operate continuously to maintain temperature stability. These systems consume significant electricity, making energy efficiency improvements difficult without compromising product safety. Any deviation from required temperature ranges can lead to spoilage of pharmaceuticals, vaccines, or perishable food products. Furthermore, integrating renewable energy into cold storage operations introduces additional complexity. Solar-powered refrigeration systems must store excess energy during the day to maintain cooling during nighttime operations, requiring large energy storage batteries or hybrid power systems. Logistics transportation also presents challenges. Refrigerated trucks must maintain temperature stability during long-distance travel, even when vehicles are stationary during loading or customs inspections. Achieving net-zero emissions in such conditions requires advanced battery technologies, high-efficiency insulation materials, and sophisticated temperature control systems.

Expansion of Renewable-Powered Cold Storage Facilities: Renewable energy integration is becoming a defining trend in the Net-Zero Cold Chain Logistics Infrastructure Market. Approximately 41% of newly constructed cold storage warehouses globally are integrating solar photovoltaic systems, while nearly 27% are adopting hybrid renewable-battery energy systems. These facilities can reduce grid electricity consumption by 20–35% while maintaining continuous refrigeration operations for temperature-sensitive goods.

Rapid Adoption of Low-GWP Refrigeration Technologies: Refrigeration systems using CO₂ and ammonia-based cooling technologies now account for nearly 36% of new industrial cold storage installations worldwide. These low-global-warming-potential refrigerants can reduce greenhouse gas emissions from refrigeration units by up to 50% compared to traditional hydrofluorocarbon systems, making them increasingly popular among logistics operators seeking compliance with environmental regulations.

Integration of AI-Driven Energy Management Systems: Artificial intelligence is increasingly deployed in cold chain operations to optimize refrigeration energy usage. AI-enabled predictive maintenance systems have been shown to reduce compressor failure rates by nearly 22% and improve refrigeration efficiency by 15–18%. Approximately 34% of large cold storage operators are already implementing smart monitoring platforms to enhance temperature stability and reduce operational costs.

Electrification of Refrigerated Transport Fleets: Logistics providers are accelerating the transition toward electric refrigerated trucks to reduce carbon emissions in cold chain transportation. Industry estimates indicate that over 18% of newly purchased refrigerated delivery vehicles in 2025 are electric or hybrid models, while fleet electrification initiatives aim to convert 35–40% of refrigerated transport vehicles by 2035 across major logistics operators.

The Net-Zero Cold Chain Logistics Infrastructure Market is segmented across type, application, and end-user industries, reflecting the diverse technological and operational requirements of temperature-controlled supply chains. Infrastructure solutions vary significantly depending on refrigeration technology, warehouse design, and logistics transportation requirements. Net-zero initiatives are increasingly integrated across these segments through renewable energy adoption, low-GWP refrigerants, and digital monitoring systems. Cold storage infrastructure remains the backbone of the industry, providing large-scale refrigerated warehouse capacity for food distribution, pharmaceuticals, and industrial supply chains. Transport-based refrigeration solutions such as electric refrigerated trucks and temperature-controlled containers support long-distance logistics and last-mile delivery networks. Applications span pharmaceutical distribution, food and beverage logistics, agriculture exports, and chemical storage operations. Among these, pharmaceutical logistics is becoming increasingly critical due to the rising demand for biologics and vaccines requiring strict temperature stability. End-users include pharmaceutical manufacturers, food producers, logistics service providers, and retail chains. Their infrastructure requirements vary depending on product sensitivity, distribution scale, and regulatory compliance standards governing temperature-controlled logistics operations.

Cold chain infrastructure types primarily include energy-efficient cold storage warehouses, refrigerated transportation systems, and smart monitoring & automation platforms. Among these, energy-efficient cold storage warehouses dominate the market with approximately 46% share, as large-scale refrigerated facilities form the foundation of global food and pharmaceutical logistics networks. These warehouses incorporate advanced insulation materials, AI-driven refrigeration control systems, and renewable energy integration to maintain stable temperatures while minimizing carbon emissions. Refrigerated transportation systems account for about 34% of infrastructure deployment, supporting long-distance distribution of perishable goods and temperature-sensitive pharmaceuticals. Electrified refrigerated trucks and hybrid refrigeration units are increasingly used to reduce emissions during transport operations. Smart monitoring and automation platforms represent nearly 20% of infrastructure solutions, enabling real-time temperature monitoring, predictive maintenance, and automated warehouse management. Among these categories, smart monitoring platforms are the fastest-growing segment with an estimated growth rate of nearly 20% annually, driven by the rising adoption of IoT sensors and AI-based cold chain analytics platforms. The remaining infrastructure technologies collectively contribute roughly 54% of the market, including hybrid refrigeration systems, energy storage solutions, and modular cold warehouse structures.

• A 2025 technology deployment assessment by an international logistics research institute found that more than 1,200 cold storage warehouses worldwide implemented IoT-based refrigeration monitoring systems to maintain temperature stability for pharmaceutical distribution networks.

Applications in the Net-Zero Cold Chain Logistics Infrastructure Market include pharmaceutical logistics, food and beverage distribution, agriculture export supply chains, and chemical storage operations. Among these, food and beverage logistics represents the largest application segment with approximately 44% share, driven by global trade in perishable food products such as seafood, dairy, and fresh produce. Pharmaceutical logistics accounts for nearly 32% of cold chain infrastructure usage, as biologics, vaccines, and temperature-sensitive medicines require precise temperature control during storage and transportation. Increasing global vaccine distribution and biologic drug production are expanding demand for specialized cold logistics networks. Agriculture export logistics contributes around 14% of applications, supporting international trade in fruits, vegetables, and frozen food products. Chemical and specialty industrial storage applications represent roughly 10% of the market, requiring temperature-controlled handling for sensitive compounds. Among all segments, pharmaceutical logistics is the fastest-growing application with approximately 19% annual growth, driven by the rapid expansion of biologics and advanced therapies. Consumer adoption trends further reinforce these patterns. In 2025, nearly 52% of pharmaceutical manufacturers globally relied on specialized cold chain logistics networks, while about 46% of large food retailers implemented AI-based cold storage monitoring systems to prevent spoilage and improve supply chain efficiency.

• A global healthcare logistics study in 2025 reported that over 180 hospitals implemented advanced cold storage systems capable of maintaining ultra-low temperatures below –70°C for vaccine and biologic storage.

End-users in the Net-Zero Cold Chain Logistics Infrastructure Market include pharmaceutical manufacturers, food & beverage companies, logistics service providers, and retail chains. Among these, food and beverage companies represent the largest end-user segment with approximately 40% share, as supermarkets, food processors, and exporters depend heavily on refrigerated storage and transport to preserve product freshness and quality. Logistics service providers account for about 29% of market adoption, as third-party logistics companies operate large networks of cold warehouses and temperature-controlled transportation fleets serving multiple industries. Pharmaceutical manufacturers contribute nearly 22% of infrastructure demand, particularly for biologics and vaccine distribution networks requiring strict thermal stability. Retail chains and e-commerce grocery platforms make up the remaining 9%, supporting last-mile refrigerated delivery operations. The pharmaceutical sector is the fastest-growing end-user with an estimated growth rate of nearly 21% annually, driven by increased biologic drug production and expanding global vaccine distribution networks. Adoption trends further highlight the importance of sustainable infrastructure. In 2025, about 48% of large logistics providers reported deploying energy-efficient refrigeration systems, while more than 37% of pharmaceutical companies implemented digital temperature monitoring platforms across distribution networks.

• A 2025 industry technology survey found that over 500 global pharmaceutical companies deployed automated cold storage warehouses capable of maintaining multi-temperature zones for biologics, vaccines, and clinical trial materials.

North America accounted for the largest market share at 36.4% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 20.1% between 2026 and 2033.

The Net-Zero Cold Chain Logistics Infrastructure Market demonstrates strong regional diversification driven by food export trade, pharmaceutical logistics expansion, and sustainability-focused infrastructure investments. North America leads with more than 3.9 billion cubic feet of refrigerated warehouse capacity, supported by large pharmaceutical distribution networks and food retail supply chains. Europe follows with 28.7% of global market share, supported by aggressive decarbonization regulations and the rapid adoption of low-GWP refrigeration technologies across more than 1,200 industrial cold storage facilities. Asia-Pacific accounts for approximately 24.5% of global infrastructure installations, with China operating more than 195 million cubic meters of cold storage capacity and India expanding its network with over 8,500 cold chain facilities. South America represents 6.2% of the global market, driven by agricultural export logistics from Brazil and Argentina handling more than 65 million tons of temperature-sensitive food exports annually. Meanwhile, the Middle East & Africa contributes nearly 4.2% of the market, supported by rising pharmaceutical distribution infrastructure and food import logistics hubs across the UAE and South Africa.

North America represents the most mature regional ecosystem for the Net-Zero Cold Chain Logistics Infrastructure Market, accounting for approximately 36.4% of the global market share in 2025. The region hosts more than 1,800 temperature-controlled warehouses, collectively providing over 3.9 billion cubic feet of refrigerated storage capacity. Major demand drivers include pharmaceutical manufacturing, biologics distribution, vaccine storage, and large-scale food retail logistics networks. The United States alone accounts for nearly 82% of the regional cold storage infrastructure capacity, while Canada contributes significant expansion in seafood export cold logistics. Governments across the region have introduced incentives for low-GWP refrigerant adoption, electrified refrigerated transport fleets, and renewable-powered warehouses, supporting the transition toward carbon-neutral logistics systems. Advanced technologies such as AI-enabled refrigeration optimization platforms and IoT-based temperature monitoring sensors are widely implemented across logistics networks. A notable example includes Lineage Logistics, which has deployed solar-powered cold storage systems across more than 30 warehouse facilities, improving energy efficiency and reducing grid electricity usage. Regional consumer behavior shows higher adoption of temperature-controlled pharmaceutical distribution networks, particularly within healthcare and biotechnology industries.

Europe holds approximately 28.7% share of the Net-Zero Cold Chain Logistics Infrastructure Market, making it the second-largest regional contributor. Key markets include Germany, the United Kingdom, and France, which collectively account for more than 55% of the region’s refrigerated storage capacity. Germany alone operates more than 800 temperature-controlled logistics facilities, supporting food processing and pharmaceutical exports. European regulatory frameworks strongly influence the market landscape, particularly through sustainability initiatives such as the European Green Deal and F-Gas Regulation, which mandate the gradual phase-out of high-global-warming refrigerants across industrial refrigeration systems. As a result, nearly 48% of newly constructed cold storage warehouses in Europe utilize CO₂-based refrigeration technology. Technological advancements such as automated warehouse management systems, AI-driven energy monitoring platforms, and robotics-enabled cold storage operations are rapidly expanding. A notable regional player, NewCold Advanced Cold Logistics, operates fully automated cold warehouses capable of storing more than 70,000 pallet positions per facility, significantly improving energy efficiency. Consumer behavior across the region is influenced heavily by regulatory compliance, where sustainability certification requirements encourage enterprises to adopt transparent and environmentally responsible cold chain operations.

Asia-Pacific represents the fastest-growing regional market for net-zero cold chain infrastructure and currently accounts for nearly 24.5% of global infrastructure installations. The region hosts over 215 million cubic meters of cold storage capacity, with China, India, and Japan serving as the largest consuming countries. China alone operates approximately 195 million cubic meters of refrigerated storage, driven by the expansion of seafood exports, pharmaceutical manufacturing, and urban grocery logistics. India has expanded its cold chain infrastructure to over 8,500 cold storage facilities, supporting agricultural supply chains and vaccine distribution programs. Infrastructure modernization is also accelerating with the adoption of solar-powered cold warehouses, automated pallet handling systems, and IoT-based monitoring platforms. Technology innovation hubs in cities such as Shanghai, Tokyo, and Bangalore are driving the integration of digital cold chain analytics platforms capable of reducing energy consumption by nearly 17%. A notable regional player, Nichirei Logistics Group, has implemented advanced automated refrigeration warehouses capable of handling over 50,000 pallet units while optimizing power usage through AI-driven energy management systems. Regional consumer behavior is influenced by rapid e-commerce growth and the rising demand for fresh food delivery services across urban populations.

South America accounts for approximately 6.2% of the global Net-Zero Cold Chain Logistics Infrastructure Market, driven largely by agricultural exports and food processing industries. Key countries such as Brazil and Argentina dominate the region’s cold chain ecosystem, collectively managing more than 65 million tons of temperature-sensitive food exports annually, including poultry, beef, seafood, and fresh produce. Brazil operates over 1,300 refrigerated warehouses supporting global food distribution networks. Infrastructure development in the region is increasingly influenced by renewable energy integration, particularly solar-powered cold storage systems designed to reduce operational electricity costs. Governments have also introduced trade policies encouraging modern logistics infrastructure upgrades to support export competitiveness. A notable regional logistics operator, Frialsa Frigoríficos, has expanded its cold storage capacity across multiple Latin American ports to support temperature-controlled food exports. Consumer behavior in the region shows growing demand for frozen and packaged food products, particularly in urban retail markets, further encouraging investment in efficient cold storage networks and sustainable refrigerated transport systems.

The Middle East & Africa region contributes approximately 4.2% of the global Net-Zero Cold Chain Logistics Infrastructure Market, supported by expanding food import logistics, pharmaceutical distribution networks, and infrastructure modernization initiatives. Major growth countries include the United Arab Emirates and South Africa, both of which are investing heavily in advanced logistics hubs and refrigerated storage facilities. The UAE alone handles more than 18 million tons of temperature-sensitive food imports annually, requiring large-scale cold storage capacity across ports and free trade zones. Technological modernization is also accelerating, with cold storage facilities increasingly implementing automated warehouse management systems and energy-efficient refrigeration technologies to minimize power consumption. Regional trade partnerships and logistics corridor initiatives are supporting cross-border cold chain connectivity across the Gulf Cooperation Council and African trade networks. A regional operator, RSA Cold Chain, has developed integrated refrigerated warehouses and distribution networks across Southern Africa, improving supply chain efficiency for food retailers and pharmaceutical distributors. Consumer behavior patterns across the region are heavily influenced by urban population growth and rising demand for imported food products.

United States – 32.1% Market Share: It dominates due to its massive refrigerated warehouse capacity exceeding 3.7 billion cubic feet and strong pharmaceutical logistics demand.

China – 18.6% Market Share: It leads Asia-Pacific cold chain infrastructure expansion with over 195 million cubic meters of cold storage capacity and rapidly growing food export logistics networks.

The competitive landscape of the Net-Zero Cold Chain Logistics Infrastructure Market is moderately consolidated, with a combination of global logistics providers, cold storage infrastructure developers, and specialized refrigeration technology companies competing across multiple regions. The market currently includes over 120 active infrastructure developers and logistics operators globally, ranging from multinational cold chain logistics companies to regional refrigerated warehouse operators.

The top five companies collectively control approximately 42–46% of global market share, reflecting the strong influence of large cold storage infrastructure operators with extensive global networks. Leading companies are investing heavily in automated cold storage facilities, renewable-powered refrigeration systems, and AI-enabled energy management technologies to improve efficiency and sustainability. Strategic initiatives across the market include facility expansions, long-term partnerships with pharmaceutical companies, and mergers aimed at strengthening geographic distribution networks.

For example, several large logistics providers have collectively invested more than USD 10 billion in cold storage infrastructure expansion projects since 2022, focusing on automated warehouses capable of storing 50,000–80,000 pallet positions per facility. Companies are also deploying advanced refrigeration technologies such as CO₂ transcritical cooling systems and ammonia-based industrial refrigeration, which can reduce refrigeration emissions by nearly 45% compared to traditional systems.

Innovation is also shaping competitive differentiation. Approximately 38% of leading cold storage operators have implemented AI-based predictive maintenance systems, enabling real-time monitoring of compressor performance and reducing refrigeration downtime by nearly 20%. As sustainability commitments intensify across global supply chains, companies that integrate renewable energy systems, electrified refrigerated transport fleets, and advanced digital monitoring platforms are expected to strengthen their competitive positioning within the market.

Americold Realty Trust

United States Cold Storage

NewCold Advanced Cold Logistics

Nichirei Logistics Group

RSA Cold Chain

Frialsa Frigoríficos

AGRO Merchants Group

Snowman Logistics

Tippmann Group

Burris Logistics

VersaCold Logistics Services

Kloosterboer Group

Coldman Logistics

Technological transformation is playing a critical role in advancing the Net-Zero Cold Chain Logistics Infrastructure Market, particularly through the integration of energy-efficient refrigeration systems, digital monitoring platforms, and renewable-powered warehouse facilities. Modern cold storage infrastructure increasingly relies on low-global-warming-potential refrigerants such as CO₂ and ammonia, which can reduce refrigeration-related greenhouse gas emissions by up to 50% compared to hydrofluorocarbon-based systems.

Automation technologies are also transforming cold warehouse operations. Automated storage and retrieval systems (AS/RS) are capable of handling more than 300 pallet movements per hour, enabling large-scale facilities to operate efficiently while minimizing human exposure to extreme low-temperature environments. Robotics-assisted pallet handling systems further enhance warehouse productivity and reduce operational labor costs by nearly 20–25%.

Artificial intelligence and IoT-based monitoring technologies are increasingly integrated across cold chain infrastructure. Smart refrigeration systems utilize hundreds of connected temperature and humidity sensors, generating real-time data streams that allow predictive maintenance algorithms to detect compressor inefficiencies or refrigerant leaks before operational failures occur. Such systems can reduce refrigeration energy consumption by 15–18% while maintaining precise thermal stability.

Renewable energy integration is another key technological development. Solar photovoltaic systems installed on cold storage warehouse rooftops can generate up to 2–4 megawatts of electricity per facility, significantly reducing grid electricity consumption. Battery storage systems are also used to maintain refrigeration stability during peak demand hours or grid outages.

Additionally, blockchain-enabled cold chain monitoring platforms are gaining traction for pharmaceutical logistics. These systems create tamper-proof temperature records across distribution networks, ensuring compliance with strict healthcare regulations governing biologic drug transportation. Combined with AI-based analytics, these technologies enable cold chain operators to optimize logistics routes, reduce energy consumption, and improve product safety across temperature-controlled supply chains.

• In October 2025, Lineage Logistics was named Temperature Controlled Storage Operator of the Year 2025 at the Temperature Controlled Storage & Distribution Awards, highlighting its customer service excellence and leadership in advancing sustainable cold chain operations across its UK network, with a customer satisfaction score averaging 4.79/5. Source:- www.onelineage.com

• In March 2025, Americold Realty Trust completed a major solar energy installation at its Lurgan cold storage facility (Northern Ireland), generating approximately 616 MWh of renewable energy annually, covering about 21 % of the site’s energy needs and avoiding ~225 metric tons of CO₂ emissions per year as part of its sustainability and operational efficiency initiatives.

• In July 2025, Americold was recognized as a 2025 G75 Green Supply Chain Partner by Inbound Logistics for its sustainability leadership, including over 22 million kWh of energy savings from 25 projects in 2024 and 34 active solar installations across multiple global sites supporting reduced emissions and energy consumption strategies.

• Throughout 2025 and into 2026, NewCold Advanced Cold Logistics continuously expanded its automated cold chain network with multiple facility enhancements — including expansions in Lebanon, Indiana and McDonough, Georgia, alongside construction progress in Sydney, strengthening global temperature‑controlled logistics capacity and automation.

The Net-Zero Cold Chain Logistics Infrastructure Market Report provides a comprehensive analysis of global infrastructure development supporting sustainable temperature-controlled supply chains. The report evaluates key components of cold chain infrastructure, including energy-efficient refrigerated warehouses, temperature-controlled transport fleets, smart refrigeration monitoring systems, and renewable-powered cooling facilities. It examines market segmentation across infrastructure types, applications, and end-user industries, offering detailed insights into how sustainability initiatives are transforming cold chain logistics networks worldwide.

The report covers a wide geographic scope spanning North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting regional infrastructure capacity, technological adoption patterns, and policy environments supporting net-zero logistics development. The study analyzes cold storage capacity expansion trends, including the global deployment of more than 700 million cubic meters of refrigerated storage facilities and the increasing use of automated warehouses capable of managing 50,000–80,000 pallet positions.

Industry applications evaluated within the report include pharmaceutical distribution, food and beverage logistics, agriculture export supply chains, and specialty chemical storage operations. These sectors collectively account for the majority of demand for temperature-controlled logistics infrastructure, particularly due to the rapid growth of biologics manufacturing, vaccine distribution networks, and international food trade.

The report also explores emerging infrastructure segments such as solar-powered cold warehouses, AI-enabled refrigeration management platforms, blockchain-based supply chain monitoring systems, and electrified refrigerated transport vehicles. Additionally, the analysis evaluates strategic industry trends such as infrastructure automation, cold chain digitalization, and sustainability-driven investment initiatives shaping the future of temperature-controlled logistics networks globally.

Designed for logistics operators, cold storage infrastructure developers, food exporters, pharmaceutical manufacturers, and investment stakeholders, the report provides a structured overview of technological developments, infrastructure expansion patterns, and regional adoption trends influencing the global Net-Zero Cold Chain Logistics Infrastructure Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,580.0 Million |

| Market Revenue (2033) | USD 6,184.9 Million |

| CAGR (2026–2033) | 18.6% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia‑Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Lineage Logistics; Americold Realty Trust; United States Cold Storage; NewCold Advanced Cold Logistics; Nichirei Logistics Group; RSA Cold Chain; Frialsa Frigoríficos; AGRO Merchants Group; Snowman Logistics; Tippmann Group; Burris Logistics; VersaCold Logistics Services; Kloosterboer Group; Coldman Logistics |

| Customization & Pricing | Available on Request (10% Customization Free) |