Reports

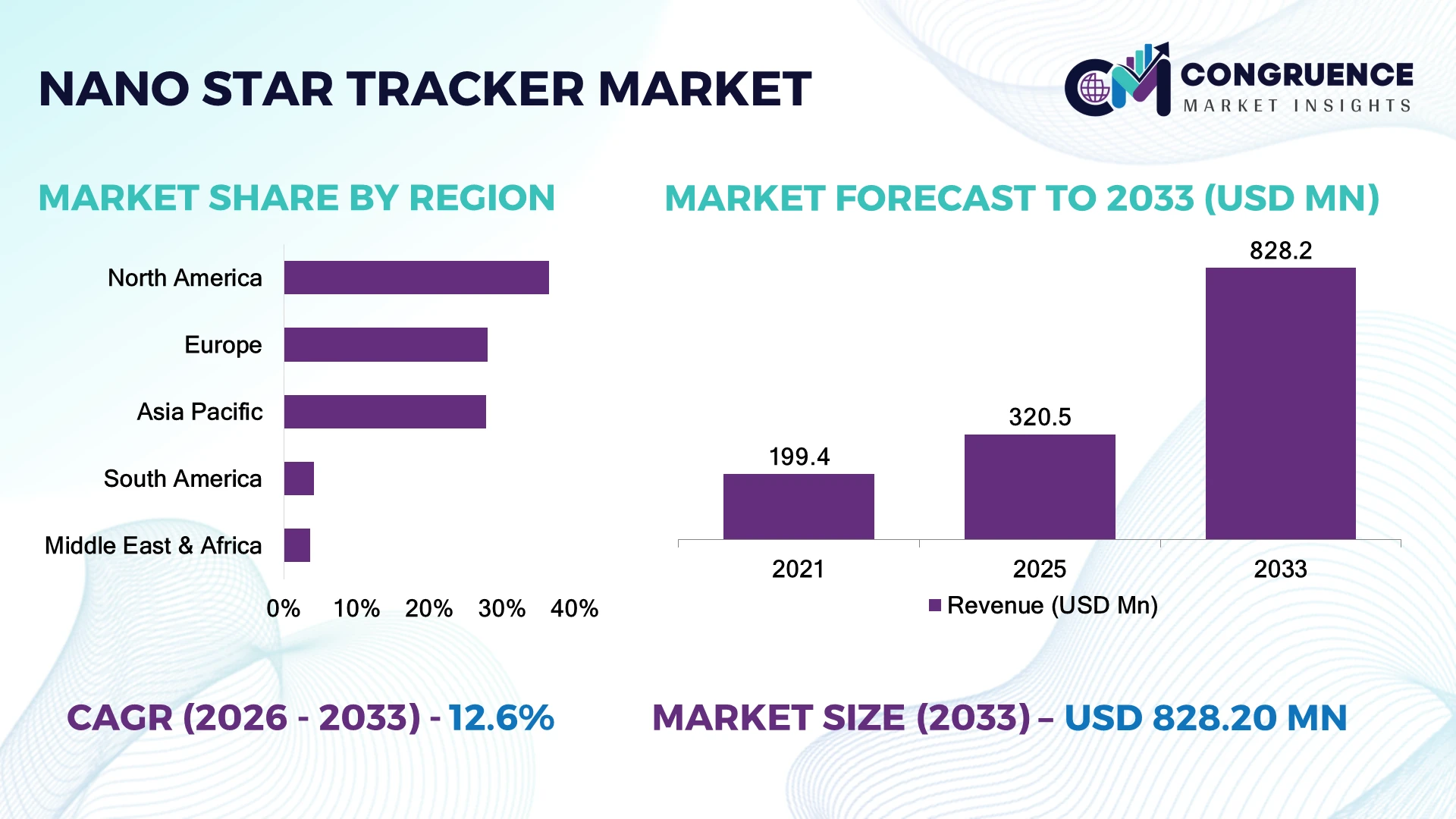

The Global Nano Star Tracker Market was valued at USD 320.5 Million in 2025 and is anticipated to reach a value of USD 828.2 Million by 2033 expanding at a CAGR of 12.6% between 2026 and 2033. Growth is being driven by increasing nanosatellite deployments, higher demand for autonomous spacecraft attitude determination, and rapid adoption of precision optical navigation systems across commercial and defense space missions.

The United States leads the Nano Star Tracker Market with approximately 37% of global small satellite manufacturing capacity, supported by investments exceeding USD 15 billion in commercial space, defense, and satellite technologies. Compared with Luxembourg, the United States delivers significantly larger satellite deployment volumes, while Luxembourg maintains strong specialization in commercial space infrastructure. Ongoing geopolitical competition in space capabilities continues accelerating domestic satellite manufacturing and component localization.

Strategic investment in compact optical navigation technologies and resilient aerospace supply chains is becoming essential for sustaining competitive leadership.

Market Size & Growth: Valued at USD 320.5 Million in 2025 and projected to reach USD 828.2 Million by 2033 at a CAGR of 12.6%, supported by accelerating nanosatellite deployment and autonomous spacecraft navigation.

Top Growth Drivers: Small satellite launches (+33%), defense space programs (+24%), and Earth observation missions (+19%) strengthen market demand.

Short-Term Forecast: By 2028, onboard attitude determination accuracy improves by 18%, while calibration time declines by approximately 14%.

Emerging Technologies: AI-enabled image processing, radiation-hardened sensors, and miniaturized optics improve tracking efficiency by nearly 21%.

Regional Leaders: North America exceeds USD 285 Million, Europe approaches USD 210 Million, and Asia-Pacific surpasses USD 240 Million through expanding satellite programs.

Consumer/End-User Trends: Nearly 49% of nanosatellite manufacturers prioritize integrated star tracker solutions for autonomous navigation.

Pilot/Case Example: A 2026 satellite validation mission improved pointing accuracy by 17% while reducing onboard processing requirements by 13%.

Competitive Landscape: The top five suppliers control approximately 58% market share, led by Blue Canyon Technologies, ARCSEC, NewSpace Systems, Sodern, and Tensor Tech.

Regulatory & ESG Impact: Space debris mitigation initiatives improve mission planning efficiency by approximately 12% through higher navigation precision.

Investment & Funding: Industry investments exceed USD 2.4 Billion, supported by satellite constellation expansion, defense contracts, and regional manufacturing growth.

Innovation & Future Outlook: AI-assisted navigation, compact CMOS imaging, and edge-based spacecraft processing are redefining next-generation space mission capabilities.

Nano star trackers are becoming indispensable for CubeSats, Earth observation platforms, and defense satellites where high-precision attitude determination directly improves mission performance. Miniaturized optical sensors now support nearly 36% of newly designed nanosatellite platforms. Continued localization of critical space-grade electronics and expanding satellite constellation programs are strengthening component innovation, creating a strong foundation for the strategic market developments ahead.

The Nano Star Tracker Market has become strategically important as governments and commercial operators accelerate deployment of small satellites requiring precise autonomous navigation. Growing investments in Earth observation, secure communications, and defense space assets are increasing demand for compact optical guidance systems, while supply-chain restructuring is encouraging domestic production of radiation-tolerant electronics and space-qualified optical components.

Modern nano star trackers improve attitude determination accuracy by approximately 22% compared with conventional miniature optical sensors while reducing payload weight by nearly 18%. North America leads commercial spacecraft innovation and satellite integration, whereas Europe maintains strengths in precision optical engineering and space-qualified sensor technologies. Over the next two to three years, autonomous navigation systems are expected to be integrated into more than 55% of newly deployed nanosatellite platforms, improving mission reliability and reducing dependence on ground-based corrections.

Satellite manufacturers are increasingly integrating nano star trackers with onboard AI processing, inertial measurement units, and flight computers to enhance real-time spacecraft autonomy. Companies are expanding production capacity, strengthening partnerships with satellite integrators, and investing in compact optical technologies optimized for constellation deployments. These strategic initiatives position nano star trackers as critical enabling systems for next-generation space missions, delivering operational precision, mission flexibility, and long-term competitive advantage across the expanding global space economy.

Rapid deployment of CubeSats and low Earth orbit satellite constellations is accelerating demand for nano star trackers that provide autonomous attitude determination with minimal payload weight. Nearly 54% of newly manufactured nanosatellites now integrate precision star tracking systems, while onboard pointing accuracy improves by approximately 23% through advanced optical navigation. The United States continues expanding commercial and defense satellite programs, encouraging domestic production of space-qualified optical sensors and radiation-hardened electronics. This structural shift improves mission autonomy while reducing dependence on ground-based corrections. In response, manufacturers are expanding optical assembly facilities, investing in AI-enabled navigation algorithms, and strengthening partnerships with satellite integrators to deliver compact, high-precision guidance systems for next-generation spacecraft.

Dependence on radiation-hardened image sensors, precision optics, and space-qualified electronic components continues creating structural procurement challenges. Critical space-grade components account for nearly 37% of total nano star tracker manufacturing costs, while specialized optical assemblies increase subsystem production expenses by approximately 24%. Limited global availability of qualified aerospace components has intensified supply-chain pressure following stricter export controls affecting advanced space technologies. These constraints reduce manufacturing flexibility and extend spacecraft integration schedules. Companies are responding by diversifying supplier networks, increasing localized production of optical assemblies, establishing long-term procurement agreements, and qualifying alternative electronic components to improve supply resilience without compromising mission reliability.

Artificial intelligence is creating new opportunities by enabling onboard image recognition, adaptive star catalog processing, and autonomous spacecraft orientation with reduced computational requirements. More than 42% of newly developed nanosatellite platforms are designed to support AI-assisted navigation functions, while advanced image processing improves attitude solution speed by approximately 19% and lowers onboard computing load by nearly 16%. Japan continues investing in intelligent satellite technologies supporting autonomous space operations and deep-space exploration. Companies are expanding R&D programs, partnering with flight software developers, and integrating edge computing capabilities into compact navigation systems. A significant strategic opportunity lies in reducing spacecraft operational dependence on continuous ground control through intelligent onboard decision-making.

Maintaining consistent optical calibration across varying orbital environments, thermal conditions, and mission durations remains a major execution challenge. Around 33% of system qualification activities focus on calibration validation, while integration testing requirements have increased by nearly 21% for multi-satellite constellation programs. Germany's aerospace sector continues strengthening qualification requirements for precision optical payloads operating in demanding orbital environments. These technical demands increase engineering complexity, extend mission preparation schedules, and require extensive validation before launch. Companies must invest in advanced optical testing facilities, digital simulation platforms, and collaborative verification programs with satellite manufacturers to ensure reliable long-term spacecraft performance across increasingly complex mission architectures.

Miniaturized Optical Sensor Integration: Satellite manufacturers are deploying lighter optical assemblies that reduce payload weight by approximately 18% while improving pointing precision by nearly 20%. Growing CubeSat deployments are accelerating this transition. Companies are scaling compact sensor production and strengthening partnerships with spacecraft integrators to support high-volume constellation manufacturing.

Domestic Space Component Localization: Supply-chain restructuring is encouraging regional manufacturing of space-qualified optics and electronics. Localized procurement has shortened component lead times by around 17% while improving production continuity by approximately 15%. Manufacturers are expanding domestic assembly capabilities and qualifying multiple suppliers to strengthen resilience against export restrictions affecting critical aerospace technologies.

Edge-Based Navigation Processing: Onboard processing architectures increasingly execute star identification and attitude calculations without continuous ground intervention. Advanced embedded processors improve navigation response speed by nearly 22% while reducing communication dependency by approximately 14%. Satellite developers are integrating AI-capable processors with star trackers to enhance autonomous mission operations and constellation management.

Radiation-Hardened Sensor Evolution: New-generation CMOS imaging sensors improve radiation tolerance by approximately 19% while extending operational stability by nearly 16% during long-duration missions. Rather than increasing subsystem size, manufacturers are investing in advanced semiconductor packaging, specialized optical coatings, and collaborative technology development to improve mission reliability across commercial and defense spacecraft.

CMOS-Based Nano Star Trackers account for approximately 64% of the market owing to their compact design, lower power consumption, reduced manufacturing cost, and seamless integration with CubeSat and nanosatellite platforms. Their superior imaging performance and compatibility with miniaturized onboard electronics make them the preferred solution for commercial and scientific satellite missions. Radiation-Hardened Nano Star Trackers represent the fastest-growing segment as defense agencies and deep-space missions increasingly prioritize long-duration reliability under harsh orbital environments. CCD-based systems continue serving high-precision scientific missions, while hybrid optical architectures maintain strategic relevance for specialized aerospace applications requiring enhanced redundancy. Companies are expanding radiation-tolerant sensor development, investing in miniaturized optical assemblies, and strengthening partnerships with satellite manufacturers to accelerate next-generation navigation system deployment.

Investment priorities are steadily shifting toward intelligent, lightweight optical navigation technologies that combine higher pointing accuracy with lower power consumption. Manufacturers in the United States and Japan continue expanding advanced sensor integration capabilities to support growing satellite constellation deployments and increasingly autonomous spacecraft operations.

According to findings presented at the 2025 Small Satellite Conference, compact CMOS-based optical navigation systems continue gaining adoption across CubeSat programs due to improved integration efficiency, lower payload mass, and enhanced mission flexibility.

Earth Observation accounts for approximately 42% of Nano Star Tracker demand, supported by expanding commercial imaging constellations, environmental monitoring missions, and precision remote sensing programs. High pointing accuracy and autonomous spacecraft stabilization remain essential for capturing high-resolution imagery and maximizing mission efficiency. Communication Satellites represent the fastest-growing application as low Earth orbit broadband constellations require compact, high-performance attitude determination systems for reliable network coverage. Scientific research missions continue driving demand for precision optical navigation, while technology demonstration satellites maintain strategic importance for validating next-generation spacecraft technologies. Nearly 39% of newly launched nanosatellite missions now incorporate advanced autonomous attitude determination systems to improve operational accuracy and reduce ground intervention.

Satellite manufacturers are expanding modular spacecraft platforms while integrating AI-enabled navigation software and compact optical payloads. Standardized spacecraft architectures and higher subsystem interoperability are strengthening deployment efficiency across both commercial and government satellite programs.

A 2026 International Astronautical Federation (IAF) technical assessment highlighted autonomous attitude determination as a key enabling capability for expanding small satellite constellation performance and mission reliability.

Commercial satellite operators account for approximately 48% of Nano Star Tracker procurement due to rapid constellation deployment, expanding Earth observation services, and increasing demand for autonomous spacecraft operations. Defense and Government Space Agencies represent the fastest-growing end-user group as sovereign satellite programs, secure communications, and national space capabilities continue expanding worldwide. Research institutions remain important adopters for scientific missions and technology validation, while academic CubeSat programs contribute steady demand through university-led satellite development initiatives. Nearly 35% of recently funded nanosatellite programs include enhanced autonomous navigation capabilities to improve operational independence and mission longevity.

Manufacturers are targeting these customer groups through mission-specific product customization, long-term engineering partnerships, flexible integration support, and scalable production capabilities. Companies are also strengthening software compatibility, launch-provider collaboration, and lifecycle technical services to improve deployment readiness and secure long-term satellite platform partnerships.

According to the 2025 Space Foundation industry assessment, commercial satellite operators continue increasing investment in autonomous spacecraft technologies to improve constellation efficiency, reduce operational complexity, and support large-scale orbital deployments.

North America accounted for the largest market share at 36.4% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 13.8% between 2026 and 2033.

Commercial Space Expansion Strengthens Precision Navigation Leadership

North America leads the Nano Star Tracker Market through its mature commercial space ecosystem, expanding defense satellite programs, and advanced spacecraft manufacturing capabilities. The region contributes approximately 36% of global market demand, supported by increasing deployment of CubeSats, Earth observation satellites, and low Earth orbit communication constellations. Nearly 51% of newly integrated nanosatellite platforms in the region utilize autonomous optical attitude determination systems to improve mission accuracy and reduce operational dependence on ground stations. Aerospace manufacturers continue expanding precision optics production, strengthening spacecraft integration capabilities, and forming strategic partnerships with satellite operators to support large-scale constellation deployment while improving mission reliability.

United States Market Outlook: The United States dominates regional activity through its leadership in commercial launch services, satellite manufacturing, defense space programs, and advanced optical technologies. More than 57% of North America's nanosatellite integration activities are concentrated in the country, supported by continued investment in autonomous spacecraft technologies and domestic production of radiation-hardened electronics. Strong collaboration among satellite manufacturers, launch providers, and aerospace technology companies continues accelerating innovation in compact optical navigation systems.

Precision Optical Engineering Supports Autonomous Space Missions

Europe maintains a strong position through advanced optical engineering, institutional space programs, and increasing investment in autonomous satellite technologies. The region accounts for approximately 28% of global market demand, supported by high-value Earth observation, scientific research, and secure communication missions. Nearly 34% of newly developed European nanosatellite platforms incorporate miniaturized star trackers with enhanced onboard processing capabilities. Companies continue expanding optical sensor development, radiation-resistant imaging technologies, and spacecraft integration partnerships to strengthen mission autonomy and long-duration operational reliability.

France Market Outlook: France serves as Europe's leading market through its established aerospace industry, precision optical manufacturing, and strong institutional space capabilities. The country's concentration of satellite manufacturers and optical technology developers supports continuous advancement in miniaturized navigation systems. Approximately 41% of Europe's precision spacecraft optical subsystem development is associated with French aerospace programs, reinforcing long-term investment in compact star tracker technologies.

Satellite Manufacturing Scale Accelerates Navigation Technology Adoption

Asia-Pacific represents the fastest-expanding Nano Star Tracker Market through rapid satellite manufacturing growth, expanding national space programs, and increasing investment in commercial space technologies. The region contributes nearly 43% of global small satellite production, creating sustained demand for compact optical navigation systems. China, Japan, India, and South Korea continue strengthening spacecraft manufacturing infrastructure and domestic production of space-qualified electronic components. Regional manufacturers have expanded precision optical assembly capabilities, reducing subsystem integration timelines by approximately 18% while improving supply-chain resilience for satellite production.

China Market Outlook: China leads the regional market through its large-scale satellite manufacturing capacity, expanding commercial launch activities, and integrated aerospace supply chain. More than 54% of Asia-Pacific's nanosatellite production is concentrated in China, encouraging wider deployment of compact star tracker technologies across commercial and government missions. Domestic manufacturers continue investing in optical sensor fabrication, onboard processing technologies, and spacecraft subsystem integration to strengthen global competitiveness.

National Space Programs Encourage Technology Adoption

South America is steadily advancing nano star tracker adoption through expanding Earth observation initiatives, university satellite programs, and national space technology development. Brazil and Argentina continue strengthening satellite research capabilities while increasing deployment of compact spacecraft for environmental monitoring and scientific missions. Approximately 22% of newly developed regional nanosatellite projects now integrate autonomous optical navigation systems to improve mission precision. Limited domestic production of space-grade electronics remains an operational constraint, encouraging regional partnerships and technology transfer initiatives to strengthen spacecraft manufacturing capabilities.

Brazil Market Outlook: Brazil remains the region's most significant market through its established aerospace sector, satellite development expertise, and expanding national space initiatives. Continued investment in Earth observation missions and academic CubeSat programs is increasing demand for precision attitude determination technologies. Growing collaboration between research institutions and aerospace manufacturers is strengthening the country's long-term capability in compact spacecraft subsystem development.

Space Infrastructure Investment Expands Market Potential

The Middle East & Africa market is gaining momentum as governments invest in satellite infrastructure, Earth observation capabilities, and national space strategies. Gulf countries continue expanding space technology programs, while South Africa strengthens scientific satellite development and aerospace research. Around 18% of recently announced regional satellite initiatives include autonomous spacecraft navigation technologies to improve mission efficiency and reduce operational complexity. Technology partnerships and infrastructure modernization are encouraging wider adoption of advanced optical guidance systems across emerging space programs.

United Arab Emirates Market Outlook: The United Arab Emirates has become the region's leading market through sustained investment in national space initiatives, satellite development, and advanced aerospace innovation. Continued expansion of indigenous spacecraft programs and international technology collaborations is strengthening demand for compact optical navigation systems. Increasing focus on autonomous satellite capabilities and precision mission planning is reinforcing the country's position as a regional hub for advanced space technologies.

The Nano Star Tracker Market is led by specialized space navigation companies including Blue Canyon Technologies, Sodern, NewSpace Systems, ARCSEC, and Tensor Tech, competing directly on pointing accuracy, SWaP optimization, and radiation tolerance, while emerging regional developers compete through cost-efficient subsystem integration. The top five companies collectively account for approximately 58% of market share. Competition centers on optical precision, onboard processing, and rapid satellite integration rather than pricing alone. Advanced CMOS imaging improves attitude determination by nearly 21%, compact architectures reduce payload weight by approximately 18%, and standardized interfaces shorten spacecraft integration time by around 16%. Companies are expanding optical manufacturing, partnering with satellite integrators, and strengthening vertical control over sensor calibration and embedded software. Competitive momentum is shifting toward AI-enabled autonomous navigation and constellation-optimized star trackers. Space qualification, radiation-hard component availability, and flight heritage remain critical entry barriers. Success depends on proven orbital reliability, scalable production, and seamless spacecraft integration.

Blue Canyon Technologies

Sodern

NewSpace Systems

ARCSEC

Tensor Tech

Jena-Optronik GmbH

CubeSpace

Rocket Lab

Berlin Space Technologies

Leonardo S.p.A.

Redwire Corporation

Space Micro Inc.

Nano star tracker technology is rapidly advancing through AI-assisted star identification, radiation-hardened CMOS sensors, and ultra-compact optical assemblies that improve autonomous spacecraft navigation. Nearly 52% of newly developed nanosatellite platforms now integrate miniaturized star trackers, while advanced image-processing algorithms improve attitude determination speed by approximately 23%. Low-power embedded processors and high-sensitivity imaging sensors enable precise navigation without increasing payload size, supporting expanding CubeSat and constellation missions.

The most significant technology transition is the shift from conventional CCD architectures to advanced CMOS-based optical systems. Compared with legacy CCD star trackers, modern CMOS platforms reduce power consumption by approximately 28% while improving processing efficiency by nearly 20%. Commercial satellite operators, defense spacecraft manufacturers, and Earth observation missions gain the strongest competitive advantage through lighter payloads, faster onboard processing, and improved radiation tolerance. Integrated inertial navigation interfaces and edge-based computing further strengthen spacecraft autonomy and reduce dependence on ground-based navigation support.

Between 2026 and 2028, AI-enabled optical navigation, radiation-resistant semiconductor packaging, and digital spacecraft autonomy will redefine competitive positioning. Autonomous navigation systems are expected to exceed 60% deployment across newly launched nanosatellite constellations. Companies investing in intelligent software, compact optics, and vertically integrated manufacturing will strengthen mission reliability, accelerate satellite deployment, and secure long-term leadership as autonomous orbital operations become a standard capability.

April 2025 – Sodern delivered the first flight model of its HORUS star tracker to Airbus Defence & Space under a multi-year agreement. The compact unit weighs only 1.6 kg, improving satellite integration and high-precision attitude determination. Source: Sodern

May 2025 – Sodern commercially launched the ASTRADIA daytime star tracker for GNSS-denied navigation, combining celestial tracking with inertial navigation to deliver continuous positioning for civil and military platforms, expanding technology beyond traditional space applications. Source: Sodern

April 2026 – Rocket Lab introduced its High-Performance Star Tracker (ST-HP) featuring greater than 50 kRad radiation tolerance and pointing accuracy better than 1 arcsecond, strengthening long-duration spacecraft performance for LEO and deep-space missions. Source: Rocket Lab

June 2025 – Blue Canyon Technologies successfully launched its CubeSat platform supporting NASA's ARCSTONE mission, reinforcing the company's flight-proven spacecraft and precision attitude determination capabilities for advanced Earth observation calibration missions. Source: RTX.

This report provides comprehensive analysis of the Nano Star Tracker Market across product types, satellite applications, end-users, and major geographic regions. It evaluates CMOS-based, CCD-based, radiation-hardened, and hybrid optical navigation systems while assessing deployment across Earth observation, communication, scientific research, defense, and technology demonstration satellites. The study examines adoption patterns, spacecraft integration trends, autonomous navigation capabilities, and competitive participation across more than 12 leading space technology companies.

The report delivers strategic insights supporting investment planning, product development, geographic expansion, and competitive positioning between 2026 and 2033. It evaluates regional manufacturing capabilities, optical sensor innovation, spacecraft subsystem integration, and emerging opportunities in autonomous satellite navigation. Coverage extends to AI-enabled image processing, radiation-hardened electronics, compact optical architectures, and constellation-focused navigation systems, enabling decision-makers to identify high-growth segments, operational priorities, and long-term competitive strategies across the expanding global space industry.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 320.5 Million |

|

Market Revenue in 2033 |

USD 828.2 Million |

|

CAGR (2026 - 2033) |

12.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Blue Canyon Technologies, Sodern, NewSpace Systems, ARCSEC, Tensor Tech, Jena-Optronik GmbH, CubeSpace, Rocket Lab, Berlin Space Technologies, Leonardo S.p.A., Redwire Corporation, Space Micro Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |