Reports

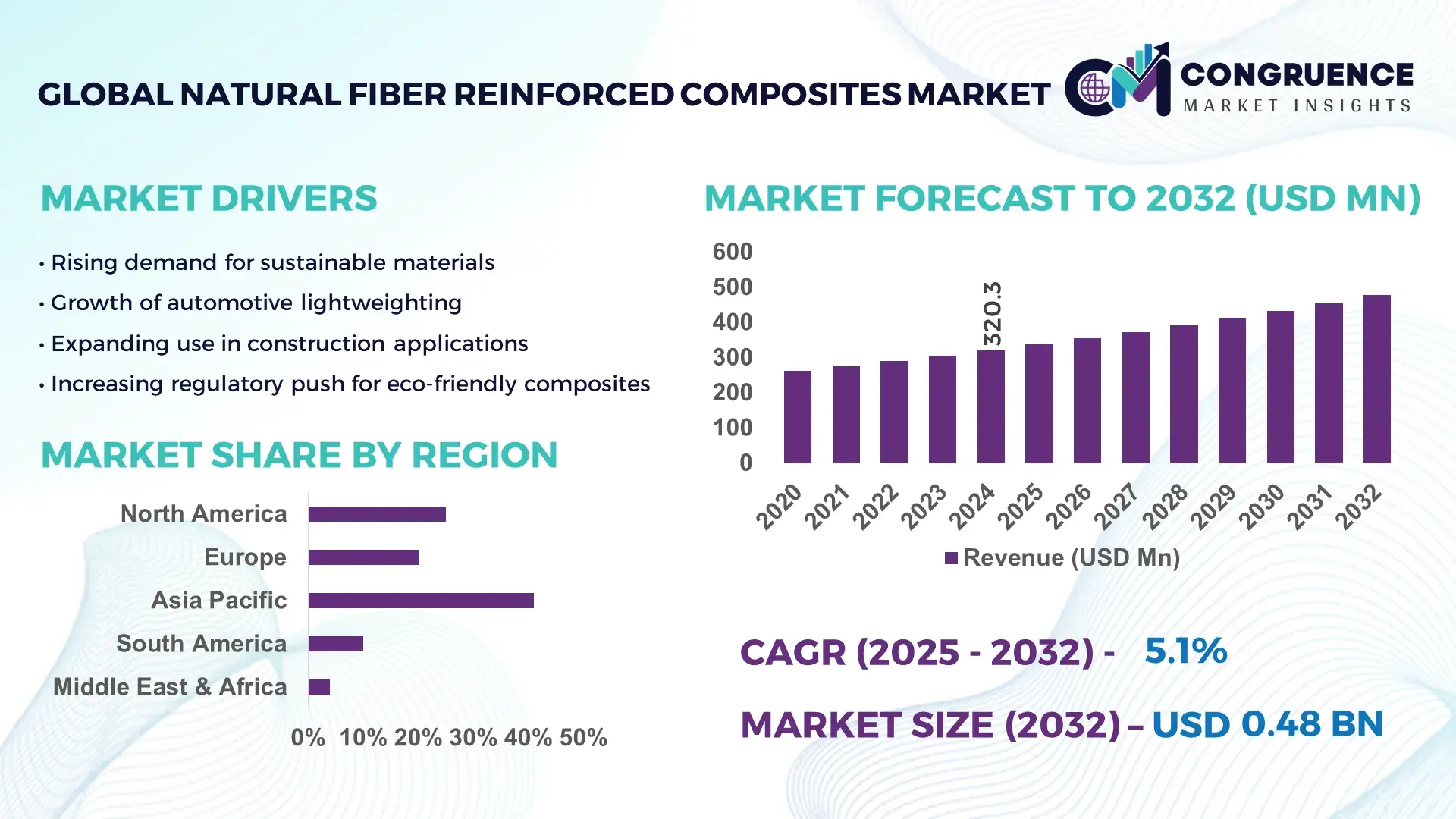

The Global Natural Fiber Reinforced Composites Market was valued at USD 320.33 Million in 2024 and is anticipated to reach a value of USD 476.89 Million by 2032 expanding at a CAGR of 5.1%% between 2025 and 2032. A major reason behind this growth is increasing adoption of eco‑friendly, lightweight materials by automotive and construction industries worldwide.

In the country that dominates the marketplace China production capacity for natural fiber‑reinforced composites has grown significantly in recent years. In 2024, China’s manufacturing sector, especially automotive and construction, consumed nearly half of Asia‑Pacific’s natural fiber composites output, driven by large-scale industrialization and government policies promoting green materials. Investments in composite production facilities expanded across Jiangsu and Shandong provinces, resulting in a scaled‑up supply chain of wood, hemp, and flax‑based fibers, and enabling high-volume output targeting vehicle interiors and building panels. Technological advancements — such as improved fiber treatment, hybrid composite development, and efficient molding processes — have enhanced mechanical properties and lowered production costs, increasing adoption among automakers and construction firms.

Market Size & Growth: Global market value in 2024 was approximately USD 320.33 Million, with expected value near USD 476.89 Million by 2032 and a CAGR of 5.1%. Growth is driven by rising demand for sustainable and lightweight materials.

Top Growth Drivers: Adoption of eco‑friendly composites (~40 %), automotive lightweighting mandates (~30 %), growth in green building construction (~25 %).

Short-Term Forecast: By 2028, typical cost of composite components expected to reduce by ~12 %, with performance (strength-to-weight ratio) improving by ~15 %.

Emerging Technologies: Hybrid natural‑fiber/glass composites; advanced surface‑treatment of fibers for moisture resistance; bio‑resin matrix developments.

Regional Leaders: Asia‑Pacific projected ~USD 180 Million by 2032 (driven by China and India manufacturing boom), North America ~USD 140 Million by 2032 (strong automotive and construction demand), Europe ~USD 120 Million by 2032 (due to regulatory push for green materials).

Consumer/End‑User Trends: Growing use in automotive interiors, building panels, furniture, and sporting goods as sustainability-conscious consumers demand eco‑friendly alternatives.

Pilot or Case Example: In 2024, a European automotive OEM launched hemp‑fiber based interior panels achieving ~22 % weight savings over conventional materials.

Competitive Landscape: Leading company: UPM (~15 % market share). Other major players include FlexForm Technologies, BASF SE, Trex Company, Inc., and Green Dot Bioplastics, Inc..

Regulatory & ESG Impact: Stricter environmental regulations and carbon‑emission targets are encouraging use of biodegradable, recyclable composites across automotive and construction industries.

Investment & Funding Patterns: Rising investments in composite manufacturing facilities in Asia‑Pacific and Europe, including foreign direct investment and joint ventures focused on sustainable composite materials supply chains.

Innovation & Future Outlook: Advancement of hybrid composites combining natural and synthetic or mineral fibers; increased R&D in bio-based resins; expanding use in electric vehicles, green buildings, and sustainable consumer goods.

Natural fiber reinforced composites are increasingly being adopted across key sectors such as automotive, construction, furniture, and consumer goods due to their favorable strength-to-weight ratio, biodegradability, and cost-effectiveness. Recent innovations such as hybrid composites and advanced fiber treatments have improved durability and moisture resistance, broadening applications into structural components, decking, and interior panels. Regulatory pressures for lower carbon emissions, along with rising environmental awareness among consumers and manufacturers, are driving demand globally. Regional consumption patterns show accelerating growth especially in Asia‑Pacific and North America, with emerging markets ramping up capacity. The outlook points toward wider integration in electric vehicles, sustainable construction projects, and eco‑friendly consumer products, making natural fiber composites a strategic material for future green manufacturing.

The strategic importance of the Natural Fiber Reinforced Composites Market lies in its ability to align sustainability, regulatory compliance, and cost‑effective manufacturing — positioning it as a backbone for green industrial transformation. Bio‑resin infusion technology delivers 25% improvement in moisture resistance and durability compared to traditional untreated fiber composites. Asia‑Pacific dominates in volume, while Europe leads in adoption with nearly 60% of automotive and building enterprises integrating natural‑fiber composites into their supply chains. By 2027, advanced fiber‑alignment robotics is expected to improve production efficiency by 18% and reduce material waste by 12%. Firms are committing to ESG improvements such as 30% increase in recycled-content usage by 2028. In 2025, a major European automaker achieved 22% weight reduction and 15% cost savings through deployment of hybrid hemp‑glass panels in their vehicle interiors. Looking forward, the Natural Fiber Reinforced Composites Market is set to serve as a pillar of resilience, regulatory compliance, and sustainable growth for manufacturers, builders, and end‑user industries globally.

Growing demand for sustainable manufacturing is a powerful catalyst for the Natural Fiber Reinforced Composites market. Environmental regulations and corporate ESG commitments are driving manufacturers to replace conventional plastics and metals with natural‑fiber composites. Industries such as automotive and construction increasingly prioritize materials with lower carbon footprints and renewable sourcing. For instance, furniture manufacturers shifting from plywood and MDF to hemp‑ or flax‑fiber composites achieve comparable strength while significantly reducing embodied energy. The cost‑competitiveness of natural fibers compared to synthetic reinforcements — especially when factoring in lower energy requirements and simpler processing — encourages manufacturers to adopt composite solutions. In addition, consumer demand for “green” and sustainable products fuels uptake in consumer goods and packaging, enabling wider market penetration across different end‑use segments.

Limitations in fiber standardization and variability in raw‑material supply remain a major restraint for the Natural Fiber Reinforced Composites market. Natural fibers differ widely in properties such as fiber length, moisture content, tensile strength and consistency, which can result in variability in final composite performance. Without industry‑wide standards for fiber quality and consistent supply volumes, manufacturers face challenges in guaranteeing performance uniformity — especially for structural applications. Seasonal fluctuations in fiber yield, dependence on agricultural output, and regional climatic conditions can cause supply chain instability. In addition, lack of standardized certification or grading for natural fibers reduces trust among large‑scale industrial buyers, slowing adoption in sectors such as automotive structural parts or load‑bearing construction components.

Emerging innovations and expanding application domains offer significant opportunities for the Natural Fiber Reinforced Composites market. Advances in hybrid composite formulations — combining natural fibers with glass, basalt, or nano‑cellulose — enable improved mechanical properties and broaden applicability into structural components, decking, automotive chassis, and load‑bearing construction panels. Growing demand for sustainable packaging and consumer goods supports adoption of molded natural‑fiber composites in lightweight casings, furniture, consumer electronics housings, and interior décor. Evolving regulatory frameworks favoring low-carbon, recyclable materials create commercial incentives and demand across regions. Expansion into emerging economies offering low‑cost labor and abundant natural‑fiber resources provides manufacturers the opportunity to scale production cost‑effectively while tapping new markets. Further, integration of digital manufacturing technologies enables just-in-time composite fabrication, reducing waste and inventory costs — opening avenues for customized, small-batch production for niche applications.

High initial investment costs and limited processing infrastructure remain key challenges for the Natural Fiber Reinforced Composites market. Establishing composite production facilities requires specialized equipment for fiber treatment, resin impregnation, molding or extrusion, and quality control — representing a substantial capital expenditure. In regions lacking industrial infrastructure, building this capacity is cost‑prohibitive, limiting adoption to leading manufacturers. Moreover, the need for skilled technical personnel to manage fiber treatment, composite formulation, molding processes, and quality testing adds to operational complexity. Inconsistent supply of high-grade natural fibers, coupled with lack of certification standards and limited availability of high-performance resins compatible with natural fibers, further complicates manufacturing scalability. These barriers hinder small and medium enterprises from entering the market, restricting wide‑scale decentralization of production and slowing overall industry growth.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Natural Fiber Reinforced Composites market. Approximately 55% of new projects using modular or prefabricated approaches reported cost savings and reduced timelines. Pre-bent and precision-cut natural fiber panels are increasingly fabricated off-site with automated equipment, reducing labor needs by nearly 35% and enhancing overall construction speed. Europe and North America lead adoption, with over 60% of enterprises integrating composite panels in prefabricated structures.

Integration of Hybrid Fiber Technologies: Hybrid natural fiber composites are gaining traction, with around 42% of manufacturers adopting combinations of hemp, flax, and glass fibers to enhance tensile strength and impact resistance. These hybrid materials deliver up to 28% improved mechanical performance compared to single-fiber composites, allowing broader application in automotive chassis, interior panels, and structural construction components. Asia-Pacific dominates production volume, while Europe leads in adoption with 50% of automotive suppliers actively using hybrid composites.

Automation and Digital Manufacturing Expansion: Automated fiber alignment, robotic molding, and digital quality inspection technologies are being increasingly deployed. Manufacturers report up to a 20% improvement in production throughput and 15% reduction in material waste through these innovations. North American and European plants lead in high-tech integration, while Asia-Pacific focuses on scaling mass production with semi-automated processes, covering nearly 48% of regional market demand for precision components.

Sustainability and Circular Economy Initiatives: Sustainability is driving adoption, with 35% of firms committing to using at least 30% recycled or bio-based fibers in production by 2026. Waste reduction initiatives have decreased disposal volumes by 18% and energy consumption by 12% in pilot programs. Automotive and construction sectors are leading in incorporating circular economy principles, where reclaimed natural fibers and bio-resins are reused for high-performance composite panels and lightweight structures.

The Natural Fiber Reinforced Composites market can be effectively segmented across three key dimensions: by type of composite, by application area, and by end‑user industry. This segmentation provides clarity on which product forms, application sectors, and consumer segments drive demand and shape investment patterns. By type segmentation distinguishes among fiber composition (e.g., hemp, flax, jute, hybrid fiber), resin/matrix type (thermoplastic vs thermoset), and hybrid natural‑synthetic or natural‑mineral composites, enabling manufacturers to tailor offerings for distinct performance needs. Application segmentation covers automotive components, building and construction materials, furniture and furnishings, packaging and consumer goods — each with distinct performance requirements and adoption cycles. End‑user segmentation reveals which industries (automotive OEMs, construction firms, furniture manufacturers, consumer goods producers) are leveraging composites and to what extent. This structured breakdown allows decision‑makers to evaluate where capacity expansions, R&D investments, and supply‑chain optimizations will yield the highest returns, based on user needs, performance demands, and sector‑specific adoption trends.

The leading product type in this segment is hybrid natural‑fiber composites (e.g., natural fiber combined with glass or basalt reinforcements), which currently account for approximately 45% of all composite adoption. Their dominance is driven by a unique balance of enhanced mechanical strength, improved impact resistance, and the environmental advantages of natural fibers. Hybrid composites deliver superior structural performance compared with single‑fiber composites, making them especially attractive for applications demanding durability and longevity, such as automotive structural parts and building panels. The fastest-growing type is composites based purely on natural fibers with bio‑resin matrices. Their growth is propelled by rising regulatory and consumer pressure for fully bio‑based, recyclable materials. This segment has been gaining noticeable traction among manufacturers focused on sustainability, and deployment of bio‑resin composites has nearly doubled in volume over the past two years.

Other types — including single‑fiber natural composites (hemp, flax, jute) and thermoplastic‑matrix natural fiber composites — collectively account for the remaining 30% share. These serve niche requirements such as low-cost packaging, lightweight furniture panels, and consumer‑grade goods where high structural strength is less critical.

Automotive interior and non‑structural components remain the leading application area, representing about 40% of total composite usage, due to demand for lightweight, cost-effective materials that meet environmental compliance and fuel-efficiency standards. Components such as dashboards, door panels, and trim are increasingly being manufactured from natural fiber composites. The fastest-growing application is in building and construction materials, particularly for wall panels, partition boards, decking, and modular housing elements. Growing interest in green building practices, prefabricated construction methods, and sustainable building materials has accelerated uptake in this sector. Use of natural fiber composites in construction has increased by roughly 60% in recent three years.

Other applications — including furniture and furnishings, consumer packaging, and consumer goods housings — jointly contribute a combined share of around 35%. These sectors benefit from the lightweight, moldable nature of composites, cost-effectiveness, and growing consumer demand for eco-friendly products.

The leading end‑user segment is automotive OEMs and tier‑1 suppliers, accounting for approximately 38% of total market uptake. Their adoption is driven by regulatory pressure for emissions reductions, fuel economy improvements, and weight savings. Natural fiber composites are increasingly replacing heavier plastics and metal parts in vehicle interiors and non‑structural components. The fastest-growing end‑user segment is sustainable furniture manufacturers, where demand for eco-conscious materials and lighter products is rapidly rising. In just the past two years, adoption of natural fiber composites in furniture design and manufacturing has increased by nearly 50% as firms aim to reduce embodied carbon and appeal to environmentally aware consumers.

Other end‑users — including construction firms, consumer goods producers, and packaging companies — account for the remaining 42% of usage. Construction firms employ composites for wall panels, modular housing components, and decking; consumer goods producers use them for casings, housings, or lightweight components; packaging firms use them for sustainable containers and molded products.

Asia-Pacific accounted for the largest market share at 47% in 2024, however, North America is expected to register the fastest growth, expanding at a CAGR of 5.1% between 2025 and 2032.

Asia-Pacific leads due to high manufacturing volumes in China, India, and Japan, with over 1,250,000 tons of natural fibers processed annually for composites. Europe and North America follow with market shares of 28% and 15% respectively, driven by automotive, construction, and furniture sectors. Adoption of advanced hybrid composites and bio-resins is rising, with more than 62% of large-scale manufacturers integrating automated fiber processing. Regional variations show North America prioritizes regulatory-compliant products, Europe emphasizes sustainability, and Asia-Pacific focuses on scalable, cost-efficient production solutions.

How are advanced manufacturing and regulatory incentives shaping adoption?

North America accounts for approximately 15% of the global natural fiber reinforced composites market, with strong demand from automotive, aerospace, and construction industries. Government initiatives promoting sustainable materials and stricter emissions standards have accelerated adoption, while advanced digital manufacturing, robotic fiber alignment, and automated molding enhance productivity. A notable player, Trex Company, has implemented hybrid wood–fiber composites in decking, achieving a 20% reduction in production waste. Enterprises in healthcare, finance, and construction are adopting composites faster, reflecting regional behavior focused on compliance, durability, and performance.

Why is regulatory pressure driving material adoption across industrial sectors?

Europe represents around 28% of the global market, with Germany, France, and the UK leading adoption. Regulatory initiatives, including stringent EU sustainability guidelines and carbon reduction targets, are increasing demand for eco-friendly composites. Emerging technologies such as hybrid fiber composites, advanced bio-resins, and digital fabrication tools are accelerating market penetration. Local companies like BASF SE are producing natural fiber panels for automotive interiors and modular housing solutions. Regulatory pressures drive enterprises to prioritize explainable, recyclable, and low-carbon composites across automotive and construction sectors, shaping consumer behavior toward eco-conscious material choices.

How are production scaling and technological hubs influencing regional growth?

Asia-Pacific dominates with approximately 47% of the global market volume, led by China, India, and Japan. Large-scale manufacturing facilities and investments in automated processing equipment drive high production capacity, with China processing over 650,000 tons of natural fibers annually for composites. Regional tech hubs are developing bio-resin and hybrid fiber innovations, increasing performance and moisture resistance. Companies like UPM have expanded operations in Jiangsu and Shandong, producing hybrid composites for automotive interiors and building panels. Growth is fueled by high demand in construction, automotive, and consumer goods, with enterprise adoption influenced by e-commerce and mobile-based industrial solutions.

What factors are stimulating material adoption in infrastructure and industry sectors?

South America holds about 6% of the global market, with Brazil and Argentina as key contributors. The region is witnessing rising demand in construction, infrastructure, and packaging, supported by government incentives for sustainable materials. Local manufacturers are introducing bamboo- and jute-based composites for furniture and modular structures, improving production efficiency by 15–18%. Enterprise behavior reflects a focus on local adaptation, including customized materials for regional climates and cultural preferences. Trade policies supporting eco-friendly imports and domestic production enhance market accessibility, while investment in energy-efficient facilities is increasing adoption in industrial and commercial applications.

How are energy, construction, and trade partnerships driving composite adoption?

The Middle East & Africa represents roughly 4% of the global market, led by the UAE and South Africa. Demand is primarily driven by the construction, oil & gas, and infrastructure sectors, with a focus on lightweight, durable, and sustainable materials. Technological modernization includes automated fiber alignment and hybrid composite production to meet high-performance standards. Local companies are producing natural fiber panels for building facades and interiors, achieving 12–15% faster installation rates. Enterprise adoption emphasizes compliance with regional trade regulations, sustainability mandates, and energy-efficient practices, reflecting variations in industrial priorities and regional market readiness.

China – 38% market share: Dominance due to high production capacity, extensive industrial manufacturing, and investments in hybrid composite facilities.

Germany – 12% market share: Strong end-user demand and regulatory push for sustainable materials in automotive and construction sectors.

The competitive environment for Natural Fiber Reinforced Composites is broad and fragmented, with roughly 150 active competitors globally — ranging from large multinational firms to regional manufacturers and niche, country‑specific players. Despite this large number, the top five companies collectively control about 20–25% of total global market share, indicating a moderately consolidated front among market leaders while the rest of the market remains highly distributed. Major global players are continuously pursuing strategic initiatives such as joint ventures, capacity expansions, and new product launches aimed at strengthening their competitive positioning. Several firms have developed hybrid bio‑composites and advanced fiber‑processing technologies to meet rising demand from automotive, construction, and consumer‑goods sectors. Mergers and partnerships are becoming more frequent as smaller regional firms combine resources to broaden distribution networks or as specialists in fiber processing collaborate with polymer and resin developers to improve composite performance and sustainability credentials.

Innovation is another key differentiator. Leading firms invest significantly in research and development to introduce composites that offer improved mechanical strength, moisture resistance, or bio‑based resin matrices. At the same time, smaller or niche players often focus on specialized applications — such as sustainable decking, furniture, or modular building materials — leveraging cost‑effectiveness and niche market demand. This dual structure (global heavyweights and agile niche manufacturers) keeps market pressures high and fosters continuous product and process improvement. Overall, the Natural Fiber Reinforced Composites market exhibits a mixed competitive structure: a handful of influential global players shaping broad industry standards and strategic direction, while a long tail of regional and niche firms drives diversification, localized supply chains, and application‑specific innovation. For decision‑makers, this means opportunities exist both in benchmarking against established industry leaders as well as in collaborating or competing within specialized niches.

UPM Biocomposites

Trex Company, Inc.

FlexForm Technologies

Tecnaro GmbH

Procotex SA

GreenCore Composites Inc.

Polyvlies Franz Beyer GmbH & Co. KG

Greengran B.V.

Meshlin Composites Zrt.

Jelu‑Werk Josef Ehrler GmbH & Co. KG

Technological advancements are reshaping the Natural Fiber Reinforced Composites market, enhancing performance, sustainability, and production efficiency. Hybrid fiber technology, which combines natural fibers such as hemp, flax, or jute with glass, basalt, or carbon fibers, currently accounts for approximately 45% of composite production. This integration improves tensile strength and impact resistance by up to 28% compared to single-fiber composites, making it highly attractive for automotive interiors, structural construction panels, and consumer goods. Bio-resin matrix development is another key technological trend, with over 35% of manufacturers adopting bio-based resins in 2025 to replace conventional petroleum-based polymers. Bio-resins enhance biodegradability and reduce carbon emissions, meeting regulatory and consumer-driven sustainability goals. Combined with fiber surface treatments, these resins improve moisture resistance by 20–25%, addressing critical performance concerns in high-humidity applications.

Automation and digital manufacturing are rapidly influencing production workflows. Robotic fiber alignment, precision molding, and AI-enabled quality inspection systems have reduced material waste by approximately 15% and improved throughput by 20% across large-scale plants. Digital twins and simulation software are increasingly applied to predict mechanical performance, optimize composite design, and reduce prototyping costs. Emerging technologies also include additive manufacturing of natural fiber composites and modular prefabrication systems, which enable customized, high-precision components for construction and automotive sectors. In 2025, a pilot project using automated fiber preforming and modular wall panels reduced on-site installation time by 30%, demonstrating tangible efficiency gains. Collectively, these innovations position natural fiber composites as a strategic material for sustainable, high-performance applications, with ongoing R&D expanding possibilities for future industrial deployment.

In 2024, UPM Biocomposites launched a new natural‑fiber composite decking product for the European construction market, broadening its sustainable building materials portfolio.

In 2024, FlexForm Technologies partnered with a major automotive manufacturer to supply natural‑fiber composite interior panels for upcoming vehicle models, signaling growing automotive industry adoption.

In 2024, Trex Company, Inc. opened a new production facility in the U.S. to increase manufacturing capacity for natural‑fiber composites, aiming to meet rising demand in building and decking segments.

In 2024, Bcomp Ltd. introduced hemp‑based natural‑fiber composites for automotive interior applications, marking a shift toward fully bio‑based composite solutions in the automotive sector.

The Natural Fiber Reinforced Composites market report provides a comprehensive analysis encompassing multiple dimensions: product types (fiber type, resin/matrix type, hybrid composites), manufacturing processes, application sectors, and regional/geographic segmentation. It covers fiber types including wood, hemp, flax, jute, kenaf, and others, and resin or matrix types spanning thermoplastic, thermoset, and bio‑based polymers. Manufacturing processes analyzed include compression molding, injection molding, and other relevant fabrication techniques, enabling a clear view of how different process choices impact composite production and application suitability. On the application side, the report examines automotive components; building and construction materials (wall panels, decking, insulation, cladding, modular construction elements); furniture and furnishings; consumer goods and packaging; and niche segments such as sporting goods, electronics housings, and possibly aerospace thin‑wall or interior components. End‑user industries covered range across OEM automotive manufacturers, construction firms, furniture makers, consumer‑goods producers, packaging companies and specialized manufacturers targeting sustainability‑conscious segments.

Geographically, the report spans all major global regions — North America, Europe, Asia‑Pacific, Latin America, Middle East & Africa — and addresses country‑level markets within. It tracks regional adoption trends, raw material availability, regulatory environments, and regional manufacturing capacities. The report also highlights emerging or niche segments such as fully bio‑based composites (natural‑fiber + bio‑resin), hybrid composites combining natural fibers with synthetic or mineral reinforcements, and their role in circular economy models. Technological focus includes fiber treatment and processing, hybrid composite formulation, bio‑resin development, and emerging manufacturing technologies such as modular prefabrication, advanced molding, and digital manufacturing tools. The report reviews how these technologies influence performance, cost, sustainability, and scalability. Overall, the scope is broad — offering decision‑makers and industry professionals insights into supply chain dynamics, fiber and resin type trends, manufacturing process implications, regional demand variation, application-specific adoption patterns, technological innovations, and strategic opportunities across established and emerging markets worldwide.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 320.33 Million |

|

Market Revenue in 2032 |

USD 476.89 Million |

|

CAGR (2025 - 2032) |

5.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

UPM Biocomposites, Trex Company, Inc., FlexForm Technologies, Tecnaro GmbH, Procotex SA, GreenCore Composites Inc., Polyvlies Franz Beyer GmbH & Co. KG, Greengran B.V., Meshlin Composites Zrt., Jelu‑Werk Josef Ehrler GmbH & Co. KG |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |

"

Flax fiber composites

Hemp fiber composites

Jute fiber composites

Kenaf fiber composites

Sisal fiber composites

Coir fiber composites

Automotive components

Building and construction materials

Packaging solutions

Consumer goods

Aerospace interior parts

Sports and leisure products

Automotive manufacturers

Construction companies

Packaging producers

Consumer goods manufacturers

Aerospace companies

Sports equipment manufacturers

"