Reports

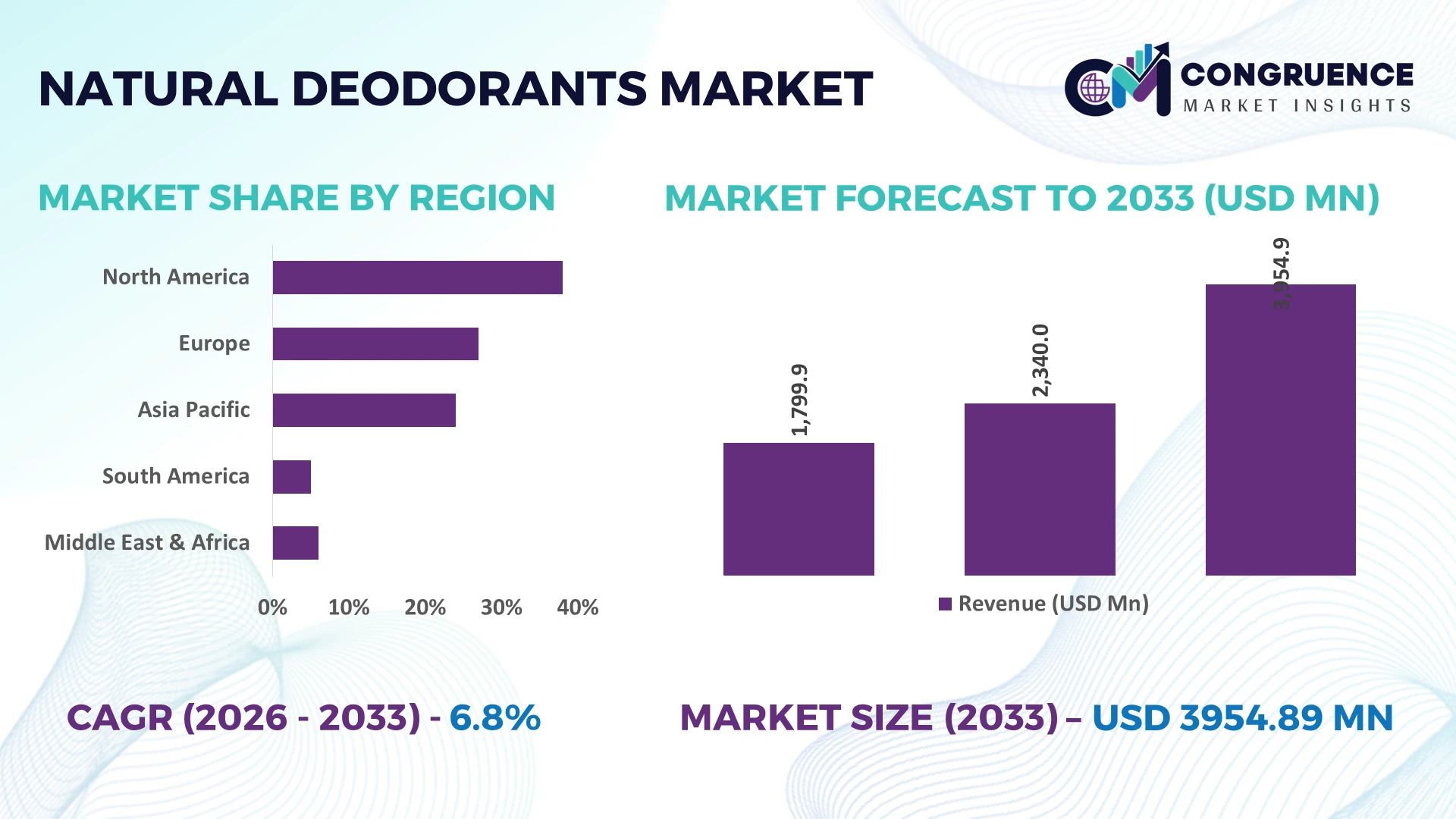

The Global Natural Deodorants Market was valued at USD 2340 Million in 2025 and is anticipated to reach a value of USD 3954.89 Million by 2033 expanding at a CAGR of 6.78% between 2026 and 2033. Growth is being driven by aluminum-free formulations, microbiome-friendly ingredients, clean-label personal care innovation, and expanding retail penetration of plant-based deodorant products across premium and mass-market channels.

The United States remains the dominant country, accounting for approximately 34% of global natural deodorant consumption, supported by strong clean beauty adoption, over USD 500 million in annual category investments, and advanced product development across personal care brands. Compared with Germany, where natural personal care penetration exceeds 18% of beauty product sales, U.S. manufacturers deploy around 25% more product innovation cycles annually. Growing consumer scrutiny of ingredient transparency following tightening sustainability and packaging regulations across North America and Europe continues to accelerate adoption of certified natural formulations.

Companies prioritizing ingredient traceability, sustainable packaging integration, and premium retail expansion are positioned to secure stronger market share gains in the evolving natural deodorants landscape.

Market Size & Growth: USD 2340 Million in 2025, reaching USD 3954.89 Million by 2033 at 6.78% CAGR, supported by rapid expansion of aluminum-free and clean-label product portfolios.

Top Growth Drivers: Natural ingredient preference (+42%), sustainable packaging adoption (+31%), and premium personal care penetration (+27%) remain the three strongest growth catalysts.

Short-Term Forecast: By 2028, manufacturing efficiency improves by 14% through automated filling systems and optimized ingredient sourcing networks.

Emerging Technologies: AI-driven formulation design, microbiome-focused ingredients, and advanced biodegradable packaging reduce development cycles by approximately 18%.

Regional Leaders: North America exceeds USD 1.4 billion, Europe approaches USD 1.1 billion, and Asia-Pacific surpasses USD 850 million, supported by rising clean-beauty adoption.

Consumer/End-User Trends: Nearly 58% of premium personal care consumers actively seek deodorants free from aluminum, parabens, and synthetic fragrances.

Pilot/Case Example: In 2025, a large-scale packaging optimization initiative reduced material usage by 16% while improving distribution efficiency by 11%.

Competitive Landscape: Leading brands collectively control nearly 38% market share, with competition intensifying across premium and direct-to-consumer channels.

Regulatory & ESG Impact: Sustainable packaging mandates and waste-reduction targets lowered packaging material intensity by approximately 12% across major manufacturers.

Investment & Funding: More than USD 650 million has been directed toward facility expansion, product innovation, and strategic partnerships amid supply-chain diversification.

Innovation & Future Outlook: Refillable formats, probiotic deodorants, and waterless formulations are reshaping product strategy and accelerating global category differentiation.

Natural Deodorants Market demand is expanding across personal care retail, e-commerce, wellness-focused consumer segments, and premium beauty channels. Product innovation increasingly centers on probiotic ingredients, odor-neutralizing mineral complexes, and refillable packaging systems. More than 40% of new product launches emphasize sustainable formulations and packaging efficiency. Ongoing packaging regulations and ingredient transparency requirements are strengthening operational standards, setting the stage for deeper strategic evaluation across the competitive landscape.

Natural deodorants have evolved from a niche wellness category into a strategically important segment within personal care portfolios, driven by ingredient transparency requirements, premiumization, and sustainability-led product differentiation. Competitive intensity is increasing as multinational brands and emerging clean-beauty companies compete for shelf space and direct-to-consumer channels. A notable market shift is the restructuring of botanical ingredient supply chains, with manufacturers reducing dependence on single-origin sourcing and improving procurement resilience. More than 55% of new product launches now emphasize natural certification, refillability, or sensitive-skin positioning, reinforcing long-term category relevance.

Technology integration is improving formulation efficiency and production consistency. AI-assisted ingredient screening reduces product development cycles by approximately 20% compared with traditional trial-and-error formulation methods, while automated filling systems lower packaging waste by nearly 15%. The United States leads in product commercialization and retail penetration, whereas Germany demonstrates stronger adoption of certified natural personal care standards. A practical example includes manufacturers deploying refillable deodorant systems that reduce packaging material consumption while strengthening customer retention through subscription-based replenishment models.

Over the next two to three years, adoption of microbiome-friendly formulations and recyclable packaging formats is expected to expand across mainstream retail networks. Companies are increasing investments in ingredient traceability, strategic supplier partnerships, and regional manufacturing capabilities. Organizations that combine formulation innovation, supply-chain resilience, and sustainability execution will secure stronger competitive positioning and long-term operational advantage.

The primary growth driver is the accelerating shift toward clean-label and aluminum-free personal care products. More than 60% of premium beauty consumers actively review ingredient lists before purchase, while natural-certified product launches have increased by over 30% during the past three years. Regulatory scrutiny surrounding ingredient disclosure and packaging sustainability is reinforcing this transition. In the United States, retailers are allocating larger shelf space to natural personal care categories, improving product visibility and conversion rates. The direct impact is stronger demand for plant-derived actives, probiotic formulations, and refillable packaging solutions. In response, companies are expanding manufacturing capacity, forming partnerships with botanical ingredient suppliers, and investing in formulation innovation. A notable strategic insight is that ingredient transparency is increasingly functioning as a competitive differentiator rather than solely a compliance requirement.

Supply-chain dependence on natural oils, plant extracts, and specialty fragrance ingredients remains a significant structural limitation. Prices for selected botanical inputs can fluctuate by 15–25% annually due to climate variability, agricultural yield disruptions, and logistics constraints. Manufacturers in countries dependent on imported natural ingredients face additional procurement risks and extended lead times. These pressures directly affect production planning, inventory management, and gross-margin stability. Packaging costs have also increased as brands transition toward recyclable and refillable formats. To mitigate these challenges, companies are diversifying supplier networks, localizing ingredient sourcing where feasible, and negotiating long-term procurement agreements. A key operational insight is that supply-chain resilience increasingly influences profitability as much as brand positioning within the natural deodorants category.

A significant opportunity lies in microbiome-friendly deodorants, refill ecosystems, and advanced natural odor-control technologies. Consumer interest in skin-health-focused personal care has increased by approximately 35%, while refillable product adoption in premium beauty categories has surpassed 20% in several developed markets. Emerging formulation technologies using probiotic cultures and enzyme-based odor neutralization provide measurable performance improvements without synthetic compounds. Japan and South Korea are becoming important innovation hubs for functional natural personal care products, creating partnership and licensing opportunities. Companies are strengthening R&D programs, expanding into subscription-based refill models, and building ecosystems around sustainability-focused consumer engagement. A less obvious opportunity is the operational cost reduction achieved through concentrated and water-efficient formulations, which lower transportation and packaging intensity while supporting premium pricing strategies.

Maintaining consistent efficacy while scaling production remains a major execution challenge. Approximately 40% of consumer complaints within natural personal care categories relate to performance variability, longevity, or sensory characteristics. Unlike synthetic formulations, natural ingredient profiles can vary based on harvest conditions, origin, and processing methods, creating quality-control complexities. Regulatory requirements for ingredient verification and sustainability claims are also becoming more stringent across key consumer markets. These factors affect deployment consistency, brand credibility, and long-term customer retention. Companies must invest in advanced testing protocols, formulation standardization technologies, and digital quality-monitoring systems to address these issues. A critical strategic insight is that future market leaders will differentiate through manufacturing precision and verified product performance rather than relying solely on natural ingredient positioning.

Refill Systems Gain Momentum: Refillable deodorant formats are expanding rapidly, with packaging material usage declining by 20–30% per unit and repeat purchase rates improving by nearly 25%. Sustainability regulations and retailer waste-reduction targets are accelerating deployment across the United States and Germany. Companies are restructuring packaging supply chains, securing aluminum and recycled-material partnerships, and integrating subscription refill programs to lower logistics costs while strengthening customer retention.

Microbiome Science Reshapes Formulation: Products incorporating probiotics, prebiotics, and microbiome-supporting ingredients have increased by more than 35% in new product pipelines. Clinical testing efficiency has improved by approximately 15% through digital formulation analytics, while sensitive-skin product adoption has expanded by over 20%. Manufacturers are partnering with biotechnology firms to commercialize differentiated odor-control solutions that improve performance without relying on conventional active ingredients.

Retail Data Drives Product Development: Consumer analytics platforms now influence over 40% of new product launch decisions, reducing product development timelines by nearly 18%. Digital demand tracking enables brands to identify ingredient preferences, fragrance trends, and regional purchasing behavior more precisely. Companies are deploying AI-supported forecasting systems and integrating retailer data streams to optimize inventory allocation and reduce stock imbalances.

Localized Sourcing Expands Resilience: Supply-chain disruptions and climate-related agricultural variability have encouraged brands to localize sourcing strategies. More than 30% of manufacturers have diversified botanical ingredient procurement networks, reducing lead-time exposure by approximately 12%. A notable shift involves regional ingredient processing partnerships, allowing faster formulation adjustments and improved production continuity while supporting stricter traceability requirements.

