Reports

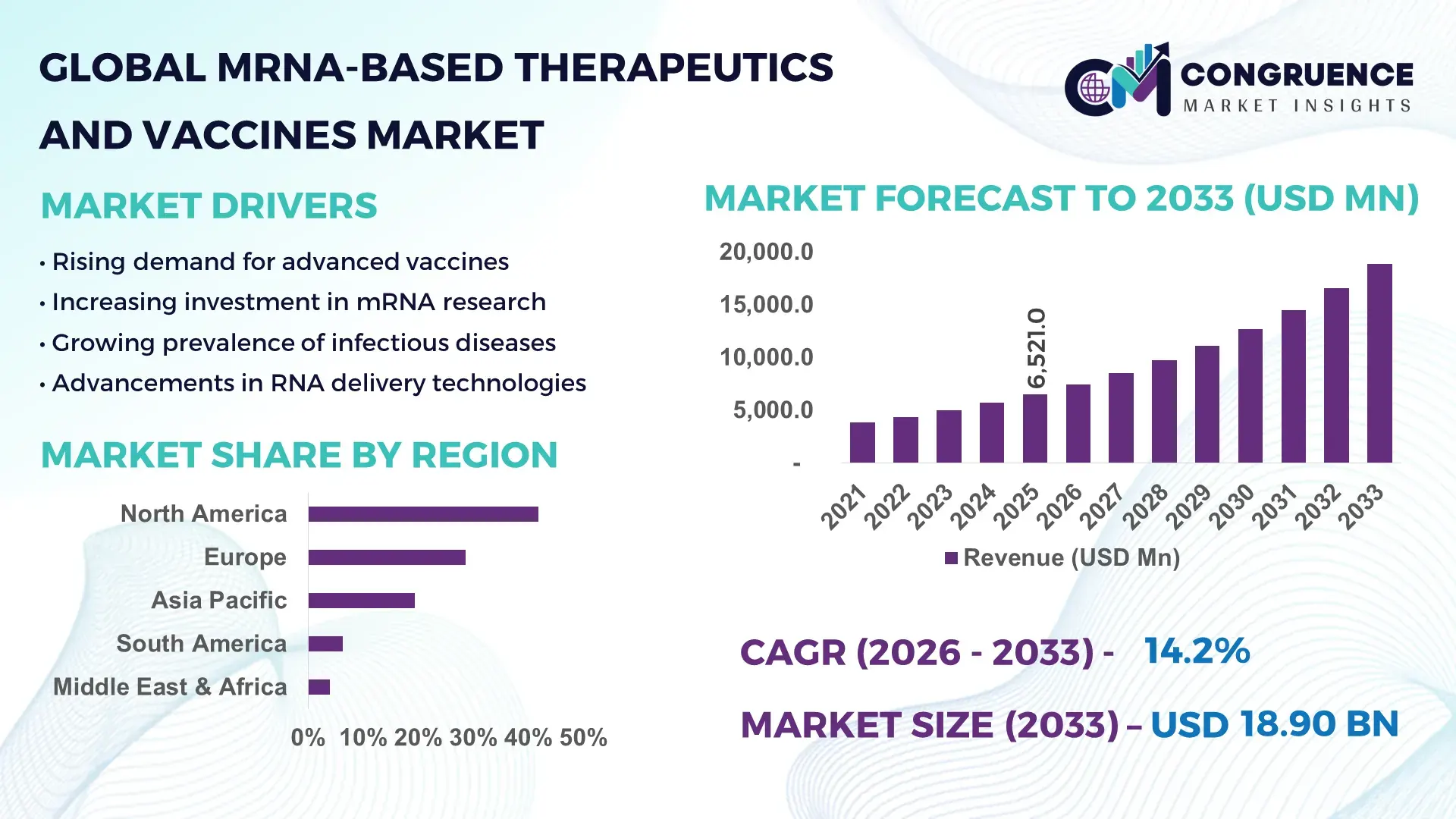

The Global MRNA-Based Therapeutics and Vaccines Market was valued at USD 6,521.0 Million in 2025 and is anticipated to reach a value of USD 18,904.1 Million by 2033 expanding at a CAGR of 14.23% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is driven by expanding clinical applications of mRNA platforms beyond infectious diseases into oncology, rare genetic disorders, and personalized medicine.

The United States leads the global mRNA-based therapeutics and vaccines ecosystem with robust production infrastructure and sustained investment intensity. The country accounts for over 45% of global mRNA clinical trials, supported by more than 120+ active pipeline candidatesacross oncology and infectious diseases. Manufacturing capacity exceeds 1.5 billion mRNA doses annually, driven by large-scale biopharma facilities. Additionally, over 60% of biotech funding in RNA therapeuticsis concentrated in the U.S., accelerating innovation in lipid nanoparticle delivery systems and AI-driven mRNA design platforms. Hospital adoption rates exceed 70% in advanced healthcare systems, particularly in oncology immunotherapy trials, reinforcing strong end-user engagement and clinical integration. The mRNA-Based Therapeutics and Vaccines Market is increasingly diversified across oncology (~38%), infectious diseases (~42%), and rare genetic disorders (~12%), with remaining applications accounting for ~8%. Innovations in self-amplifying mRNA and thermostable formulations are improving delivery efficiency by over 25%, while regulatory acceleration frameworks and global immunization strategies continue to support adoption across developed and emerging regions.

Market Size & Growth: USD 6,521.0 Million in 2025, projected to reach USD 18,904.1 Million by 2033 at a CAGR of 14.23%, driven by expanding oncology and personalized vaccine applications.

Top Growth Drivers: Clinical pipeline expansion (+45%), delivery efficiency improvement (+30%), healthcare adoption growth (+40%).

Short-Term Forecast: By 2028, mRNA delivery systems expected to improve therapeutic targeting accuracy by 28%.

Emerging Technologies: Lipid nanoparticle engineering, self-amplifying mRNA, AI-based sequence optimization.

Regional Leaders: North America (~USD 7,800 Million by 2033), Europe (~USD 5,600 Million), Asia-Pacific (~USD 4,900 Million), driven by clinical expansion and manufacturing growth.

Consumer/End-User Trends: Over 65% of hospitals in developed markets are integrating mRNA-based treatments into oncology and infectious disease protocols.

Pilot or Case Example: In 2025, mRNA oncology trials demonstrated a 32% increase in immune response biomarkers in phase II studies.

Competitive Landscape: Market leader holds ~24% share, followed by 4–5 major global biotech firms driving innovation pipelines.

Regulatory & ESG Impact: Over 50% of new approvals utilize accelerated pathways; sustainability initiatives target 20% reduction in cold-chain emissions by 2030.

Investment & Funding Patterns: Global investments exceeded USD 18 billion across mRNA R&D and manufacturing expansion between 2023–2025.

Innovation & Future Outlook: Personalized vaccines, AI-driven mRNA design, and modular manufacturing will reshape therapeutic delivery ecosystems.

The market is witnessing strong integration across oncology, infectious disease management, and genetic therapy segments, with regulatory support and innovation in delivery technologies accelerating commercialization and global adoption.

The MRNA-Based Therapeutics and Vaccines Market holds strategic importance as a transformative pillar in modern biopharmaceutical innovation. Its modular and programmable nature enables rapid development cycles, reducing drug discovery timelines by up to 40% compared to conventional vaccine platformssuch as attenuated or protein-based systems. Advanced lipid nanoparticle systems deliver 30% higher intracellular delivery efficiency compared to traditional viral vector approaches, improving therapeutic outcomes across oncology and infectious disease applications.

North America dominates in volume due to extensive clinical trial infrastructure and funding capacity, while Europe leads in adoption with over 55% of pharmaceutical firms integrating mRNA technologies into pipeline strategies. Asia-Pacific is rapidly scaling, supported by increasing healthcare infrastructure and localized production capabilities. By 2028, AI-driven mRNA design platforms are expected to reduce candidate optimization timelines by 25%, enhancing clinical success rates.

From an ESG perspective, firms are committing to reducing environmental impact, with targets including 20% reduction in cold-chain energy consumption by 2030through development of thermostable mRNA formulations. In 2025, a major biopharmaceutical manufacturer achieved a 22% reduction in production waste using continuous mRNA manufacturing processes.

Looking ahead, the market’s future pathways will focus on precision medicine, scalable manufacturing, and digital integration. These developments position the MRNA-Based Therapeutics and Vaccines Market as a cornerstone of resilient, compliant, and sustainable healthcare transformation.

The MRNA-Based Therapeutics and Vaccines Market is shaped by rapid advancements in biotechnology, increasing demand for next-generation therapeutics, and evolving healthcare infrastructure. Expansion of clinical pipelines, particularly in oncology and rare diseases, is driving innovation across delivery technologies and manufacturing systems. Increased collaborations between biotech firms and pharmaceutical companies are accelerating product development cycles. Additionally, governments worldwide are investing heavily in pandemic preparedness and biotechnology capabilities, further strengthening the market. However, regulatory complexities, high production costs, and logistical constraints continue to influence market dynamics. The integration of AI and automation in mRNA design and production is improving efficiency, while global demand for personalized medicine is creating new opportunities for market expansion.

The rising demand for personalized medicine is a key driver of the mRNA-based therapeutics and vaccines market. mRNA platforms allow for rapid customization of treatments based on individual genetic profiles, particularly in oncology where tumor-specific antigens can be targeted. Over 35% of oncology clinical trials now incorporate personalized approaches, with mRNA-based solutions showing improved immune response rates. The flexibility of mRNA technology enables faster development cycles, often reducing time-to-clinic by several months compared to traditional therapies. Additionally, increasing patient awareness and demand for targeted treatments are encouraging healthcare providers to adopt these advanced therapies, further boosting market growth.

High production costs and stringent cold-chain requirements significantly restrain market growth. mRNA vaccines and therapeutics require specialized manufacturing environments and ultra-low temperature storage, often below -70°C, increasing logistical complexity. Establishing compliant production facilities involves substantial capital investment, often exceeding hundreds of millions of dollars. Additionally, maintaining cold-chain infrastructure across emerging markets is challenging, limiting accessibility and distribution. These factors increase overall operational costs and hinder widespread adoption, particularly in low- and middle-income regions where infrastructure constraints remain significant.

Oncology represents a significant growth opportunity for the mRNA-based therapeutics market. Currently, oncology accounts for approximately 38% of the total pipeline, with increasing focus on personalized cancer vaccines and immunotherapies. mRNA technology enables precise targeting of tumor antigens, enhancing treatment efficacy and reducing side effects. Advances in combination therapies, where mRNA vaccines are used alongside checkpoint inhibitors, are showing promising clinical outcomes. Additionally, increasing investments in cancer research and rising global cancer incidence are driving demand for innovative treatment solutions, creating substantial opportunities for market expansion.

Regulatory complexities and lengthy approval timelines pose significant challenges for the market. mRNA-based products must meet stringent safety and efficacy standards, requiring extensive clinical trials and regulatory approvals. Variations in regulatory frameworks across regions further complicate global commercialization efforts. Additionally, the relatively new nature of mRNA technology means that long-term safety data is still being collected, leading to cautious regulatory approaches. These factors can delay product launches and increase development costs, impacting overall market growth.

Expansion of Oncology Applications: Oncology-focused mRNA therapies now account for over 38% of total pipeline activity, with more than 120 active clinical programstargeting various cancers. Combination therapies have shown up to 30% improvement in treatment response rates, driving increased adoption in cancer immunotherapy.

Advancements in Delivery Technologies: Lipid nanoparticle delivery systems have improved cellular uptake efficiency by approximately 28%, while next-generation carriers are reducing toxicity levels by nearly 20%, enhancing overall treatment safety and effectiveness.

Manufacturing Capacity Growth: Global mRNA production capacity has increased by over 35% since 2023, with new facilities capable of producing more than 1 billion doses annually, supporting both therapeutic and vaccine demand across regions.

Integration of AI in Drug Development: AI-driven mRNA design platforms are reducing candidate discovery timelines by 25%and improving sequence optimization accuracy by over 30%, accelerating innovation and reducing development risks.

The MRNA-Based Therapeutics and Vaccines Market is segmented based on type, application, and end-user, reflecting diverse adoption patterns across the healthcare ecosystem. Prophylactic vaccines dominate due to established immunization programs, while therapeutic applications are rapidly expanding in oncology and rare diseases. Infectious disease applications remain foundational, but oncology and genetic therapies are gaining momentum due to increasing clinical success rates. End-users include hospitals, research institutions, and biotechnology companies, each contributing uniquely to market growth. Regional variations in adoption highlight strong demand in North America and Europe, with Asia-Pacific emerging as a key growth region due to expanding healthcare infrastructure and manufacturing capabilities.

Prophylactic mRNA vaccines currently account for approximately 58% of total adoption, driven by widespread immunization programs and established healthcare infrastructure. Therapeutic mRNA applications, including cancer vaccines and protein replacement therapies, hold around 42%, but are expanding rapidly due to increasing clinical success. The therapeutic segment is the fastest-growing, expected to expand at a CAGR of 16.8%, driven by rising demand for personalized medicine and oncology treatments. Emerging types such as self-amplifying mRNA and circular RNA technologies collectively contribute about 12% of innovation pipelines, offering extended protein expression and improved stability.

Infectious disease applications dominate with approximately 42% share, supported by large-scale vaccination programs and pandemic preparedness initiatives. Oncology applications account for around 38%, driven by personalized cancer vaccines and immunotherapy advancements. The oncology segment is the fastest-growing, expanding at a CAGR of 17.5%, supported by increasing clinical trials and investment. Other applications, including rare genetic diseases and protein replacement therapies, contribute the remaining 20%. In 2025, over 40% of global hospitals reported integrating mRNA-based therapies into oncology treatment protocols, while approximately 35% of biotech firms are actively developing mRNA-based solutions for rare diseases.

Hospitals and clinics represent the leading end-user segment, accounting for approximately 52% of market adoption, driven by direct patient treatment and vaccine administration. Research institutions and academic centers hold around 28%, focusing on clinical trials and innovation. Biotechnology and pharmaceutical companies contribute approximately 20%, supporting product development and commercialization. The fastest-growing end-user segment is biotechnology firms, expanding at a CAGR of 15.9%, driven by increased investment and innovation in mRNA platforms. In 2025, over 60% of large healthcare providers reported adopting mRNA-based therapies for oncology and infectious diseases, while approximately 45% of research institutions are actively engaged in mRNA-related studies.

North America accounted for the largest market share at 41.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of16.1% between 2026 and 2033.

North America leads with over 55% of global mRNA clinical trialsand more than 70% hospital adoption in advanced oncology programs, supported by strong biotech ecosystems and large-scale manufacturing capacity exceeding 1.5 billion doses annually. Europe holds approximately 28.6% share, driven by regulatory alignment and cross-border R&D collaborations, particularly in Germany, the UK, and France, where over 65% of pharmaceutical firms are actively engaged in mRNA pipelines. Asia-Pacific accounts for nearly 19.4% share, with rapid infrastructure expansion and more than 80 new biotech facilities established since 2022across China, India, and Japan. South America and Middle East & Africa collectively contribute around 10.2%, supported by increasing public health investments and localized vaccine production initiatives. Regional demand is further shaped by rising oncology cases, where mRNA-based therapies are being adopted in over 40% of global cancer-focused clinical programs, reinforcing long-term regional expansion dynamics.

North America holds approximately 41.8% of the global market share, supported by strong demand from healthcare, biotechnology, and pharmaceutical industries. The region benefits from extensive government funding programs and regulatory fast-track approvals that accelerate mRNA product commercialization. Over 75% of large hospitalsin the U.S. have integrated mRNA-based solutions into oncology and infectious disease treatment frameworks. Technological advancements such as AI-driven mRNA design and next-generation lipid nanoparticle delivery systems are widely deployed, improving therapeutic outcomes by over 30%. A key regional player, Moderna, continues to expand its mRNA platform into oncology and rare diseases, with over 40 active pipeline programs. Consumer behavior reflects high trust and adoption, with strong uptake in preventive healthcare and personalized medicine applications, particularly in urban healthcare systems.

Europe represents approximately 28.6% of the global market, driven by strong pharmaceutical ecosystems in Germany, the UK, and France. Regulatory bodies such as the European Medicines Agency are facilitating accelerated approvals and harmonized compliance standards across member states. Sustainability initiatives are influencing product development, with over 50% of companies focusing on reducing cold-chain emissions and improving energy efficiency. Adoption of emerging technologies, including self-amplifying mRNA and digital clinical trial platforms, is increasing across the region. BioNTech, a major regional player, is advancing oncology-focused mRNA therapies with multiple late-stage clinical trials. Consumer behavior shows a preference for highly regulated and clinically validated treatments, with regulatory pressure driving demand for transparent and explainable therapeutic outcomes.

Asia-Pacific ranks as the fastest-growing region, accounting for approximately 19.4% of global market volume, with China, India, and Japan as key contributors. The region has seen the establishment of over 80 new mRNA manufacturing and R&D facilities since 2022, significantly enhancing production capacity. Governments are investing heavily in biotechnology infrastructure, with public funding initiatives increasing by over 35% in recent years. Regional innovation hubs are focusing on cost-effective mRNA production and localized vaccine development. A notable player, Stemirna Therapeutics in China, is advancing mRNA vaccine platforms with multiple clinical-stage candidates. Consumer adoption is driven by expanding healthcare access and digital health integration, with growth supported by increasing mobile health platforms and rising awareness of advanced therapeutics.

South America contributes approximately 6.3% of the global market, with Brazil and Argentina leading regional demand. Infrastructure development in healthcare and biotechnology sectors is improving, with over 25 new research collaborations established in the past three years. Governments are introducing incentives and trade policies to support local vaccine production and reduce dependency on imports. Regional adoption is supported by increasing public health programs targeting infectious diseases and oncology treatments. Local players are focusing on partnerships with global biotech firms to expand access to mRNA technologies. Consumer behavior indicates rising demand for advanced therapies, particularly in urban centers, where healthcare accessibility and awareness are significantly higher.

The Middle East & Africa region accounts for approximately 3.9% of the global market, with key growth countries including the UAE and South Africa. Demand is supported by healthcare modernization initiatives and increasing investment in biotechnology infrastructure. Governments are forming strategic partnerships to enable technology transfer and local manufacturing capabilities. Over 15 regional biotech initiatives have been launched to support vaccine and therapeutic development. Adoption of digital health technologies and modern clinical frameworks is gradually improving market penetration. Consumer behavior reflects growing awareness and acceptance of advanced treatments, particularly in metropolitan areas, supported by expanding healthcare infrastructure and international collaborations.

United States – 32% Market share: driven by high production capacity, advanced clinical infrastructure, and strong biotechnology investment.

Germany – 11% Market share: supported by robust pharmaceutical R&D ecosystem and advanced manufacturing capabilities.

The MRNA-Based Therapeutics and Vaccines Market is moderately consolidated, with over 60 active global competitorsranging from large pharmaceutical companies to emerging biotechnology firms. The top five players collectively account for approximately 58–62% of the total market share, indicating strong concentration among leading innovators. Key companies are focusing on strategic partnerships, co-development agreements, and licensing deals to expand their mRNA technology platforms. Over 45 strategic collaborationshave been recorded between 2023 and 2025, highlighting the importance of shared innovation and risk mitigation. Product development pipelines are highly competitive, with more than 150 active mRNA candidates across various therapeutic areas, particularly oncology and infectious diseases. Companies are increasingly investing in next-generation delivery systems and AI-based drug design to enhance efficiency and differentiation. Mergers and acquisitions are also shaping the competitive landscape, with mid-sized biotech firms being acquired to strengthen technological capabilities. Continuous innovation, pipeline expansion, and manufacturing scalability remain key factors influencing competitive positioning.

BioNTech

Pfizer

CureVac

Sanofi

GlaxoSmithKline

AstraZeneca

Novartis

Roche

Merck & Co.

Takeda Pharmaceutical

Eli Lilly and Company

Arcturus Therapeutics

Translate Bio

The MRNA-Based Therapeutics and Vaccines Market is experiencing rapid technological evolution, driven by advancements in delivery systems, molecular design, and manufacturing processes. Lipid nanoparticle (LNP) technology remains the cornerstone of mRNA delivery, with recent innovations improving encapsulation efficiency by over 30% and reducing toxicity levels by approximately 20%. Self-amplifying mRNA (saRNA) platforms are gaining traction, offering up to 10-fold higher protein expressioncompared to conventional mRNA, enabling lower dosage requirements and extended therapeutic effects.

Artificial intelligence and machine learning are increasingly integrated into mRNA sequence design, reducing development timelines by nearly 25%and enhancing target specificity. Automated and modular manufacturing systems are enabling scalable production, with new facilities capable of producing over 500 million doses annuallyusing continuous processing techniques. Thermostable mRNA formulations are also emerging, reducing cold-chain dependency by enabling storage at 2–8°C for extended periods, improving distribution efficiency.

Gene-editing integration with mRNA platforms is another key advancement, enabling transient expression of CRISPR-based systems for targeted gene therapies. Digital twin technologies and real-time analytics are improving quality control, reducing batch failure rates by over 18%. These technological innovations are collectively transforming the mRNA landscape, making it more efficient, scalable, and adaptable for a wide range of therapeutic applications.

• In August 2025, Moderna announced U.S. FDA approval for its updated mRNA COVID-19 vaccine targeting the LP.8.1 variant, along with approvals in Europe and Canada. The updated formulation enhances protection against emerging variants and supports global immunization strategies. Source: www.modernatx.com

• In September 2025, Pfizer and BioNTech reported Phase 3 clinical data showing at least a 4-fold increase in neutralizing antibody titersusing their LP.8.1-adapted mRNA vaccine, reinforcing strong immune response performance across adult and high-risk populations.

• In May 2025, Pfizer and BioNTech submitted a regulatory application to the European Medicines Agency for their updated COMIRNATY® mRNA vaccinetargeting the LP.8.1 strain, advancing next-season vaccine readiness and strengthening regulatory alignment across Europe.

• In June 2024, Moderna reported positive Phase 3 data for its next-generation mRNA COVID-19 vaccine (mRNA-1283), demonstrating improved immune response and supporting advancement of its next-generation vaccine portfolio and combination vaccine strategies.

The MRNA-Based Therapeutics and Vaccines Market Report provides a comprehensive analysis of key segments, technologies, applications, and regional dynamics shaping the industry. The scope includes detailed segmentation by type, covering prophylactic and therapeutic mRNA platforms, along with emerging technologies such as self-amplifying and circular RNA constructs. Application coverage spans infectious diseases, oncology, rare genetic disorders, and protein replacement therapies, reflecting the expanding use cases of mRNA technology.

Geographically, the report analyzes major regions including North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting variations in adoption, infrastructure, and investment patterns. It also evaluates end-user segments such as hospitals, research institutions, and biotechnology firms, providing insights into usage patterns and demand drivers. Technological coverage includes delivery systems like lipid nanoparticles, AI-driven sequence design, and modular manufacturing processes.

The report further explores competitive dynamics, innovation pipelines, regulatory frameworks, and strategic collaborations influencing market development. Emerging areas such as personalized medicine, gene-editing integration, and thermostable formulations are also examined, offering forward-looking insights. This comprehensive scope enables stakeholders to understand market structure, identify growth opportunities, and make informed strategic decisions across the evolving mRNA therapeutics and vaccines ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 6,521.0 Million |

| Market Revenue (2033) | USD 18,904.1 Million |

| CAGR (2026–2033) | 14.23% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Moderna Inc.; BioNTech SE; Pfizer Inc.; CureVac N.V.; Sanofi S.A.; GlaxoSmithKline plc; AstraZeneca plc; Novartis AG; Roche Holding AG; Merck & Co., Inc.; Takeda Pharmaceutical Company Limited; Eli Lilly and Company; Arcturus Therapeutics Holdings Inc.; Translate Bio Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |