Reports

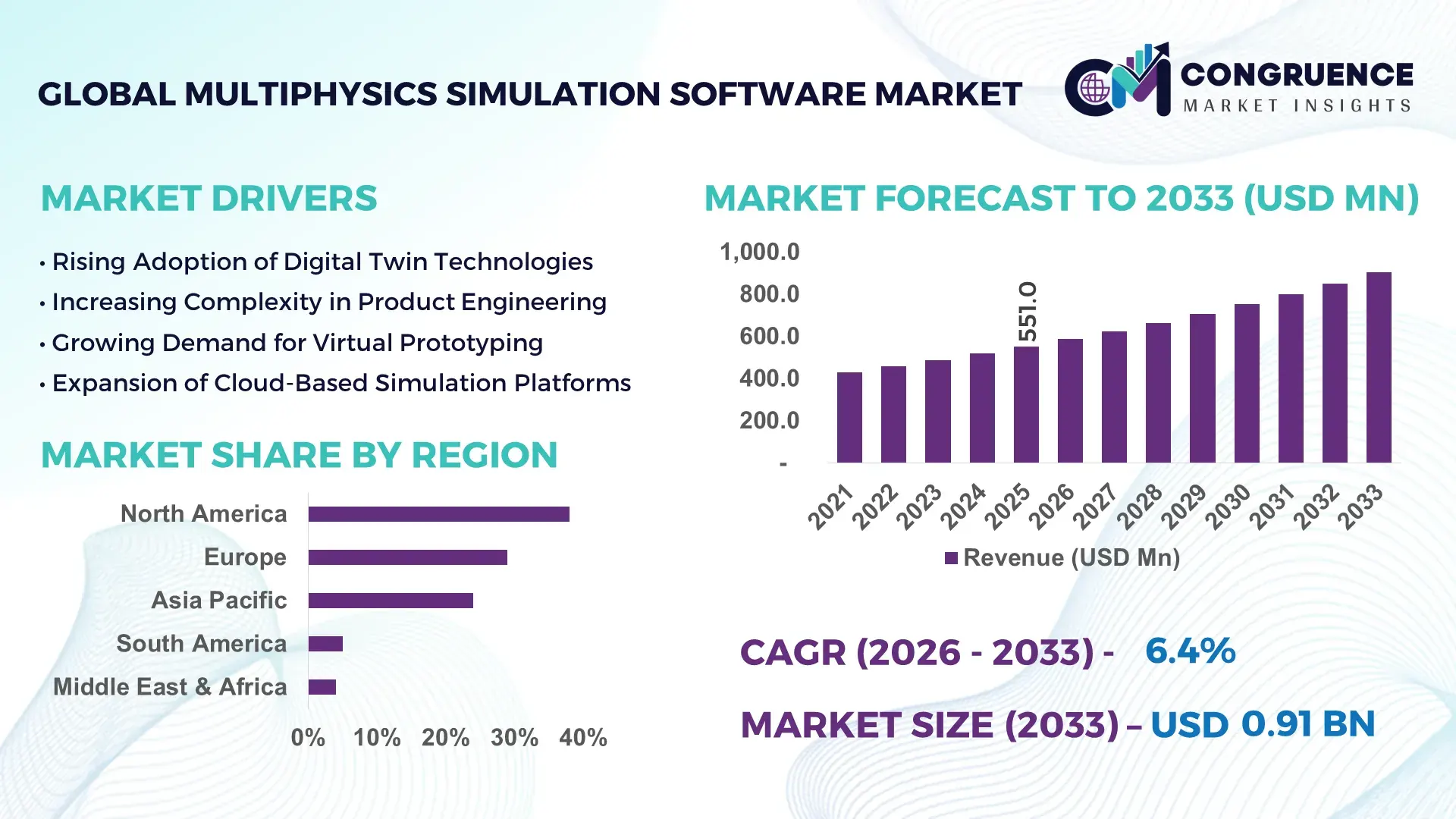

The Global Multiphysics Simulation Software Market was valued at USD 551.0 Million in 2025 and is anticipated to reach a value of USD 905.1 Million by 2033 expanding at a CAGR of 6.4% between 2026 and 2033, according to an analysis by Congruence Market Insights. The market is primarily driven by the accelerating integration of advanced digital engineering tools across aerospace, automotive, electronics, and energy sectors to reduce prototyping costs and shorten product development cycles.

The United States remains the dominant country in the Multiphysics Simulation Software Market, supported by strong R&D intensity and advanced industrial infrastructure. The U.S. invests over 3.4% of GDP in research and development, with engineering simulation forming a core component in aerospace and defense programs. More than 65% of leading aerospace OEMs deploy multiphysics platforms for thermal-structural and fluid-structure interaction modeling. The country hosts over 40% of global high-performance computing (HPC) installations, enabling large-scale multiphysics simulations. Automotive electrification programs and semiconductor manufacturing expansion further contribute to high enterprise adoption, particularly in California, Texas, and Michigan-based industrial clusters.

Market Size & Growth: Valued at USD 551.0 Million in 2025 and projected to reach USD 905.1 Million by 2033, expanding at 6.4%, driven by increasing virtual prototyping adoption reducing physical testing cycles by up to 30%.

Top Growth Drivers: 48% rise in digital twin adoption, 37% improvement in design efficiency, 42% reduction in product failure risks through simulation integration.

Short-Term Forecast: By 2028, engineering validation cycles are expected to shorten by 25%, improving time-to-market KPIs across manufacturing industries.

Emerging Technologies: AI-assisted simulation solvers, GPU-accelerated high-performance computing, and cloud-native collaborative simulation platforms.

Regional Leaders: North America projected at USD 320.0 Million by 2033 with aerospace-led adoption; Europe at USD 250.0 Million driven by automotive electrification; Asia-Pacific at USD 210.0 Million supported by semiconductor fabrication growth.

Consumer/End-User Trends: Aerospace, automotive, and electronics account for over 60% of deployments, with SMEs increasing SaaS-based usage by 35%.

Pilot or Case Example: In 2024, a U.S.-based EV manufacturer achieved 28% battery thermal efficiency improvement using coupled electro-thermal simulation models.

Competitive Landscape:ANSYS holds approximately 32% share, followed by COMSOL, Siemens Digital Industries Software, Dassault Systèmes, and Altair Engineering.

Regulatory & ESG Impact: Carbon reduction mandates are pushing 45% of manufacturers to use simulation to cut material waste by up to 20%.

Investment & Funding Patterns: Over USD 1.2 Billion invested in simulation-focused R&D and cloud engineering platforms in the past three years, with increased venture funding in AI-driven solvers.

Innovation & Future Outlook: Integration of generative design and real-time digital twins is expected to enhance predictive maintenance accuracy by 30% over the next five years.

Automotive contributes nearly 30% of industry demand, followed by aerospace at 25% and electronics at 18%. Cloud-based simulation platforms have grown by 35% adoption in mid-sized enterprises. Stricter energy efficiency regulations in Europe and North America are increasing demand for thermal and structural simulation. AI-enabled solvers and GPU acceleration are improving computational speed by 40%, positioning multiphysics simulation as a core pillar of digital engineering transformation.

The Multiphysics Simulation Software Market holds strategic relevance as industries transition toward digital-first product development frameworks. Engineering teams increasingly rely on integrated physics modeling to simulate structural, thermal, electromagnetic, and fluid dynamics interactions within unified environments. AI-powered simulation delivers 35% faster convergence rates compared to traditional finite element solvers, significantly reducing validation cycles. Cloud-based deployment models also enable distributed teams to collaborate in real time, improving productivity by approximately 28% compared to on-premise-only systems.

North America dominates in volume due to established aerospace and defense manufacturing clusters, while Asia-Pacific leads in adoption growth, with over 52% of advanced electronics manufacturers integrating multiphysics tools into semiconductor and EV battery design workflows. By 2028, AI-driven adaptive meshing and automated solver tuning are expected to cut computational time by 30%, improving design throughput in automotive and renewable energy sectors.

From a compliance and ESG perspective, firms are committing to sustainability metrics such as 20% material waste reduction and 15% energy optimization in manufacturing plants by 2030, leveraging simulation-driven optimization models. In 2024, a German automotive OEM achieved a 22% reduction in prototype iterations through digital twin-enabled multiphysics validation, lowering material consumption and production delays.

Looking ahead, the Multiphysics Simulation Software Market is positioned as a foundational pillar for industrial resilience, regulatory compliance, and sustainable product innovation, supporting enterprises in achieving faster innovation cycles while meeting environmental and performance benchmarks.

The Multiphysics Simulation Software Market is shaped by rapid digitalization of industrial design processes, expansion of electric mobility, semiconductor miniaturization, and increasing demand for energy-efficient infrastructure. Enterprises are replacing traditional sequential simulation methods with integrated multiphysics environments to capture complex interactions across mechanical, electrical, and thermal domains. Over 60% of advanced manufacturing firms now incorporate simulation at early-stage design to reduce late-cycle modifications. Growth in high-performance computing infrastructure, including GPU clusters and cloud HPC services, is enhancing simulation scale and precision. Additionally, rising regulatory standards in aerospace safety and automotive emissions are reinforcing reliance on validated virtual testing frameworks.

The expansion of Industry 4.0 initiatives has significantly increased reliance on simulation-led product development. Over 70% of large-scale manufacturers have adopted digital twin strategies, integrating multiphysics simulation into lifecycle management systems. Automotive electrification programs require coupled electro-thermal simulations to ensure battery reliability and safety compliance. Aerospace manufacturers report up to 30% reduction in wind tunnel testing through advanced fluid-structure interaction models. Furthermore, semiconductor manufacturers depend on electromagnetic and thermal modeling to address sub-5nm chip design complexities. These trends collectively strengthen enterprise demand for integrated simulation environments capable of modeling multi-domain physical phenomena simultaneously.

Advanced multiphysics simulations require substantial computational resources, including GPU clusters and high-performance processors. Enterprise-grade HPC infrastructure can increase IT expenditure by 25–35% annually. Licensing models for advanced solvers and multi-user environments also add operational complexity. Small and mid-sized enterprises often face integration barriers when aligning simulation software with legacy PLM systems. Data management challenges further arise as large-scale simulation datasets frequently exceed several terabytes per project. Additionally, skilled workforce shortages in computational modeling and numerical analysis create adoption bottlenecks, particularly in developing economies where specialized engineering expertise remains limited.

AI-enabled solver optimization presents significant opportunity by automating mesh generation, parameter tuning, and predictive modeling. Automated workflows can reduce simulation setup time by up to 40%. Cloud-native platforms enable subscription-based access, increasing SME participation by nearly 35%. Renewable energy expansion, particularly offshore wind and hydrogen infrastructure, requires complex multiphysics modeling of thermal, structural, and fluid interactions. Electric vehicle battery innovation also demands enhanced electrochemical-thermal simulations to improve lifecycle durability by over 20%. These emerging applications provide substantial expansion avenues across industrial, energy, and high-tech manufacturing sectors.

Multiphysics simulations generate highly complex datasets requiring advanced validation and calibration procedures. Aerospace and medical device industries must comply with strict safety certifications, often necessitating additional verification cycles that extend project timelines by 15–20%. Integration of heterogeneous physics domains increases modeling uncertainties, demanding specialized expertise in numerical methods. Cybersecurity risks associated with cloud-based simulation environments further complicate enterprise deployment strategies. Moreover, ensuring interoperability between CAD, PLM, and ERP platforms requires standardized data protocols, which remain inconsistent across global industrial ecosystems.

AI-Integrated Solver Optimization Enhancing Simulation Speed by 35%: Enterprises are increasingly embedding machine learning algorithms into multiphysics solvers, reducing convergence times by 35% and lowering manual configuration efforts by 30%. Automated mesh refinement tools are improving accuracy levels by 18%, particularly in aerospace and EV battery modeling applications.

Cloud-Based Deployment Expanding SME Adoption by 40%: Subscription-based cloud platforms have increased accessibility for mid-sized firms, with 40% of new users opting for SaaS models. Remote collaboration capabilities have improved engineering productivity by 25%, while reducing infrastructure investment requirements by 32%.

GPU Acceleration Delivering 50% Computational Efficiency Gains: GPU-powered HPC clusters are achieving up to 50% faster processing for fluid dynamics and electromagnetic simulations. Semiconductor manufacturers leveraging GPU acceleration report 20% shorter chip validation cycles, enhancing competitiveness in high-performance electronics markets.

Expansion in Renewable Energy Applications Increasing Usage by 28%: Offshore wind, hydrogen systems, and solar thermal projects have raised multiphysics simulation demand by 28%. Integrated structural and thermal analysis tools are improving turbine blade durability by 22% and optimizing energy yield performance by 15%, reinforcing the market’s role in sustainable infrastructure development.

The Multiphysics Simulation Software Market is segmented by type, application, and end-user, reflecting the diverse technical requirements across industries. By type, deployment models and solver architectures differ based on scalability, integration flexibility, and computational intensity. Applications span structural, thermal, fluid, and electromagnetic simulations, with integrated multi-domain modeling gaining prominence as product designs become more complex. End-user segmentation highlights strong adoption across aerospace, automotive, electronics, energy, and industrial manufacturing sectors. Over 60% of advanced manufacturers integrate multiphysics simulation in early-stage product validation to reduce physical prototyping iterations by nearly 30%. Increasing regulatory scrutiny in safety-critical industries further reinforces the need for validated multi-domain simulation platforms capable of ensuring compliance and performance optimization across design lifecycles.

The market by type is broadly categorized into on-premise software, cloud-based simulation platforms, and hybrid deployment models. On-premise solutions currently account for approximately 48% of total adoption, driven by large enterprises in aerospace and defense requiring strict data control and high-performance computing integration. Cloud-based platforms hold nearly 34% share, while hybrid models contribute around 18%. However, cloud-based simulation is the fastest-growing type, expanding at an estimated CAGR of 9.1%, supported by scalable GPU access and subscription-based licensing models. On-premise deployments remain dominant due to integration with proprietary HPC clusters and compliance-driven industries demanding secure infrastructure. Cloud platforms are gaining momentum as they reduce infrastructure costs by up to 32% and enable collaborative engineering across geographically distributed teams. Hybrid models are increasingly used by automotive OEMs balancing data sensitivity with scalable computational bursts during peak simulation workloads.

• In 2024, a U.S. national laboratory expanded its cloud-based HPC simulation framework to support over 5,000 concurrent engineering simulations, accelerating materials research validation cycles by 27%.

By application, the Multiphysics Simulation Software Market covers structural analysis, fluid dynamics, thermal analysis, electromagnetic simulation, and coupled multi-domain modeling. Structural analysis leads with approximately 29% share, widely used in aerospace airframe validation and automotive crash testing. Fluid dynamics accounts for 24%, while thermal analysis represents nearly 18%. Coupled multi-domain modeling, although currently at 16%, is the fastest-growing application segment, expanding at an estimated CAGR of 10.3% due to rising electric vehicle and semiconductor design complexity. While structural analysis dominates due to established engineering workflows, adoption in coupled electro-thermal and fluid-structure simulations is accelerating rapidly, expected to exceed 25% penetration in EV battery design projects by 2033. Remaining applications, including electromagnetic modeling and acoustics simulation, collectively account for around 13%, supporting niche use cases in telecommunications and advanced electronics. In 2025, more than 41% of global automotive OEMs reported integrating electro-thermal multiphysics simulation into battery safety validation processes. Additionally, 38% of semiconductor manufacturers are deploying electromagnetic-thermal coupled modeling tools to address sub-3nm chip heat dissipation challenges.

• In 2024, a European aerospace research consortium implemented advanced fluid-structure interaction simulation to validate next-generation composite wings, reducing physical wind tunnel testing requirements by 22%.

End-user segmentation highlights aerospace and defense as the leading segment, accounting for approximately 26% of overall demand, followed by automotive at 24% and electronics & semiconductor at 19%. However, renewable energy and electric mobility infrastructure represent the fastest-growing end-user segment, expanding at an estimated CAGR of 11.2%, driven by offshore wind, hydrogen systems, and grid modernization initiatives. The remaining sectors, including industrial manufacturing, healthcare devices, and oil & gas, collectively contribute around 31%. Aerospace leads due to stringent safety validation requirements and reliance on digital twins for airframe and propulsion system analysis. Automotive adoption is strong in crash simulation and EV battery optimization, while semiconductor firms leverage multiphysics tools for heat and electromagnetic interference modeling. In 2025, over 52% of large manufacturing enterprises reported embedding simulation-driven validation into their digital engineering workflows. Additionally, 44% of renewable energy developers indicated increased reliance on structural-thermal simulation for turbine blade durability assessments.

• In 2024, a leading Asian electric vehicle manufacturer reported achieving a 24% reduction in battery prototype iterations through integrated electro-thermal multiphysics modeling deployed across its R&D centers.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.7% between 2026 and 2033.

Europe followed with a 29% share, while Asia-Pacific held 24%, South America 5%, and the Middle East & Africa 4% in 2025. North America’s leadership is supported by over 65% enterprise-level adoption across aerospace and automotive OEMs. Europe demonstrates strong regulatory-driven usage, with nearly 48% of industrial manufacturers integrating simulation for compliance validation. Asia-Pacific benefits from rapid semiconductor and EV production expansion, with more than 52% of advanced electronics firms deploying multiphysics tools. South America and the Middle East & Africa are emerging markets, collectively contributing 9% share, supported by infrastructure modernization and energy-sector digital transformation initiatives.

North America holds approximately 38% of the global Multiphysics Simulation Software Market share, driven primarily by aerospace, defense, automotive, and semiconductor industries. The United States accounts for over 82% of the regional demand, supported by strong R&D expenditure exceeding 3% of GDP. Regulatory frameworks in aerospace safety and automotive crash validation require advanced structural and fluid-structure simulations, pushing adoption across Tier-1 suppliers. More than 60% of large enterprises in the region integrate digital twin technologies into product lifecycle management systems. Local player ANSYS continues expanding AI-enabled solver capabilities and GPU optimization, reporting performance improvements of up to 35% in high-complexity simulations. Regional consumer behavior reflects higher enterprise adoption in healthcare and finance sectors for risk modeling and system optimization, with 45% of Fortune 500 manufacturers embedding simulation into early-stage design validation workflows.

Europe represents 29% of the global Multiphysics Simulation Software Market, with Germany, the United Kingdom, and France collectively accounting for nearly 68% of regional consumption. Automotive electrification initiatives in Germany and aerospace innovation in France significantly contribute to simulation demand. Regulatory mandates under sustainability and emissions standards have pushed nearly 50% of automotive OEMs to increase reliance on electro-thermal modeling tools. The region demonstrates strong adoption of AI-integrated simulation platforms, with approximately 43% of engineering enterprises leveraging cloud-based multiphysics environments. Dassault Systèmes, headquartered in France, continues advancing 3DEXPERIENCE-based simulation integration across digital manufacturing ecosystems. Regional behavior indicates regulatory pressure driving demand for explainable and traceable simulation workflows, particularly in aerospace and renewable energy sectors where compliance documentation is mandatory.

Asia-Pacific accounts for 24% of the global Multiphysics Simulation Software Market and ranks as the fastest-growing region in overall deployment expansion. China, Japan, and India collectively contribute over 70% of regional demand, driven by semiconductor fabrication, EV battery production, and heavy infrastructure projects. China leads in manufacturing scale, with more than 40% of global EV output supported by advanced electro-thermal simulations. Innovation hubs in Japan and South Korea emphasize robotics and precision electronics, with nearly 55% of high-tech manufacturers adopting electromagnetic-thermal coupling models. Altair Engineering has expanded partnerships with regional automotive OEMs to strengthen GPU-accelerated modeling capabilities. Consumer behavior reflects strong industrial orientation, where 50% of engineering firms prioritize cost-efficient cloud simulation platforms to manage rapid product development cycles.

South America holds approximately 5% of the global Multiphysics Simulation Software Market, with Brazil and Argentina representing over 65% of regional demand. Infrastructure expansion and offshore oil & gas exploration are primary drivers, with nearly 38% of regional industrial simulation usage linked to energy-sector applications. Government-backed energy modernization programs have encouraged digital engineering adoption across pipeline and structural validation projects. Local engineering firms increasingly deploy structural and thermal simulation for renewable hydropower optimization, reducing maintenance downtime by 18%. Regional consumer behavior reflects demand tied to industrial modernization and localized engineering services, with mid-sized enterprises accounting for nearly 44% of new software deployments as they digitize legacy production facilities.

The Middle East & Africa accounts for nearly 4% of the global Multiphysics Simulation Software Market, with the UAE and South Africa contributing over 58% of regional demand. Oil & gas remains dominant, representing 46% of multiphysics simulation use cases, particularly in fluid flow and thermal stress analysis. Construction megaprojects and renewable energy diversification initiatives are expanding simulation requirements for structural durability assessments. Technological modernization strategies across Gulf countries have resulted in a 33% increase in digital engineering tool procurement since 2023. Regional trade partnerships and smart city initiatives encourage adoption of digital twin-based multiphysics platforms. Consumer behavior indicates growing enterprise interest in energy optimization and predictive maintenance modeling to improve operational efficiency across large-scale infrastructure assets.

United States – 34% Market Share: It leads due to high R&D intensity, advanced aerospace production capacity, and widespread enterprise-level digital twin integration.

Germany – 12% Market Share: It's strength is driven by automotive electrification programs, precision engineering leadership, and strong regulatory compliance frameworks supporting advanced virtual validation.

The Multiphysics Simulation Software Market demonstrates a moderately consolidated competitive structure, with the top five companies collectively accounting for approximately 68% of global market share. The market features over 45 active global and regional competitors, including established engineering software vendors and specialized physics-based modeling providers. Leading firms compete on solver accuracy, computational speed, multi-domain integration capability, and cloud scalability.

Major players are heavily investing in AI-integrated solvers, GPU acceleration, and digital twin frameworks to enhance simulation efficiency by 25–40%. Strategic initiatives include cross-industry partnerships with automotive OEMs, aerospace manufacturers, and semiconductor foundries to expand application-specific libraries. Over 30% of recent product launches since 2023 have incorporated machine learning-assisted mesh generation or adaptive modeling capabilities. Mergers and acquisitions remain active, particularly in niche electromagnetic and CFD (computational fluid dynamics) domains, strengthening portfolio depth.

Cloud-native platforms are reshaping competition, with nearly 35% of new enterprise contracts favoring SaaS-based simulation deployments. Vendors are also prioritizing interoperability with PLM and CAD ecosystems, enabling end-to-end digital engineering workflows. The competitive environment is increasingly innovation-driven, where performance benchmarks, compliance-ready validation modules, and scalable HPC compatibility determine enterprise-level procurement decisions.

Dassault Systèmes

Altair Engineering

Hexagon AB

PTC Inc.

Autodesk

ESI Group

MSC Software

OpenFOAM Foundation

NUMECA International

Zuken

Maplesoft

Technological advancements in the Multiphysics Simulation Software Market are centered around AI-driven automation, GPU-accelerated computing, digital twin integration, and cloud-native scalability. AI-enhanced solvers now reduce mesh generation time by up to 40% while improving convergence stability by approximately 30%. Adaptive algorithms automatically optimize boundary conditions, minimizing manual intervention and reducing engineering design cycles by nearly 25%.

GPU acceleration is transforming computational performance, delivering up to 50% faster processing for CFD and electromagnetic simulations compared to CPU-only architectures. Over 45% of newly installed HPC clusters for engineering applications now incorporate hybrid CPU-GPU configurations to manage large-scale, coupled multiphysics workloads exceeding 10 million mesh elements.

Cloud-native simulation platforms are expanding enterprise accessibility, enabling elastic compute scaling and reducing infrastructure procurement costs by nearly 32%. Approximately 35% of mid-sized enterprises have transitioned at least part of their simulation workloads to SaaS-based environments. Digital twin integration is another critical advancement, with 48% of advanced manufacturers embedding multiphysics engines into lifecycle management systems for real-time operational monitoring.

Emerging technologies include reduced-order modeling (ROM), which decreases simulation runtime by up to 60% in repetitive design scenarios, and quantum-inspired optimization algorithms under pilot testing in aerospace research facilities. These advancements position multiphysics simulation as a cornerstone of digital engineering transformation across manufacturing, energy, and semiconductor industries.

• In July 2025, Synopsys completed its acquisition of ANSYS, officially integrating ANSYS’s multiphysics simulation portfolio into its broader design and EDA ecosystem—creating a unified platform for engineering simulation and silicon design that aims to accelerate cross-domain product development across aerospace, automotive, and industrial sectors. Source: www.ansys.com

• In December 2024, ANSYS announced the extension of its collaboration with Cummins to further enhance simulation-led product development workflows that support carbon-neutral engineering solutions; the partnership aims to expand ANSYS’s multiphysics capabilities and embed them deeper into Cummins’ power solutions R&D. Source: www.ansys.com

• In December 2024, ANSYS also revealed a strategic collaboration with Sony Semiconductor Solutions to advance scenario-based perception testing in autonomous vehicles, leveraging real-time multispectral simulation to accelerate ADAS/AV validation under diverse environmental conditions. Source: www.ansys.com

• In May 2025, Siemens Digital Industries Software introduced the Simcenter FLOEFD 2506 release, enhancing CAD-embedded CFD and thermal workflow capabilities that allow more efficient electronics thermal design and integration with broader multiphysics simulation environments—reflecting a continuous product innovation cycle within the Simcenter portfolio. Source: www.blogs.sw.siemens.com

The Multiphysics Simulation Software Market Report provides a comprehensive assessment of industry trends, segmentation, competitive dynamics, and technology advancements across global regions. The report covers three primary segmentation pillars: type (on-premise, cloud-based, hybrid), application (structural, fluid dynamics, thermal, electromagnetic, and coupled multi-domain modeling), and end-user industries including aerospace, automotive, electronics, energy, industrial manufacturing, and healthcare devices.

Geographically, the scope spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, representing 100% of global demand coverage. The analysis includes evaluation of more than 45 active market participants and profiles 14+ leading vendors. Industry-specific deployment insights are incorporated, including enterprise-level adoption rates exceeding 60% in aerospace and over 50% in automotive electrification programs.

The report also examines emerging technological domains such as AI-enabled solver automation, GPU acceleration, digital twin integration, and reduced-order modeling. Infrastructure considerations including HPC clusters, cloud elasticity, and data interoperability standards are evaluated to assess operational scalability. Additionally, regulatory compliance trends in safety-critical industries and ESG-driven design optimization initiatives are analyzed to provide decision-makers with actionable intelligence on long-term industrial transformation and competitive positioning within the Multiphysics Simulation Software Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 551.0 Million |

| Market Revenue (2033) | USD 905.1 Million |

| CAGR (2026–2033) | 6.4% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | ANSYS; COMSOL; Siemens Digital Industries Software; Dassault Systèmes; Altair Engineering; Hexagon AB; PTC Inc.; Autodesk; ESI Group; MSC Software; OpenFOAM Foundation; NUMECA International; Zuken; Maplesoft |

| Customization & Pricing | Available on Request (10% Customization Free) |