Reports

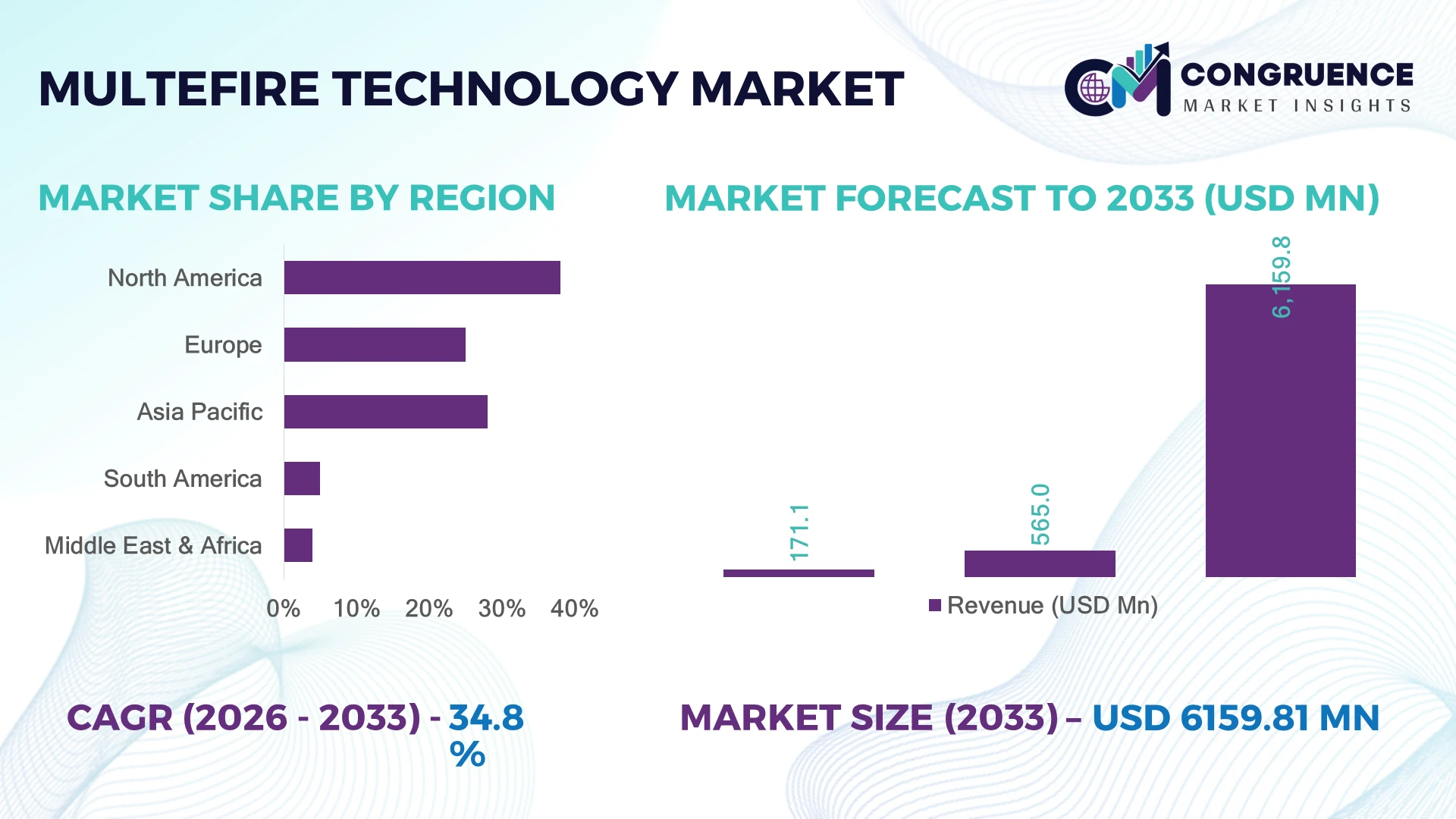

The Global MulteFire Technology Market was valued at USD 565.0 Million in 2025 and is anticipated to reach a value of USD 6,159.8 Million by 2033 expanding at a CAGR of 34.8% between 2026 and 2033. Growth is driven by private wireless network deployments, industrial IoT expansion, spectrum-sharing innovations, and demand for secure high-performance connectivity across enterprise environments.

The United States dominates the MulteFire Technology landscape with nearly 38% market share, supported by private 5G investments, advanced manufacturing, and enterprise automation initiatives exceeding USD 100 billion annually. China follows with around 25% share, driven by industrial digitalization and smart factory deployments, while U.S. adoption of private wireless solutions remains over 20% higher than several emerging markets. The global expansion of Industry 4.0 initiatives after the U.S. CHIPS Act and regional semiconductor investments strengthens technology adoption.

Strategic investment should prioritize enterprise-grade wireless infrastructure, industrial connectivity, and scalable private network ecosystems.

Market Size & Growth: USD 565.0 Million in 2025 to USD 6,159.8 Million by 2033, expanding at 34.8% CAGR, driven by private wireless networks and Industry 4.0 connectivity.

Top Growth Drivers: Industrial IoT adoption (35%), enterprise automation (32%), and private network deployment (30%) are accelerating global MulteFire demand.

Short-Term Forecast: By 2028, enterprises achieve 25% lower connectivity costs and 40% higher network reliability through advanced private wireless systems.

Emerging Technologies: AI-enabled network optimization, edge computing integration, and advanced spectrum-sharing technologies are reshaping MulteFire deployments.

Regional Leaders: North America reaches USD 2.3 billion, Asia Pacific USD 2.1 billion, and Europe USD 1.2 billion by 2033, supported by industrial wireless adoption.

Consumer/End-User Trends: Over 45% of industrial enterprises are prioritizing private wireless connectivity for automation, robotics, and real-time monitoring applications.

Pilot/Case Example: A 2024 smart manufacturing deployment using private wireless networks achieved 30% faster operational response and 20% downtime reduction.

Competitive Landscape: Key players include Qualcomm, Nokia, Ericsson, Cisco, and Huawei, with leading vendors capturing significant enterprise deployments.

Regulatory & ESG Impact: Spectrum-sharing policies and energy-efficient networking solutions reduce enterprise network energy consumption by approximately 20%.

Investment & Funding: More than USD 15 billion is being directed toward private wireless, 5G infrastructure, and industrial connectivity partnerships globally.

Innovation & Future Outlook: Next-generation MulteFire solutions integrate AI orchestration, edge intelligence, and seamless private-public network convergence for strategic enterprise transformation.

MulteFire Technology is becoming essential for factories, logistics hubs, ports, and critical infrastructure requiring secure wireless connectivity without dependence on traditional licensed networks. Innovations in cloud-native network management, edge processing, and automated spectrum allocation are expanding application opportunities, with industrial users reporting up to 35% improvement in operational visibility. Growing private network adoption across manufacturing regions and evolving spectrum regulations are creating a stronger foundation for scalable wireless ecosystems, leading into broader strategic transformation discussions.

MulteFire Technology is becoming strategically important as enterprises seek dedicated, secure, and flexible wireless infrastructure to support automation, connected operations, and digital transformation. The shift toward private wireless ecosystems is accelerating as manufacturers, logistics providers, and energy companies restructure supply chains and modernize infrastructure following global disruptions and regional industrial policies.

Compared with traditional Wi-Fi networks, MulteFire-based private wireless solutions deliver stronger mobility management, improved reliability, and up to 40% better connectivity performance in industrial environments. North America leads through advanced enterprise deployments and semiconductor investments, while Asia Pacific demonstrates faster adoption through large-scale smart manufacturing initiatives and government-backed digital infrastructure programs.

Industrial facilities are increasingly deploying MulteFire networks for autonomous robots, predictive maintenance, and real-time production monitoring. Companies are expanding partnerships with telecom providers, equipment manufacturers, and software developers to create integrated connectivity platforms. Over the next 2–3 years, enterprise adoption will focus on scalable private networks, reduced operational complexity, and improved automation efficiency. Organizations that prioritize MulteFire capabilities will gain stronger competitive positioning through enhanced operational control, resilient connectivity, and future-ready industrial ecosystems.

Private wireless network adoption is the primary growth catalyst for MulteFire Technology, driven by manufacturing automation, smart logistics, and mission-critical connectivity requirements. Industrial enterprises deploying private networks report up to 40% improvement in operational reliability and nearly 30% reduction in communication-related downtime. The U.S. manufacturing sector’s Industry 4.0 investments and Germany’s smart factory initiatives are accelerating enterprise adoption. Companies such as telecom equipment providers and semiconductor firms are expanding partnerships, investing in spectrum-sharing solutions, and developing enterprise-grade MulteFire platforms. The strategic shift is moving connectivity ownership from public operators toward industrial enterprises seeking greater control, security, and performance.

MulteFire adoption faces constraints from interoperability challenges, infrastructure readiness gaps, and integration costs across existing enterprise systems. Around 35% of industrial organizations identify network integration complexity as a major barrier, while nearly 25% cite limited technical expertise for private wireless deployment. Supply-chain dependency for advanced radio components and semiconductor modules, particularly across Asian manufacturing hubs, increases procurement risks. Companies are addressing these limitations through localized sourcing strategies, multi-vendor partnerships, and standardized network architectures. A key operational challenge remains balancing MulteFire deployment costs with measurable productivity gains, especially for small and medium-sized enterprises requiring scalable connectivity solutions.

The integration of edge computing, artificial intelligence, and autonomous systems is creating significant opportunities for MulteFire Technology adoption. AI-driven network optimization can improve resource utilization by approximately 35%, while automated industrial workflows can enhance production efficiency by more than 25% in connected facilities. Countries such as Japan and South Korea are advancing smart manufacturing ecosystems through robotics and digital infrastructure programs. Companies are investing in R&D partnerships, cloud-native network platforms, and industry-specific solutions for ports, energy facilities, and logistics centers. A unique opportunity lies in combining MulteFire with private edge networks to enable real-time decision-making without relying on centralized connectivity infrastructure.

Long-term MulteFire expansion depends on solving scalability, cybersecurity, and workforce capability challenges across complex industrial environments. Approximately 40% of enterprises consider cybersecurity management a critical factor when deploying private wireless networks, while nearly 30% face difficulties integrating new connectivity layers with legacy operational technology systems. Large industrial sites in countries such as the United States and China require highly resilient networks capable of supporting thousands of connected devices simultaneously. Companies must strengthen encryption technologies, invest in specialized workforce training, and establish ecosystem partnerships to maintain deployment consistency. The ability to secure large-scale industrial wireless environments will determine competitive differentiation and sustainable adoption.

Private Network Deployment Surge Enterprises are accelerating MulteFire-based private wireless deployments as factories, ports, and logistics facilities require dedicated connectivity with higher reliability. Industrial users report up to 40% improvement in network performance and nearly 30% reduction in operational disruptions after replacing fragmented connectivity systems. The U.S. manufacturing sector and European industrial hubs are expanding private network adoption following supply-chain resilience initiatives. Companies are responding by forming telecom partnerships, scaling enterprise solutions, and integrating MulteFire with edge computing platforms to improve automation workflows and reduce dependency on public networks.

AI-Driven Network Optimization Artificial intelligence integration is transforming MulteFire operations through automated spectrum management, predictive maintenance, and real-time network optimization. AI-enabled connectivity platforms are improving resource utilization by approximately 35% and reducing manual network management activities by nearly 25%. Manufacturing companies in Japan and South Korea are adopting intelligent wireless systems to support robotics and autonomous production lines. Technology providers are investing in cloud-native architectures, AI orchestration tools, and automated monitoring solutions to enhance scalability and operational efficiency across complex industrial environments.

Industrial IoT Connectivity Expansion MulteFire adoption is increasing across industrial IoT applications as enterprises connect more sensors, machines, and autonomous devices. Smart factories are deploying thousands of connected endpoints, with industrial wireless adoption improving workflow visibility by over 30% and reducing response delays by nearly 20%. Labor shortages and rising automation requirements are accelerating this transition, particularly in automotive and electronics manufacturing centers. Companies are restructuring digital infrastructure strategies by combining MulteFire networks with robotics, analytics platforms, and real-time monitoring systems to improve productivity.

Spectrum Innovation and Enterprise Adoption Advancements in shared spectrum models and regulatory modernization are creating new deployment opportunities for MulteFire technology. Countries including the United States are expanding enterprise access to flexible spectrum resources, enabling more than 25% faster private network deployment cycles in selected industrial environments. Supply-chain localization efforts and semiconductor ecosystem investments are further supporting adoption. Companies are developing interoperable solutions, expanding regional partnerships, and improving hardware compatibility to address enterprise requirements for secure, scalable, and cost-efficient wireless infrastructure.

Standalone MulteFire networks represent the leading type segment due to their ability to provide independent private wireless connectivity without relying on traditional cellular infrastructure. These solutions are widely adopted across manufacturing, logistics, and industrial automation environments because of improved security, deployment flexibility, and operational control. Standalone deployments account for approximately 45% of enterprise-focused MulteFire installations, while integrated solutions maintain strong demand among organizations seeking hybrid connectivity models. Companies are prioritizing standalone architectures for mission-critical operations where consistent performance and data ownership are essential.Integrated MulteFire solutions represent the fastest-growing type category as enterprises combine private wireless capabilities with existing telecom and edge ecosystems. Adoption is increasing by nearly 30% as businesses seek simplified deployment, lower infrastructure complexity, and seamless integration with cloud platforms. Legacy connectivity solutions continue serving smaller deployments, but investment priorities are shifting toward scalable architectures supporting automation, robotics, and industrial analytics. Technology providers are expanding partnerships to deliver flexible MulteFire platforms that support diverse enterprise requirements.

Industrial automation is the leading application segment for MulteFire Technology, supported by demand for reliable wireless communication across smart factories, robotics operations, and connected production systems. Manufacturing enterprises represent nearly 50% of application deployments as companies modernize facilities with automated equipment and real-time monitoring capabilities. Automotive and electronics manufacturers are increasing adoption to improve production accuracy, reduce downtime by approximately 20%, and enable faster decision-making. Companies are expanding investments in private wireless infrastructure to support advanced manufacturing workflows. Logistics and transportation applications are emerging as the fastest-growing segment as warehouses, ports, and distribution centers adopt autonomous systems and connected asset tracking. Adoption is increasing by around 35% due to rising automation requirements and supply-chain digitization efforts. Energy, utilities, and healthcare sectors are also integrating MulteFire for secure operational communication and remote monitoring. Businesses are developing industry-specific solutions, combining MulteFire with edge analytics and IoT platforms to improve efficiency and operational resilience.

Manufacturing enterprises are the dominant end-user segment in the MulteFire Technology Market due to extensive requirements for automation, machine connectivity, and real-time production monitoring. Automotive, semiconductor, and electronics manufacturers account for nearly 55% of industrial private wireless deployments because of their dependence on low-latency and secure communication networks. Large factories are investing in MulteFire solutions to improve operational efficiency by 25–30% through automated workflows and predictive maintenance capabilities. Companies are partnering with connectivity providers to develop customized industrial network solutions. Transportation, logistics, and energy organizations represent the fastest-growing end-user categories as infrastructure operators expand digital systems and autonomous operations. Adoption among these users is increasing by approximately 35% as ports, warehouses, and utility networks require reliable wireless connectivity. Small and medium enterprises are gradually adopting simplified solutions through managed service models, reducing deployment complexity. Vendors are responding through flexible pricing models, ecosystem partnerships, and sector-specific platforms designed for scalable adoption.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of36.2% between 2026 and 2033.

North America remains the leading MulteFire Technology market due to strong enterprise adoption, advanced telecom infrastructure, and early deployment of private wireless networks across manufacturing, logistics, and energy sectors. The region contributes approximately 38% of global adoption, supported by U.S. investments in industrial automation and enterprise 5G ecosystems. More than 45% of large manufacturers in the United States are evaluating private wireless solutions for operational modernization. Companies are expanding partnerships with network providers, semiconductor firms, and automation specialists to accelerate secure connectivity deployment and support smart factory transformation.

United States Market Outlook: The United States dominates regional adoption through advanced manufacturing, semiconductor expansion, and private network initiatives across industrial campuses. Over 100 large-scale enterprise facilities have adopted private wireless connectivity frameworks for automation and real-time monitoring. Strong investments in domestic technology infrastructure and flexible spectrum policies are supporting MulteFire deployment across automotive, aerospace, and logistics operations.

Europe is advancing MulteFire adoption through smart manufacturing initiatives, Industry 4.0 programs, and increasing demand for secure industrial communication networks. The region represents nearly 25% of global market adoption, with Germany, the United Kingdom, and France leading deployments across automotive, engineering, and energy sectors. European manufacturers are integrating private wireless networks to improve production flexibility, with connected industrial facilities achieving approximately 20–30% improvements in operational visibility. Sustainability-focused modernization programs and digital infrastructure investments are encouraging companies to deploy energy-efficient wireless solutions and strengthen automation capabilities.

Germany Market Outlook: Germany leads European MulteFire adoption through its advanced automotive and industrial manufacturing ecosystem. More than 50% of major industrial companies are increasing investments in factory digitalization, robotics, and connected production systems. Strong engineering capabilities, automation expertise, and Industry 4.0 initiatives position Germany as a key testing ground for enterprise wireless technologies.

Asia-Pacific represents the fastest-expanding MulteFire Technology market due to large-scale manufacturing activity, industrial automation investments, and rapid digital infrastructure development. The region contributes approximately 28% of current market adoption, driven by China, Japan, South Korea, and Taiwan. Electronics, semiconductor, and automotive manufacturers are deploying private wireless networks to support robotics and intelligent production systems, with automation investments increasing by over 30% across major industrial hubs. Companies are scaling partnerships with telecom operators and technology providers to support high-volume industrial connectivity requirements.

China Market Outlook: China is the largest Asia-Pacific contributor due to extensive manufacturing capacity, smart factory initiatives, and government-backed digital transformation programs. More than 10,000 advanced manufacturing facilities are incorporating industrial connectivity technologies, creating strong demand for secure wireless infrastructure. The country’s semiconductor ecosystem and industrial automation investments continue to strengthen MulteFire deployment opportunities.

South America is gradually adopting MulteFire technology as industries modernize operations and improve connectivity infrastructure across mining, manufacturing, logistics, and energy sectors. The region accounts for nearly 5% of global adoption, with Brazil leading enterprise deployment activity. Industrial companies are investing in private wireless networks to overcome remote connectivity challenges, particularly in mining and large-scale production environments. Adoption remains concentrated in major industrial zones, where connectivity improvements can enhance operational efficiency by approximately 20%. Companies are focusing on partnerships, localized deployment models, and managed connectivity services to reduce infrastructure barriers.

Brazil Market Outlook: Brazil represents the strongest South American market due to its mining, agriculture technology, manufacturing, and logistics industries. Large industrial operators are increasing automation investments, with private connectivity solutions supporting remote monitoring across geographically dispersed facilities. Growing digital infrastructure programs and enterprise modernization efforts are creating opportunities for MulteFire deployment.

The Middle East & Africa market is developing through infrastructure modernization, smart city initiatives, and industrial diversification programs. The region contributes around 4% of global adoption, with the United Arab Emirates and Saudi Arabia leading deployment activity across energy, logistics, and industrial sectors. Large infrastructure projects are increasing demand for secure wireless communication, while digital transformation programs are accelerating enterprise adoption. Companies are investing in private network partnerships and automation solutions to improve operational control, with connected infrastructure projects reporting efficiency improvements of approximately 25%.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional MulteFire adoption through smart infrastructure investments, logistics modernization, and technology-focused industrial development. More than 100 smart infrastructure projects are incorporating advanced connectivity solutions across transportation and commercial facilities. Strong investment in digital transformation and enterprise automation positions the UAE as a strategic market for private wireless technologies.

The MulteFire Technology market is contested by global telecom leaders, private wireless specialists, and industrial connectivity innovators. Nokia, Ericsson, Huawei, Cisco, and semiconductor ecosystem providers compete through private network platforms, industrial integration, and device compatibility. The top five players collectively control approximately 60% of enterprise private wireless influence, creating a moderately concentrated structure. Competition is centered on technology capability, deployment speed, customization, and ecosystem partnerships, with advanced vendors achieving 25–40% efficiency improvements through automation and edge integration. Leaders are expanding through industrial alliances, R&D investments, and vertical solutions, while regional suppliers compete through cost flexibility. The competitive shift is moving toward integrated private wireless ecosystems, creating entry barriers around patents, spectrum expertise, industrial partnerships, and network reliability. Winning requires scalable platforms, strong enterprise relationships, and continuous innovation.

Ericsson

Huawei

Cisco

Qualcomm

Intel

Samsung Electronics

ZTE

Mavenir

CommScope

Airspan Networks

Druid Software

MulteFire technology is evolving through private wireless networking, edge computing, artificial intelligence-based orchestration, and industrial IoT integration. Advanced MulteFire deployments improve network reliability by approximately 30% compared with traditional enterprise Wi-Fi environments while supporting low-latency industrial applications. AI-enabled network management is reducing manual configuration requirements by nearly 25%, allowing manufacturers to optimize connected operations, robotics workflows, and predictive maintenance systems.

The transition from legacy Wi-Fi-based industrial connectivity to MulteFire-powered private networks is creating measurable performance advantages, including up to 40% improvement in coverage consistency and mobility management. Edge computing integration enables faster decision-making by processing operational data closer to production sites, benefiting automotive, semiconductor, logistics, and energy companies requiring real-time control.

Between 2026 and 2028, technology adoption will increasingly focus on AI-driven automation, cloud-native private networks, and seamless integration with 5G infrastructure. Companies investing in interoperable platforms, advanced security frameworks, and industrial-specific solutions will gain competitive advantages. The strongest beneficiaries will be telecom equipment providers and industrial technology firms capable of combining connectivity, analytics, and automation into unified enterprise ecosystems.

March 2025 — Nokia launched the Nokia DAC Marketplace to expand its industrial private wireless ecosystem by adding third-party applications, devices, and services. The platform introduced solutions from seven new ecosystem partners, improving enterprise access to deployable Industry 4.0 solutions. Source: www.nokia.com

May 2025 — Nokia partnered with A.P. Moller - Maersk to deploy private wireless connectivity across 450 vessels for real-time cargo tracking. The deployment strengthens maritime IoT operations by improving supply-chain visibility, asset monitoring, and operational efficiency.

March 2025 — Ericsson collaborated with OneLayer to introduce zero-trust access solutions for mission-critical private networks. The solution automates device onboarding at scale and strengthens security management for industrial private cellular deployments.

September 2025 — Nokia released its Industrial Digitalization Report highlighting private wireless and edge adoption trends. The study showed 87% of enterprises achieved ROI within one year, while 94% of industrial users deployed edge solutions supporting AI-driven applications.

The MulteFire Technology Market Report covers comprehensive analysis across technology types, applications, end-user industries, regional markets, competitive positioning, and emerging deployment opportunities. The study evaluates standalone and integrated MulteFire solutions across industrial automation, logistics, energy, healthcare, and enterprise connectivity applications. It examines adoption patterns across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting infrastructure maturity and industrial digitalization trends.

The report provides strategic insights into technology innovation, private wireless ecosystem development, company positioning, and future deployment opportunities between 2026 and 2033. Coverage includes approximately 10+ major industry participants, evolving connectivity architectures, automation integration, and enterprise transformation initiatives. The analysis supports investment planning, market entry strategies, partnership decisions, and competitive positioning by identifying high-potential segments and operational shifts shaping the global MulteFire ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 565.0 Million |

| Market Revenue (2033) | USD 6,159.8 Million |

| CAGR (2026–2033) | 34.8% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Nokia; Ericsson; Huawei; Cisco; Qualcomm; Intel; Samsung Electronics; ZTE; Mavenir; CommScope; Airspan Networks; Druid Software |

| Customization & Pricing | Available on Request (10% Customization Free) |