Stick deodorants remain the leading segment, accounting for an estimated 42% of total category volume due to superior portability, lower packaging complexity, and efficient retail distribution. Their scalable manufacturing processes and strong shelf stability make them attractive for mass-market and premium brands alike. Companies continue investing in aluminum-free stick formulations, biodegradable packaging, and fragrance customization to strengthen market positioning. Roll-On products maintain relevance through precise application and growing acceptance in Europe, while Spray formats benefit from convenience-oriented consumers seeking rapid application and lightweight textures.

Cream deodorants represent the fastest-growing type, supported by increasing demand for concentrated formulations and sensitive-skin compatibility. Adoption has expanded by approximately 18% over the last two years as consumers prioritize ingredient transparency and multifunctional skincare benefits. Gel formulations are also gaining traction through quick-drying properties and premium positioning. Manufacturers are broadening product portfolios through targeted innovation, while investment priorities increasingly favor high-performance natural formulations that combine efficacy, skin compatibility, and sustainability advantages. The shift indicates growing preference for differentiated products rather than traditional mass-market formats alone.

Personal Care remains the dominant application segment, representing nearly 50% of product utilization due to routine hygiene adoption, broad demographic reach, and strong retail availability. Demand concentration is supported by increasing preference for clean-label daily grooming products and wider product accessibility through online and offline channels. Daily Use applications closely follow, benefiting from rising replacement frequency and growing awareness of ingredient transparency. Companies are expanding production capabilities and improving inventory planning to support sustained consumption patterns across mainstream consumer groups.

Sensitive Skin Care is emerging as the fastest-growing application, with adoption increasing by approximately 22% as consumers seek fragrance-free and dermatologist-focused solutions. Sports & Fitness applications are also expanding due to active lifestyle trends and performance-oriented product positioning, while Travel Use products benefit from compact packaging innovation and airport-compliant formats. Manufacturers are introducing specialized product lines, enhancing formulation testing, and deploying targeted marketing strategies to capture these evolving use cases. Demand is increasingly shifting toward application-specific solutions that address functional performance requirements rather than generalized odor protection alone.

Women remain the largest end-user segment, accounting for approximately 48% of category demand due to higher engagement with clean beauty products, premium personal care spending, and ingredient-conscious purchasing behavior. Product variety, fragrance innovation, and sustainability preferences continue to strengthen demand concentration within this group. Men represent a significant and expanding segment as natural grooming adoption rises, supported by targeted product launches and broader retail availability. Companies are increasing investment in gender-specific branding and performance-focused product differentiation to strengthen market penetration.

Health-Conscious Consumers are the fastest-growing end-user category, with adoption increasing by nearly 24% as wellness-oriented purchasing decisions influence personal care routines. Athletes are driving demand for long-lasting odor-control formulations, while Teenagers increasingly favor natural alternatives aligned with social media-driven ingredient awareness. Manufacturers are responding through customized formulations, influencer partnerships, and premium product ecosystems that address distinct consumer priorities. Future demand is shifting toward functional benefits, transparency, and lifestyle alignment, encouraging companies to diversify portfolios and refine customer segmentation strategies.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.1% between 2026 and 2033.

Premium Personal Care Innovation Leadership

North America maintains the largest share of the natural deodorants market due to strong clean-label product adoption, mature retail infrastructure, and extensive direct-to-consumer distribution networks. The region contributes approximately 38% of global demand, supported by advanced product formulation capabilities and high consumer awareness of ingredient transparency. More than 60% of premium personal care launches in the United States now emphasize natural, aluminum-free, or sustainable positioning. Retailers continue expanding shelf allocation for certified natural products, while brands are investing in refillable packaging systems and localized ingredient sourcing. Strategic partnerships between manufacturers and specialty ingredient suppliers are improving formulation consistency and accelerating commercialization timelines.

United States Market Outlook: The United States remains the regional growth engine due to its advanced personal care manufacturing ecosystem and strong consumer preference for clean beauty products. Over 65% of natural deodorant purchases occur through omnichannel retail platforms, enabling rapid product testing and market scaling. Brands are increasing investment in microbiome-focused formulations, sustainable packaging technologies, and automated production systems to strengthen competitive differentiation and improve operational efficiency.

Regulation-Driven Sustainability Transformation

Europe represents a highly developed market characterized by stringent ingredient standards, sustainability regulations, and strong demand for certified natural personal care products. The region accounts for approximately 29% of global consumption and demonstrates high adoption of environmentally responsible packaging formats. More than 40% of newly launched natural deodorant products in key European markets incorporate recyclable or refillable packaging systems. Manufacturers are modernizing production facilities and expanding botanical ingredient procurement partnerships to support compliance requirements. Regulatory alignment across major markets is accelerating adoption of traceability systems and transparent product labeling practices.

Germany Market Outlook: Germany serves as the regional benchmark for natural personal care adoption due to strong consumer awareness and a mature organic products ecosystem. Natural and organic beauty products represent a significant share of premium personal care sales, encouraging continued product innovation. German manufacturers are investing in low-impact packaging technologies and advanced formulation research, while retailers increasingly prioritize verified sustainability credentials within personal care procurement strategies.

Manufacturing Scale and Consumer Expansion

Asia-Pacific is emerging as the fastest-expanding market, supported by rising disposable income, urbanization, and growing awareness of natural personal care solutions. The region accounts for nearly 23% of global demand and benefits from extensive manufacturing infrastructure and ingredient processing capabilities. More than 30% of new personal care production investments announced across key Asian markets are focused on clean-label and sustainable product categories. Local and international brands are increasing distribution reach through digital commerce platforms and specialized wellness retail channels. Manufacturing modernization initiatives are improving production flexibility and accelerating product launches.

China Market Outlook: China remains the most strategically important market due to its large consumer base, advanced manufacturing capacity, and expanding premium personal care sector. Digital commerce contributes significantly to product discovery and customer acquisition, supporting rapid adoption of natural formulations. Domestic manufacturers are increasing investment in plant-based ingredient innovation and automated production technologies, while multinational brands continue expanding localized product portfolios to align with evolving consumer preferences.

Growing Preference for Botanical Formulations

South America is experiencing steady market development driven by increasing awareness of natural personal care products and strong availability of botanical raw materials. The region contributes approximately 6% of global demand and benefits from established agricultural supply chains supporting natural ingredient production. Manufacturers are investing in regional sourcing networks and localized packaging operations to reduce procurement risk and improve cost control. Consumer preference for plant-derived formulations continues to strengthen, although infrastructure limitations and logistics variability remain operational considerations. Product accessibility through pharmacy and specialty retail channels is expanding steadily.

Brazil Market Outlook: Brazil leads regional activity through its large beauty and personal care industry, extensive biodiversity resources, and strong domestic manufacturing capabilities. Local companies are leveraging naturally derived ingredients to develop differentiated product offerings while improving vertical integration across sourcing and production operations. Growth in premium personal care categories is encouraging additional investment in sustainable packaging solutions and advanced formulation technologies to enhance competitiveness.

Retail Modernization and Wellness Investment

The Middle East & Africa market is benefiting from expanding retail infrastructure, premium personal care adoption, and growing consumer interest in wellness-oriented products. The region accounts for roughly 4% of global demand, with market activity concentrated in major urban centers. Modern retail expansion and digital commerce platforms are improving product availability and supporting category awareness. Manufacturers are forming distribution partnerships and introducing premium natural formulations tailored to local climate and consumer preferences. Investment in retail modernization initiatives is strengthening market accessibility while supporting long-term category development.

United Arab Emirates Market Outlook: The United Arab Emirates serves as a strategic hub for premium personal care distribution and product innovation across the region. Advanced retail infrastructure, strong consumer purchasing power, and growing wellness-focused spending support natural deodorant adoption. More than 50% of premium personal care product launches in major metropolitan retail channels now emphasize clean-label or sustainability-focused positioning, encouraging continued investment from both domestic and international brands.

The market is led by Native, Schmidt’s, Tom’s of Maine, Salt & Stone, Each & Every, and Crystal, with global clean-beauty brands competing directly against specialist natural deodorant innovators. The top five players collectively control approximately 42% of market activity, creating competition between scale-driven brands and premium formulation specialists. Competition centers on ingredient transparency, product efficacy, packaging innovation, and retail penetration. Brands using refillable systems report packaging reductions of 20–30%, while automated formulation and production processes improve development efficiency by nearly 15%. Companies are expanding through retailer partnerships, microbiome-focused product innovation, and localized ingredient sourcing strategies. Vertical integration is increasing as manufacturers secure botanical supply chains to reduce procurement volatility and improve quality consistency. The competitive shift is moving from basic aluminum-free positioning toward performance validation, sustainability credentials, and differentiated skin-health benefits. The primary entry barrier remains formulation credibility and distribution access. Winning requires proven efficacy, resilient sourcing networks, strong retail execution, and continuous product innovation.

Native

Schmidt’s

Tom’s of Maine

Crystal

Salt & Stone

Each & Every

Green Tidings

PiperWai

Kopari Beauty

Corpus Naturals

Pretty Frank

Ursa Major

Dr. Hauschka

Weleda AG

Natural deodorant manufacturers are increasingly deploying AI-assisted formulation platforms, automated batching systems, and digital quality-control technologies to improve product consistency and speed. AI-supported ingredient screening reduces formulation development time by approximately 18%, while automated production lines improve manufacturing efficiency by nearly 12%. More than 45% of premium natural personal care brands now use digital product-testing workflows to accelerate commercialization. These technologies help companies reduce reformulation cycles, improve ingredient compatibility analysis, and strengthen operational scalability in highly competitive retail environments.

Emerging technologies are centered on microbiome-based formulations, enzyme-driven odor neutralization, and advanced refillable packaging systems. Microbiome-focused deodorants demonstrate up to 20% better odor-management performance than conventional plant-based formulations, while refill systems reduce packaging material consumption by 25–30%. Adoption of refillable and reusable packaging formats has surpassed 30% among leading sustainability-focused brands. Companies are integrating biotechnology partnerships with packaging innovation programs to improve product differentiation, strengthen consumer retention, and reduce material dependency across supply chains.

Disruptive innovation is shifting toward precision skin-health analytics and bioengineered active ingredients. Compared with traditional trial-and-error formulation methods, AI-enabled product development improves research productivity by nearly 22%. Brands investing in biotechnology and personalized deodorant solutions gain a measurable competitive advantage through superior efficacy and faster product launches. Between 2026 and 2028, wider deployment of predictive formulation platforms and next-generation odor-control technologies will redefine performance standards, making early technology adoption increasingly important for market leadership.

January 2025 – Native launched a limited-edition deodorant collection through an exclusive retail partnership with Target, expanding multi-category product visibility across national distribution channels. The collaboration introduced multiple fragrance variants and strengthened retail penetration within high-traffic consumer segments. Source: nasdaq.com

April 2025 – Wild Cosmetics was acquired by Unilever, accelerating access to broader distribution networks and product development resources. Wild had previously reported 77% annual sales growth, highlighting the strategic value of refillable natural deodorant platforms within premium personal care portfolios. Source: theguardian.com

November 2025 – Wild introduced a refillable roll-on deodorant featuring a reusable aluminum case and bio-based compostable refill pack. The launch expanded circular packaging deployment and strengthened low-waste product positioning within the United Kingdom personal care market. Source: packagingworld.com

February 2026 – Dr. Squatch expanded its deodorant portfolio with Invisible Glide and Spray Deodorants after internal research showed nearly 90% of surveyed men expressed interest in non-staining natural deodorant alternatives. The launch strengthens performance-focused innovation and category differentiation.

This report provides a comprehensive assessment of the natural deodorants market across key product types including Stick, Roll-On, Spray, Cream, and Gel formulations. The analysis evaluates demand patterns across Personal Care, Sports & Fitness, Sensitive Skin Care, Daily Use, and Travel Use applications, alongside end-user segments such as Men, Women, Teenagers, Athletes, and Health-Conscious Consumers. The study examines adoption trends, product innovation intensity, distribution evolution, and competitive positioning across major global markets. More than 40% of recent product launches emphasize sustainability, refillability, or microbiome-focused formulations, reflecting ongoing technological transformation.

The report further covers North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting operational dynamics, manufacturing developments, and country-level strategic opportunities. It analyzes emerging technologies including AI-assisted formulation design, advanced odor-neutralization systems, and sustainable packaging innovations. The research supports investment planning, expansion strategy development, partnership evaluation, portfolio optimization, and competitive benchmarking while identifying high-priority growth pockets and operational trends expected to influence market direction between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 2340 Million |

Market Revenue in 2033 | USD 3954.89 Million |

CAGR (2026 - 2033) | 6.78% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Native, Schmidt’s, Tom’s of Maine, Crystal, Salt & Stone, Each & Every, Green Tidings, PiperWai, Kopari Beauty, Corpus Naturals, Pretty Frank, Ursa Major, Dr. Hauschka, Weleda AG |

Customization & Pricing | Available on Request (10% Customization is Free) |