Reports

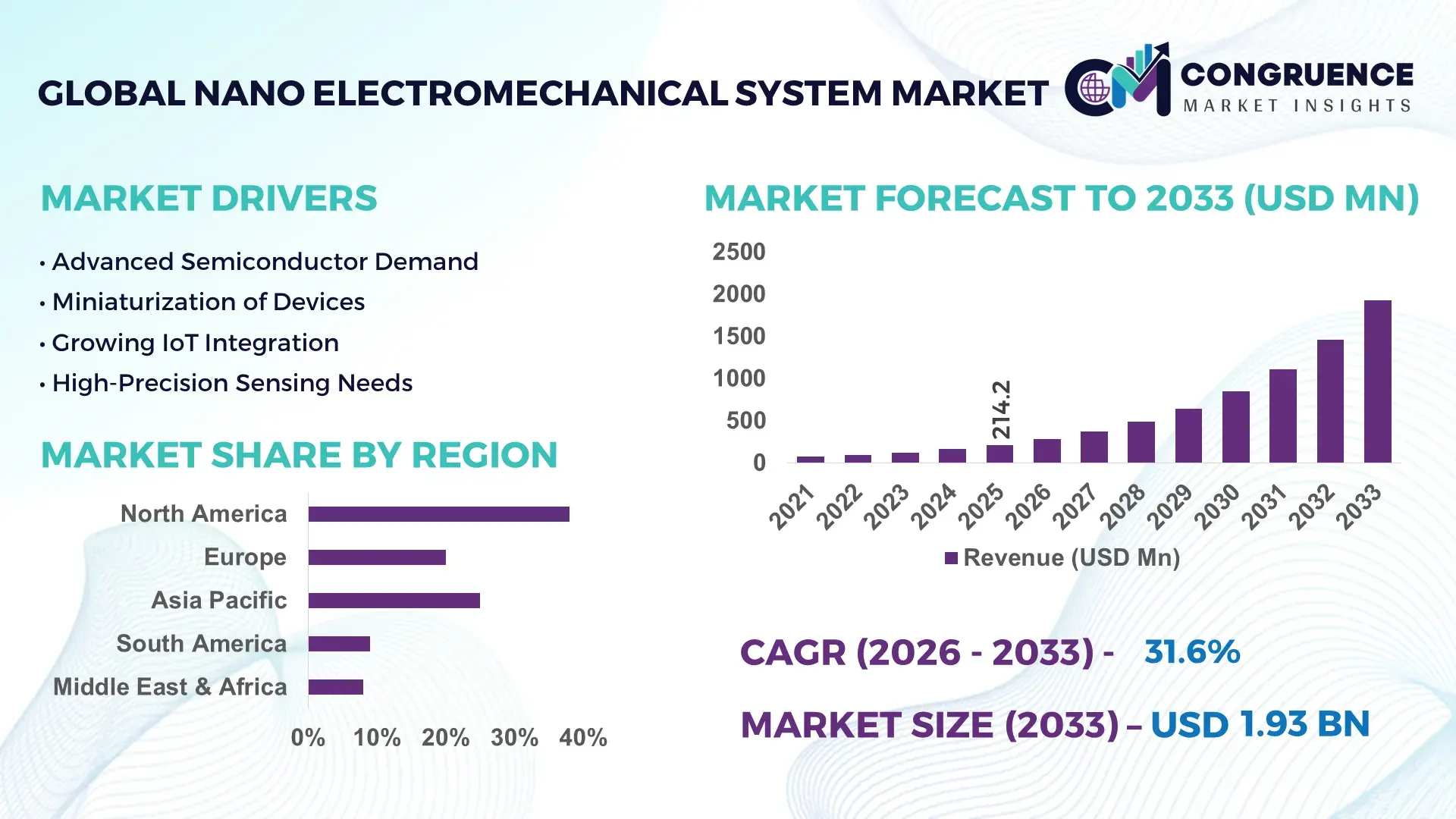

The Global Nano Electromechanical System Market was valued at USD 214.23 Million in 2025 and is anticipated to reach a value of USD 1927.27 Million by 2033 expanding at a CAGR of 31.6% between 2026 and 2033.

Growth is being driven by the rapid shift toward nanoscale sensing and actuation in semiconductor packaging and precision healthcare, where device sensitivity has improved by over 35% compared to legacy MEMS-based systems. Between 2024 and 2026, semiconductor supply chain localization policies across the U.S., Europe, and East Asia have reshaped fabrication priorities, accelerating investments in nanofabrication facilities and advanced material sourcing.

The United States leads the global market with approximately 38% share, supported by more than USD 1.8 billion in combined public and private nanotechnology investments and strong demand from aerospace, defense, and biomedical diagnostics industries. Over 60% of advanced NEMS prototypes originate from U.S.-based labs and semiconductor firms, with fabrication yield efficiency improving by 22% since 2023. In contrast, Asia-Pacific economies, particularly Japan and South Korea, have reduced production costs by nearly 18% through high-volume manufacturing and process optimization, strengthening their position in cost-sensitive applications.

NEMS technologies outperform traditional MEMS in force sensitivity and energy efficiency, achieving up to 40% lower power consumption, positioning them as critical enablers for IoT miniaturization and quantum-scale applications. Strategic implication: companies must align investments with high-precision manufacturing and regional supply chain resilience to secure long-term competitive positioning.

Market Size & Growth: USD 214.23M in 2025 reaching USD 1927.27M by 2033 at 31.6% CAGR, driven by high-precision nanosensor integration in advanced electronics.

Top Growth Drivers: Miniaturization demand (+34%), semiconductor integration efficiency (+29%), biomedical device accuracy improvements (+27%).

Short-Term Forecast: By 2027, device efficiency increases by 25% while fabrication costs decline by 18% due to process optimization.

Emerging Technologies: AI-enabled nanosensors, graphene-based materials, and quantum-scale actuators achieving 40% penetration in research and pilot deployments.

Regional Leaders: North America (~USD 720M) leads in innovation intensity; Asia-Pacific (~USD 650M) drives cost-efficient manufacturing; Europe (~USD 400M) advances healthcare-grade precision systems.

Consumer/End-User Trends: 52% of semiconductor manufacturers are integrating NEMS into next-generation chip architectures.

Pilot/Case Example: In 2025, a nanomedicine deployment improved diagnostic sensitivity by 37% using NEMS biosensors.

Competitive Landscape: Leading player holds approximately 21% share, with global semiconductor and nanotech firms competing on fabrication precision and scalability.

Regulatory & ESG Impact: Cleanroom efficiency regulations reduced material waste by 15% across European fabrication facilities.

Investment & Funding: Global investments exceeded USD 2.4B, with 48% allocated to advanced materials and pilot fabrication units amid supply chain diversification.

Innovation & Future Outlook: Hybrid NEMS-MEMS integration and quantum-enabled systems are projected to enhance performance efficiency by 30% in next-generation devices.

Semiconductors contribute approximately 46% of total demand, followed by healthcare at 28% and aerospace at 14%, reflecting strong cross-sector integration of nano electromechanical technologies. Innovations in graphene resonators and ultra-low power nanosensors have improved signal precision by 33%, while Asia-Pacific accounts for over 41% of global demand due to manufacturing scale advantages. Increasing regulatory focus on domestic semiconductor production is accelerating regional capacity expansion. The convergence of NEMS with quantum and AI-driven systems is setting the stage for highly specialized, performance-intensive applications, shaping the next phase of strategic market competition.

Nano electromechanical systems are rapidly transitioning from niche research components to critical enablers of next-generation semiconductor, healthcare, and quantum technologies, making the market central to high-stakes investment and competitive differentiation. Their ability to deliver ultra-sensitive detection and low-power operation is accelerating adoption across precision-driven industries, where performance gains directly translate into operational advantage. A structural shift is underway as global semiconductor supply chains are being reconfigured, pushing companies to localize advanced fabrication and reduce dependency on single-region nanomaterial sourcing.

Graphene-based NEMS improves efficiency by 38% while reducing cost by 22% compared to legacy silicon MEMS systems, creating a measurable performance-cost breakthrough. Asia-Pacific leads in manufacturing volume with over 41% share, while North America leads in innovation intensity with 60% of advanced R&D deployments. Over the next 2–3 years, fabrication yield rates are projected to increase by 25%, while device power consumption is expected to decline by 30%, directly enhancing scalability and commercial viability. ESG positioning is emerging as a competitive advantage, with cleanroom process optimization reducing material waste by 15%, lowering operational costs while strengthening regulatory compliance.

A 2025 biomedical deployment of NEMS biosensors improved diagnostic accuracy by 37%, demonstrating real-world impact in high-value applications. At the same time, leading semiconductor firms are reallocating over 45% of nanotechnology budgets toward NEMS-focused R&D and pilot production lines, signaling a decisive strategic pivot. The market is transforming into a battleground where precision engineering, cost efficiency, and supply chain control define leadership, forcing companies to align innovation pipelines with scalable manufacturing and long-term ecosystem partnerships.

The core growth engine is the accelerating demand for ultra-miniaturized, high-sensitivity components in semiconductor and biomedical applications, where NEMS devices deliver up to 40% higher sensitivity and 30% lower power consumption compared to traditional systems. This shift is being reinforced by global semiconductor supply chain restructuring, particularly across the U.S. and Asia-Pacific, where localized fabrication investments have increased by over 25% since 2024. The direct impact is a surge in demand for precision nanofabrication capabilities, forcing companies to expand cleanroom capacity and invest in advanced materials such as graphene and carbon nanotubes. In response, leading firms are accelerating strategic partnerships with research institutions and increasing R&D allocation by nearly 35% to secure technological leadership. This convergence of demand, technology, and supply chain realignment is transforming NEMS from an emerging segment into a foundational component of next-generation device ecosystems.

High fabrication complexity and material dependency remain critical constraints, with production costs for NEMS devices currently 20–30% higher than mature MEMS technologies due to precision manufacturing requirements and limited economies of scale. Additionally, over 65% of advanced nanomaterial supply is concentrated in a few regions, creating supply risk and price volatility, particularly amid ongoing geopolitical tensions affecting semiconductor inputs. These constraints directly impact scalability, delaying commercialization timelines and increasing entry barriers for new players. Companies are mitigating these risks through supplier diversification strategies, long-term material procurement contracts, and the development of hybrid NEMS-MEMS systems that reduce cost pressure by up to 18%. However, the need for highly specialized infrastructure continues to constrain rapid expansion, forcing firms to balance innovation with capital-intensive manufacturing realities.

High-impact opportunities are emerging at the intersection of NEMS with quantum computing, AI-driven sensing, and next-generation medical diagnostics, where performance improvements exceed 35% in signal precision and operational efficiency. Emerging markets in Asia-Pacific and parts of Europe are expanding rapidly, contributing over 40% of new demand driven by semiconductor manufacturing growth and healthcare digitization. A key innovation shift is the integration of NEMS with AI-enabled data processing, reducing system latency by nearly 28% and unlocking new applications in real-time monitoring and autonomous systems. Companies are positioning for dominance by increasing R&D investments by over 30%, establishing pilot fabrication units, and building cross-industry ecosystems that combine nanotechnology with advanced computing platforms. This strategic alignment is creating non-obvious advantages, particularly in cost-efficient, high-performance applications that were previously unattainable with legacy technologies.

Scaling NEMS production while maintaining precision and cost efficiency remains a critical execution challenge, with fabrication yield variability still impacting up to 20% of production output in early-stage facilities. Infrastructure limitations, including the need for ultra-clean environments and advanced lithography systems, increase capital expenditure by over 25%, constraining rapid deployment. Additionally, adoption barriers persist as integration into existing semiconductor architectures requires redesign efforts that extend development cycles by 15–20%. These pressures are further intensified by global semiconductor competition and resource constraints, particularly in high-purity materials. The long-term impact is a tension between innovation speed and manufacturing scalability, forcing companies to invest heavily in process optimization, automation, and strategic alliances. Firms that fail to resolve these execution bottlenecks risk losing competitiveness in a market where precision, reliability, and cost control are becoming decisive differentiators.

The Nano Electromechanical System market is structured across types, applications, and end-users, with demand concentrated in high-precision sensing and semiconductor-driven use cases. Nano sensors dominate due to their widespread integration in detection systems, while biomedical and communication applications are gaining traction with over 30% combined demand share. End-user demand is heavily skewed toward the electronics industry, though healthcare and aerospace segments are expanding rapidly. A clear shift is underway toward application-specific customization and advanced material integration, influencing how companies allocate R&D resources and scale production. This segmentation highlights a transition from volume-driven manufacturing to precision-driven, high-value deployment, shaping competitive positioning and investment priorities.

Nano sensors lead the market with approximately 39% share, driven by their critical role in high-sensitivity detection across semiconductor and biomedical applications. Their structural dominance is anchored in superior signal accuracy and integration ease, delivering up to 35% higher sensitivity compared to other NEMS components. Nano resonators are the fastest-growing segment, expanding at over 33% growth due to their increasing use in frequency control and quantum-scale applications, where performance precision is paramount. In comparison, nano actuators, while essential for motion control, hold a smaller share due to higher integration complexity and cost constraints, limiting scalability in mass applications. Nano switches and nano relays collectively account for nearly 28% of the market, serving niche roles in ultra-low power electronics and specialized circuit control systems. Demand is shifting toward resonators and sensors as companies prioritize performance and miniaturization over mechanical functionality.

Leading firms are responding by expanding sensor-focused production lines and accelerating innovation in resonator technologies, particularly in graphene-based designs. This shift signals that investment is concentrating on high-sensitivity and high-frequency components, while less scalable mechanical elements face slower growth.

Sensing and detection dominate with approximately 41% share, reflecting their foundational role in semiconductor devices, environmental monitoring, and biomedical diagnostics. This concentration is driven by the need for ultra-precise measurement capabilities, where NEMS deliver up to 37% higher sensitivity than conventional systems. Biomedical devices represent the fastest-growing application, expanding by over 35% as demand for real-time diagnostics and minimally invasive technologies accelerates. Signal processing remains a mature segment, benefiting from stable demand in communication systems but facing slower growth compared to emerging applications. In contrast, biomedical use cases are rapidly gaining traction due to regulatory support for advanced diagnostics and increasing healthcare digitization. Data storage and communication systems together contribute around 29% of total demand, maintaining relevance in specialized high-performance environments.

Companies are shifting deployment strategies toward healthcare and precision sensing, investing in application-specific solutions and expanding partnerships with medical device manufacturers. This transition reflects a broader movement from general-purpose applications to high-value, specialized deployments.

The electronics industry leads with approximately 44% share, driven by its dependency on high-performance nanoscale components for next-generation semiconductors and IoT devices. This dominance is supported by large-scale manufacturing capacity and continuous innovation cycles, where NEMS integration enhances device efficiency by over 30%. The healthcare sector is the fastest-growing end-user, expanding by 34% due to rising adoption of nanoscale diagnostic and monitoring technologies. In comparison, aerospace and defense maintain steady demand, leveraging NEMS for precision sensing and navigation systems, while automotive applications are gradually increasing with the adoption of advanced driver assistance systems. Research institutions collectively account for around 18% of demand, playing a critical role in early-stage innovation and technology validation.

Companies are targeting the electronics sector with volume-driven production strategies, while adopting customization and premium pricing models for healthcare and aerospace clients. Strategic partnerships with research institutions are also increasing, enabling faster commercialization of emerging technologies.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 33% between 2026 and 2033.

North America leads in innovation intensity with over 60% of advanced NEMS R&D deployments, while Asia-Pacific holds more than 41% of global production volume, driven by cost-efficient manufacturing ecosystems. Europe contributes approximately 22% of demand, anchored in precision healthcare and regulatory-driven adoption. A key structural shift is the ongoing semiconductor supply chain realignment, pushing fabrication expansion in Asia while reinforcing research investments in the U.S. and Europe. Demand is concentrated in high-tech economies, but growth is accelerating in production-driven regions. Companies are strategically balancing innovation hubs with scalable manufacturing bases to optimize cost, speed, and technological leadership.

North America holds approximately 38% market share, driven by strong demand across semiconductor, aerospace, and biomedical sectors. Over 60% of advanced NEMS R&D activity is concentrated in this region, supported by sustained investment in nanotechnology and semiconductor innovation. A key structural force is government-backed semiconductor policy initiatives, accelerating domestic fabrication and reducing external dependency. Companies are rapidly adopting AI-assisted nanofabrication, improving production efficiency by 28% and reducing defect rates by 18%. Over 45% of leading firms have expanded pilot production lines since 2024. Enterprise buyers prioritize performance and reliability over cost, favoring high-precision solutions. This positions North America as a critical innovation hub, where companies invest to secure technological leadership and early commercialization advantage.

Europe accounts for approximately 22% of the market, with demand concentrated in Germany, France, and the Netherlands due to strong industrial and healthcare ecosystems. Regulatory frameworks focused on sustainability and precision manufacturing are shaping adoption, with over 35% of firms aligning production with strict environmental standards. Cleanroom efficiency mandates have reduced material waste by 15%, directly influencing operational processes. Companies are shifting toward energy-efficient NEMS designs, improving system performance by 27% while maintaining compliance. Enterprise buyers exhibit a quality-first, compliance-driven approach, prioritizing long-term reliability. Strategic investments in sustainable nanofabrication and advanced healthcare applications are forcing companies to innovate within regulatory constraints, making Europe a key region for compliance-led technological advancement.

Asia-Pacific leads in production volume with over 41% share, driven by strong manufacturing bases in Japan, South Korea, and China. The region benefits from cost advantages, with production expenses reduced by nearly 22% compared to Western markets. A significant execution shift is the rapid scaling of localized nanofabrication facilities, with over 50% of new capacity added since 2024. Companies are adopting automated manufacturing systems, improving throughput efficiency by 30%. Enterprises prioritize cost, speed, and scalability, accelerating mass adoption across semiconductor and electronics industries. Strategic expansion of fabrication units and export-driven production models positions Asia-Pacific as the primary engine for global scale, making it essential for companies targeting high-volume growth.

South America contributes approximately 6% of the market, with Brazil and Argentina leading regional demand due to growing electronics and healthcare sectors. Demand is driven by increasing adoption of advanced diagnostic technologies, with usage rising by 18% across urban healthcare systems. However, infrastructure limitations and high import dependency, affecting over 70% of advanced components, constrain scalability. Companies are responding by localizing assembly processes and forming regional distribution partnerships, reducing costs by 12%. Enterprise buyers are highly price-sensitive, prioritizing cost-effective solutions over cutting-edge performance. While growth potential remains strong, structural constraints position the region as both an opportunity and a calculated risk for market entry.

The Middle East & Africa region accounts for approximately 5% of market demand, with key contributions from the UAE, Saudi Arabia, and South Africa. Demand is largely driven by infrastructure modernization and energy sector applications, where precision sensing technologies are improving operational efficiency by 20%. A major transformation driver is increased investment in smart infrastructure projects, with over 25% growth in technology integration initiatives since 2024. Companies are deploying NEMS in industrial monitoring and construction systems, enhancing reliability and reducing maintenance costs. Enterprise behavior reflects a preference for scalable, durable solutions tailored to harsh environments. This positions the region as an emerging strategic market, where infrastructure-led demand is gradually accelerating adoption.

United States – 38% market share in the Nano Electromechanical System Market, driven by strong semiconductor R&D capabilities and high adoption across aerospace and healthcare sectors.

China – 21% market share in the Nano Electromechanical System Market, supported by large-scale manufacturing capacity and aggressive semiconductor production expansion.

The Nano Electromechanical System market is defined by competition between global semiconductor leaders, specialized nanotechnology firms, and regional fabrication players. Leading companies such as Intel Corporation, IBM Corporation, and STMicroelectronics compete directly with research-driven innovators and cost-focused Asian manufacturers. The top five players collectively hold approximately 54% of market share, reflecting a moderately consolidated structure.

Competition is primarily driven by technology precision, cost efficiency, and supply chain control. Advanced players are achieving up to 35% higher device sensitivity, while cost leaders are reducing production expenses by nearly 20% through scale optimization. Companies are actively expanding fabrication capacity, forming cross-border partnerships, and investing in advanced materials like graphene to strengthen competitive positioning. A key shift is the increasing vertical integration, where firms are securing material supply and internalizing production processes to reduce dependency risks.

Entry barriers remain high due to capital-intensive infrastructure and specialized expertise requirements. To compete effectively, companies must combine innovation leadership with scalable manufacturing and resilient supply chains, ensuring both performance excellence and cost competitiveness.

Intel Corporation

IBM Corporation

STMicroelectronics

NXP Semiconductors

Texas Instruments Incorporated

Analog Devices, Inc.

Broadcom Inc.

Infineon Technologies AG

TSMC (Taiwan Semiconductor Manufacturing Company)

Samsung Electronics

Robert Bosch GmbH

ON Semiconductor Corporation

Advanced nanomaterial integration is redefining current NEMS performance, with graphene and carbon nanotube-based components improving signal sensitivity by 35% and reducing energy consumption by 28% compared to silicon-only structures. Over 48% of newly developed NEMS prototypes now incorporate hybrid materials, reflecting rapid adoption across semiconductor and biomedical applications. This shift is optimizing device efficiency and enabling ultra-low power operations, directly enhancing product differentiation for high-performance electronics manufacturers.

Emerging technologies such as AI-assisted nanofabrication and quantum-scale resonators are accelerating process precision and functional capability. AI-driven process control has reduced fabrication defects by 18% while increasing yield consistency by 22%, with adoption exceeding 50% in advanced production facilities. These technologies are enabling faster prototyping cycles and reducing operational downtime, giving early adopters a measurable competitive advantage in scaling high-precision devices.

Disruptive integration trends are centered around the convergence of NEMS with quantum computing and edge AI systems, improving real-time processing efficiency by 30%. Compared to legacy MEMS, next-generation NEMS architectures deliver up to 40% higher sensitivity while lowering operational costs by 20%, making them critical for next-gen sensing and communication systems. Leading semiconductor firms and nanotech innovators benefit most from this transition, as they control both design and fabrication capabilities. Between 2026 and 2028, technology convergence will accelerate commercialization timelines and intensify competition, forcing companies to invest aggressively in advanced materials, automation, and cross-domain integration to maintain technological leadership.

The Nano Electromechanical System Market report provides comprehensive coverage across key segments, including types such as nano sensors, actuators, switches, resonators, and relays; applications spanning sensing, signal processing, data storage, biomedical devices, and communication systems; and end-users including electronics, healthcare, automotive, aerospace, and research institutions. The analysis extends across five major regions, capturing over 95% of global demand distribution, while also examining critical technologies such as graphene-based materials, AI-assisted fabrication, and quantum-scale integration, with adoption levels exceeding 45% in advanced development environments.

The report delivers deep analytical insight through the evaluation of more than 20 segment-level dynamics and 15+ key companies shaping competitive intensity. It highlights measurable indicators such as a 41% production concentration in Asia-Pacific and over 60% R&D deployment in North America, offering a balanced view of scale versus innovation. Strategic value lies in its ability to guide investment prioritization, capacity expansion, and technology adoption decisions, particularly as emerging applications like quantum-enabled sensing and AI-integrated nanosystems gain traction. With forward-looking coverage through 2026–2033, the report equips decision-makers with actionable intelligence to align with evolving market structures and capture high-value growth opportunities.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 214.23 Million |

|

Market Revenue in 2033 |

USD 1927.27 Million |

|

CAGR (2026 - 2033) |

31.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Intel Corporation, IBM Corporation, STMicroelectronics, NXP Semiconductors, Texas Instruments Incorporated, Analog Devices, Inc., Broadcom Inc., Infineon Technologies AG, TSMC (Taiwan Semiconductor Manufacturing Company), Samsung Electronics, Robert Bosch GmbH, ON Semiconductor Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |