Reports

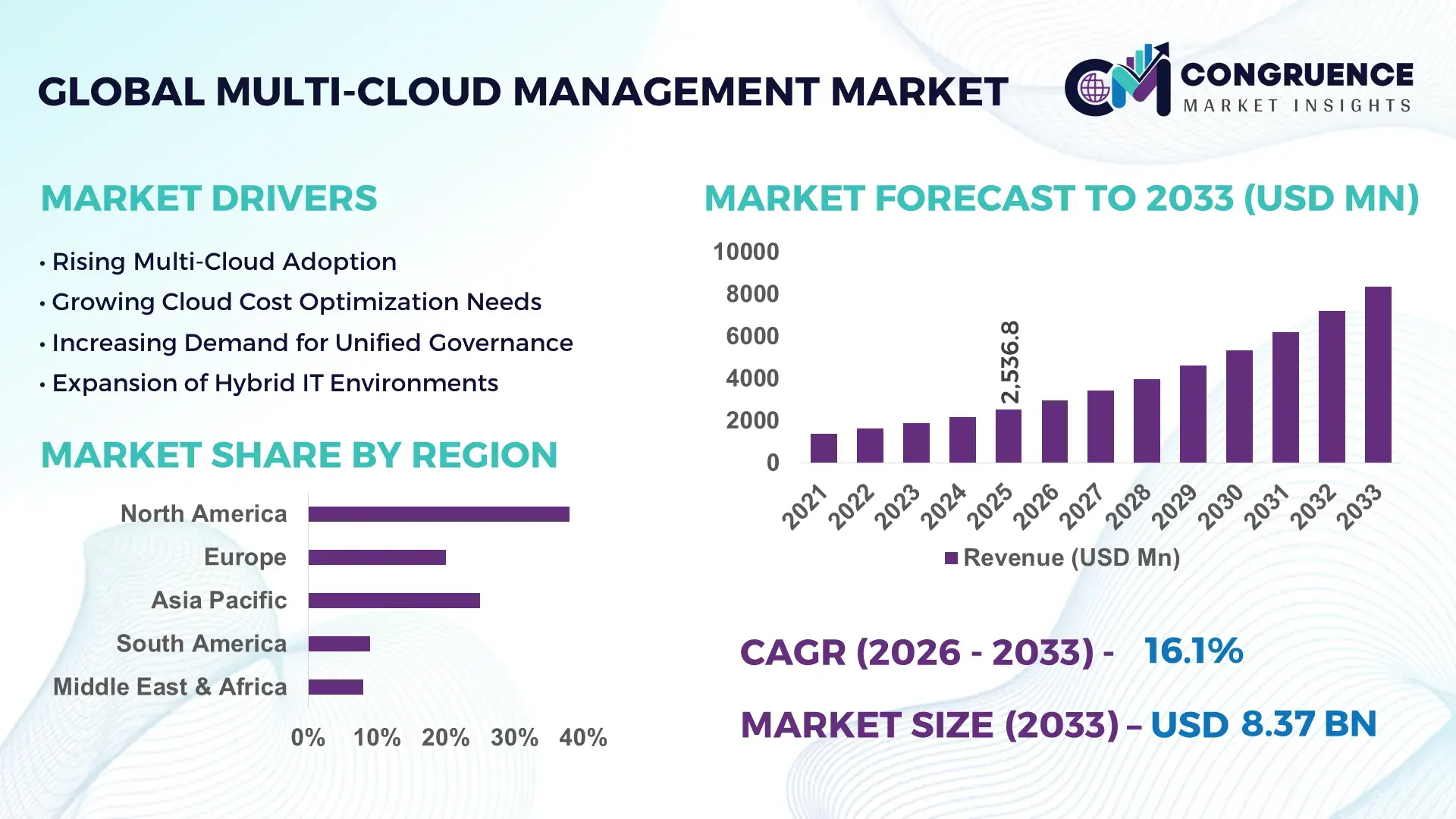

The Global Multi-Cloud Management Market was valued at USD 2536.78 Million in 2025 and is anticipated to reach a value of USD 8374.17 Million by 2033 expanding at a CAGR of 16.1% between 2026 and 2033. Enterprise cloud modernization strategies intensified in 2026 as large organizations shifted mission-critical workloads across hybrid and distributed cloud environments to improve workload portability, reduce infrastructure concentration risks, and strengthen compliance monitoring across regional data frameworks.

The United States dominates the global multi-cloud management market with nearly 36% market share, supported by hyperscale cloud and AI infrastructure investments exceeding USD 95 billion between 2024 and 2026. More than 72% of Fortune 1000 enterprises operate workloads across three or more cloud platforms, particularly within financial services, retail, defense, and healthcare industries. Following rising geopolitical cybersecurity tensions linked to Eastern European cyber incidents, federal digital infrastructure programs accelerated secure multi-cloud adoption and zero-trust cloud governance deployment. Compared with Western Europe, U.S. enterprises achieve approximately 29% faster cloud workload migration due to mature DevSecOps ecosystems, higher AI integration levels, and stronger enterprise automation spending.

Organizations prioritizing interoperable cloud governance, workload observability, and automated policy enforcement are securing stronger operational resilience and lower long-term infrastructure dependency exposure.

Market Size & Growth: USD 2536.78 Million in 2025 advancing toward USD 8374.17 Million by 2033 at 16.1% growth, driven by enterprise AI infrastructure expansion and hybrid cloud modernization.

Top Growth Drivers: AI-based workload optimization improves cloud efficiency by 34%, Kubernetes adoption exceeds 61%, and sovereign cloud deployments rise by 28% globally.

Short-Term Forecast: By 2027, automated cloud governance platforms are projected to reduce enterprise cloud operating costs by 26% while improving deployment speed by 31%.

Emerging Technologies: AIOps, container orchestration, and predictive cloud analytics improve infrastructure utilization by 37% across advanced multi-cloud ecosystems.

Regional Leaders: North America surpasses USD 3.1 billion through hyperscale AI adoption, Europe exceeds USD 1.9 billion with sovereign cloud expansion, and Asia-Pacific crosses USD 2.4 billion through telecom and manufacturing cloud transformation.

Consumer/End-User Trends: More than 68% of large enterprises now manage workloads across three or more cloud providers to improve operational continuity and compliance flexibility.

Pilot/Case Example: In 2026, a multinational banking deployment reduced cloud provisioning time by 43% through AI-enabled multi-cloud automation integration.

Competitive Landscape: Top five vendors collectively control nearly 48% market share, with competition centered on automation depth, interoperability, cybersecurity integration, and cost governance capabilities.

Regulatory & ESG Impact: Data localization policies and energy-efficient cloud optimization frameworks lowered enterprise infrastructure power consumption by 18% across regulated industries.

Investment & Funding: Global enterprise cloud modernization investments exceeded USD 28 billion in 2026, led by AI partnerships, sovereign cloud infrastructure, and regional data center expansion.

Innovation & Future Outlook: Autonomous cloud operations, edge-integrated orchestration, and generative AI-based infrastructure governance are reshaping next-generation multi-cloud management strategies.

BFSI contributes nearly 29% of total market demand due to rising cross-border digital transaction infrastructure and regulatory compliance requirements, while telecom and healthcare collectively account for over 34% through distributed application deployment and secure data management initiatives. AI-driven cloud observability platforms, autonomous workload balancing, and predictive infrastructure analytics are emerging as major technology innovations improving operational efficiency across enterprise environments. North America leads adoption, while Asia-Pacific records the fastest deployment growth due to aggressive digital infrastructure investments and regional supply chain diversification strategies following semiconductor and cybersecurity disruptions. Increasing integration of edge computing with multi-cloud governance platforms is positioning enterprises for highly automated and resilient distributed IT ecosystems over the next decade.

Multi-cloud management platforms have become strategically critical as enterprises prioritize operational resilience, vendor diversification, and AI-ready infrastructure modernization across globally distributed digital environments. Rising regulatory scrutiny around data localization and cybersecurity compliance is accelerating deployment across banking, healthcare, manufacturing, and telecom sectors. More than 67% of large enterprises now operate across multiple cloud ecosystems to reduce service concentration risks and improve workload continuity during infrastructure disruptions linked to global supply-chain instability and rising geopolitical cyber threats.

AI-enabled multi-cloud orchestration platforms deliver nearly 35% faster workload provisioning and reduce infrastructure idle costs by approximately 28% compared with legacy centralized cloud administration systems. North America leads in advanced automation integration and cloud-native deployment maturity, while Asia-Pacific records faster infrastructure scaling due to rapid digital transformation investments across India, Singapore, and South Korea. Over the next two to three years, containerized workload deployment is projected to exceed 70% among enterprise cloud environments as organizations prioritize interoperability and real-time resource optimization.

Global enterprises are increasingly forming strategic partnerships with cloud security providers and edge infrastructure specialists to strengthen observability and distributed governance capabilities. In 2026, several multinational retailers integrated AI-driven cloud monitoring platforms to improve application uptime and reduce cross-cloud latency by over 22%. Companies prioritizing intelligent orchestration, compliance automation, and scalable cloud governance frameworks are strengthening long-term competitive positioning across highly digitized industries.

Enterprise adoption of AI-driven workloads and distributed digital operations is accelerating demand for advanced multi-cloud management platforms across banking, telecom, healthcare, and manufacturing industries. More than 64% of large enterprises now deploy applications across at least three cloud environments to improve operational continuity and reduce infrastructure dependency risks. Kubernetes-based orchestration adoption increased by nearly 39% between 2024 and 2026 as organizations prioritized automated workload balancing and scalable application deployment. Following stricter data localization regulations in countries including India and Germany, enterprises are restructuring cloud architectures to support region-specific compliance management and sovereign data control. Major technology providers are expanding regional cloud partnerships and AI-enabled governance capabilities to reduce deployment complexity and strengthen interoperability. Companies integrating predictive cloud analytics and automated policy enforcement are achieving approximately 31% faster infrastructure optimization cycles and stronger operational resilience.

Complex interoperability requirements and rising cloud governance costs remain major structural restraints for enterprise-scale multi-cloud deployment. Nearly 46% of enterprises report operational inefficiencies caused by inconsistent API architectures and fragmented workload visibility across multiple cloud providers. Cross-cloud data transfer expenses increased by approximately 21% in 2026 as AI-driven applications generated significantly higher processing and storage traffic. In the United States and parts of Western Europe, enterprises face growing compliance pressure linked to cybersecurity auditing, regional data residency mandates, and infrastructure transparency requirements, increasing deployment and monitoring complexity. Vendor-specific integration limitations continue to slow migration timelines and reduce operational flexibility for mid-sized organizations. To reduce dependency risks, companies are investing in open-source orchestration frameworks, localized data infrastructure, and long-term interoperability partnerships while prioritizing automated governance tools to improve cloud cost predictability and infrastructure control.

Sovereign cloud infrastructure development and AI-enabled automation are creating high-value opportunities for multi-cloud management providers across regulated industries and emerging digital economies. More than 58% of enterprises in India, the UAE, and Germany are restructuring cloud architectures to align with national data residency requirements and localized cybersecurity frameworks. AI-based workload orchestration platforms are reducing cloud resource overprovisioning by nearly 33%, while automated observability tools improve cross-cloud incident response efficiency by approximately 29%. Governments are accelerating digital infrastructure modernization through sovereign cloud incentives and public-private cloud partnerships, particularly in healthcare, financial services, and smart manufacturing ecosystems. Companies are expanding R&D investments into autonomous cloud governance, edge-integrated orchestration, and carbon-aware workload balancing to differentiate enterprise offerings. A non-obvious growth opportunity is emerging within mid-sized industrial enterprises seeking lower-cost multi-cloud optimization platforms to manage AI-enabled operational technology infrastructure without hyperscale deployment complexity.

Long-term scalability challenges are intensifying as enterprises manage increasingly complex cloud-native environments across distributed infrastructure ecosystems. Nearly 49% of organizations report shortages in advanced cloud governance and Kubernetes orchestration expertise, slowing enterprise-wide deployment consistency and increasing operational dependency on external managed service providers. In Japan and the United States, rising AI workload density has increased multi-cloud infrastructure latency and observability complexity by approximately 24%, particularly within real-time analytics and edge-computing operations. Cybersecurity pressures are also expanding as multi-cloud attack surfaces grow across hybrid enterprise architectures, increasing compliance monitoring costs and operational risk exposure. Companies must strengthen unified governance frameworks, AI-driven anomaly detection systems, and workforce reskilling programs to maintain deployment scalability and service continuity. Enterprises failing to standardize cloud interoperability layers risk higher infrastructure fragmentation, lower automation efficiency, and weaker long-term competitive adaptability.

AI-Led Cloud Automation Expansion Enterprise adoption of AI-driven cloud automation platforms increased by nearly 42% during 2026 as organizations prioritized predictive workload balancing and autonomous infrastructure provisioning. Large financial institutions in the United States reduced cloud incident resolution time by approximately 36% through AIOps integration. Companies are expanding partnerships with observability providers and automation specialists to improve operational continuity amid rising cybersecurity and compliance pressure.

Sovereign Data Infrastructure Acceleration National data localization regulations in India, Germany, and Saudi Arabia are reshaping enterprise cloud deployment models. More than 47% of regulated enterprises now prioritize sovereign cloud-compatible orchestration platforms to maintain regional compliance and infrastructure transparency. Multi-cloud vendors are restructuring deployment strategies through localized data center alliances and compliance-focused governance tools, creating stronger demand for region-specific workload management capabilities.

Edge-Oriented Hybrid Deployment Shift Telecom operators and manufacturing companies increased edge-integrated multi-cloud deployments by nearly 38% in 2026 to support low-latency analytics and industrial automation workloads. Distributed orchestration frameworks are improving application response efficiency by approximately 27% compared with centralized architectures. Companies are scaling edge-cloud interoperability investments to support AI-enabled production systems and real-time operational intelligence across supply-chain networks.

FinOps and Cost Governance Adoption Enterprise cloud spending optimization has become a strategic priority as cross-cloud operational costs rise alongside AI workload intensity. More than 61% of enterprises now deploy FinOps-based governance frameworks to improve infrastructure visibility and reduce idle resource consumption. Organizations in Singapore and Canada are integrating automated cost allocation tools and predictive usage analytics to improve budget accuracy while strengthening procurement and vendor management strategies.

Security Management remains the leading segment within the multi-cloud management market due to rising enterprise focus on zero-trust architecture, compliance automation, and cross-cloud threat visibility. Nearly 44% of large enterprises prioritize unified security governance platforms to manage distributed workloads and AI-driven applications across hybrid environments. Cloud Automation is emerging as the fastest-growing segment as organizations accelerate AI-enabled orchestration and autonomous infrastructure optimization, improving deployment efficiency by approximately 35%. Mature segments such as Cloud Monitoring and Infrastructure Management continue supporting operational visibility and workload stability, particularly across telecom and financial services environments. Cost Management platforms are also gaining traction as enterprises seek stronger FinOps integration to control escalating AI infrastructure expenses. Companies are responding through integrated security analytics, automated remediation capabilities, and multi-platform orchestration partnerships to improve operational resilience and enterprise scalability.

Workload Management dominates the application landscape as enterprises prioritize seamless workload distribution, application portability, and infrastructure resilience across multiple cloud ecosystems. More than 63% of global enterprises now deploy advanced workload orchestration tools to improve operational continuity and reduce dependency on single-cloud infrastructure. Resource Optimization is the fastest-growing application segment, driven by rising AI infrastructure costs and increasing demand for automated cloud efficiency management, with enterprises reporting nearly 31% reductions in idle resource consumption. Disaster Recovery and Data Backup remain critical for regulated sectors including BFSI and healthcare, where operational downtime and compliance failures create significant financial exposure. Application Management and Compliance Management are also expanding as organizations integrate cloud-native DevSecOps frameworks and region-specific governance protocols. Companies are strengthening automation capabilities, hybrid integration strategies, and predictive analytics deployment to improve operational agility and infrastructure control.

BFSI remains the leading end-user segment due to high dependency on secure digital transaction infrastructure, regulatory compliance frameworks, and real-time workload availability. Nearly 34% of enterprise-scale multi-cloud deployments originate from banking and financial institutions managing distributed payment systems, fraud analytics, and AI-driven customer operations. Healthcare is emerging as the fastest-growing end-user segment as hospitals and healthcare networks accelerate cloud-based clinical analytics, telemedicine platforms, and patient data interoperability initiatives. IT and Telecom sectors continue investing heavily in edge-integrated orchestration and low-latency cloud infrastructure to support 5G-enabled applications and distributed data traffic management. Manufacturing and Retail enterprises are increasingly adopting multi-cloud governance platforms to improve supply-chain visibility, predictive maintenance, and omnichannel digital operations. Companies are expanding sector-specific cloud partnerships, cybersecurity customization, and compliance-driven deployment models to strengthen competitive differentiation and enterprise retention.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 18.4% between 2026 and 2033.

AI-Integrated Enterprise Cloud Leadership

North America maintains leadership in the multi-cloud management market due to strong hyperscale infrastructure concentration, enterprise AI adoption, and advanced DevSecOps deployment maturity. Nearly 72% of large enterprises in the region operate across three or more cloud platforms to improve operational continuity and reduce infrastructure concentration risk. Financial services, healthcare, and telecom sectors continue accelerating investment in AI-driven orchestration and cloud governance automation. In 2026, multiple U.S.-based hyperscale operators expanded sovereign cloud partnerships and edge-cloud integration programs to improve workload distribution efficiency by approximately 28%. Strong cybersecurity compliance enforcement and high enterprise cloud migration intensity continue positioning the region as the global center for advanced multi-cloud infrastructure management and automation deployment.

United States Market Outlook: The United States leads regional deployment activity through high enterprise cloud spending, mature AI infrastructure ecosystems, and strong hyperscale data center concentration. More than 74% of Fortune 1000 companies deploy multi-cloud governance platforms across distributed business operations, particularly in BFSI, defense, and retail sectors. Federal cybersecurity modernization initiatives and zero-trust compliance frameworks are accelerating cloud orchestration adoption, while enterprise investment in predictive cloud optimization tools continues strengthening operational resilience and infrastructure scalability.

Sovereign Cloud and Compliance Modernization

Europe is strengthening its position through sovereign cloud infrastructure expansion, regulatory modernization, and enterprise cybersecurity transformation. Approximately 61% of regulated enterprises across Germany, France, and the Netherlands prioritize region-specific cloud governance platforms to comply with data residency and infrastructure transparency mandates. Manufacturing, banking, and public-sector organizations are increasing deployment of automated compliance management and cross-cloud monitoring systems to improve operational control. In 2026, several European cloud alliances accelerated localized infrastructure partnerships supporting low-latency workload management and carbon-efficient cloud operations. Sustainability-linked digital infrastructure policies are also encouraging enterprises to integrate energy-efficient workload orchestration technologies, improving cloud utilization efficiency by nearly 24% across enterprise environments.

Germany Market Outlook: Germany leads the European market due to strong industrial cloud adoption, advanced manufacturing digitization, and strict enterprise cybersecurity standards. More than 58% of large German manufacturers now deploy hybrid and multi-cloud frameworks to support industrial automation and predictive maintenance systems. Government-backed digital sovereignty initiatives and rising investment in localized data infrastructure continue accelerating enterprise migration toward secure cloud-native operational ecosystems across automotive, engineering, and financial sectors.

High-Speed Digital Infrastructure Expansion

Asia-Pacific is emerging as the fastest-growing multi-cloud management market due to rapid enterprise digitization, hyperscale infrastructure expansion, and accelerating AI-enabled cloud adoption. Countries including India, China, Singapore, and South Korea are increasing investment in distributed cloud ecosystems to support telecom modernization, e-commerce expansion, and industrial automation. More than 66% of large enterprises in the region now prioritize multi-cloud deployment to strengthen scalability and reduce operational downtime risks. In 2026, regional telecom operators expanded edge-integrated cloud infrastructure projects supporting 5G-enabled analytics and real-time application orchestration. Manufacturing and retail sectors are increasingly integrating AI-driven cloud monitoring tools to improve operational efficiency and supply-chain visibility across distributed enterprise networks.

India Market Outlook: India is becoming a strategic growth hub due to aggressive digital infrastructure expansion, rising enterprise cloud migration, and supportive data localization initiatives. More than 63% of large Indian enterprises adopted hybrid or multi-cloud governance frameworks by 2026, particularly across banking, telecom, healthcare, and e-commerce sectors. Rapid hyperscale data center construction, AI startup ecosystem growth, and government-backed digital transformation programs are strengthening enterprise demand for scalable cloud orchestration and compliance automation platforms.

Enterprise Modernization and Connectivity Expansion

South America is experiencing steady multi-cloud management adoption as enterprises modernize digital infrastructure and improve operational resilience across banking, telecom, and retail sectors. Brazil and Chile account for a major share of enterprise cloud deployments due to increasing investment in regional data infrastructure and cybersecurity modernization. Approximately 46% of large enterprises in the region expanded hybrid cloud operations during 2026 to improve workload flexibility and disaster recovery capabilities. However, infrastructure fragmentation and inconsistent connectivity standards continue limiting deployment scalability in secondary markets. Companies are responding through localized partnerships, managed cloud services expansion, and AI-enabled operational monitoring to improve enterprise cloud efficiency and infrastructure control across distributed operational environments.

Brazil Market Outlook: Brazil dominates the regional market through strong enterprise cloud migration activity, expanding financial technology ecosystems, and rising telecom infrastructure investment. Nearly 57% of large enterprises in Brazil increased deployment of multi-cloud workload management systems to support digital banking and omnichannel retail operations. Local enterprises are also strengthening cybersecurity frameworks and regional cloud partnerships to improve compliance readiness and operational continuity amid rising digital transaction volumes.

Digital Sovereignty and Infrastructure Diversification

The Middle East & Africa market is expanding through aggressive digital transformation programs, sovereign cloud investments, and enterprise modernization initiatives. Gulf countries are accelerating deployment of localized cloud infrastructure to support financial services, smart city operations, and government digitalization strategies. Approximately 52% of large enterprises in the UAE and Saudi Arabia increased investment in AI-enabled cloud governance tools during 2026 to improve workload visibility and cybersecurity resilience. Regional telecom providers are also expanding edge-cloud integration partnerships to support low-latency industrial applications and distributed analytics. Infrastructure maturity gaps across several African economies continue limiting deployment consistency, although rising public-private cloud partnerships are improving regional enterprise cloud accessibility.

Saudi Arabia Market Outlook: Saudi Arabia leads regional deployment momentum through large-scale digital infrastructure programs and sovereign cloud investment strategies aligned with national economic diversification goals. More than 54% of enterprise organizations in the country accelerated migration toward multi-cloud governance frameworks to strengthen operational continuity and regulatory compliance. Expansion of hyperscale data centers, AI-focused digital initiatives, and telecom modernization projects continues positioning the country as a strategic cloud infrastructure hub within the Middle East.

Global cloud leaders including Microsoft, IBM, VMware, Cisco, and Oracle compete directly against cloud-native automation specialists and regional managed service providers focused on interoperability and governance efficiency. The top five players collectively control nearly 48% of the market through integrated orchestration ecosystems, enterprise security capabilities, and large-scale cloud partnership networks. Competition is increasingly shaped by automation depth, AI-driven observability, deployment speed, and cross-platform compatibility, with advanced orchestration reducing enterprise workload management time by approximately 34%. Vendors are strengthening positions through sovereign cloud alliances, edge-infrastructure partnerships, and acquisition-led portfolio expansion targeting regulated industries and AI-intensive workloads. Technology innovators compete on predictive analytics and autonomous cloud governance, while cost-focused providers emphasize flexible deployment models and localized support capabilities. Rising cybersecurity complexity and integration standardization requirements create strong entry barriers. Winning against established competitors requires scalable interoperability, automated governance precision, and industry-specific compliance intelligence.

VMware, Inc.

Cisco Systems, Inc.

Broadcom Inc.

BMC Software, Inc.

Flexera Software LLC

Rackspace Technology, Inc.

CloudBolt Software, Inc.

Nutanix, Inc.

ServiceNow, Inc.

Citrix Systems, Inc.

Snow Software AB

AI-driven orchestration, Kubernetes-native automation, and unified observability platforms are reshaping enterprise multi-cloud management architectures. More than 68% of large enterprises now deploy AI-enabled monitoring systems to improve workload allocation and reduce infrastructure downtime. Advanced AIOps platforms lower incident response time by nearly 36%, while automated resource optimization reduces idle cloud expenditure by approximately 29%. Compared with legacy centralized cloud administration models, modern containerized orchestration frameworks improve deployment speed by over 41% and strengthen workload portability across distributed environments. Financial institutions and telecom operators are gaining competitive advantage through predictive analytics integration and real-time policy enforcement across hybrid cloud ecosystems.

Emerging technologies between 2026 and 2028 include autonomous cloud governance, edge-cloud synchronization frameworks, and sovereign cloud orchestration platforms supporting localized compliance requirements. Nearly 52% of enterprises in Germany, India, and Singapore are prioritizing sovereign cloud-compatible infrastructure management tools following stricter cybersecurity and data residency regulations. Companies integrating carbon-aware workload balancing systems are also improving energy efficiency by approximately 18% across hyperscale cloud operations while reducing operational complexity in distributed AI environments.

Disruptive innovation is accelerating through generative AI-based infrastructure management and multi-cloud FinOps automation platforms. Enterprises deploying predictive cost-governance engines are improving infrastructure utilization by nearly 33% while reducing cross-cloud latency through edge-integrated orchestration. Cloud providers and enterprise software vendors investing early in AI-native governance ecosystems, interoperability frameworks, and zero-trust automation capabilities are strengthening long-term enterprise retention and operational scalability advantages.

June 2024 – Oracle and Google Cloud announced a strategic multicloud partnership integrating Oracle Database services within Google Cloud infrastructure across 11 regions, improving deployment interoperability and reducing cross-cloud transfer costs for enterprise modernization initiatives. Source: oracle.com

March 2024 – Microsoft and Oracle expanded Oracle Database@Azure availability to 15 planned cloud regions, strengthening enterprise multicloud deployment flexibility and accelerating AI-integrated workload migration capabilities across Europe and North America. Source: news.microsoft.com

October 2025 – Oracle and AMD expanded AI infrastructure collaboration with planned deployment of 50,000 GPUs for next-generation OCI AI superclusters, significantly increasing multicloud AI processing scale and enterprise computational efficiency. Source: reddit.com/r/amd_fundamentals

April 2026 – Stellantis and Microsoft signed a five-year AI and cloud modernization partnership involving over 100 AI-driven initiatives, targeting 60% data-center footprint reduction through Azure-enabled multicloud infrastructure optimization. Source: reuters.com

The report provides comprehensive analysis of the multi-cloud management market across core technology segments including cloud automation, security management, infrastructure management, cloud monitoring, and cost governance platforms. It evaluates operational deployment trends across workload management, disaster recovery, compliance management, application management, resource optimization, and enterprise backup environments. More than 65% of enterprise-scale deployments assessed within the study involve hybrid or distributed multi-cloud architectures integrating AI-enabled orchestration and Kubernetes-based automation frameworks.

The study covers strategic demand analysis across BFSI, healthcare, IT and telecom, manufacturing, government, and retail sectors while evaluating deployment intensity across North America, Europe, Asia-Pacific, South America, and Middle East & Africa. The report also assesses enterprise adoption patterns linked to sovereign cloud infrastructure, edge-integrated orchestration, AI-driven observability, and FinOps optimization platforms between 2026 and 2033. Strategic insights support expansion planning, cloud investment prioritization, competitive benchmarking, infrastructure modernization, and long-term digital transformation decision-making across enterprise cloud ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 2536.78 Million |

|

Market Revenue in 2033 |

USD 8374.17 Million |

|

CAGR (2026 - 2033) |

16.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Microsoft Corporation, IBM Corporation, Oracle Corporation, VMware, Inc., Cisco Systems, Inc., Broadcom Inc., BMC Software, Inc., Flexera Software LLC, Rackspace Technology, Inc., CloudBolt Software, Inc., Nutanix, Inc., ServiceNow, Inc., Citrix Systems, Inc., Snow Software AB |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |