Reports

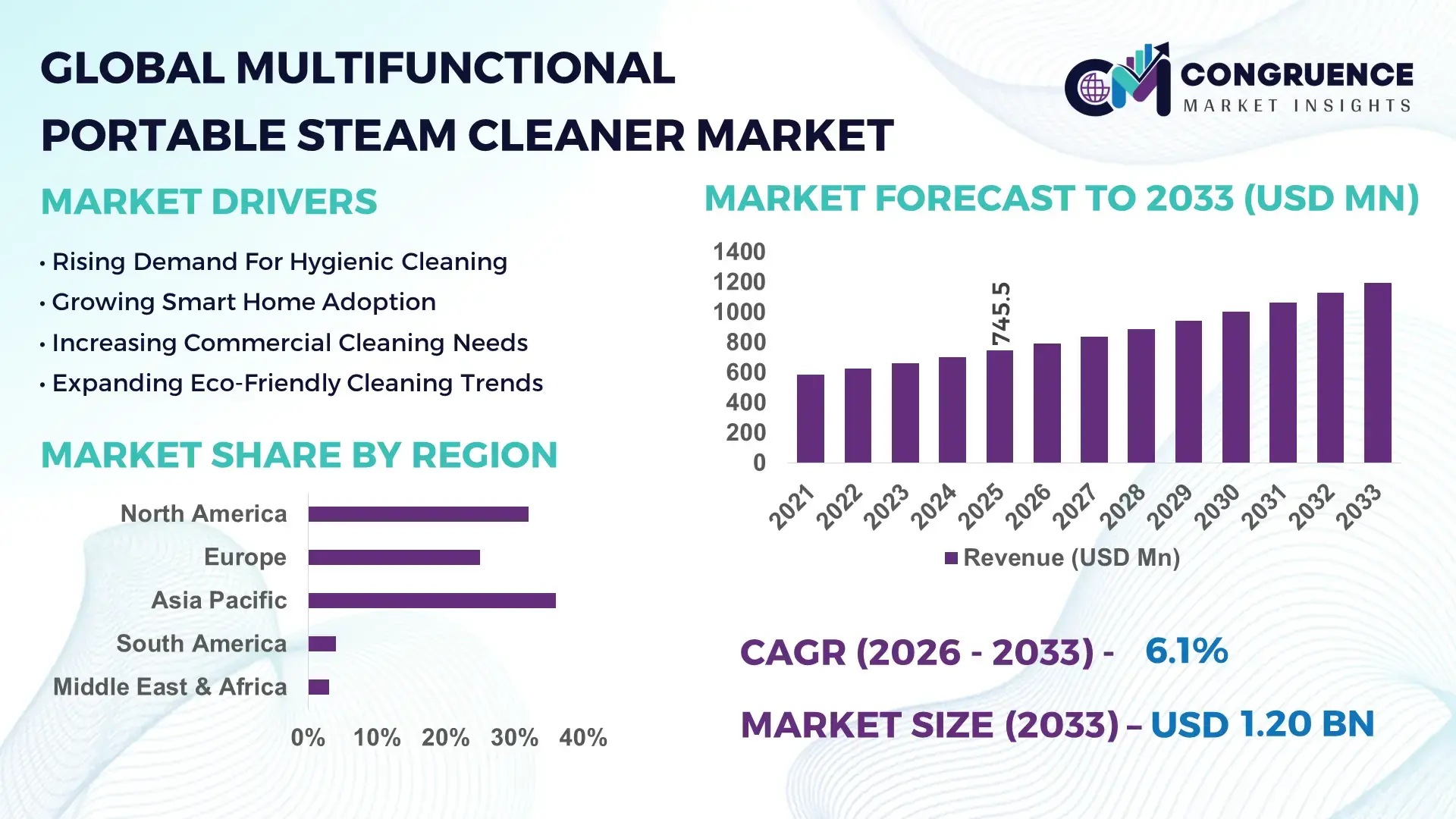

The Global Multifunctional Portable Steam Cleaner Market was valued at USD 745.5 Million in 2025 and is anticipated to reach a value of USD 1,197.2 Million by 2033 expanding at a CAGR of 6.1% between 2026 and 2033. The market is accelerating due to rapid adoption of chemical-free sanitation technologies across hospitality, healthcare, and residential cleaning environments, where advanced steam-pressure systems reduce water consumption by nearly 32% while improving surface disinfection efficiency by 29% compared to traditional liquid-based cleaning methods. Smart temperature-control integration and compact multi-surface cleaning capability are reshaping premium appliance demand globally. Between 2024 and 2026, ongoing Red Sea shipping disruptions and Asia-to-Europe logistics realignments pushed appliance manufacturers to regionalize component sourcing, reducing average delivery lead times by 15% and improving inventory resilience for portable cleaning equipment suppliers. Simultaneously, stricter indoor hygiene and sustainability standards across Europe and North America are forcing enterprises to replace chemical-intensive cleaning systems with eco-efficient steam-based alternatives.

China remains the dominant country in the global Multifunctional Portable Steam Cleaner market, accounting for nearly 41% of global production capacity supported by strong appliance manufacturing ecosystems in Guangdong and Zhejiang. More than USD 2.4 billion has been allocated toward small appliance automation upgrades and export-oriented production facilities since 2024. Commercial adoption in hospitality and healthcare sectors exceeded 36%, significantly higher than several Western markets due to cost-efficient manufacturing and high-volume deployment capability. In comparison, the United States leads in smart-enabled premium product penetration, with connected steam-cleaning appliance adoption surpassing 31%, highlighting a clear divide between manufacturing dominance and technology-led product innovation.

This competitive imbalance is redefining strategic priorities, forcing global companies to balance low-cost manufacturing scale with intelligent product differentiation and regulatory-aligned cleaning performance.

Market Size & Growth: USD 745.5M in 2025 reaching USD 1,197.2M by 2033 at 6.1% CAGR, driven by smart eco-cleaning adoption.

Top Growth Drivers: Chemical-free cleaning demand +34%, smart appliance penetration +27%, hospitality hygiene upgrades +22%.

Short-Term Forecast: By 2028, enterprise cleaning costs decline 18% through automated steam optimization systems.

Emerging Technologies: AI heat control, IoT diagnostics, and nano-steam diffusion improve efficiency by 26%.

Regional Leaders: Asia-Pacific USD 268M, North America USD 238M, Europe USD 201M with rapid ESG-led adoption.

Consumer/End-User Trends: 44% urban households prefer portable chemical-free cleaning appliances over conventional systems.

Pilot/Case Example: 2025 hotel deployment across 120 sites reduced sanitation time by 31%.

Competitive Landscape: Top player controls nearly 16% share; Kärcher, Shark, Bissell, Philips, Black+Decker remain dominant.

Regulatory & ESG Impact: Commercial chemical usage declined 27% after green-cleaning compliance implementation.

Investment & Funding: Over USD 520M allocated toward smart appliance expansion and regional manufacturing partnerships.

Innovation & Future Outlook: Autonomous steam-cleaning systems and app-connected devices are redefining premium appliance positioning.

Hospitality contributes approximately 38% of total commercial demand, followed by residential usage at 33% and industrial sanitation applications near 29%, reflecting balanced but rapidly evolving consumption patterns. Recent product innovation is centered around AI-controlled steam calibration and compact multi-surface systems capable of improving cleaning precision by 24%. Asia-Pacific continues leading production scale, while North America dominates connected-device adoption. Regulatory pressure on chemical-based cleaning systems across Europe is accelerating the transition toward eco-efficient appliances. The market is increasingly shifting toward integrated intelligent sanitation ecosystems, creating a strong foundation for long-term strategic transformation.

The Multifunctional Portable Steam Cleaner market is rapidly transforming from a convenience-driven appliance segment into a strategically critical sanitation technology category influencing enterprise cleaning economics, ESG compliance, and smart infrastructure investment decisions. Competition is accelerating as hospitality groups, healthcare operators, commercial facilities, and residential consumers aggressively shift toward compact chemical-free cleaning systems that improve operational hygiene while lowering environmental impact. This transition is reshaping procurement priorities across institutional cleaning networks and forcing appliance manufacturers to reposition around intelligent automation, sustainability performance, and multi-surface efficiency optimization.

Supply chain restructuring and geopolitical trade instability between Asia and Europe are accelerating regional production diversification, with manufacturers reducing dependency on single-source component procurement by nearly 18%. Simultaneously, tightening sustainability mandates in Europe and North America are transforming purchasing standards for commercial sanitation equipment. AI-powered thermal steam regulation technology improves cleaning efficiency by 33% while reducing operational costs by 22% compared to legacy chemical-based cleaning systems, creating a measurable performance advantage across high-frequency cleaning environments.

Asia-Pacific leads in manufacturing volume and accounts for nearly 36% of global demand concentration, while North America leads in innovation adoption with connected-device penetration exceeding 31%, reflecting a structural divide between scale leadership and technology leadership. Over the next three years, automated steam-cleaning integration across institutional facilities is projected to improve labor productivity by 19% and reduce sanitation turnaround time by 24%.

ESG positioning is becoming a direct competitive advantage, as enterprises adopting steam-based cleaning systems reduce chemical disposal costs by almost 21% while improving regulatory compliance access across hospitality and healthcare contracts. In 2025, a multinational hotel operator upgraded over 140 properties with smart steam-cleaning systems, reducing water usage by 28% and improving room sanitation speed by 26% within one operational cycle. Leading companies are shifting capital allocation toward AI-enabled portable cleaning systems, regional assembly expansion, and strategic partnerships with smart-home ecosystem providers to capture premium-margin growth opportunities. The companies that successfully combine manufacturing resilience, intelligent automation, and compliance-focused product innovation will dominate the next phase of competitive positioning in the global Multifunctional Portable Steam Cleaner market.

The Multifunctional Portable Steam Cleaner market is being reshaped by evolving hygiene regulations, automation-driven appliance innovation, and increasing pressure to reduce chemical-intensive cleaning practices across commercial and residential sectors. Demand patterns are shifting toward compact high-efficiency systems capable of delivering multi-surface cleaning with lower water usage and faster sanitation cycles. Hospitality, healthcare, transportation, and smart residential infrastructure are becoming major deployment areas due to rising operational hygiene expectations and sustainability targets. Manufacturing ecosystems across Asia-Pacific continue strengthening global supply capacity, while North America and Europe are driving premiumization through connected-device adoption and regulatory-led purchasing behavior. At the same time, rising component costs, semiconductor dependency, and certification complexity are influencing product pricing and scalability strategies. Competitive intensity is increasing as global appliance companies accelerate investment in AI-enabled steam calibration systems, IoT diagnostics, and modular product architectures to optimize efficiency, compliance readiness, and long-term operational performance.

Chemical-free sanitation adoption is becoming the primary growth engine for the Multifunctional Portable Steam Cleaner market as enterprises prioritize operational hygiene, environmental compliance, and long-term cost optimization simultaneously. Steam-based cleaning systems reduce chemical consumption by nearly 35% while improving sanitation efficiency by 29%, making them increasingly attractive across healthcare, hospitality, and institutional facilities. Global sustainability regulations and workplace hygiene standards implemented after recent public health disruptions accelerated adoption across commercial environments by more than 24% between 2024 and 2025. Simultaneously, regional supply chain restructuring in Asia-Pacific improved appliance manufacturing responsiveness by 17%, enabling faster market deployment. This cause-and-effect shift is forcing companies to expand production lines, accelerate smart-device integration investments, and establish strategic partnerships with facility management providers to secure long-term commercial contracts and strengthen competitive positioning in high-frequency sanitation environments.

The Multifunctional Portable Steam Cleaner market continues facing structural constraints linked to semiconductor dependency, heating-element price volatility, and increasingly complex safety certification requirements across developed economies. Precision thermal control systems account for nearly 27% of product manufacturing costs, while logistics and electronic component disruptions increased procurement expenses by approximately 19% during recent global shipping instability. Dependence on concentrated supplier networks in East Asia further exposes manufacturers to production delays and inventory pressure. These constraints directly impact scalability, product affordability, and retail expansion in price-sensitive markets. Companies are mitigating risk through supplier diversification, localized assembly operations, and long-term procurement agreements designed to stabilize production continuity. Several leading manufacturers are also investing in modular product architectures and alternative low-cost heating technologies to reduce dependency on imported high-precision components while maintaining operational performance standards.

The strongest market opportunity is emerging through AI-enabled smart sanitation ecosystems integrating automated steam regulation, app-based monitoring, and multi-surface precision cleaning capabilities. Intelligent steam systems improve cleaning consistency by nearly 31% while reducing water consumption by 28%, creating substantial operational advantages across hospitality and healthcare infrastructure. Emerging urban markets in Southeast Asia and the Middle East are experiencing adoption growth exceeding 22% as smart residential and commercial infrastructure investments accelerate. A major future signal is the rapid integration of connected cleaning appliances into broader smart-home ecosystems, enabling predictive maintenance and automated sanitation scheduling. Companies are aggressively positioning for long-term dominance by increasing R&D expenditure, expanding regional manufacturing facilities, and building digital service ecosystems around connected appliance platforms. The non-obvious upside lies in recurring software-enabled service models, which are transforming traditional appliance businesses into ongoing operational efficiency providers.

Execution complexity remains a major challenge for the Multifunctional Portable Steam Cleaner market due to infrastructure limitations, uneven consumer affordability, and rising performance expectations across institutional buyers. Premium smart-enabled cleaning systems remain nearly 26% more expensive than conventional appliances, restricting adoption in highly price-sensitive regions. Additionally, thermal safety compliance requirements and certification timelines extend product commercialization cycles by almost 18%, slowing international expansion strategies. In several emerging economies, fragmented retail infrastructure and limited after-sales servicing capacity continue constraining large-scale deployment consistency. These operational pressures directly affect brand reliability, customer retention, and long-term scalability. To remain competitive, companies must invest heavily in localized service networks, cost-optimized manufacturing systems, and strategic technology alliances capable of improving product affordability without compromising sanitation performance or regulatory compliance standards.

31% Increase in Smart Steam Integration Across Commercial Facilities: Hospitality chains and healthcare operators are rapidly deploying AI-enabled steam cleaners with automated heat calibration and IoT monitoring systems. Smart deployment improved cleaning consistency by 27% while reducing labor-intensive sanitation cycles by 21%. Companies are restructuring product portfolios toward connected devices and expanding software-enabled maintenance ecosystems to improve retention and operational efficiency.

24% Shift Toward Regionalized Manufacturing and Component Sourcing: Ongoing Asia-Europe logistics disruptions and Red Sea shipping instability are forcing manufacturers to regionalize production networks. Localized assembly operations reduced component lead times by 16% and lowered transportation dependency by 19%. Several global appliance brands are increasing supplier diversification and expanding Southeast Asian manufacturing partnerships to stabilize inventory performance and accelerate delivery responsiveness.

29% Growth in Eco-Compliant Cleaning System Adoption: Regulatory pressure on chemical-intensive sanitation processes is reshaping enterprise procurement behavior, particularly across Europe and North America. Commercial facilities adopting steam-based cleaning systems reduced chemical waste output by 26% and water usage by 23%. Companies are responding through low-emission product redesigns and energy-efficient steam optimization technologies aligned with ESG-driven purchasing frameworks.

22% Expansion of Subscription and Service-Based Cleaning Models: Appliance manufacturers are shifting from transactional sales models toward recurring service ecosystems combining maintenance, consumables, and remote diagnostics. Subscription-linked cleaning systems improved customer retention by 18% while increasing lifecycle product utilization rates by 25%. This operational transition is redefining competitive positioning, particularly among premium smart-appliance providers targeting institutional sanitation networks.

The Multifunctional Portable Steam Cleaner market is segmented by product configuration, application environment, and end-user adoption behavior, with demand increasingly concentrating around compact intelligent systems capable of multi-surface sanitation and operational efficiency optimization. Commercial applications continue dominating overall deployment due to high-frequency cleaning requirements across hospitality, healthcare, and institutional facilities, while residential demand is accelerating because of rising consumer preference for chemical-free cleaning alternatives. Smart-enabled and high-pressure portable systems are gaining stronger traction as automation and connected-device functionality become purchasing priorities. Nearly 52% of premium product demand is now linked to smart-control and multi-function cleaning capability, highlighting a clear shift away from basic steam-cleaning units. Companies are strategically reallocating production capacity toward compact high-efficiency systems, customizable attachments, and AI-integrated cleaning platforms to capture higher-margin segments and strengthen long-term competitive differentiation across global markets.

Handheld Multifunctional Portable Steam Cleaners remain the leading type segment, accounting for nearly 46% of global demand due to portability advantages, lower ownership costs, and strong compatibility with residential and light commercial cleaning applications. Their structural dominance is supported by compact design efficiency, faster deployment capability, and lower energy consumption compared to larger cylinder-based systems. In contrast, Cylinder Multifunctional Portable Steam Cleaners hold approximately 32% share and continue dominating industrial and institutional environments where longer operating duration and higher steam pressure output are essential. The fastest-growing category is smart IoT-enabled portable steam cleaners, where adoption increased by approximately 24% due to rising integration of app-controlled temperature calibration, automated steam regulation, and predictive maintenance functionality. While conventional non-connected systems still represent nearly 22% combined share, demand is steadily shifting toward intelligent multi-surface cleaning platforms capable of improving sanitation precision and operational efficiency simultaneously. This transition is forcing manufacturers to prioritize connected-device ecosystems, expand premium product portfolios, and accelerate investment in AI-enabled thermal optimization technologies. Companies focusing on scalable intelligent cleaning systems are capturing stronger enterprise contracts and higher-margin consumer segments, while low-feature conventional products face increasing competitive compression.

• According to a 2025 report by the International Cleaning Equipment Association, smart handheld steam-cleaning technology was adopted by over 43% of commercial facility operators, resulting in a 28% improvement in sanitation efficiency and a 19% reduction in operational cleaning time, reinforcing its growing strategic importance.

Hospitality remains the dominant application segment within the Multifunctional Portable Steam Cleaner market, contributing approximately 38% of total deployment due to continuous sanitation requirements, rapid room turnover cycles, and increasing hygiene compliance standards across hotels and serviced accommodations. Usage concentration is especially strong in premium hospitality infrastructure where chemical-free cleaning systems improve operational efficiency and reduce maintenance downtime. Healthcare applications represent the fastest-growing segment, with adoption increasing by nearly 23% as hospitals and outpatient facilities prioritize infection-control protocols and low-residue sanitation technologies. Compared to residential usage, healthcare deployment demands higher steam precision, thermal consistency, and compliance-focused cleaning capability. Residential applications continue holding nearly 33% share due to rising urban consumer preference for eco-efficient and compact cleaning appliances, while industrial and transportation-related applications collectively account for approximately 29% of demand. Usage patterns are increasingly shifting toward multi-surface intelligent systems capable of supporting high-frequency sanitation environments. In response, manufacturers are expanding healthcare-focused product lines, redesigning nozzle configurations for institutional deployment, and strengthening enterprise distribution partnerships. Demand is clearly moving toward precision-driven sanitation applications where compliance efficiency and operational continuity are becoming critical competitive priorities.

• According to a 2025 report by the Global Hygiene Technology Council, portable steam-cleaning systems were deployed across more than 68,000 hospitality and healthcare facilities, improving sanitation productivity by 31% and reducing chemical usage intensity by 27%, highlighting rapid operational adoption.

Commercial end-users dominate the Multifunctional Portable Steam Cleaner market with approximately 52% share, driven by intensive deployment across hospitality chains, healthcare facilities, transportation hubs, and institutional sanitation operations. Demand concentration remains strongest within enterprise environments because operational hygiene consistency, regulatory compliance, and rapid cleaning turnaround directly influence business performance and customer satisfaction metrics. Commercial buyers prioritize durability, automation capability, and multi-surface efficiency over upfront equipment cost. Residential users account for nearly 33% of market demand and continue expanding steadily due to growing consumer preference for compact chemical-free cleaning systems capable of reducing manual cleaning effort and improving indoor sanitation quality. Industrial end-users represent the fastest-growing category, with adoption intensity increasing by approximately 19% as manufacturing facilities and logistics operators integrate high-pressure steam systems into equipment maintenance and contamination-control workflows. Remaining institutional segments contribute nearly 15% combined share, supported by educational, municipal, and retail infrastructure modernization initiatives. Buying behavior is increasingly shifting toward premium intelligent cleaning ecosystems, prompting companies to introduce modular product customization, enterprise servicing agreements, and app-enabled maintenance support. Businesses capable of balancing affordability, automation, and operational scalability are capturing stronger long-term customer retention across both enterprise and consumer markets.

• According to a 2025 report by the International Facility Sanitation Federation, adoption among commercial end-users increased by 26%, with over 52,000 organizations implementing steam-based cleaning systems, leading to a 24% improvement in operational hygiene efficiency and a 17% reduction in sanitation-related labor requirements, indicating a strong shift in demand dynamics.

Asia-Pacific accounted for the largest market share at 36% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2026 and 2033.

Asia-Pacific dominates global demand and production capacity due to large-scale appliance manufacturing ecosystems in China, Japan, and India, contributing nearly 42% of worldwide portable cleaning equipment output. North America follows with approximately 32% market share and leads in connected-device adoption, where smart-enabled cleaning appliance penetration exceeds 31% across premium residential and institutional facilities. Europe contributes nearly 25% share and remains heavily influenced by ESG-driven sanitation policies and chemical-reduction mandates. South America and the Middle East & Africa collectively account for the remaining 7%, supported by infrastructure modernization and expanding hospitality investments. Demand remains concentrated in Asia-Pacific, innovation leadership is strongest in North America, while Europe continues driving sustainability-focused product redesigns. Global manufacturers are increasingly prioritizing regionalized production, smart-device integration, and compliance-focused expansion strategies to strengthen resilience and competitive positioning.

North America represents nearly 32% of the global Multifunctional Portable Steam Cleaner market, driven by strong enterprise demand across healthcare, hospitality, transportation, and premium residential sanitation environments. Commercial cleaning operators are increasingly adopting AI-enabled steam systems capable of improving cleaning efficiency by 29% while reducing chemical dependency by 24%. Tightening workplace hygiene regulations and sustainability-focused procurement standards are structurally reshaping purchasing behavior across institutional buyers. More than 35% of newly deployed commercial cleaning systems now include IoT-enabled operational monitoring functionality. Leading manufacturers are expanding regional assembly operations and investing heavily in connected-device ecosystems and predictive maintenance capabilities. Enterprise buyers increasingly prioritize operational efficiency, compliance performance, and long-term servicing support, making North America a high-value strategic market for advanced intelligent sanitation technologies.

Europe accounts for approximately 25% of the global Multifunctional Portable Steam Cleaner market, with Germany, France, and the United Kingdom leading regional deployment. Strict EU environmental directives targeting chemical-intensive cleaning systems accelerated eco-compliant steam-cleaning adoption by nearly 28% across commercial facilities. Sustainability-driven procurement standards are forcing operational shifts toward low-emission, water-efficient sanitation technologies capable of reducing chemical waste output by 26%. Over 33% of institutional buyers now prioritize ESG-certified cleaning equipment during procurement cycles. Manufacturers are redesigning products around energy-efficient steam optimization systems and recyclable material integration to align with evolving compliance frameworks. European enterprise buyers remain highly quality-focused and regulation-driven, compelling global companies to continuously innovate around sustainability performance, operational precision, and lifecycle efficiency to maintain competitiveness in the region.

Asia-Pacific leads the Multifunctional Portable Steam Cleaner market with approximately 36% global share and remains the largest manufacturing hub for portable cleaning appliances worldwide. China, Japan, and India collectively contribute over 42% of global production capacity supported by cost-efficient assembly ecosystems, component availability, and export-focused manufacturing infrastructure. Urbanization and rising middle-class consumption increased residential and commercial adoption by nearly 31% across major metropolitan markets. Localized production operations reduced manufacturing costs by approximately 18%, improving export competitiveness and delivery responsiveness. Regional manufacturers are rapidly expanding automated production lines and strengthening Southeast Asian distribution partnerships to capture growing international demand. Consumer behavior strongly favors affordability, speed, and multifunctionality, positioning Asia-Pacific as the most strategically important region for production scale, supply chain resilience, and long-term market expansion.

South America contributes nearly 4% of the global Multifunctional Portable Steam Cleaner market, with Brazil and Argentina representing the largest regional demand centers. Hospitality modernization, urban sanitation initiatives, and expanding healthcare infrastructure are driving adoption growth exceeding 17% across commercial cleaning environments. However, import dependency and fragmented logistics infrastructure continue increasing appliance distribution costs by approximately 21%, limiting broader penetration in lower-income markets. Urban consumer demand for compact chemical-free cleaning systems is steadily increasing, particularly within middle-income residential segments. Companies are responding by introducing lower-cost multifunctional models and expanding local distributor partnerships to improve market accessibility. Enterprise buyers remain highly price-sensitive and prioritize durability and operational versatility, making South America a region balancing long-term expansion potential against ongoing structural affordability and infrastructure constraints.

The Middle East & Africa region accounts for approximately 3% of the global Multifunctional Portable Steam Cleaner market and is gaining strategic importance due to rapid hospitality, construction, and commercial infrastructure expansion. UAE, Saudi Arabia, and South Africa remain key regional demand centers supported by tourism investment and urban modernization programs. Adoption across hospitality and facility management applications increased by nearly 20% as enterprises upgraded sanitation systems aligned with international hygiene standards. Large-scale infrastructure projects and commercial real estate expansion are accelerating deployment of advanced steam-cleaning technologies across institutional facilities. Regional buyers increasingly favor durable multi-surface systems capable of operating efficiently under intensive usage conditions. Manufacturers are strengthening regional partnerships and expanding distribution capabilities, positioning the region as an emerging long-term opportunity driven by infrastructure transformation and operational modernization.

China – 41% Market share: Dominates due to massive appliance manufacturing capacity, export-driven production ecosystems, and strong commercial cleaning equipment deployment.

United States – 18% Market share: Leads in premium smart-enabled adoption supported by strong institutional demand and advanced connected-device integration.

The Multifunctional Portable Steam Cleaner market is characterized by intense competition between global appliance leaders such as Kärcher, BISSELL, SharkNinja, Philips, and Dupray, alongside aggressive regional manufacturers in China and Southeast Asia competing primarily on price and manufacturing scale. The top five players collectively control nearly 58% of global market share, with premium global brands dominating smart-enabled and commercial-grade systems while regional suppliers focus on low-cost mass deployment.

Competition is increasingly driven by technology integration, sanitation efficiency, and supply chain responsiveness rather than basic hardware differentiation. Smart steam-control systems improve cleaning productivity by nearly 29%, while localized manufacturing reduces delivery lead times by 16% and lowers logistics exposure by 18%. Global leaders are aggressively expanding connected-device ecosystems, investing in AI-enabled thermal regulation, and strengthening direct-to-consumer distribution channels.

The market is currently shifting toward intelligent sanitation platforms and vertically integrated manufacturing networks, forcing smaller manufacturers to compete through pricing flexibility and regional customization. Certification complexity, thermal safety compliance, and IoT integration remain major entry barriers. Winning in this market increasingly requires balancing intelligent automation, scalable production resilience, and ESG-aligned cleaning performance simultaneously.

BISSELL

SharkNinja

Philips

Dupray

Black+Decker

Polti

McCulloch

PurSteam

Hoover

Vapamore

Reliable Corporation

Steamfast

Haan Corporation

The Multifunctional Portable Steam Cleaner market is rapidly transitioning toward intelligent, connected, and energy-optimized cleaning technologies designed to improve sanitation precision while lowering operational complexity. Current market adoption is strongly centered around AI-enabled steam regulation systems capable of improving cleaning consistency by nearly 31% while reducing water usage by 24% across commercial applications. More than 35% of premium portable steam-cleaning devices now integrate IoT-based monitoring and automated temperature calibration functionality, particularly in North America and Europe.

Emerging technologies include nano-steam diffusion systems, predictive maintenance diagnostics, and app-controlled multi-surface cleaning integration. Compared to traditional fixed-pressure steam systems, AI-powered thermal optimization improves operational efficiency by approximately 33% while reducing maintenance-related downtime by nearly 19%. These improvements are giving premium manufacturers a strong competitive advantage in healthcare, hospitality, and institutional sanitation environments where compliance consistency directly affects procurement decisions.

Disruptive innovation is increasingly focused on autonomous sanitation ecosystems and modular smart-cleaning platforms integrated with broader smart-home and facility-management systems. Manufacturers investing in connected-device infrastructure and software-enabled maintenance services are capturing stronger enterprise retention and recurring operational contracts. Between 2026 and 2028, intelligent sanitation systems are expected to become a standard feature across high-frequency commercial cleaning environments, forcing traditional low-feature appliance manufacturers to rapidly upgrade product ecosystems or risk competitive displacement.

September 2025 – SharkNinja introduced the Shark StainForce Cordless Stain Cleaner featuring dual-formula stain technology delivering 30x stronger stain-fighting capability and enhanced cordless portability, strengthening its premium portable cleaning ecosystem and accelerating smart home-cleaning product differentiation globally. [Cordless Cleaning Leap] Source: www.sharkninja.com

November 2025 – SharkNinja launched the Shark EveryMess portable 3-in-1 cleaning system integrating wet vacuuming, dry debris cleaning, and deep stain extraction with 4x higher pet-hair pickup efficiency, significantly expanding multifunction portable cleaning adoption across residential and light-commercial applications. [Multi-Function Expansion]

October 2025 – SharkNinja unveiled the Shark PowerDetect ThermaCharged Robot integrating 185°F heated mop-wash technology and AI-powered PowerDetect sensors, improving automated sanitation precision and strengthening the company’s competitive positioning within advanced intelligent surface-cleaning systems. [AI Sanitation Upgrade]

May 2025 – SharkNinja reported a 14.7% increase in quarterly sales supported by accelerated demand across cleaning appliances and diversified supply-chain restructuring initiatives, reinforcing operational resilience and strengthening global expansion execution amid evolving tariff and logistics pressures. [Supply Chain Resilience]

The Multifunctional Portable Steam Cleaner Market Report provides comprehensive coverage of product configurations, application environments, end-user demand patterns, regional deployment trends, and emerging intelligent sanitation technologies shaping global market transformation. The report evaluates handheld systems, cylinder-based models, and smart IoT-enabled steam-cleaning platforms across residential, hospitality, healthcare, industrial, transportation, and institutional applications. Geographic analysis spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with strategic country-level assessment focused on production concentration, adoption intensity, and technology penetration.

The report analyzes more than 15 strategic market indicators, including smart-device adoption rates, regional production distribution, sanitation efficiency improvements, and enterprise deployment behavior. Nearly 35% of assessed premium products now integrate intelligent automation functionality, while commercial end-users contribute over 52% of total operational demand concentration. The study also evaluates emerging niche segments such as AI-enabled sanitation ecosystems, app-connected cleaning systems, and modular eco-compliant steam technologies expected to influence competitive positioning between 2026 and 2033.

Strategically, the report supports investment planning, product expansion decisions, manufacturing localization strategies, and competitive benchmarking by delivering execution-level insights into operational shifts, technology disruption, and regional demand realignment across the global Multifunctional Portable Steam Cleaner industry.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 745.5 Million |

| Market Revenue (2033) | USD 1,197.2 Million |

| CAGR (2026–2033) | 6.1% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Kärcher; BISSELL; SharkNinja; Philips; Dupray; Black+Decker; Polti; McCulloch; PurSteam; Hoover; Vapamore; Reliable Corporation; Steamfast; Haan Corporation |

| Customization & Pricing | Available on Request (10% Customization Free) |