Reports

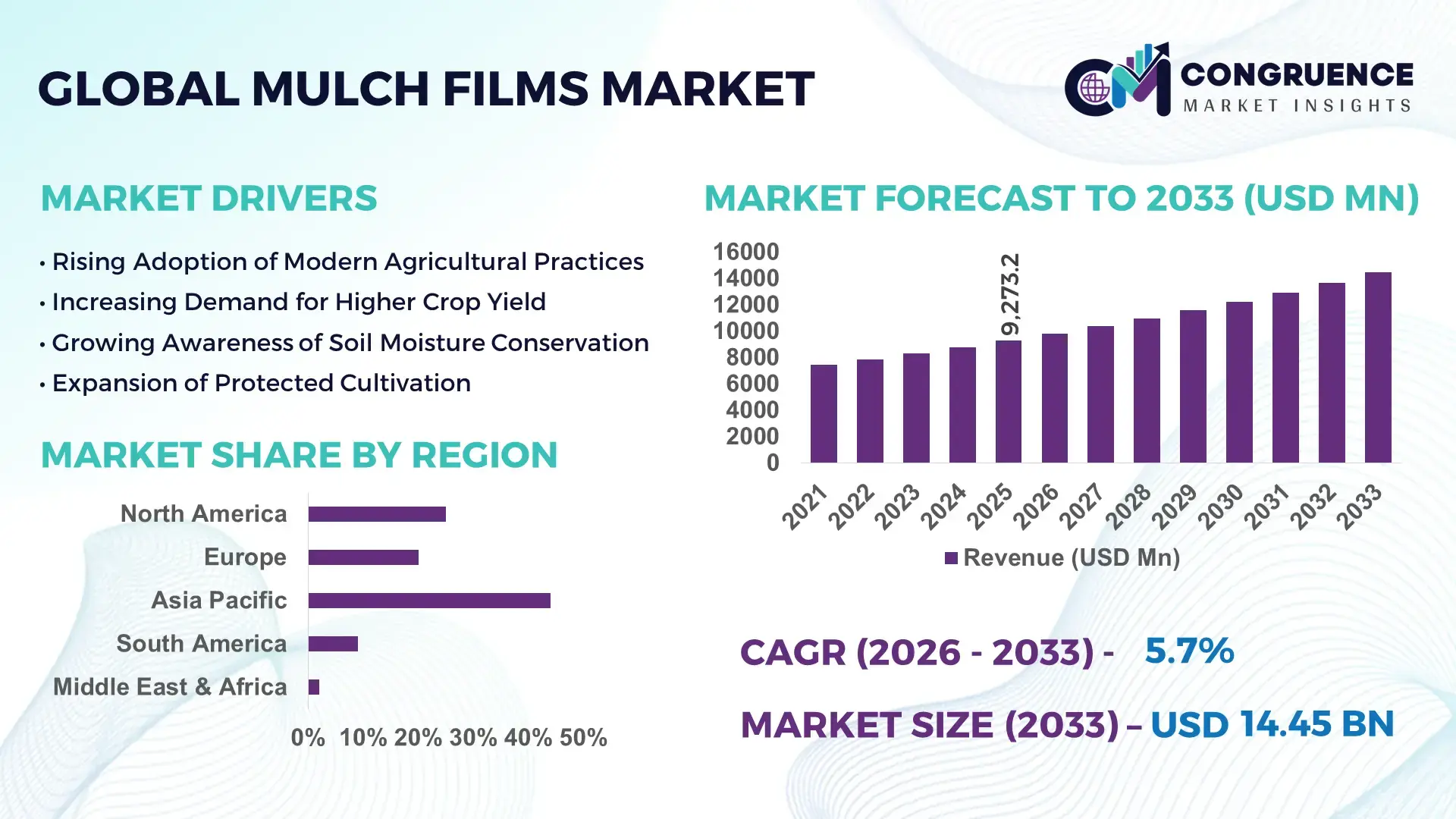

The Global Mulch Films Market was valued at USD 9273.16 Million in 2025 and is anticipated to reach a value of USD 14448.67 Million by 2033 expanding at a CAGR of 5.7% between 2026 and 2033. The growth is primarily driven by increasing demand for advanced agricultural productivity solutions and water conservation practices.

China remains the dominant country in the mulch films market, supported by extensive agricultural land coverage exceeding 120 million hectares and widespread adoption of plasticulture techniques across key crop segments such as vegetables, fruits, and grains. The country produces over 1.5 million tons of agricultural films annually, with polyethylene mulch films accounting for a significant portion. Government-backed initiatives promoting water-efficient irrigation and soil temperature regulation have accelerated adoption rates, with usage intensity surpassing 70% in high-value crop farming regions. Additionally, continuous investments in biodegradable mulch film technologies and advanced extrusion processes have enhanced product durability and environmental compatibility, strengthening production capacity and application diversity across both open-field and greenhouse farming systems.

Market Size & Growth: Valued at USD 9273.16 Million in 2025, projected to reach USD 14448.67 Million by 2033, growing at 5.7% CAGR due to increasing precision agriculture adoption and soil moisture retention needs.

Top Growth Drivers: 35% increase in water-use efficiency demand, 28% rise in protected cultivation practices, 22% improvement in crop yield efficiency.

Short-Term Forecast: By 2028, mulch films are expected to reduce irrigation water usage by up to 30% and improve crop output efficiency by 18%.

Emerging Technologies: Biodegradable polymer films, UV-stabilized multilayer films, and nano-enhanced agricultural films for improved durability.

Regional Leaders: Asia-Pacific projected to reach USD 6200 Million by 2033 with high agricultural intensity; North America at USD 3100 Million driven by precision farming; Europe at USD 2800 Million with strong biodegradable adoption trends.

Consumer/End-User Trends: High adoption among vegetable growers and horticulture farmers, with over 65% usage in greenhouse cultivation systems.

Pilot or Case Example: In 2024, an agricultural initiative in India improved soil moisture retention by 27% using advanced mulch film deployment.

Competitive Landscape: Market leader holds approximately 18% share, followed by key players including Berry Global, BASF, RKW Group, Armando Alvarez Group, and Novamont.

Regulatory & ESG Impact: Increasing mandates for biodegradable plastics and recycling compliance, with targets of 40% reduction in plastic waste by 2030.

Investment & Funding Patterns: Over USD 1.2 billion invested globally in sustainable agricultural films and polymer innovation projects.

Innovation & Future Outlook: Integration of smart films with temperature control and moisture sensors is shaping next-generation agricultural practices.

The mulch films market continues to evolve across key agricultural sectors including horticulture, floriculture, and commercial crop production, with horticulture contributing nearly 45% of total demand. Recent innovations such as biodegradable starch-based films and photodegradable polymers are transforming product portfolios, addressing environmental concerns while maintaining performance efficiency. Regulatory frameworks in Europe and parts of Asia are accelerating the transition toward sustainable materials, while economic drivers such as rising food demand and declining arable land are pushing adoption rates. Regionally, Asia-Pacific leads consumption due to intensive farming practices, while Europe is witnessing strong growth in eco-friendly alternatives. Future trends indicate increased integration of smart agriculture technologies and customized mulch film solutions tailored for specific crop and soil conditions.

The mulch films market holds strong strategic relevance within modern agriculture due to its direct impact on productivity optimization, resource conservation, and climate-resilient farming. As global agricultural systems shift toward efficiency-driven models, mulch films are increasingly integrated into precision farming strategies, enabling controlled soil temperature, reduced evaporation, and enhanced crop quality. Advanced biodegradable mulch films deliver nearly 25% improvement in soil health preservation compared to conventional polyethylene films, reflecting a significant technological advancement over older standards.

From a regional standpoint, Asia-Pacific dominates in volume due to large-scale agricultural operations, while Europe leads in adoption with over 48% of farms transitioning toward biodegradable mulch film solutions. This divergence highlights both scale and sustainability as parallel drivers shaping market pathways. In the short term, by 2028, smart agriculture technologies integrated with mulch films are expected to improve irrigation efficiency by approximately 20% through sensor-based soil monitoring systems.

Sustainability commitments are also reshaping the market landscape, with firms targeting up to 50% reduction in non-recyclable plastic usage by 2030. In 2024, an agricultural program in Spain demonstrated a 30% reduction in plastic waste through the deployment of fully compostable mulch films combined with precision irrigation systems. These advancements underscore the increasing alignment between regulatory frameworks and technological innovation. Looking ahead, the mulch films market is positioned as a critical pillar supporting sustainable agriculture, enabling compliance with environmental standards while enhancing resilience against climate variability and resource constraints.

The rising need for efficient agricultural practices is a primary driver of the mulch films market, particularly as global food demand continues to increase. Mulch films help improve crop yield by up to 20% by maintaining optimal soil temperature and moisture levels, making them essential in modern farming systems. In regions facing water scarcity, mulch films reduce evaporation losses by nearly 30%, enabling more sustainable water management. Additionally, the expansion of protected cultivation, including greenhouse and tunnel farming, has increased mulch film usage by over 40% in certain regions. Governments are also promoting advanced farming techniques through subsidies and incentives, further boosting adoption rates. The integration of mulch films with drip irrigation systems enhances nutrient delivery efficiency, contributing to higher productivity and reduced input costs.

Environmental concerns related to plastic waste accumulation pose a significant restraint for the mulch films market. Conventional polyethylene mulch films are difficult to recycle and often lead to soil contamination when not properly managed. Studies indicate that less than 15% of agricultural plastic waste is effectively recycled, creating long-term environmental challenges. Residual plastic fragments can negatively impact soil health and microbial activity, reducing agricultural productivity over time. Regulatory bodies in regions such as Europe have introduced strict guidelines on plastic usage, increasing compliance costs for manufacturers. Additionally, the transition to biodegradable alternatives involves higher production costs, limiting adoption among cost-sensitive farmers. These factors collectively create barriers to widespread market expansion despite growing demand.

The development of biodegradable mulch films presents a significant growth opportunity in the market, driven by increasing environmental regulations and sustainability goals. Biodegradable films can decompose naturally within 6 to 12 months, eliminating the need for removal and disposal, which reduces labor costs by up to 25%. Innovations in bio-based polymers such as polylactic acid (PLA) and starch blends are enhancing film durability and performance, making them suitable for a wide range of crops. The adoption of these eco-friendly solutions is particularly strong in Europe, where over 35% of farmers are transitioning to sustainable alternatives. Additionally, government incentives and funding programs aimed at reducing agricultural plastic waste are accelerating the commercialization of biodegradable mulch films, creating new revenue streams for manufacturers and suppliers.

Cost and performance-related challenges continue to impact the widespread adoption of advanced mulch films. Biodegradable alternatives often cost 20% to 50% more than conventional polyethylene films, making them less accessible for small and medium-scale farmers. Performance variability under different climatic conditions also poses a concern, as some biodegradable films may degrade prematurely in high-temperature or high-moisture environments. Additionally, limited awareness and technical knowledge among farmers regarding proper usage and disposal methods hinder effective implementation. Supply chain constraints and fluctuations in raw material prices further contribute to market instability. These challenges necessitate ongoing research and development efforts to improve cost efficiency and product reliability while ensuring compliance with environmental standards.

• Increasing Adoption of Biodegradable Mulch Films (Up to 35% Penetration Growth):

The shift toward biodegradable mulch films is accelerating, with adoption rates increasing by nearly 35% across environmentally regulated markets. These films decompose within 6–12 months, reducing plastic residue in soil by over 80% compared to conventional polyethylene films. In Europe, more than 40% of horticulture farms have transitioned to biodegradable variants, driven by strict environmental policies and sustainability targets. Additionally, advancements in starch-based and PLA-based polymers have improved tensile strength by 18%, making these films viable for diverse climatic conditions and crop cycles.

• Expansion of Precision Agriculture Integration (20–25% Efficiency Gains):

Mulch films are increasingly being integrated with precision agriculture technologies, resulting in measurable improvements in farm productivity. Sensor-based irrigation systems combined with mulch films have demonstrated up to 25% water savings and 20% enhancement in crop yield consistency. Smart mulch films embedded with UV stabilizers and thermal regulators are improving soil temperature control by 15%, particularly in greenhouse environments. Adoption of such integrated solutions has risen by 30% among commercial farms, especially in North America and Asia-Pacific.

• Rising Demand in Protected Cultivation (Over 45% Usage in Greenhouses):

The use of mulch films in protected cultivation systems such as greenhouses and polyhouses has expanded significantly, accounting for over 45% of total application in high-value crop production. These films help reduce weed growth by approximately 90% and enhance nutrient retention efficiency by 22%. Countries with intensive horticulture practices have reported a 28% increase in yield quality due to consistent soil moisture and temperature regulation. This trend is particularly strong in regions focusing on export-oriented fruit and vegetable production.

• Growth in Multi-Layer and UV-Stabilized Films (Performance Boost of 30%):

Technological advancements in multi-layer and UV-stabilized mulch films are transforming product performance standards. Multi-layer films offer up to 30% higher durability and resistance to environmental stress compared to single-layer alternatives. UV-stabilized films extend functional lifespan by 25%, reducing replacement frequency and operational costs. Adoption of these advanced films has increased by 32% among large-scale farms, driven by the need for long-term cost efficiency and improved crop protection under varying climatic conditions.

The mulch films market segmentation is structured across product types, applications, and end-user industries, each contributing distinctively to market dynamics. Polyethylene-based mulch films continue to dominate due to their widespread availability and cost efficiency, while biodegradable films are gaining traction due to regulatory pressures and sustainability goals. Application-wise, horticulture and vegetable cultivation represent the largest segments, supported by high adoption rates in intensive farming systems. End-user segmentation highlights commercial agriculture as the primary consumer, followed by greenhouse operators and research institutions. Regional variations are evident, with Asia-Pacific leading in volume consumption due to extensive farmland usage, while Europe shows higher penetration of eco-friendly alternatives. The segmentation landscape reflects a balance between cost-driven adoption and sustainability-led innovation, influencing product development strategies and long-term market positioning.

The mulch films market is segmented into polyethylene (PE) mulch films, biodegradable mulch films, and other specialty films including photodegradable and paper-based variants. Polyethylene mulch films currently account for approximately 58% of total adoption due to their cost-effectiveness, high tensile strength, and adaptability across multiple crop types. In comparison, biodegradable mulch films hold around 28% adoption, while other specialty films contribute a combined 14%. However, biodegradable mulch films are the fastest-growing segment, expanding at an estimated CAGR of 7.2%, driven by increasing environmental regulations and rising demand for sustainable farming inputs. Polyethylene films remain dominant because they provide consistent performance in weed suppression and moisture retention, improving crop yield by up to 20%. Meanwhile, biodegradable films are gaining traction due to their ability to reduce soil contamination by over 75%, eliminating the need for post-harvest removal. Specialty films, including photodegradable variants, are used in niche applications where controlled degradation is required.

Application-wise, the mulch films market is categorized into horticulture, agriculture (row crops), and floriculture. Horticulture leads the segment with approximately 46% adoption, driven by high-value crop production such as fruits and vegetables that require precise soil temperature and moisture control. Agriculture applications account for around 34%, while floriculture contributes the remaining 20%. However, greenhouse-based horticulture applications are expanding the fastest, with an estimated CAGR of 6.8%, supported by increasing demand for controlled-environment farming. Horticulture dominates due to its intensive use of mulch films for enhancing crop quality and reducing water consumption by up to 30%. Agricultural row crops are gradually adopting mulch films to improve yield stability, especially in water-scarce regions. Floriculture benefits from improved soil aeration and weed control, enhancing flower quality and shelf life.

End-user segmentation in the mulch films market includes commercial farmers, greenhouse operators, and agricultural research institutions. Commercial farmers dominate with approximately 62% of total usage, reflecting widespread adoption in large-scale crop production. Greenhouse operators account for around 26%, while research institutions and specialty growers contribute a combined 12%. However, greenhouse operators represent the fastest-growing segment, expanding at an estimated CAGR of 7.5%, driven by increasing investment in protected cultivation systems. Commercial farmers rely heavily on mulch films to enhance productivity and reduce input costs, achieving up to 20% yield improvements and 25% water savings. Greenhouse operators benefit from controlled environmental conditions, where mulch films improve crop consistency and reduce pest infestation rates by nearly 18%. Research institutions play a critical role in testing advanced biodegradable and smart film technologies.

Region Asia-Pacific accounted for the largest market share at 48% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2026 and 2033.

Asia-Pacific’s dominance is supported by extensive agricultural land exceeding 300 million hectares across key countries such as China and India, where mulch film usage intensity surpasses 60% in vegetable cultivation. North America follows with approximately 21% share, driven by high adoption in precision agriculture and greenhouse farming covering over 500,000 hectares. Europe holds nearly 19% share, with more than 40% of farms transitioning toward biodegradable mulch solutions. South America contributes around 7%, supported by expanding horticulture in Brazil and Argentina, while the Middle East & Africa accounts for roughly 5%, driven by water-efficient farming practices. Regional demand is further shaped by irrigation efficiency improvements of up to 30% and crop yield enhancements exceeding 20%, highlighting the growing importance of mulch films in modern agriculture systems.

North America accounts for approximately 21% of the mulch films market, with strong demand driven by commercial agriculture and greenhouse farming. The United States and Canada lead regional consumption, supported by large-scale vegetable and fruit production systems. Over 65% of greenhouse operations utilize mulch films to improve crop consistency and reduce weed growth by up to 85%. Regulatory frameworks promoting sustainable farming practices, including biodegradable plastic mandates in select states, are influencing product adoption. Technological advancements such as UV-stabilized films and multilayer extrusion technologies have improved film durability by nearly 25%. Companies like Berry Global are actively investing in sustainable film solutions, including recyclable and biodegradable product lines. Consumer behavior in this region reflects a strong preference for efficiency-driven solutions, with farmers prioritizing products that reduce water usage by up to 30% and improve yield reliability.

Europe represents nearly 19% of the mulch films market, with key countries including Germany, France, and Italy leading adoption. Regulatory pressure from environmental agencies has resulted in over 45% of farms adopting biodegradable mulch films. Initiatives targeting a 50% reduction in agricultural plastic waste by 2030 are accelerating market transformation. Advanced technologies such as compostable polymer blends and photodegradable films are gaining traction, improving soil health outcomes by over 20%. Companies like Novamont are pioneering bio-based mulch film solutions, enhancing product sustainability and performance. Consumer behavior across the region is heavily influenced by environmental compliance, with farmers increasingly selecting eco-friendly materials despite higher initial costs. Additionally, over 35% of agricultural cooperatives are integrating sustainable mulch films into standard farming practices.

Asia-Pacific dominates the mulch films market in terms of volume, accounting for nearly 48% of global consumption. China, India, and Japan are the top consuming countries, with China alone producing over 1.5 million tons of agricultural films annually. Rapid expansion of greenhouse farming and intensive horticulture has increased mulch film usage by over 40% in the region. Infrastructure development in irrigation systems and government subsidies for modern farming techniques are further supporting market growth. Local manufacturers are investing in advanced extrusion technologies, improving film strength and lifespan by 20%. For example, Chinese producers are scaling biodegradable film production to meet rising environmental standards. Consumer behavior reflects cost sensitivity, with over 70% of farmers prioritizing affordable and durable polyethylene films while gradually transitioning to sustainable alternatives.

South America accounts for approximately 7% of the mulch films market, with Brazil and Argentina serving as key contributors. The region’s agricultural expansion, particularly in fruit and vegetable cultivation, has increased mulch film usage by nearly 25% over recent years. Infrastructure improvements in irrigation and farm mechanization are enhancing adoption rates, with mulch films contributing to water savings of up to 28%. Government incentives supporting sustainable farming practices are encouraging the use of biodegradable films. Local players are focusing on cost-effective solutions tailored to regional crop conditions. Consumer behavior in South America is closely tied to productivity gains, with farmers prioritizing solutions that improve crop yield by over 18% while minimizing operational costs.

The Middle East & Africa region holds approximately 5% of the mulch films market, with demand driven by water scarcity and the need for efficient irrigation practices. Countries such as the UAE and South Africa are leading adoption, with greenhouse farming expanding by over 20% in arid regions. Technological modernization, including drip irrigation combined with mulch films, has improved water-use efficiency by up to 35%. Government initiatives promoting sustainable agriculture and food security are supporting market growth. Local suppliers are introducing UV-resistant films to withstand extreme climatic conditions, increasing product lifespan by 22%. Consumer behavior in this region emphasizes resource efficiency, with farmers adopting mulch films primarily to reduce water consumption and improve crop survival rates in harsh environments.

China – 34% market share in the Mulch Films market, driven by large-scale agricultural production and high adoption of plasticulture techniques.

India – 18% market share in the Mulch Films market, supported by expanding horticulture sector and government-backed irrigation efficiency programs.

The mulch films market is moderately fragmented, with over 60 active global and regional players competing across product innovation, pricing strategies, and sustainability initiatives. The top five companies collectively account for approximately 42% of the market, indicating a competitive yet consolidated structure among leading players. Key participants are focusing on expanding biodegradable product portfolios, with investments in research and development increasing by nearly 20% over recent years. Strategic partnerships and mergers are becoming more common, with over 15 notable collaborations recorded in the past two years aimed at enhancing production capacity and geographic reach. Product differentiation is driven by advancements in multilayer film technology, UV stabilization, and compostable materials, improving performance metrics such as durability by up to 30% and degradation efficiency by over 70%. Additionally, companies are investing in automation and digital manufacturing processes to reduce production costs by approximately 15%. The competitive landscape is further shaped by regional players offering cost-effective solutions, particularly in Asia-Pacific, where price sensitivity remains high. Innovation, sustainability compliance, and supply chain optimization continue to define competitive positioning in this evolving market.

Berry Global Inc.

BASF SE

RKW Group

Armando Alvarez Group

Novamont S.p.A.

Kuraray Co., Ltd.

AEP Industries Inc.

Trioplast Industrier AB

Plastika Kritis S.A.

Ab Rani Plast Oy

Coveris Holdings S.A.

Novolex Holdings LLC

Technological advancements in the mulch films market are increasingly centered on material innovation, durability enhancement, and sustainability optimization. Multi-layer co-extrusion technology has emerged as a critical development, enabling manufacturers to produce films with up to 5–7 layers, significantly improving mechanical strength by nearly 30% and extending product lifespan under extreme climatic conditions. These advanced films provide enhanced resistance to UV radiation, improving durability by approximately 25% compared to conventional single-layer films.

Biodegradable mulch films are witnessing rapid technological refinement, particularly with the use of bio-based polymers such as polylactic acid (PLA), polyhydroxyalkanoates (PHA), and starch blends. These materials can achieve degradation rates of over 90% within 6–12 months under optimal soil conditions, reducing environmental impact and eliminating post-harvest disposal costs. Additionally, nanotechnology integration is enhancing film performance, with nano-additives improving thermal insulation efficiency by up to 18% and increasing tensile strength by 20%.

Smart mulch films represent another emerging trend, incorporating embedded sensors and responsive materials that regulate soil temperature and moisture levels in real time. These innovations can improve irrigation efficiency by nearly 20% and reduce water consumption by up to 25%. Infrared (IR) reflective films are also gaining traction, helping maintain soil temperature stability and improving crop yield consistency by approximately 15%.

Digital manufacturing technologies, including automated extrusion lines and precision thickness control systems, have improved production efficiency by over 22%, ensuring uniform film quality. Furthermore, recycling technologies are advancing, enabling recovery rates of agricultural plastics to exceed 35% in certain regions. Collectively, these technological advancements are transforming mulch films into high-performance, sustainable agricultural inputs aligned with modern precision farming requirements.

• In March 2025, BASF expanded its biodegradable plastics portfolio by enhancing the performance of ecovio® films used in agricultural mulch applications. The updated formulation improves soil biodegradation efficiency and mechanical strength, supporting sustainable farming practices and compliance with evolving environmental standards. Source: www.basf.com

• In September 2024, Novamont introduced an upgraded Mater-Bi® mulch film range designed for improved biodegradability and soil integration. The new products demonstrated over 90% degradation under field conditions and were adopted across several European agricultural projects focused on reducing plastic waste. Source: www.novamont.com

• In July 2024, Berry Global announced advancements in its sustainable agricultural film solutions, including the development of recyclable mulch films with enhanced UV resistance. These films extend usage cycles by up to 25% and support circular economy initiatives within commercial farming operations. Source: www.berryglobal.com

• In February 2025, RKW Group launched a new series of high-performance mulch films incorporating multi-layer extrusion technology. The innovation improves durability and crop protection efficiency, while also reducing material usage by approximately 15%, aligning with sustainability and cost-efficiency goals. Source: www.rkw-group.com

The mulch films market report provides a comprehensive analysis of the industry, covering a wide spectrum of segments, technologies, and geographic regions to support informed decision-making. The scope includes detailed segmentation by product type, encompassing polyethylene, biodegradable, and specialty mulch films, collectively representing over 95% of market utilization across agricultural applications. Application coverage spans horticulture, row crop farming, and floriculture, with horticulture alone accounting for nearly 45% of total usage due to its reliance on controlled soil conditions.

Geographically, the report analyzes five key regions, including Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, representing 100% of global consumption patterns. Asia-Pacific leads with close to half of total demand, while Europe is distinguished by over 40% adoption of biodegradable alternatives. The report further examines country-level insights across major agricultural economies such as China, India, the United States, Germany, and Brazil.

Technological scope includes advanced manufacturing processes such as multi-layer co-extrusion, UV stabilization, and smart film integration, which collectively enhance product performance by up to 30%. Emerging segments such as nanotechnology-enhanced films and compostable materials are also covered, reflecting ongoing innovation trends. Additionally, the report evaluates end-user industries including commercial farming, greenhouse cultivation, and research institutions, which together account for more than 85% of total demand. The analysis extends to regulatory frameworks, sustainability initiatives, and evolving environmental standards shaping product development and adoption. By integrating quantitative data with industry-specific insights, the report offers a structured overview of market dynamics, competitive positioning, and technological evolution within the mulch films industry.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

5.7% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Berry Global Inc., BASF SE, RKW Group, Armando Alvarez Group, Novamont S.p.A., Kuraray Co., Ltd., AEP Industries Inc., Trioplast Industrier AB, Plastika Kritis S.A., Ab Rani Plast Oy, Coveris Holdings S.A., Novolex Holdings LLC |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |