Reports

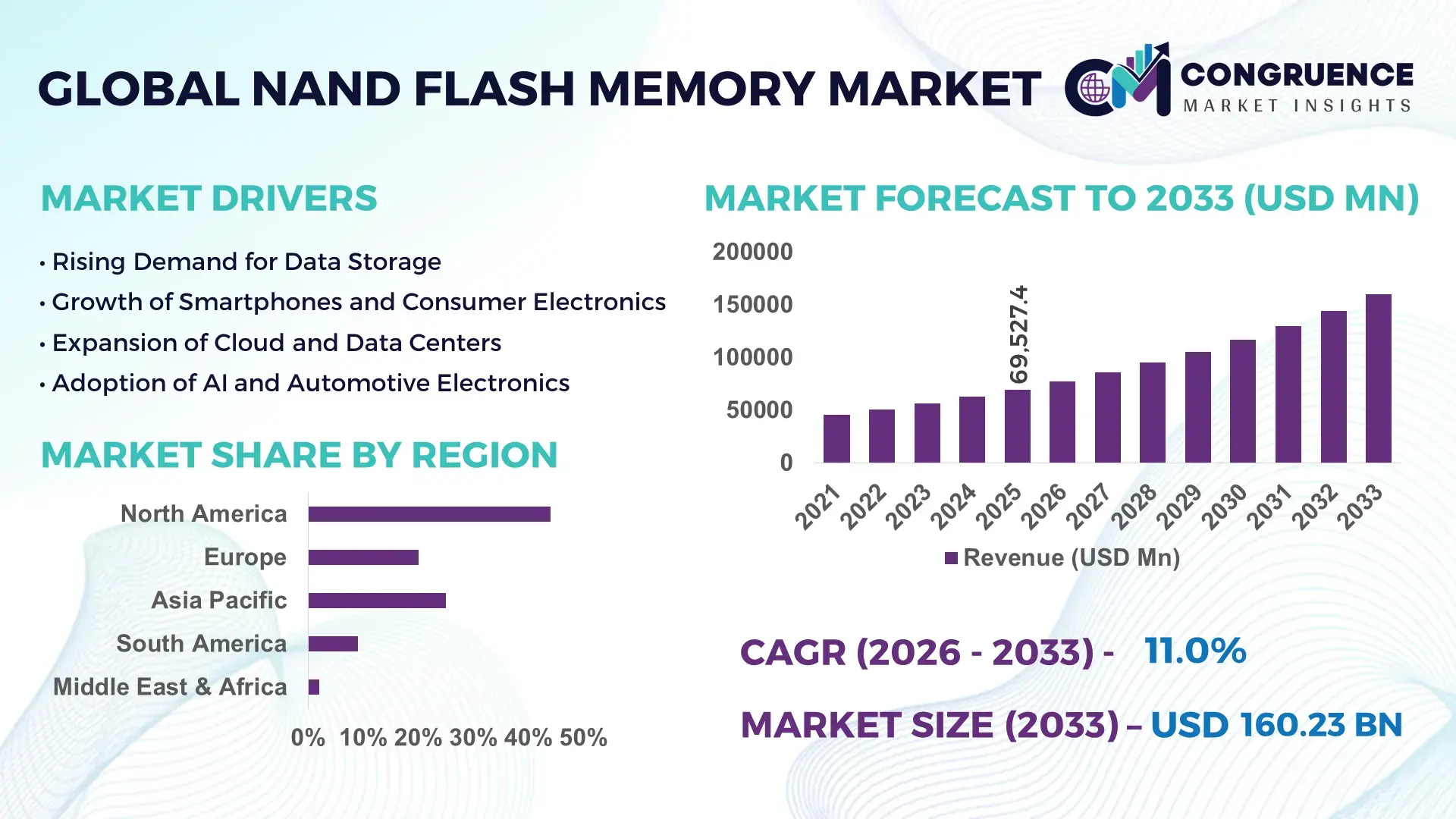

The Global NAND Flash Memory Market was valued at USD 69527.4 Million in 2025 and is anticipated to reach a value of USD 160228 Million by 2033 expanding at a CAGR of 11% between 2026 and 2033. This growth is propelled by escalating demand for high-capacity storage in data centers, smartphones, and AI-powered applications, alongside ongoing innovation in 3D NAND technologies.

Asia-Pacific continues as the central hub for NAND flash memory manufacturing, housing major fabrication facilities across South Korea, Japan, China, and Taiwan that collectively account for the largest portion of global output and exports. Investment by leading players has driven advanced 3D NAND layer counts beyond 200+, and production ecosystems in Seoul and Tokyo report near-maximum capacity utilization rates, reflecting deep vertical integration from wafers to SSD products. In China, smartphone and electronics assembly demand has driven hundreds of billions of gigabytes of NAND consumption annually, while South Korean fabs sustain large volumes of enterprise and consumer storage devices.

Market Size & Growth: Market valued at USD 69,527.4M in 2025; projected to reach USD 160,228M by 2033 at an 11% CAGR driven by data center, mobile, and SSD demand.

Top Growth Drivers: Smartphone storage adoption (~40%+ NAND consumption), enterprise SSD deployment (~30%+), AI and cloud workload expansion (~25%+).

Short-Term Forecast: By 2028, average NAND storage density per device expected to increase by more than 30%, enhancing capacity performance.

Emerging Technologies: 3D NAND with >200 layers, QLC/TLC architecture evolution, advanced controller integration.

Regional Leaders: Asia-Pacific (~USD 80B by 2033; electronics manufacturing force), North America (~USD 45B by 2033; cloud & enterprise focus), Europe (~USD 25B by 2033; automotive & IoT uptake).

Consumer/End-User Trends: Strong uptake in smartphones, laptops, automotive infotainment, and edge devices with a shift toward high-density, energy-efficient storage.

Pilot or Case Example: 2025 industry pilot drives SSD performance gains with >20% reduction in latency in enterprise storage deployments.

Competitive Landscape: Market leader Samsung Electronics (≈33% share), followed by SK Hynix, Micron Technology, Kioxia, Western Digital.

Regulatory & ESG Impact: Semiconductor policies and incentives expanding regional manufacturing; environmental measures prioritize energy-efficient memory solutions.

Investment & Funding Patterns: Global NAND capacity investments exceeding USD 50B with expanded fabrication and packaging facilities underway.

Innovation & Future Outlook: Innovations include vertically stacked NAND, next-gen controllers, and high-performance enterprise solutions shaping long-term demand.

Asia-Pacific’s demand for NAND flash continues to be driven by key industry sectors such as consumer electronics, data centers, automotive electronics, and industrial IoT, with smartphones and SSDs comprising significant usage segments. Recent product innovations include multi-layer 3D NAND with enhanced bit density and improved reliability, while emerging trends see increased adoption of low-power solutions and advanced controller technologies. Regulatory incentives in major manufacturing countries further enable capacity scaling, and regional consumption patterns reflect fast growth in emerging economies, reinforcing a positive future outlook for storage technology adoption and ecosystem expansion.

The NAND Flash Memory Market holds strategic relevance as the foundational storage layer for digital infrastructure spanning hyperscale data centers, enterprise IT systems, smartphones, automotive electronics, and AI computing platforms. Advanced 3D NAND architectures now deliver up to 18% improvement in cost-per-bit efficiency compared to earlier low-layer 3D and planar NAND standards, enabling higher storage densities within constrained power envelopes. Asia-Pacific dominates in volume, while North America leads in adoption with over 60% of large enterprises and hyperscale operators standardizing high-performance SSD arrays. By 2028, AI-optimized storage management is expected to improve data throughput by 30% while reducing latency in enterprise environments.

Strategically, NAND flash underpins data-driven business models as global data creation continues expanding at double-digit rates. Manufacturers are aligning with compliance and sustainability objectives; firms are committing to ESG improvements such as 20% fabrication emission reductions and 25% materials recycling targets by 2030. In 2025, a major memory producer achieved a 40% endurance improvement in enterprise SSDs through AI-driven wear-leveling algorithms, illustrating measurable operational gains. Future pathways include wider QLC and emerging PLC adoption, controller-level AI acceleration, and integration into edge AI, autonomous mobility, and industrial IoT. The NAND Flash Memory Market is increasingly positioned as a pillar of resilience, compliance, and sustainable digital growth.

Enterprise digital transformation and cloud migration are major drivers of NAND Flash Memory demand. Hyperscale data centers increasingly rely on SSD-based architectures to meet latency requirements for AI inference, analytics, and virtualization workloads. Enterprise SSD deployments now account for a substantial share of data center storage arrays, with flash adoption rates exceeding 70% in performance-sensitive applications. Compared to traditional hard drives, NAND-based storage delivers up to 100× faster input/output operations per second and significantly lower power consumption per workload. The rapid expansion of SaaS platforms, real-time analytics, and containerized applications further amplifies the need for high-density, high-endurance NAND solutions. As enterprises modernize infrastructure to support hybrid and multi-cloud environments, NAND flash becomes a core enabler of workload consolidation, system responsiveness, and data center energy optimization.

NAND Flash production depends on highly specialized semiconductor fabrication facilities, many of which are concentrated in a limited number of geographic clusters. This concentration increases vulnerability to disruptions from geopolitical issues, natural events, and logistical bottlenecks. Advanced 3D NAND manufacturing requires extreme precision in multilayer stacking, high-aspect-ratio etching, and advanced lithography, making yield optimization increasingly challenging as layer counts rise. Equipment lead times often extend beyond 12 months, limiting rapid capacity expansion. Additionally, specialty materials such as high-purity gases and advanced photoresists face supply constraints, adding volatility to production planning. These structural complexities restrict supply flexibility, elevate operational risk, and can create imbalances between supply and demand cycles within the NAND Flash Memory Market.

The proliferation of IoT devices and edge computing infrastructure creates new demand vectors for NAND Flash Memory beyond traditional PCs and servers. Industrial automation systems, smart cities, connected healthcare devices, and autonomous vehicles increasingly require local, high-speed non-volatile storage for real-time processing. Edge AI systems benefit from NAND’s low latency and durability, enabling faster data filtering before cloud transmission. Modern vehicles integrate advanced infotainment, driver-assistance systems, and navigation platforms that depend on reliable flash storage. The global rollout of 5G further expands data generation at network edges, increasing the need for distributed storage nodes. These trends open opportunities for ruggedized, low-power NAND solutions tailored to industrial, automotive, and telecom environments, diversifying application portfolios and strengthening long-term market potential.

As manufacturers push NAND stacking beyond 200 layers and adopt multi-bit cell designs such as QLC, physical and electrical challenges intensify. Higher layer counts introduce heat dissipation constraints, cell-to-cell interference, and tighter process tolerances, affecting yield and reliability. Endurance limitations of high-density cells require advanced error correction and controller innovations, increasing design complexity. Simultaneously, the market is characterized by pronounced pricing cycles; periods of oversupply can drive double-digit percentage declines in average selling prices, while tight supply phases produce rapid price increases. This volatility complicates procurement planning for device makers and data center operators. Balancing cost efficiency, performance reliability, and scaling feasibility remains a persistent strategic challenge for participants in the NAND Flash Memory Market.

• Over 200-Layer 3D NAND Adoption Accelerates Density Gains: Manufacturers are rapidly transitioning to 200+ layer 3D NAND architectures, enabling up to 35% higher bit density per wafer compared to earlier 120–150 layer designs. This shift improves storage capacity per device by nearly 30% while lowering energy consumption per bit by approximately 15%, strengthening deployment in hyperscale and enterprise storage systems.

• Enterprise SSD Shift Toward QLC Increases Capacity per Drive: Quad-Level Cell (QLC) NAND adoption in enterprise SSDs has expanded, with QLC-based drives now representing more than 25% of new data center SSD deployments. QLC enables up to 33% greater storage capacity per die compared to TLC while reducing cost per terabyte by nearly 20%, supporting archival, AI training datasets, and high-capacity cloud storage tiers.

• Automotive and Edge Device NAND Usage Surges Beyond 40% Growth in Unit Integration: Modern vehicles and edge AI systems increasingly embed NAND flash for infotainment, navigation, and real-time analytics. Advanced vehicles now integrate 2–4× more flash storage than models five years ago, with automotive-grade NAND shipments rising over 40% in unit volume as software-defined vehicle architectures expand.

• AI-Driven Controller Optimization Improves SSD Lifespan and Performance: Storage controllers integrating AI-based wear-leveling and error management algorithms have demonstrated up to 25% improvement in SSD endurance and 20% reduction in latency under enterprise workloads. These advancements extend device lifecycle by several years, reducing replacement frequency and improving total cost of ownership for large-scale storage deployments.

The NAND Flash Memory market segmentation reflects demand patterns shaped by storage density needs, endurance requirements, and workload intensity. By type, the market is structured around SLC, MLC, TLC, and QLC technologies, each serving distinct performance and cost tiers. TLC remains dominant due to its balance between endurance and density, while QLC is expanding for high-capacity storage environments. Application segmentation shows strong concentration in enterprise SSDs, smartphones, and data center infrastructure, with emerging uptake in automotive and edge computing. End-user segmentation indicates hyperscale cloud operators and consumer electronics manufacturers as primary consumers, while industrial and automotive users are increasing integration levels. Device-level storage capacity has risen by over 25% in recent generations, and enterprise flash adoption rates now exceed 70% in performance-centric environments, reflecting the industry’s shift from mechanical storage to solid-state architectures optimized for speed, durability, and power efficiency.

TLC (Triple-Level Cell) NAND currently leads the product landscape, accounting for approximately 48% of total NAND flash adoption due to its balance of performance, endurance, and cost efficiency. Compared with MLC’s 22% share, TLC enables about 50% higher storage density while maintaining acceptable write endurance for mainstream enterprise and consumer SSDs. QLC (Quad-Level Cell) holds roughly 20% adoption, while SLC and specialized industrial-grade variants together contribute nearly 10% for high-endurance applications. QLC is the fastest-growing type, expanding at an estimated 14% CAGR, driven by demand for high-capacity storage in hyperscale data centers where read-intensive workloads dominate. QLC offers up to 33% higher density per cell than TLC, lowering cost per terabyte for archival and AI dataset storage. Meanwhile, SLC remains vital in industrial automation and defense electronics where write cycles exceed 50,000 program/erase cycles.

Enterprise SSDs represent the leading application, accounting for nearly 40% of NAND flash utilization as organizations migrate to flash-optimized data architectures. Smartphones follow with approximately 32% share, reflecting continued integration of 128 GB to 512 GB storage configurations in mainstream devices. However, automotive and edge computing applications are the fastest-growing segment, expanding at roughly 15% CAGR, supported by rising in-vehicle data processing, advanced driver assistance systems, and localized AI analytics. Automotive-grade NAND deployment per vehicle has increased 3× over five years, while edge nodes supporting 5G networks require low-latency storage for real-time data processing. Remaining applications—including PCs, tablets, and industrial IoT—collectively contribute about 28% of usage.

Hyperscale cloud service providers are the leading end-users, representing around 38% of NAND flash demand due to large-scale SSD array deployments supporting AI, analytics, and virtualized workloads. Consumer electronics manufacturers account for roughly 34%, driven by smartphones, laptops, and gaming devices integrating higher-capacity storage. Automotive OEMs are the fastest-growing end-user group, expanding at nearly 16% CAGR as software-defined vehicles require multi-terabyte onboard storage for infotainment and sensor data processing. Industrial and telecom sectors collectively hold about 28%, with flash adoption rates exceeding 60% in edge network nodes and industrial control systems requiring fast data buffering.

Asia-Pacific accounted for the largest market share at 54% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 13% between 2026 and 2033.

Asia-Pacific’s leadership is supported by the concentration of semiconductor fabrication facilities, advanced packaging ecosystems, and electronics manufacturing clusters producing over 70% of global solid-state storage devices. China, South Korea, and Japan collectively contribute more than 60% of global NAND wafer output, while regional smartphone manufacturing exceeds 1 billion units annually, each integrating flash storage ranging from 128 GB to 512 GB. North America’s growth momentum is driven by hyperscale cloud expansion, where enterprise SSD adoption in data centers surpasses 75% in performance-tier storage arrays. Europe holds roughly 17% share, supported by automotive electronics integration, while South America and the Middle East & Africa together account for about 9%, reflecting emerging infrastructure digitization and mobile device penetration exceeding 68% in urban populations. Regional demand variations show higher enterprise storage density in developed markets, while emerging regions emphasize mobile and consumer electronics applications.

How Is Enterprise Digital Transformation Reshaping High-Performance Storage Demand?

North America represents approximately 24% of global NAND flash consumption, largely driven by hyperscale data centers, enterprise IT modernization, and AI computing infrastructure. Key industries include healthcare analytics, financial services, cloud service providers, and media streaming platforms that rely on low-latency SSD storage for real-time processing. Government-backed semiconductor incentives and technology modernization policies encourage domestic research and fabrication investments. Enterprise flash storage penetration exceeds 70% in mission-critical workloads, while AI training clusters increasingly deploy multi-petabyte flash arrays. A prominent regional memory technology firm has expanded advanced SSD controller development, achieving around 20% performance-per-watt improvement in data center deployments. Consumer behavior shows strong enterprise procurement patterns, particularly in healthcare and finance sectors where data compliance and performance reliability drive purchasing decisions.

How Are Sustainability Policies Influencing Advanced Storage Adoption?

Europe accounts for nearly 17% of the NAND flash market, with Germany, the UK, and France serving as major demand centers. Automotive electronics and industrial automation systems represent significant drivers, as advanced vehicles integrate 3× more onboard storage than five years ago. Regional sustainability regulations promote energy-efficient data center operations, leading to preference for SSDs that reduce power usage by up to 30% compared to mechanical drives. Digital transformation initiatives across manufacturing sectors accelerate adoption of flash-based industrial control systems. A European semiconductor equipment firm has increased local support for advanced memory testing solutions, improving manufacturing yield monitoring by 18%. Consumer and enterprise buyers in this region emphasize regulatory compliance, long product lifecycles, and environmentally responsible technology procurement.

What Makes High-Volume Electronics Production a Storage Growth Engine?

Asia-Pacific leads global NAND flash production and consumption, exceeding 50% of total market volume. China, Japan, South Korea, and India represent the largest consuming countries, supported by electronics manufacturing exceeding hundreds of millions of devices annually. Regional infrastructure includes advanced semiconductor fabs, assembly plants, and packaging hubs that supply global SSD and mobile device markets. Innovation hubs in Seoul, Tokyo, and Shenzhen drive rapid transitions to multilayer NAND exceeding 200 layers. A leading regional manufacturer recently enhanced production efficiency by 15% through advanced wafer inspection automation. Consumer behavior reflects strong mobile device demand, e-commerce platform usage, and rapid adoption of AI-enabled applications that require high-capacity embedded storage.

How Is Infrastructure Digitization Expanding Storage Needs?

South America contributes roughly 5% of global NAND flash demand, with Brazil and Argentina as leading markets. Growth is associated with telecom infrastructure upgrades, digital banking expansion, and increased cloud adoption among enterprises. Government technology incentives and trade agreements support electronics imports and local assembly operations. Data center capacity in major urban centers has grown by over 20% in recent years, increasing SSD integration in enterprise systems. A regional technology integrator has deployed flash-based storage systems in over 200 financial institutions, improving transaction processing speeds by 18%. Consumer patterns show rising smartphone storage adoption and increased demand for localized digital media platforms.

How Is Digital Modernization Driving High-Speed Storage Deployment?

The Middle East & Africa region represents close to 4% of global NAND flash consumption, with the UAE and South Africa as key growth markets. Oil and gas digitalization, smart city projects, and cloud infrastructure investments fuel demand for high-reliability SSD storage. Regional technology modernization includes government-backed digital transformation strategies and data localization policies supporting domestic data center expansion. A regional telecom operator recently integrated flash-based edge storage across more than 1,000 network nodes, improving data processing efficiency by 22%. Consumer adoption trends show rising use of mobile banking, video streaming, and e-commerce platforms requiring higher device storage capacities.

China NAND Flash Memory Market – 28% share: Strong electronics manufacturing base and large-scale device assembly operations drive substantial NAND consumption.

South Korea NAND Flash Memory Market – 21% share: Advanced semiconductor fabrication infrastructure and leadership in memory technology production support dominant market positioning.

The NAND Flash Memory market exhibits a highly consolidated structure, with fewer than 10 major global manufacturers controlling most advanced fabrication capacity. The top five companies collectively account for approximately 85% of global NAND output, reflecting high barriers to entry driven by capital requirements exceeding USD 10 billion for leading-edge fabrication facilities and process nodes below 20 nm equivalent. Competitive positioning is defined by technology leadership in 3D NAND stacking beyond 200 layers, controller integration capabilities, and cost-per-bit efficiency improvements of 15–20% per technology generation.

Strategic initiatives include joint ventures for fabrication sharing, long-term supply agreements with hyperscale cloud operators, and co-development of enterprise SSD platforms. Product innovation cycles average 12–18 months, with vendors introducing higher-density QLC solutions and PCIe Gen5 SSDs delivering over 14 GB/s throughput. Mergers, asset transfers, and capacity realignments have further concentrated supply. R&D intensity remains high, with leading firms allocating around 8–10% of annual budgets to memory process innovation. Competition increasingly focuses on endurance optimization, AI-enhanced storage management, and energy efficiency, with enterprise customers prioritizing SSD lifespan extensions exceeding 25% and power-per-terabyte reductions near 20%.

Samsung Electronics

SK hynix

Micron Technology

Kioxia Holdings Corporation

Western Digital Corporation

Solidigm

Yangtze Memory Technologies Co. (YMTC)

Intel Corporation

Toshiba Corporation

Powerchip Semiconductor Manufacturing Corporation (PSMC)

Macronix International

Winbond Electronics

Technological progress in the NAND Flash Memory market is centered on multilayer 3D NAND scaling, controller intelligence, interface evolution, and materials engineering. Leading manufacturers have surpassed 200-layer stacking, with some development pipelines targeting over 300 layers, enabling up to 30–40% higher bit density per wafer compared to 176-layer generations. This vertical scaling improves storage capacity per die while reducing cost-per-bit and power consumption per stored gigabyte by nearly 15%. However, higher layer counts demand advanced etching precision and stress-control techniques to maintain signal integrity and endurance.

Cell architecture evolution from TLC to QLC has increased bits per cell from 3 to 4, raising theoretical density by 33%. QLC now supports read-intensive enterprise workloads, while controller-level error correction technologies such as LDPC (Low-Density Parity-Check) coding enhance reliability, extending SSD lifespan by over 20% in some enterprise environments. Emerging PLC (Penta-Level Cell) research aims to store 5 bits per cell, potentially increasing density another 25%, though endurance optimization remains a technical focus.

Interface technologies are also advancing. PCIe Gen5 SSDs now deliver throughput exceeding 14 GB/s, nearly double Gen4 performance, supporting AI training and high-performance computing clusters. NVMe protocol optimization reduces latency to below 20 microseconds in enterprise systems. Meanwhile, Zoned Namespace (ZNS) SSD architectures improve write efficiency by up to 30% in large-scale data centers by minimizing write amplification.

AI integration within storage controllers enables predictive wear-leveling and workload-aware caching, improving endurance by approximately 25% and reducing latency variability. Additionally, innovations in packaging, such as chiplet-based SSD architectures and advanced thermal dissipation materials, help maintain performance stability under sustained workloads. Collectively, these technologies strengthen scalability, efficiency, and reliability across enterprise, mobile, and edge computing environments.

• In July 2024, Micron Technology began volume production of its ninth-generation NAND flash technology, featuring G9 TLC NAND capable of 3.6 GB/s transfer speeds and up to 73% higher density than competing technologies, supporting AI, edge, and enterprise storage applications with enhanced bandwidth and efficiency. (Micron Technology)

• In August 2025, SK hynix commenced mass production of industry-first 321-layer QLC NAND flash, doubling integration density and improving write performance by up to 56% and read speeds by approximately 18%, aimed at high-capacity SSDs for AI server and enterprise storage. (SK hynix Newsroom -)

• In September 2025, NAND flash contract prices were projected to rise 5–10% in 4Q25 as enterprise SSD demand increased and production adjustments reduced inventories, with SanDisk announcing a 10% price increase and broader supplier pricing realignments in response to robust QLC demand. (TrendForce)

• In September 2025, Sandisk and SK hynix formalized a memorandum of understanding to jointly define High Bandwidth Flash (HBF) technology standards, with sample deliveries expected in the second half of 2026 and the first AI-inference memory devices anticipated by early 2027. (TrendForce)

The scope of the NAND Flash Memory Market Report encompasses a comprehensive examination of product technologies, application sectors, regional footprints, and end-user landscapes that influence strategic planning and investment decisions. Coverage includes detailed segmentation by technology types such as SLC, MLC, TLC, QLC, and emerging PLC, with an emphasis on technical attributes like cell architecture, layer count, interface standards, and controller innovations. Application segments span enterprise SSDs, data center infrastructure, mobile devices, automotive storage, industrial IoT, and edge computing platforms, capturing device-specific storage requirements and workload characteristics.

Geographically, the report analyzes key regional markets including North America, Europe, Asia-Pacific, South America, and Middle East & Africa, evaluating production ecosystems, consumption patterns, infrastructure investments, and regulatory environments. Technology focus areas include 3D NAND stacking beyond 200 layers, AI-enabled storage controllers, PCIe/NVMe interface advancements, zoned storage architectures, and high-bandwidth flash initiatives shaping future capabilities. End-user insights cover cloud service providers, hyperscale data centers, enterprise IT, consumer electronics manufacturers, automotive OEMs, and telecom/edge infrastructure developers. Emerging and niche segments such as HBF technology, UFS enhancements for mobile AI, ruggedized industrial flash, and localized storage for smart city deployments are also explored to provide a nuanced view of opportunities and technology adoption curves across the global NAND Flash Memory market ecosystem. The report equips decision-makers with actionable trends, technology benchmarks, competitive mapping, and strategic implications across diverse market dimensions.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

11% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Samsung Electronics , SK hynix, Micron Technology , Kioxia Holdings Corporation, Western Digital Corporation, Solidigm, Yangtze Memory Technologies Co. (YMTC), Intel Corporation, Toshiba Corporation, Powerchip Semiconductor Manufacturing Corporation (PSMC), Macronix International, Winbond Electronics |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |