Reports

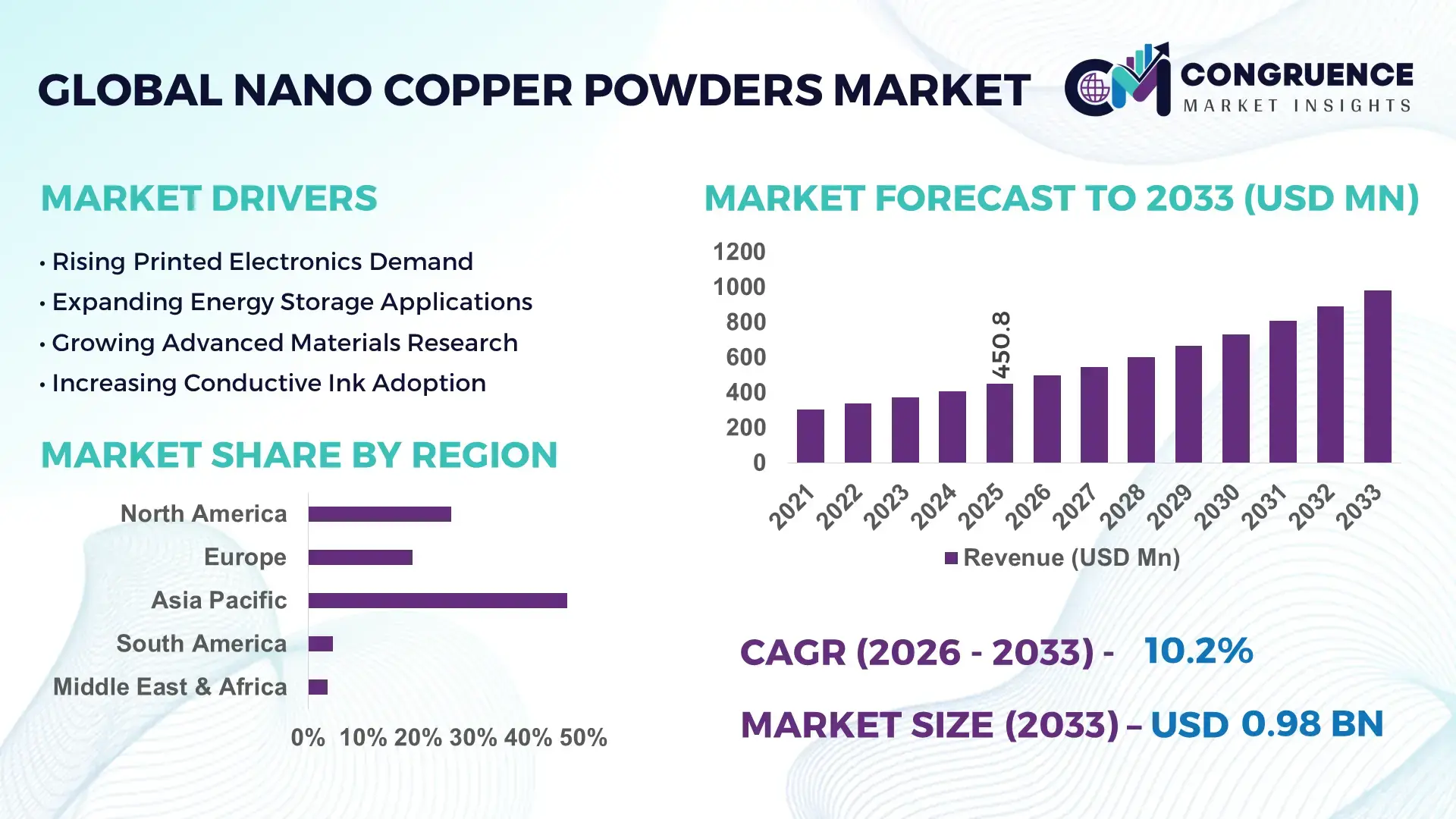

The Global Nano Copper Powders Market was valued at USD 450.8 Million in 2025 and is anticipated to reach a value of USD 980.5 Million by 2033 expanding at a CAGR of 10.2% between 2026 and 2033. Market expansion is being driven by the rapid integration of nano copper powders in conductive inks, advanced electronics packaging, lithium-ion battery components, and high-performance antimicrobial coatings, where conductivity improvements of 15–25% over conventional micron-grade copper materials are creating measurable manufacturing advantages. The market is also benefiting from the accelerating transition toward miniaturized electronic devices and next-generation printed electronics, forcing manufacturers to adopt nanomaterial-enabled production strategies. Between 2024 and 2026, global semiconductor localization initiatives, ongoing supply-chain diversification away from single-source manufacturing hubs, and heightened investment in advanced materials ecosystems have reshaped procurement strategies across electronics and energy-storage industries. Geopolitical competition surrounding semiconductor independence and critical technology supply chains has further elevated the strategic importance of conductive nanomaterials.

China remains the dominant country in the Nano Copper Powders Market, accounting for approximately 39% of global consumption and production capacity. The country has invested heavily in advanced materials manufacturing, with over 60% of its nano copper output directed toward electronics, energy storage, and conductive paste applications. More than 45% of regional printed electronics manufacturing is concentrated in China, while domestic battery and semiconductor industries continue increasing adoption rates. Compared with several mature Western markets, China maintains a significant cost advantage through integrated supply chains and large-scale production infrastructure, enabling higher commercialization rates and faster deployment of nano-enabled materials.

As industries prioritize localized advanced-material supply networks and performance-driven manufacturing, strategic investment is increasingly shifting toward scalable nano copper production capabilities, downstream application partnerships, and technology differentiation.

Market Size & Growth: USD 450.8 million in 2025 rising to USD 980.5 million by 2033 at 10.2% CAGR, supported by printed electronics and battery-material adoption.

Top Growth Drivers: Electronics demand (+28%), conductive ink deployment (+24%), and advanced battery integration (+21%) are accelerating market expansion.

Short-Term Forecast: By 2028, conductive material processing efficiency is projected to improve by 18% while production waste declines by 12%.

Emerging Technologies: AI-assisted materials design, automated nanoparticle synthesis, and advanced conductive paste formulations are improving yield rates by over 20%.

Regional Leaders: Asia-Pacific (~USD 451 million), North America (~USD 245 million), and Europe (~USD 196 million by 2033), supported by manufacturing expansion and electronics innovation.

Consumer/End-User Trends: More than 52% of electronics manufacturers are increasing nano-enabled material integration within product development pipelines.

Pilot/Case Example: In 2025, advanced conductive ink deployments improved circuit conductivity by 22% while reducing material usage by 14%.

Competitive Landscape: Leading suppliers collectively control nearly 35% of global supply; key participants include American Elements, NanoAmor, SkySpring Nanomaterials, Hongwu International, and Nanoshel.

Regulatory & ESG Impact: Material-efficiency initiatives are reducing copper waste generation by approximately 15% across advanced manufacturing applications.

Investment & Funding: More than USD 600 million in advanced-material investments have targeted production scaling, localization, and strategic partnerships since 2024.

Innovation & Future Outlook: Nano-enabled battery architectures and flexible electronics are reshaping next-generation product development and competitive positioning.

Electronics applications contribute nearly 44% of total demand, followed by energy storage at approximately 26% and industrial coatings at 18%, reflecting broad commercialization across advanced manufacturing sectors. Product innovation is increasingly focused on oxidation-resistant nano copper formulations and high-dispersion conductive pastes that improve conductivity by more than 20%. Demand remains strongest across Asia-Pacific, which accounts for over 47% of global consumption, while North American reshoring initiatives continue accelerating local procurement. Simultaneously, supply-chain diversification and advanced manufacturing policies are reshaping sourcing strategies, creating new opportunities for regional producers. These evolving dynamics are establishing the foundation for the next phase of strategic market competition and investment prioritization.

Nano copper powders are rapidly becoming a critical competitive asset across electronics, energy storage, advanced manufacturing, and conductive materials industries, transforming how companies optimize performance, reduce material costs, and secure technological differentiation. As device miniaturization accelerates and industrial manufacturers demand higher conductivity materials, nano copper powders are moving from specialized applications into mainstream production ecosystems.

A significant market shift is emerging from global supply-chain restructuring and semiconductor localization initiatives, forcing manufacturers to secure regional access to advanced conductive materials while reducing dependency on concentrated sourcing networks. This transformation is accelerating investment in scalable nanomaterial production and vertically integrated supply strategies.

Advanced nano-engineered conductive pastes improve electrical efficiency by 24% while reducing material consumption costs by 17% compared to conventional copper-based conductive systems. This measurable performance advantage is reshaping procurement decisions across battery manufacturing, flexible electronics, and semiconductor packaging operations. Asia-Pacific leads in production volume with approximately 47% of global demand concentration, while North America leads in advanced application adoption and innovation intensity, accounting for nearly 31% of high-performance electronics integration projects. Over the next two to three years, manufacturing yields are expected to improve by 18%, while conductive material utilization efficiency is projected to increase by 14% through process optimization and automation.

ESG performance is becoming a competitive differentiator as manufacturers reduce material waste by nearly 15% through precision nanoparticle deployment and advanced formulation techniques, strengthening compliance positioning and lowering operational costs. A recent conductive electronics deployment achieved a 22% improvement in conductivity performance while reducing coating thickness requirements by 13%, demonstrating the practical value of nano copper integration. Investment strategies are increasingly shifting toward capacity expansion, oxidation-resistant product development, and strategic partnerships with battery and semiconductor manufacturers. Companies allocating capital toward scalable production, advanced formulations, and localized supply networks are strengthening their competitive position as the market continues accelerating, transforming, and optimizing global advanced-material value chains.

The Nano Copper Powders Market is undergoing a period of significant transformation driven by advancements in electronics manufacturing, conductive material engineering, energy storage technologies, and high-performance industrial applications. Demand patterns are increasingly influenced by the need for superior conductivity, enhanced thermal management, and material efficiency across semiconductor packaging, printed electronics, and battery systems. Manufacturers are prioritizing oxidation-resistant formulations and scalable production methods to improve commercial viability and operational performance. Simultaneously, regional supply-chain diversification is reshaping sourcing strategies as companies seek greater resilience and localized production capabilities. Innovation in particle-size control, dispersion technology, and automated synthesis is improving product consistency and application flexibility. As competition intensifies, companies are balancing performance enhancement, production economics, and regulatory compliance while expanding partnerships across advanced manufacturing ecosystems. These interconnected forces continue redefining procurement priorities, investment decisions, and long-term competitive positioning throughout the global Nano Copper Powders Market.

The strongest growth engine in the Nano Copper Powders Market is the structural shift toward advanced electronics, high-density semiconductor packaging, and conductive printing technologies. Electronics-related applications now represent approximately 44% of market demand, while adoption of conductive nanomaterials in printed electronics has increased by nearly 28% over recent years. Simultaneously, battery manufacturers are integrating nano copper materials to improve conductivity and energy-transfer efficiency by more than 20%. Global semiconductor localization initiatives and supply-chain restructuring efforts have further accelerated demand by encouraging regional sourcing of advanced materials. The cause-and-effect relationship is clear: greater device miniaturization requires higher-performance conductive materials, which in turn increases nano copper utilization rates. In response, companies are expanding production capacity, accelerating R&D spending, and forming strategic partnerships with electronics manufacturers. Several producers are prioritizing oxidation-resistant nano copper technologies and automated manufacturing systems to improve scalability, strengthen competitive positioning, and capture emerging demand across advanced industrial applications.

Despite strong adoption momentum, material stability and production complexity remain major structural restraints. Nano copper powders are highly susceptible to oxidation, which can reduce conductivity performance by more than 15% under unfavorable storage and processing conditions. Additionally, specialized production processes can increase manufacturing costs by 20–30% compared with conventional copper powder production. Supply concentration also creates risk. Significant portions of advanced nanoparticle production capacity remain concentrated within limited manufacturing clusters, exposing buyers to procurement disruptions during geopolitical or logistics-related disturbances. These constraints directly affect scalability, project timelines, and cost predictability for downstream users. To mitigate these risks, companies are increasingly diversifying supplier networks, securing long-term procurement contracts, and investing in surface-treatment technologies that improve oxidation resistance. Alternative conductive material development and localized production initiatives are also gaining traction. The market's long-term success depends on reducing performance degradation risks while improving production efficiency and supply-chain resilience.

The most attractive opportunity lies in next-generation energy storage, flexible electronics, and advanced conductive printing applications. Flexible electronics deployment has increased by nearly 25%, while demand for conductive materials supporting advanced battery architectures has expanded by more than 22%. These segments are creating new commercial opportunities beyond traditional electronics manufacturing. A powerful innovation shift is emerging through AI-assisted material engineering and precision nanoparticle synthesis, enabling better particle uniformity and higher application performance. This creates a non-obvious advantage: manufacturers can achieve improved conductivity while reducing material intensity and overall production costs. Companies are positioning for future dominance by expanding research programs, building advanced-material ecosystems, and increasing collaboration with semiconductor and battery manufacturers. Regional investment in localized advanced-material production continues accelerating, creating new demand pockets in emerging manufacturing hubs. Businesses capable of combining scalable production, superior material performance, and strategic customer partnerships are increasingly capturing premium opportunities and strengthening long-term market influence.

The primary challenge is achieving large-scale commercial production while maintaining particle consistency, performance reliability, and cost efficiency. Variations in nanoparticle size distribution can impact conductivity performance by more than 12%, while production yield losses can exceed 10% in highly specialized manufacturing environments. These execution barriers directly affect customer confidence and commercial scalability. Regulatory scrutiny surrounding nanomaterials is also increasing across several advanced manufacturing markets, creating additional compliance requirements and extending qualification timelines. Combined with rising quality expectations from semiconductor and battery manufacturers, this is forcing producers to invest heavily in testing, validation, and process control systems. The long-term sustainability of market growth depends on solving these operational challenges without compromising profitability. Companies are responding through automation investments, advanced quality-control platforms, and strategic partnerships with downstream manufacturers. Those capable of delivering consistent performance, scalable production, and regulatory alignment will maintain competitive advantages, while less adaptable suppliers risk losing relevance as industry standards continue evolving.

22% Increase in Oxidation-Resistant Formulations Reshaping Product Development. Manufacturers are rapidly shifting toward surface-engineered nano copper powders, with adoption rising by 22% and product qualification cycles shortening by nearly 15%. Improved oxidation resistance is extending material usability and reducing performance degradation. Companies are expanding specialty product portfolios and strengthening partnerships with electronics manufacturers to capture higher-value applications.

18% Improvement in Automated Nanoparticle Production Efficiency. Automation-driven synthesis platforms are improving production consistency by 18% while reducing batch variability by approximately 12%. Producers are optimizing manufacturing workflows, lowering processing losses, and improving scalability. Rising labor constraints and quality requirements are forcing broader deployment of automated process-control technologies across advanced-material facilities.

27% Growth in Regionalized Supply Agreements Transforming Procurement Models. Companies are increasingly securing localized sourcing contracts, with regional supply agreements increasing by 27% and cross-border procurement dependency declining by 11%. Ongoing supply-chain diversification efforts are reshaping supplier relationships, improving resilience, and reducing operational risk exposure. Businesses are prioritizing long-term partnerships and geographically balanced sourcing strategies.

19% Expansion in Conductive Ink Integration Redefining Commercial Applications. Adoption of nano copper powders within conductive ink formulations has increased by 19%, while material utilization efficiency has improved by nearly 14%. This shift is optimizing printed electronics production, reducing material consumption, and accelerating product customization. Companies are scaling conductive-material portfolios and investing in application-specific formulations to strengthen market differentiation.

The Nano Copper Powders Market is segmented by type, application, and end-user, reflecting the material’s expanding role across advanced manufacturing and high-performance industrial processes. Demand remains concentrated in high-purity nano copper grades due to their superior conductivity and integration capabilities in electronics and energy-storage applications. Approximately 44% of total market demand originates from electronics-related applications, while battery and energy-storage uses account for nearly 26%, highlighting the market’s dependence on advanced conductive technologies. Demand is increasingly shifting toward specialized formulations designed for conductive inks, flexible electronics, and next-generation battery architectures. End-user purchasing behavior is also evolving as manufacturers prioritize material efficiency, oxidation resistance, and supply-chain reliability. This shift is encouraging suppliers to expand production capacity, invest in advanced particle-engineering technologies, and develop application-specific solutions. For decision-makers, understanding where demand is concentrated and where adoption is accelerating remains critical for targeting investment, product development, and commercialization strategies.

High-Purity Nano Copper Powders dominate the market with an estimated 58% share due to their superior electrical conductivity, thermal performance, and compatibility with semiconductor, conductive ink, and battery applications. Their structural advantage lies in delivering higher performance while maintaining integration flexibility across multiple advanced manufacturing processes. Manufacturers continue prioritizing these grades because they support demanding electronic applications where performance consistency is critical. Surface-Coated Nano Copper Powders represent the fastest-growing segment, expanding at an estimated 13.8% growth rate due to increasing demand for oxidation-resistant materials. These products address one of the industry's most significant technical limitations, enabling longer storage life and improved processing efficiency. The comparison between High-Purity and Surface-Coated variants highlights a clear market shift: while high-purity grades maintain dominance through performance leadership, coated variants are capturing demand through durability and operational efficiency advantages. Other specialized nano copper powder types collectively account for approximately 42% of market demand and serve niche applications such as antimicrobial coatings, catalysts, and specialty conductive composites. Companies are responding by expanding advanced-material portfolios, investing in particle-engineering innovation, and increasing production flexibility. Strategic investment is increasingly flowing toward oxidation-resistant and application-specific formulations, while conventional offerings face growing competitive pressure from performance-enhanced alternatives.

Electronics & Conductive Inks lead the market with approximately 44% share due to the widespread use of nano copper powders in printed electronics, semiconductor packaging, conductive pastes, and flexible circuits. Demand concentration exists because these applications require high conductivity, precision performance, and cost-effective alternatives to precious-metal-based conductive materials. Energy Storage & Batteries represent the fastest-growing application segment, recording growth of approximately 14.2% as battery manufacturers increasingly integrate advanced conductive materials to improve charging efficiency and energy transfer performance. Compared with the mature electronics segment, battery-related applications are benefiting from rapid technology evolution and growing electrification initiatives. The remaining applications, including industrial coatings, catalysts, antimicrobial solutions, and advanced composites, account for roughly 56% of demand collectively. Usage patterns are evolving as manufacturers deploy nano copper powders in multifunctional products capable of delivering conductivity, durability, and antimicrobial performance simultaneously. Companies are responding through application-specific product development, strategic customer collaborations, and targeted commercialization efforts. The strongest demand migration is occurring toward energy-related applications, making battery-focused innovation increasingly critical for long-term market positioning.

Electronics & Semiconductor Manufacturers remain the largest end-user segment, accounting for approximately 46% of total demand. Demand concentration is driven by extensive utilization in semiconductor packaging, printed electronics, conductive adhesives, and advanced circuit manufacturing where conductivity and miniaturization are critical competitive factors. Battery & Energy Storage Companies represent the fastest-growing end-user group, expanding by nearly 15%. Growth is fueled by increasing investment in next-generation battery systems and the need for conductive materials that improve charging efficiency and operational performance. Comparing these segments reveals a significant market evolution: semiconductor manufacturers continue driving volume demand, while energy-storage companies are accelerating future growth through emerging application development. Other end-user groups, including industrial manufacturers, healthcare product developers, coatings producers, and research institutions, collectively contribute approximately 54% of market activity. Purchasing behavior is increasingly focused on material performance, supply-chain security, and product customization. Suppliers are responding through tailored product offerings, strategic partnerships, and advanced technical support programs. Future demand is clearly shifting toward energy-transition applications, creating significant opportunities for companies capable of delivering scalable, high-performance nano copper solutions.

Asia-Pacific accounted for the largest market share at 47% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 11.4% between 2026 and 2033.

Regional performance reflects significant differences in manufacturing scale, technology adoption, and investment intensity. Asia-Pacific maintains leadership with 47% market share due to its dominant electronics, battery, and semiconductor production ecosystem. North America accounts for approximately 26% of demand and is accelerating through advanced manufacturing investments and semiconductor reshoring initiatives. Europe contributes around 19%, supported by high-value industrial applications and sustainability-focused material innovation. South America represents 4.5% of the market, while the Middle East & Africa holds 3.5% as infrastructure modernization increases advanced material adoption. Supply-chain diversification and regional manufacturing localization continue reshaping global competitive dynamics. As a result, companies are increasingly focusing investments on Asia-Pacific production capacity while expanding innovation and commercialization activities across North America and Europe.

North America accounts for approximately 26% of global market demand and remains one of the most strategically important regions for advanced nano copper adoption. Demand is concentrated within semiconductor manufacturing, conductive electronics, battery systems, and advanced aerospace applications. Semiconductor localization initiatives and supply-chain resilience programs are accelerating regional procurement of advanced conductive materials. Adoption of automated materials engineering and precision manufacturing technologies has increased by nearly 18%, improving commercialization rates across high-performance applications. Several producers have expanded advanced-material production capacity by more than 15% since 2024 to support growing demand. Enterprise buyers increasingly prioritize reliability, technical performance, and local supply security over lowest-cost sourcing. These factors continue making the region a preferred destination for technology investment, production expansion, and innovation-driven commercialization strategies.

Europe represents approximately 19% of global demand, with strong contributions from Germany, France, Italy, and the Netherlands. Regulatory emphasis on material efficiency, circular manufacturing, and sustainable industrial processes is significantly influencing procurement decisions. Nearly 37% of advanced-material development programs in the region incorporate sustainability-linked performance objectives. Manufacturers are increasingly adopting oxidation-resistant nano copper formulations that reduce material losses and improve operational efficiency. Product qualification activities linked to sustainable manufacturing initiatives have increased by approximately 14% over recent years. Enterprise customers demonstrate a quality-first and compliance-driven purchasing approach, prioritizing long-term performance and regulatory alignment. As environmental standards continue tightening, the region is forcing suppliers to innovate faster, creating a competitive environment where technological differentiation and sustainability performance are becoming inseparable.

Asia-Pacific commands approximately 47% of global market demand and remains the undisputed leader in production volume and manufacturing capacity. China, Japan, South Korea, and India serve as the primary growth engines due to their extensive electronics, battery, and semiconductor ecosystems. The region benefits from integrated supply chains, cost-efficient manufacturing, and large-scale commercialization capabilities. More than 60% of regional nano copper production supports electronics and energy-storage applications. Localized production investments have increased by nearly 20% as manufacturers strengthen supply-chain resilience and expand export capabilities. Enterprise buyers prioritize scale, speed, and production efficiency, enabling rapid adoption of advanced materials. For companies seeking global expansion and volume growth, Asia-Pacific remains the most critical region for capacity scaling and market penetration.

South America accounts for approximately 4.5% of global demand, with Brazil and Argentina representing the largest opportunities. Industrial manufacturing, energy infrastructure projects, and expanding electronics assembly activities are supporting gradual market development. However, infrastructure limitations and advanced-material import dependency continue creating cost pressures and supply challenges. Material procurement costs can be 12–18% higher than those in major manufacturing regions due to logistics and distribution constraints. Despite these limitations, localized adoption has increased by nearly 11% as regional manufacturers pursue higher-performance materials. Businesses remain highly price-sensitive and prioritize solutions delivering measurable operational benefits. The region presents a balanced opportunity-risk profile, where strategic partnerships and localized supply initiatives can unlock long-term competitive advantages.

The Middle East & Africa region contributes approximately 3.5% of global market demand, led by the United Arab Emirates, Saudi Arabia, and South Africa. Demand is increasingly linked to industrial diversification programs, infrastructure modernization, electronics manufacturing initiatives, and advanced construction materials. Regional investment in industrial transformation projects has increased by approximately 16%, supporting broader adoption of advanced conductive materials. Technology deployment within industrial manufacturing environments has accelerated as enterprises pursue operational efficiency and modernization goals. Strategic partnerships and industrial development initiatives continue expanding access to advanced materials across key markets. Buyers prioritize performance, reliability, and long-term project value. As infrastructure investment and industrial transformation efforts continue expanding, the region is emerging as an important long-term growth opportunity.

China – 39% Market Share: Dominates through its massive electronics manufacturing base, battery production capacity, integrated supply chains, and large-scale advanced materials ecosystem.

United States – 18% Market Share: Maintains strong leadership through semiconductor innovation, advanced manufacturing investments, defense applications, and high adoption of next-generation conductive technologies.

The Nano Copper Powders Market is characterized by competition between advanced-material innovators, specialty nanomaterial suppliers, and large-scale powder manufacturers. Key participants such as American Elements, NanoAmor, Nanoshel, Hongwu International Group, and SkySpring Nanomaterials compete across electronics, conductive inks, battery materials, and industrial coatings applications. The top five players collectively account for approximately 34% of global market activity, indicating a moderately fragmented but technology-driven competitive structure.

Competition is increasingly centered on conductivity performance, oxidation resistance, customization capability, and supply-chain reliability rather than price alone. Advanced oxidation-resistant formulations improve storage stability by over 20%, while automated production processes enhance batch consistency by nearly 18%. Leading suppliers are investing in capacity expansion, customer-specific formulations, strategic partnerships, and vertical integration to secure long-term contracts with electronics and battery manufacturers.

A major competitive shift is occurring toward proprietary surface-treatment technologies and localized supply networks as customers seek resilient sourcing alternatives. High technical qualification requirements, product validation timelines exceeding 12 months in some applications, and manufacturing complexity remain significant entry barriers. Winning in this market requires scalable production, differentiated material performance, strong customer integration, and reliable regional supply capabilities.

NanoAmor

Nanoshel LLC

Hongwu International Group Ltd.

SkySpring Nanomaterials Inc.

Sumitomo Metal Mining Co., Ltd.

EPRUI Nanoparticles & Microspheres Co. Ltd.

Tekna Holding ASA

Inframat Advanced Materials LLC

Nanografi Nano Technology

Strem Chemicals

US Research Nanomaterials Inc.

PlasmaChem GmbH

Nanostructured & Amorphous Materials Inc.

Nano copper powder technology is rapidly advancing from basic conductive-material production toward engineered nanoparticle platforms optimized for electronics, energy storage, and advanced manufacturing. Current commercial technologies focus on chemical reduction synthesis, plasma-assisted production, and controlled particle-size engineering. Manufacturers utilizing advanced particle-control systems report conductivity improvements of 18–24% and material utilization gains approaching 15%. Nearly 52% of high-performance electronics applications now prioritize nano-engineered conductive materials over conventional copper powders due to superior electrical performance and miniaturization compatibility.

Emerging technologies are centered on oxidation-resistant surface treatments, AI-assisted materials engineering, and precision nanoparticle dispersion systems. Surface-engineered nano copper formulations can improve storage stability by more than 20% while reducing performance degradation during manufacturing. Adoption of automated synthesis platforms has increased by approximately 17%, enabling higher production consistency and lower defect rates. These capabilities provide significant operational advantages for semiconductor, battery, and conductive ink manufacturers seeking predictable performance.

A key technology comparison is reshaping market priorities. Advanced oxidation-resistant nano copper powders improve long-term conductivity retention by nearly 25% while reducing material losses by approximately 16% compared with conventional uncoated nano copper materials. Suppliers capable of commercializing these next-generation products gain stronger access to premium electronics and energy-storage markets.

Between 2026 and 2028, commercialization of AI-optimized material design, scalable continuous-flow synthesis, and advanced conductive paste technologies is expected to accelerate. Companies investing early in automation, particle engineering, and oxidation-control technologies will capture stronger competitive positioning as performance requirements continue increasing across advanced manufacturing industries.

September 2025 – Sumitomo Metal Mining announced the development of a 100nm oxidation-resistant nano copper powder designed for power semiconductor bonding applications. The company also accelerated customer evaluations of its 200nm grade while preparing for commercial-scale production. The innovation strengthens high-performance electronics adoption and product differentiation. [Oxidation Breakthrough] Source: www.smm.co.jp

November 2025 – Critical Metals Corp (CRML) secured one of the largest strategic stockpiles of ultra-high-purity copper powder through a US$20 million acquisition, including 40 kilograms of 99.96% purity material. The move strengthens supply availability for defense, aerospace, and advanced technology sectors while enhancing Western supply-chain resilience. [Strategic Stockpile]

November 2025 – Equispheres launched its new oxygen-free Cu-OF (C10200) copper powder portfolio for additive manufacturing. Validation testing demonstrated high flowability, high sphericity, and improved processability for serial production environments. The development supports aerospace, semiconductor, and automotive applications requiring precision metal printing performance. [AM Material Launch]

December 2025 – Continuum Powders expanded its portfolio with CuNi 70/30 powder solutions engineered for marine, energy, and industrial applications. Produced using its proprietary Melt-to-Powder process, the materials deliver enhanced corrosion resistance and conductivity while supporting sustainable manufacturing through reclaimed feedstock utilization. [Portfolio Expansion]

This report provides comprehensive coverage of the Nano Copper Powders Market across major product categories, application areas, end-user industries, regional markets, and emerging technology ecosystems. The study evaluates market performance across nano copper powder types, electronics and conductive ink applications, energy-storage deployments, industrial coatings, advanced composites, and other specialized uses. Geographic coverage includes North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, while assessing manufacturing concentration, adoption trends, and regional demand patterns. Advanced technologies analyzed include oxidation-resistant nano copper formulations, precision nanoparticle synthesis, conductive paste engineering, and automated production systems.

The report delivers deep analytical insight through evaluation of more than 10 major industry participants, multiple application categories, and region-specific adoption indicators. Electronics-related applications account for approximately 44% of demand, while Asia-Pacific contributes nearly 47% of market consumption, providing critical benchmarks for strategic assessment. The analysis also examines emerging usage patterns, supply-chain localization trends, and advanced manufacturing adoption rates exceeding 20% in selected high-growth applications.

From a strategic perspective, the report supports investment planning, product-development prioritization, geographic expansion decisions, competitive benchmarking, and partnership evaluation. It also identifies emerging technology opportunities, evolving customer requirements, and future industry developments expected to influence market positioning and commercial success between 2026 and 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 450.8 Million |

| Market Revenue (2033) | USD 980.5 Million |

| CAGR (2026–2033) | 10.2% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | American Elements; NanoAmor; Nanoshel LLC; Hongwu International Group Ltd.; SkySpring Nanomaterials Inc.; Sumitomo Metal Mining Co., Ltd.; EPRUI Nanoparticles & Microspheres Co. Ltd.; Tekna Holding ASA; Inframat Advanced Materials LLC; Nanografi Nano Technology; Strem Chemicals; US Research Nanomaterials Inc.; PlasmaChem GmbH; Nanostructured & Amorphous Materials Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |