Reports

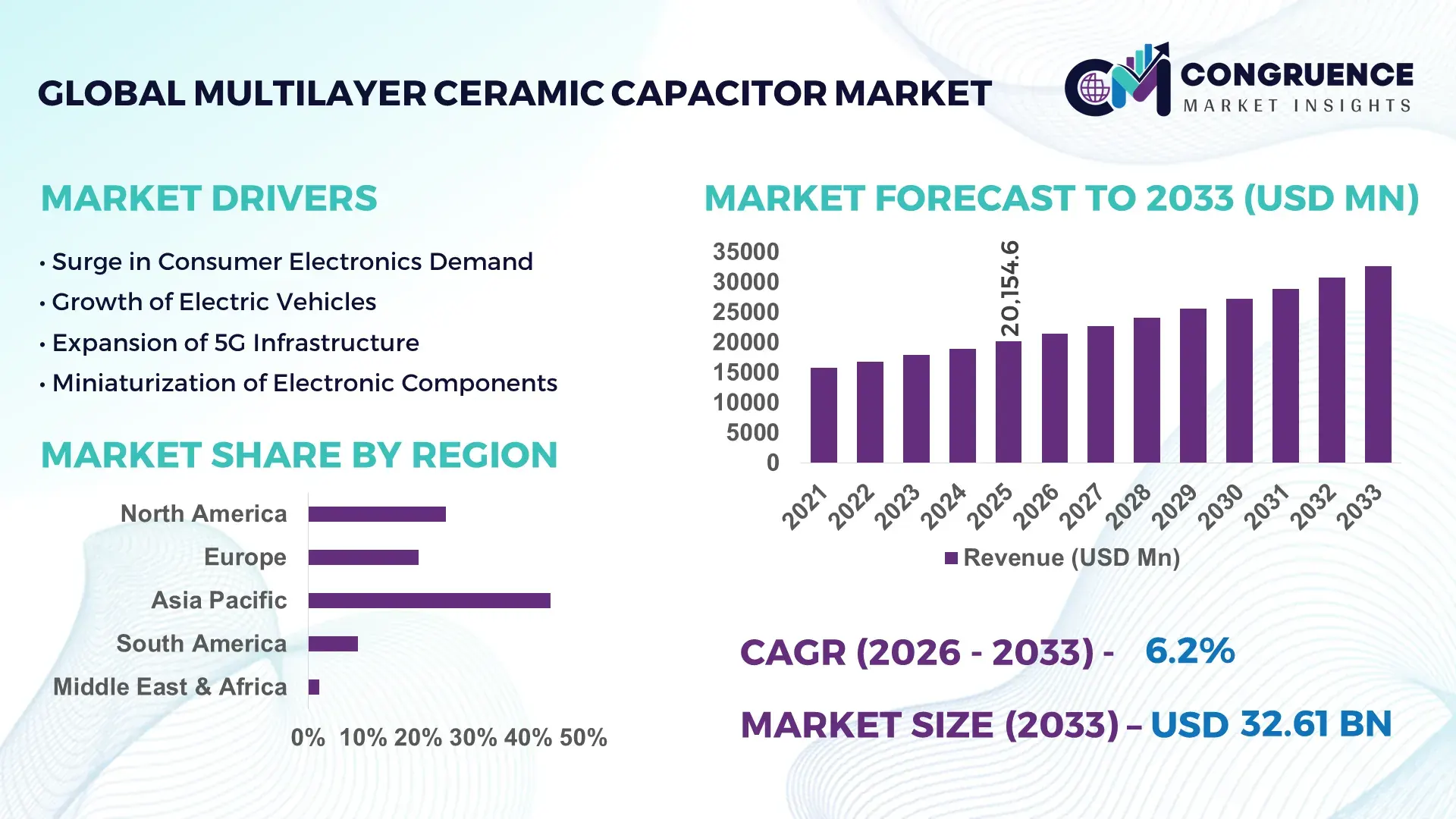

The Global Multilayer Ceramic Capacitor Market was valued at USD 20154.57 Million in 2025 and is anticipated to reach a value of USD 32611.42 Million by 2033 expanding at a CAGR of 6.2% between 2026 and 2033. The growth is primarily driven by rapid expansion in high-performance consumer electronics and automotive electrification.

China continues to be the dominant country in the Multilayer Ceramic Capacitor market, supported by extensive manufacturing infrastructure and vertically integrated supply chains. The country produces over 55% of global MLCC output, with major industrial clusters in Guangdong and Jiangsu provinces. Annual production capacity exceeds 5 trillion units, catering to domestic electronics, EV manufacturing, and telecommunications sectors. Investments in advanced dielectric materials and miniaturization technologies have enabled Chinese manufacturers to produce capacitors with capacitance values above 100 µF in compact sizes. Additionally, over 65% of smartphones manufactured globally rely on MLCC components sourced from China, highlighting strong integration with global supply networks. Government-backed semiconductor initiatives exceeding USD 40 billion have further accelerated innovation and capacity expansion in high-frequency and automotive-grade MLCCs.

Market Size & Growth: USD 20154.57 Million in 2025, projected to reach USD 32611.42 Million by 2033 at 6.2% CAGR, driven by rising demand for compact electronic components in EVs and IoT devices.

Top Growth Drivers: Automotive electronics adoption (38%), 5G infrastructure expansion (32%), miniaturization demand (29%).

Short-Term Forecast: By 2028, MLCC reliability improvements are expected to enhance performance efficiency by 22% and reduce failure rates by 18%.

Emerging Technologies: High-capacitance X7R/X8R dielectric materials, ultra-small case sizes (01005), AI-enabled manufacturing quality control.

Regional Leaders: Asia-Pacific projected at USD 19,800 Million by 2033 with strong electronics manufacturing; North America at USD 5,400 Million driven by EV adoption; Europe at USD 4,900 Million supported by industrial automation.

Consumer/End-User Trends: Automotive sector accounts for over 30% of demand, followed by smartphones and industrial electronics with increasing adoption of high-reliability MLCCs.

Pilot or Case Example: In 2024, a Japanese manufacturer achieved 25% production efficiency improvement using AI-driven defect detection systems.

Competitive Landscape: Market leader holds approximately 24% share, followed by major players including Murata Manufacturing, Samsung Electro-Mechanics, TDK Corporation, Taiyo Yuden, and Yageo Corporation.

Regulatory & ESG Impact: Adoption of RoHS compliance and lead-free manufacturing increased by over 85% across global facilities.

Investment & Funding Patterns: Over USD 3.5 billion invested in MLCC capacity expansion and R&D between 2023 and 2025.

Innovation & Future Outlook: Integration of MLCCs in autonomous vehicles and high-frequency communication modules is shaping next-generation electronics.

The Multilayer Ceramic Capacitor market demonstrates strong diversification across key industry sectors, with consumer electronics contributing approximately 40% of total demand, followed by automotive electronics at over 30%, and industrial applications accounting for nearly 20%. Recent advancements include ultra-thin layer stacking exceeding 1,000 dielectric layers per capacitor, significantly enhancing capacitance density. Environmental regulations promoting lead-free components and energy-efficient electronics are accelerating product innovation. Regional consumption remains heavily concentrated in Asia-Pacific, which accounts for more than 70% of total usage, while North America and Europe are witnessing growth driven by EV production and industrial automation. Emerging trends such as embedded capacitors in printed circuit boards and high-temperature MLCCs for aerospace applications are expected to reshape future market dynamics, enabling enhanced durability and performance in demanding environments.

The Multilayer Ceramic Capacitor Market holds strategic importance as a foundational component enabling next-generation electronics, automotive electrification, and high-speed communication systems. With over 1,000 MLCC units integrated into a single smartphone and more than 10,000 units required in electric vehicles, the market’s relevance continues to intensify across high-growth sectors. Advanced MLCC technologies such as high-layer-count capacitors deliver nearly 35% higher capacitance density compared to traditional designs, significantly improving device performance and space efficiency.

Asia-Pacific dominates in volume production due to its expansive electronics manufacturing ecosystem, while North America leads in advanced adoption with over 45% of enterprises integrating MLCCs in electric mobility and industrial automation systems. By 2027, AI-driven manufacturing optimization is expected to reduce defect rates by approximately 20% while enhancing production throughput by 18%. Companies are increasingly aligning with ESG commitments, targeting over 90% compliance with lead-free and recyclable materials by 2030, reflecting a strong shift toward sustainable electronics manufacturing.

A notable micro-scenario emerged in 2024, where a leading South Korean manufacturer achieved a 28% reduction in production defects through machine learning-based inspection systems, improving overall yield efficiency. Additionally, high-temperature MLCCs used in automotive powertrains have demonstrated 15% improved reliability under extreme conditions compared to legacy capacitor technologies. As digital transformation accelerates, the Multilayer Ceramic Capacitor Market is positioned as a critical enabler of resilience, regulatory compliance, and sustainable technological growth across global industries.

The rapid adoption of electric vehicles is significantly driving demand in the Multilayer Ceramic Capacitor market, as modern EVs require between 8,000 to 12,000 MLCC units per vehicle for power management, infotainment, and advanced driver assistance systems. Automotive-grade MLCCs are designed to operate under extreme temperatures ranging from -55°C to 150°C, ensuring reliability in critical applications. The global push toward electrification has resulted in over 14 million EVs sold annually, creating substantial demand for high-performance capacitors. Additionally, the integration of autonomous driving technologies has increased electronic component density by nearly 40%, further boosting MLCC consumption. Manufacturers are responding by developing high-reliability capacitors with enhanced vibration resistance and extended lifecycle performance to meet stringent automotive standards.

The Multilayer Ceramic Capacitor market faces notable constraints due to dependence on critical raw materials such as barium titanate and nickel, which are essential for dielectric layers and electrode formation. Fluctuations in the availability and pricing of these materials can disrupt production stability and increase manufacturing costs. For instance, nickel price volatility has shown fluctuations exceeding 20% annually, directly affecting MLCC pricing structures. Additionally, high purity requirements for ceramic powders limit the number of qualified suppliers, creating supply bottlenecks. Environmental regulations related to mining and processing further restrict raw material availability, adding complexity to the supply chain. These factors collectively challenge manufacturers’ ability to maintain consistent production volumes and cost efficiency.

The global rollout of 5G networks presents significant growth opportunities for the Multilayer Ceramic Capacitor market, as base stations and communication devices require high-frequency, low-loss capacitors for efficient signal transmission. A single 5G base station can utilize over 10,000 MLCC units, significantly higher than previous network generations. The increasing deployment of small cells and IoT-connected devices is further amplifying demand. Advanced MLCCs with improved frequency stability and reduced equivalent series resistance are becoming critical components in 5G infrastructure. Additionally, the expansion of smart cities and connected ecosystems is expected to drive large-scale adoption, creating new revenue streams for manufacturers specializing in high-performance capacitors.

The ongoing trend toward miniaturization and increased capacitance density presents significant technical challenges for the Multilayer Ceramic Capacitor market. Modern MLCCs can contain over 1,000 ceramic layers, each requiring precise thickness control at the micron level. Maintaining structural integrity while reducing size increases the risk of defects such as cracking and delamination. Furthermore, ultra-small case sizes like 01005 demand advanced manufacturing techniques and stringent quality control measures, increasing production complexity. Yield loss rates can rise by 10–15% during high-layer stacking processes, impacting overall efficiency. These challenges necessitate continuous investment in advanced manufacturing technologies, automation, and inspection systems to ensure product reliability and scalability.

• Accelerated Miniaturization with Ultra-Compact MLCC Sizes: The transition toward ultra-small MLCC case sizes such as 01005 and 008004 is significantly transforming component design strategies. Over 65% of next-generation smartphones now integrate capacitors smaller than 0.4 mm, enabling higher circuit density. Layer counts have exceeded 1,000 in advanced designs, improving capacitance density by nearly 30% compared to earlier models. This trend is further reinforced by the demand for thinner wearable devices, where PCB space optimization has improved by over 25% through high-density MLCC integration.

• Rising Demand from Electric Vehicles and Advanced Automotive Systems: Automotive applications now account for more than 30% of total MLCC consumption, with electric vehicles requiring between 8,000 and 12,000 units per vehicle. The integration of advanced driver-assistance systems has increased electronic component usage by approximately 40% per vehicle. High-temperature MLCCs capable of operating above 150°C have seen adoption rates increase by over 35% in powertrain systems. Additionally, the shift toward 800V EV architectures has driven demand for capacitors with enhanced voltage stability and durability.

• Expansion of 5G Infrastructure and High-Frequency Applications: The global rollout of 5G networks has increased demand for high-frequency MLCCs by over 45% compared to 4G infrastructure requirements. A single 5G base station utilizes up to 10,000 capacitors, reflecting a 60% increase in component density. Low equivalent series resistance (ESR) capacitors have improved signal efficiency by nearly 20%, making them critical for telecommunications equipment. The adoption of IoT devices has also surged by over 50%, further accelerating the need for high-performance capacitors in connected ecosystems.

• Integration of AI-Driven Manufacturing and Quality Control Systems: The implementation of AI and machine learning in MLCC production lines has improved defect detection accuracy by over 28%, reducing rejection rates by nearly 20%. Automated optical inspection systems now cover over 85% of manufacturing facilities, ensuring consistent quality in high-layer-count capacitors. Production efficiency has increased by approximately 25% through predictive maintenance and real-time monitoring. These advancements are enabling manufacturers to scale production while maintaining stringent reliability standards required for automotive and industrial applications.

The Multilayer Ceramic Capacitor market segmentation is defined by diverse product types, broad application areas, and a wide range of end-user industries. Type-based segmentation includes general-purpose, high-capacitance, automotive-grade, and high-frequency MLCCs, each tailored to specific performance requirements. Application segmentation highlights strong demand from consumer electronics, automotive systems, telecommunications, and industrial equipment, with consumer electronics accounting for a significant portion due to high device penetration rates. End-user segmentation reflects increasing adoption across electronics manufacturers, automotive OEMs, telecom infrastructure providers, and industrial automation companies. More than 70% of total MLCC demand is concentrated in Asia-Pacific due to strong manufacturing ecosystems, while North America and Europe are witnessing increasing adoption in EVs and advanced industrial applications. The segmentation structure reflects a balanced mix of high-volume consumer demand and high-reliability industrial requirements.

The Multilayer Ceramic Capacitor market by type is led by general-purpose MLCCs, which account for approximately 45% of total adoption due to their widespread use in consumer electronics such as smartphones, laptops, and home appliances. These capacitors offer balanced performance and cost efficiency, making them suitable for high-volume production environments. High-capacitance MLCCs follow with nearly 30% share, driven by increasing demand in power management circuits and automotive applications. However, automotive-grade MLCCs represent the fastest-growing segment, expanding at an estimated CAGR of 7.5%, supported by the rising production of electric vehicles and the need for high-reliability components capable of operating under extreme temperatures and voltage conditions. High-frequency MLCCs and specialized capacitors contribute the remaining 25% of the market, catering to telecommunications, aerospace, and medical applications where precision and stability are critical. These segments are gaining traction with the expansion of 5G infrastructure and advanced communication systems.

Consumer electronics remain the leading application segment in the Multilayer Ceramic Capacitor market, accounting for approximately 40% of total usage due to the high volume production of smartphones, tablets, and wearable devices. On average, a modern smartphone integrates over 1,000 MLCC units, reflecting strong demand for compact and high-performance components. Automotive applications follow closely with around 30% share, driven by increasing electrification and integration of advanced electronic systems. Telecommunications infrastructure represents the fastest-growing application segment, with an estimated CAGR of 8.2%, fueled by rapid 5G deployment and the expansion of data centers. Industrial applications, including automation and robotics, along with medical devices, contribute the remaining 30% of the market, supporting steady demand for reliable and durable capacitors.

Electronics manufacturers dominate the Multilayer Ceramic Capacitor market, accounting for approximately 45% of total demand, as they integrate MLCCs into a wide range of consumer and computing devices. Automotive OEMs represent the second-largest segment with around 30% share, reflecting the increasing adoption of MLCCs in electric and hybrid vehicles. However, telecom infrastructure providers are emerging as the fastest-growing end-user segment, expanding at an estimated CAGR of 8.5%, driven by large-scale 5G network deployment and data traffic growth. Other end-users, including industrial automation firms, aerospace companies, and healthcare device manufacturers, collectively contribute approximately 25% of the market. Industrial automation adoption has increased by over 20% in recent years, boosting demand for high-reliability capacitors in robotics and smart manufacturing systems.

Region Asia-Pacific accounted for the largest market share at 71% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 7.1% between 2026 and 2033.

Asia-Pacific’s dominance is supported by its massive electronics manufacturing base, producing over 5 trillion MLCC units annually, with China, Japan, and South Korea contributing more than 80% of regional output. North America holds approximately 14% share, driven by strong adoption in electric vehicles and advanced industrial automation, while Europe accounts for nearly 11%, supported by automotive electrification and regulatory compliance requirements. South America and the Middle East & Africa collectively contribute around 4% of global demand, with increasing investments in telecommunications and infrastructure development. Regional consumption patterns show that over 65% of MLCC demand is concentrated in high-volume consumer electronics production hubs, while industrial and automotive applications are expanding rapidly across developed economies. The global distribution network continues to evolve, with over 60% of supply chain operations localized within Asia-Pacific to reduce lead times and enhance production efficiency.

How are advanced electronics and EV adoption reshaping demand patterns?

North America accounts for approximately 14% of the global Multilayer Ceramic Capacitor market, driven by strong demand across automotive, aerospace, and industrial electronics sectors. Electric vehicle production in the region has increased by over 35% in recent years, significantly boosting MLCC consumption, with each EV integrating up to 10,000 capacitors. The region also benefits from regulatory support such as clean energy incentives and semiconductor manufacturing initiatives exceeding USD 50 billion in funding. Technological advancements in AI-driven manufacturing and high-reliability components are accelerating adoption in mission-critical applications. A key regional player, KEMET (a Yageo company), has expanded production capabilities for automotive-grade MLCCs, focusing on high-temperature and high-voltage applications. Consumer behavior reflects higher enterprise adoption, particularly in healthcare and financial systems, where over 40% of advanced electronic systems rely on high-performance capacitors for stable operation.

What factors are driving innovation in high-reliability electronic components?

Europe represents around 11% of the global Multilayer Ceramic Capacitor market, with key contributions from Germany, the United Kingdom, and France. The region’s automotive sector accounts for over 45% of MLCC demand, supported by strong electric vehicle production and industrial automation. Regulatory frameworks promoting sustainability, including RoHS compliance and carbon neutrality targets, have driven adoption of lead-free and energy-efficient capacitors, with over 85% of manufacturers aligning with environmental standards. Technological advancements include the integration of MLCCs in smart grid systems and industrial IoT applications, enhancing operational efficiency by over 20%. A notable regional player, TDK Corporation, has strengthened its European footprint by expanding R&D facilities focused on next-generation capacitor technologies. Consumer behavior in the region reflects strong regulatory-driven demand, with increasing preference for high-reliability and environmentally compliant electronic components.

Why is high-volume electronics manufacturing transforming component demand?

Asia-Pacific leads the Multilayer Ceramic Capacitor market in both volume and consumption, accounting for over 70% of global demand. China, Japan, and South Korea are the top consuming countries, collectively producing more than 5 trillion units annually. The region’s dominance is supported by extensive electronics manufacturing infrastructure, with over 65% of global smartphone and consumer electronics production based in this region. Technological innovation hubs in Japan and South Korea are driving advancements in high-capacitance and ultra-miniaturized MLCCs, improving performance efficiency by over 30%. Murata Manufacturing, a leading regional player, continues to invest in advanced production facilities, increasing output capacity by over 20% in recent years. Consumer behavior trends indicate strong demand driven by mobile device usage and e-commerce growth, with over 75% of global electronics exports originating from Asia-Pacific.

How are infrastructure expansion and telecom growth influencing adoption?

South America holds approximately 2.5% of the global Multilayer Ceramic Capacitor market, with Brazil and Argentina as key contributors. The region’s demand is largely driven by telecommunications expansion and energy infrastructure projects, with over 60% of MLCC usage linked to network equipment and power systems. Government incentives promoting digital connectivity and renewable energy projects have increased demand for electronic components by nearly 18% over recent years. Trade policies supporting electronics imports and assembly operations are further facilitating market growth. A notable regional development includes increased participation of local electronics assemblers integrating MLCCs into communication devices and industrial systems. Consumer behavior in the region is closely tied to media consumption and localized digital services, with growing adoption of smartphones and connected devices contributing to steady demand growth.

What role does industrial diversification play in electronic component demand?

The Middle East & Africa region accounts for approximately 1.5% of the global Multilayer Ceramic Capacitor market, with key growth countries including the United Arab Emirates and South Africa. Demand is primarily driven by oil and gas sector digitization, construction projects, and telecommunications infrastructure, with over 50% of MLCC usage linked to industrial and energy applications. Technological modernization initiatives, including smart city projects and digital transformation programs, have increased demand for electronic components by nearly 20%. Trade partnerships and import policies are facilitating access to advanced MLCC technologies, supporting regional adoption. A notable development includes the integration of MLCCs in smart grid systems across urban infrastructure projects. Consumer behavior reflects increasing reliance on mobile connectivity and digital services, with over 65% of urban populations using connected devices, driving incremental demand for electronic components.

China – 38% market share: Multilayer Ceramic Capacitor market dominance driven by large-scale production capacity exceeding 5 trillion units annually and strong integration with global electronics manufacturing.

Japan – 21% market share: Multilayer Ceramic Capacitor market leadership supported by advanced technology innovation, high-precision manufacturing, and strong presence of leading component manufacturers.

The Multilayer Ceramic Capacitor market is moderately consolidated, with the top five companies accounting for approximately 68% of total global production capacity. The competitive landscape is characterized by strong technological differentiation, high entry barriers, and continuous innovation in miniaturization and material science. Over 25 active global competitors operate across various segments, with leading players focusing on high-capacitance, automotive-grade, and high-frequency MLCCs to maintain market leadership.

Strategic initiatives such as capacity expansion, mergers, and joint ventures are shaping competition, with over USD 3.5 billion invested in new production facilities and R&D between 2023 and 2025. Companies are increasingly adopting AI-driven manufacturing processes, improving production efficiency by over 25% and reducing defect rates by nearly 20%. Product innovation remains a key competitive factor, with manufacturers introducing capacitors featuring over 1,000 dielectric layers and improved thermal stability for high-performance applications.

Additionally, supply chain optimization and regional diversification strategies are gaining importance, with over 60% of manufacturers localizing production in Asia-Pacific to reduce operational risks. Partnerships with automotive OEMs and telecom providers are further strengthening market positioning, enabling companies to secure long-term contracts and expand their global footprint.

Murata Manufacturing Co., Ltd.

Samsung Electro-Mechanics

TDK Corporation

Taiyo Yuden Co., Ltd.

Yageo Corporation

Vishay Intertechnology, Inc.

AVX Corporation

Walsin Technology Corporation

Kyocera Corporation

Darfon Electronics Corp.

Technological advancements in the Multilayer Ceramic Capacitor market are centered around miniaturization, high capacitance density, and enhanced reliability for high-performance electronic applications. One of the most notable innovations is the development of ultra-thin dielectric layers, with thicknesses reduced to less than 1 micrometer, enabling the stacking of over 1,000 ceramic layers within a single capacitor. This advancement has improved capacitance density by more than 30% compared to conventional designs, allowing integration into compact devices such as smartphones and wearables.

Material innovation is another critical area, particularly the use of advanced dielectric formulations such as X7R and X8R ceramics, which offer stable performance across temperature ranges from -55°C to 150°C. These materials have improved thermal stability by approximately 25%, making them suitable for automotive and industrial applications. Additionally, the shift from palladium-based electrodes to nickel-based internal electrodes has reduced material costs while maintaining conductivity and performance efficiency.

Automation and artificial intelligence are transforming MLCC manufacturing processes, with over 85% of production lines now utilizing automated optical inspection systems. AI-driven defect detection has enhanced quality control accuracy by nearly 28%, significantly reducing failure rates. Furthermore, innovations in high-frequency MLCCs with reduced equivalent series resistance have improved signal efficiency by up to 20%, supporting 5G and high-speed communication systems.

Emerging technologies such as embedded capacitors integrated directly into printed circuit boards are gaining traction, reducing component count by up to 15% and improving overall system reliability. Additionally, advancements in high-temperature MLCCs capable of operating above 175°C are expanding applications in electric vehicles and aerospace systems, where durability and performance under extreme conditions are critical.

• In October 2024, Murata Manufacturing Co., Ltd. announced the mass production of the world’s smallest 008004 size MLCC, measuring 0.25 mm × 0.125 mm, enabling higher component density in compact electronic devices such as wearables and advanced smartphones. Source: www.murata.com

• In March 2025, Samsung Electro-Mechanics introduced automotive-grade MLCCs designed for 150°C operating environments, enhancing reliability in electric vehicle powertrains and advanced driver-assistance systems while supporting next-generation high-voltage architectures. Source: www.samsungsem.com

• In May 2024, TDK Corporation expanded its C series MLCC lineup with high-capacitance products exceeding 100 µF, targeting industrial and automotive applications requiring stable performance under high load conditions and improved energy storage capabilities. Source: www.tdk.com

• In January 2025, Yageo Corporation announced capacity expansion initiatives in Asia, increasing MLCC production output by over 20% to address rising demand from 5G infrastructure and electric vehicle manufacturing sectors. Source: www.yageo.com

The Multilayer Ceramic Capacitor Market Report provides a comprehensive analysis of the global industry landscape, covering a wide range of segments, technologies, and regional markets. The report evaluates multiple product categories, including general-purpose MLCCs, high-capacitance variants, automotive-grade capacitors, and high-frequency components, each contributing to diverse application requirements. It examines performance characteristics such as capacitance range, voltage ratings exceeding 1,000V, and temperature stability across industrial and automotive environments.

From an application perspective, the report encompasses key sectors such as consumer electronics, automotive systems, telecommunications infrastructure, industrial automation, and medical devices. Consumer electronics alone accounts for the integration of over 1,000 MLCC units per device, while electric vehicles utilize up to 12,000 units per vehicle, reflecting the critical role of these components in modern electronics. Geographically, the report covers major regions including Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, with Asia-Pacific contributing more than 70% of global production volume. The study also includes emerging markets where infrastructure development and digital transformation are driving incremental demand.

In addition, the report analyzes technological advancements such as ultra-miniaturization, embedded capacitor technologies, and AI-driven manufacturing processes, along with supply chain dynamics and raw material considerations. It further explores niche segments such as high-temperature MLCCs for aerospace and energy applications, providing decision-makers with a holistic understanding of current trends, operational challenges, and strategic growth opportunities across the global Multilayer Ceramic Capacitor market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

6.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Murata Manufacturing Co., Ltd., Samsung Electro-Mechanics, TDK Corporation, Taiyo Yuden Co., Ltd., Yageo Corporation, Vishay Intertechnology, Inc., AVX Corporation, Walsin Technology Corporation, Kyocera Corporation, Darfon Electronics Corp. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |