Reports

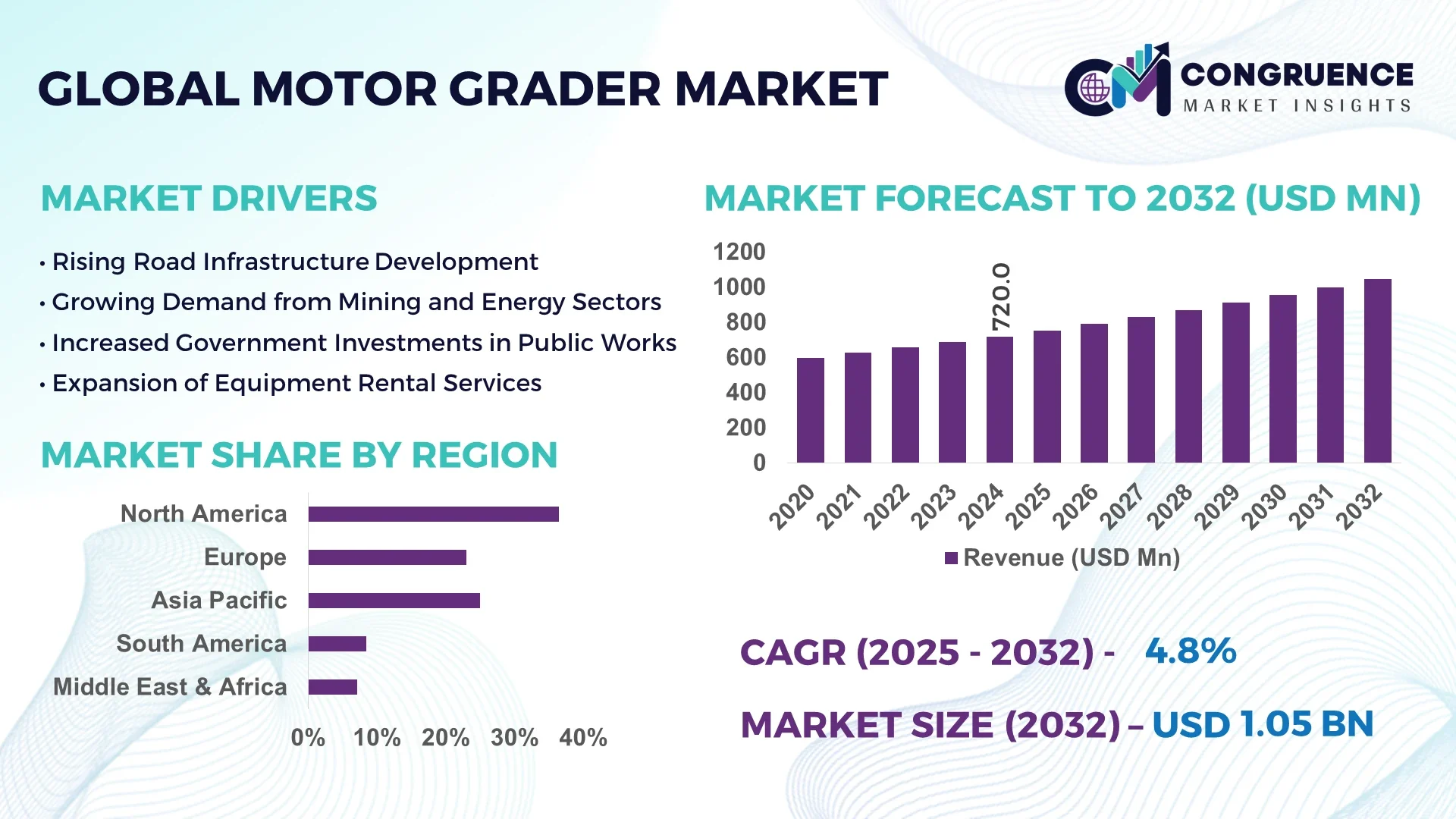

The Global Motor Grader Market was valued at USD 720 Million in 2024 and is anticipated to reach a value of USD 1,043.7 Million by 2032 expanding at a CAGR of 4.75% between 2025 and 2032.

The United States leads in motor grader production capacity, operating multiple high-output assembly plants and R&D centers focused on advanced hydraulic and GPS-integrated machines. It has invested heavily in smart manufacturing, robotic assembly, and digital cabin technologies, supplying graders for both public infrastructure and private construction sectors.

The Motor Grader Market encompasses several industry sectors such as road construction, mining, and infrastructure development. Road infrastructure accounts for a major share due to extensive repaving and new highway programmes. Technological and product innovations include semi-autonomous grading modules, GPS-guided blade control, and hybrid powertrain systems. Environmental and economic drivers—such as stricter emissions regulations and rising public spending on rural connectivity—are increasing demand in emerging regions. Consumption patterns reveal high uptake in North America, Western Europe, and Southeast Asia. Emerging trends include modular grader assemblies for rental and fleet operations, telematics-based fleet management, and introduction of electric and hybrid graders. The outlook shows steady modernization of fleets, ongoing digital transformation, and expansion in both developed and emerging economies.

AI is transforming operations within the Motor Grader Market by enabling automation, predictive maintenance, and optimized performance. AI-powered sensors now deliver real-time blade control, using terrain and slope data to adjust blade angles automatically—reducing material overcuts and ensuring precise grading. In practical terms, some grader systems report a 20% reduction in material rework and fuel savings up to 15%, thanks to AI-driven blade precision.

Operational efficiency is further enhanced through dynamic scheduling and fleet optimization. AI fleet-management platforms process telematics data—such as engine load, idle time, and location—to direct the nearest grader to tasks, reducing average reposition time by 30%. For site operators, this facilitates higher utilization rates and lower operational costs.

Maintenance is evolving from routine to predictive. Embedded AI monitors engine temperature, hydraulic pressure, and vibration. Early analysis warnings now allow replacement of components before failure occurs, cutting unplanned downtime by 35%. Process workflows are more streamlined using machine-learning models that adapt maintenance schedules based on actual usage, improving longevity and reducing repair cycles.

AI also builds operator capability by integrating remote coaching systems and virtual assistants that provide live guidance. For example, AI messages inform operators about optimal blade settings on varying terrain, enhancing performance consistency—especially in less experienced crews.

By strategically embedding intelligence into machines and fleet systems, the Motor Grader Market is seeing higher utilization, reduced costs, and improved precision. AI is enabling a shift from reactive to proactive operations, underpinning smarter, safer, and more sustainable grading.

“In 2024, a major OEM introduced an AI-enhanced grader capable of autonomously fine-tuning blade angle across 1500 m surfaces, achieving 98% first-pass accuracy.”

The Motor Grader Market is shaped by increasing demand for digital precision, efficiency, and sustainability. Demand for high-capacity machines is rising, pushed by governments launching large-scale infrastructure projects and urban expansion. Fleet modernization initiatives and the adoption of GPS/laser control systems are adding complexity to equipment requirements. Environmental regulations promoting reduced emissions are accelerating transitions toward hybrid and electric drive-trains. Simultaneously, rental and leasing models are expanding, encouraging OEMs to invest in modular designs and remote diagnostics. Overall, the market is becoming more technologically integrated, capitalizing on automation, telematics, and emissions compliance to align with evolving public and private sector requirements.

Advanced hydraulic systems and AI-controlled blade positioning are revolutionizing efficiency in the Motor Grader Market. The integration of load-sensing hydraulics and mast-less GPS guidance enables consistent depth and slope control, reducing operator error by up to 30% and improving site productivity. This precise control is particularly valuable in high-volume reprofiling projects and final-grade tasks. As a result, contractors are increasingly specifying graders with intelligent hydraulic systems to meet quality standards in road construction and grading pitches.

Motor graders equipped with AI-based automation and GPS guidance command purchase premiums often 25–40% higher than conventional models. These costs, combined with the need for skilled operators trained in digital grading systems, hinder market penetration among smaller contractors. In emerging markets, the adoption of advanced graders is further slowed by lack of infrastructure to support GPS accuracy and limited availability of formal training programs, causing delayed uptake despite potential efficiency gains.

The Rental and Fleet-as-a-Service model is gaining momentum. Rental fleets offering modular, AI-enabled graders are growing at approximately 20% annually in North America and Europe. This allows contractors to deploy advanced machines without capital expenditure, supported by telemetry-based maintenance. Fleet providers report 15–20% higher utilization and lower downtime in such models, presenting a business opportunity for OEMs and rental agencies to partner on service-led offerings.

As global regions adopt stricter Stage V and Tier 4 emissions standards, manufacturers must redesign engine systems and after-treatment devices. These regulations increase unit costs by up to 10% and introduce technical complexity in integrating emission hardware with grade-control systems. Delays in certifying hybrid or electric graders against multiple regional standards can stall product launch schedules, complicating go-to-market strategies and increasing compliance overhead.

Rise in Modular and Prefabricated Construction: Prefabricated grader components, such as engine modules and hydraulic units, are being assembled off-site using precision robotics, reducing on-site installation time by 25% and labor hours by 20%. This trend is particularly impactful in North America and Europe, enabling rapid deployment in rental fleets and infrastructure projects.

Shift Toward Electric and Hybrid Powertrains: Electric and hybrid motor graders are gaining traction, with pilot machines reporting 15–20% fuel savings and 30–40% lower CO₂ emissions compared to diesel models. These graders are being trialled in municipal roadwork and mining sites, especially in low-emission zones.

Telemetry-Enabled Fleet Optimization: Grader fleets are now standardized with telematics systems that track usage, idle time, location, and maintenance needs in real time. Contractors using these platforms report 20–25% improvements in fleet uptime and 10% reductions in fuel consumption across multi-machine operations.

Autonomous and Semi-Autonomous Control: Automated blade control systems utilizing GPS, laser, or sonic sensors are installed on over 30% of new high-end graders. These systems deliver consistent slope and contour adherence with 98% first-pass accuracy, significantly reducing rework in road base preparation.

The Motor Grader Market is segmented based on type, application, and end-user. Each segment reveals distinct dynamics shaping the demand and product development strategies in the industry. By type, motor graders range from rigid frame to articulated models, with size and engine capacity variations suited to different terrains and project scales. Applications span from construction and mining to road maintenance and snow removal. End-user segments include government agencies, construction contractors, mining companies, and rental service providers. These categories help manufacturers and stakeholders align product innovations, marketing strategies, and supply chains with customer needs. The demand trends vary across regions; for example, articulated graders are more favored in rugged terrains like South America and Africa, while North America drives innovation in smart grader technologies for urban construction. Understanding these segmentation patterns enables industry players to identify high-growth areas, optimize pricing strategies, and prioritize product line expansion based on operational use cases.

Motor graders are commonly categorized into rigid frame and articulated frame types, each serving specific operational requirements. Among these, articulated frame graders dominate the market due to their enhanced maneuverability and suitability for uneven terrain and tighter project sites. Their pivoting capabilities make them essential for urban infrastructure development and mining operations where flexibility is critical.

The fastest-growing type is the automated or AI-integrated graders, driven by increasing demand for precision in grading, reduced labor dependency, and integration with digital site management systems. These graders use real-time sensors and automated blade control, enhancing efficiency in both small-scale and large-scale projects.

Other grader types include compact motor graders, which are ideal for municipal maintenance and small-scale construction. Though niche, they are gaining relevance in emerging economies where urban infrastructure is expanding, and maneuverability is prioritized. The evolution of grader types continues to focus on adaptability, digital integration, and operator comfort to meet industry-specific requirements.

The Motor Grader Market serves a broad spectrum of applications. Road construction and maintenance is the leading application area, accounting for the majority of motor grader usage. Graders are essential for leveling roadbeds, shaping surfaces, and ensuring uniform gradients in highway and rural road development projects. Their use is widespread in national infrastructure programs globally.

The fastest-growing application is mining and quarrying, particularly in regions such as Africa and Latin America. The demand stems from the need for terrain leveling, haul road maintenance, and efficient transport of extracted materials. The rugged environment necessitates durable and high-powered graders with minimal downtime and advanced performance monitoring.

Other notable applications include snow removal in colder regions, where graders are fitted with front blades and specialized tires. Additionally, agricultural land development and airfield maintenance are emerging use cases, particularly in regions investing in logistics infrastructure. Each application segment defines unique performance requirements, influencing the product design and technology adoption.

Among all end-user categories, government and municipal agencies represent the leading segment due to their consistent procurement of motor graders for public infrastructure development, rural road connectivity, and urban planning initiatives. Their preference for durable, mid- to high-capacity graders ensures a steady demand for standardized models.

The fastest-growing end-user group is the rental and leasing service providers, especially in developed regions. Contractors increasingly rely on rental solutions to reduce capital expenditure while accessing the latest technology in AI-integrated and telematics-enabled graders. Rental fleets offer flexibility and are often maintained under service contracts, reducing downtime for users.

Other important end-users include construction contractors engaged in large-scale industrial, commercial, and residential projects. They require a diverse range of graders based on project type and complexity. Mining companies also contribute significantly, especially those operating in remote or high-load regions where heavy-duty and high-efficiency graders are critical to site operations. Each end-user segment has specific product performance expectations, driving varied grader configurations and service support needs.

North America accounted for the largest market share at 36.4% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2025 and 2032.

The Motor Grader Market displays diverse regional dynamics driven by infrastructure investment, regulatory frameworks, and digital technology adoption. North America leads due to its established construction sector, advanced rental models, and rapid integration of GPS-enabled graders. In contrast, Asia-Pacific is witnessing rapid industrial expansion, road development initiatives, and increasing adoption of mid-range graders in countries like China and India. Europe continues to emphasize sustainability and automation, while South America and the Middle East & Africa are evolving with energy-related infrastructure and government-backed urban expansion projects. Regional demand is also influenced by climate-related usage like snow grading in colder regions and rugged terrain leveling in mining zones. Across regions, public-private partnerships, modernization efforts, and smart construction solutions are redefining grader procurement and deployment patterns.

North America held a commanding 36.4% share of the global Motor Grader Market in 2024, primarily driven by robust road infrastructure programs in the U.S. and Canada. Demand is high across transportation, oil & gas, and commercial construction sectors. The U.S. Department of Transportation’s sustained funding for highway maintenance has ensured consistent grader procurement. Technological advancements, such as GPS-controlled blade systems and real-time telematics, are widely adopted among contractors. The region has also seen a rapid expansion of grader rental services, offering AI-integrated machines to mid-size construction firms. Government incentives supporting smart infrastructure and emissions regulation compliance further reinforce demand for modern, low-emission models across the region.

Europe represents a vital region in the Motor Grader Market with a focus on smart construction and sustainability initiatives. Key countries such as Germany, the UK, and France are investing in green infrastructure and autonomous road maintenance systems. Europe’s market share is shaped by public sector investments in rural and urban road upgrades, especially under EU regional development funds. Regulatory oversight by bodies such as the European Environment Agency is accelerating the shift to hybrid and electric graders. Technological adoption includes 3D machine control systems and BIM-integrated graders, particularly in Germany and the Netherlands. Demand for mid-sized graders in Eastern Europe is also growing due to cross-border transport corridor development.

Asia-Pacific is emerging as the fastest-growing region in the Motor Grader Market, driven by high construction activity and increasing investment in road networks. Countries such as China, India, and Japan are major consumers of motor graders, with China accounting for the largest volume within the region. Government programs like India’s Bharatmala and Japan’s Smart Infrastructure Plan are expanding the use of advanced construction equipment. Manufacturing hubs in China and South Korea are also exporting cost-effective graders across Southeast Asia. The region is seeing a surge in localized automation technologies and AI-driven blade control tailored to diverse terrain conditions, bolstering grader utility in infrastructure megaprojects.

South America is a key region for the Motor Grader Market, led by countries such as Brazil and Argentina. The region’s share is primarily supported by government-led infrastructure upgrades and mining sector activity. Brazil, in particular, uses motor graders extensively for rural connectivity and agribusiness-related infrastructure. Demand is also increasing from public housing and urban road projects. Government incentives aimed at reducing equipment imports and promoting local assembly are influencing procurement strategies. The integration of grader fleet tracking systems is gradually improving equipment uptime and productivity across construction sites and extractive industries.

The Middle East & Africa Motor Grader Market is witnessing significant momentum driven by infrastructure, energy, and construction development. Countries such as UAE and South Africa are investing in expressway expansion, industrial zones, and smart city initiatives. Graders are in demand for site leveling, road expansion, and desert terrain shaping. Demand trends also stem from oil and gas pipeline development in the Gulf and mining operations in Sub-Saharan Africa. Technological upgrades, such as GPS-enabled grading and AI diagnostics, are gaining traction in premium segments. Local regulatory support for modern fleet integration is boosting investments in high-capacity and all-weather motor graders.

United States - 32.1% Market Share

The United States leads the Motor Grader Market due to high production capacity and widespread use in infrastructure and road maintenance.

China - 26.8% Market Share

China ranks second in the Motor Grader Market owing to strong end-user demand, ongoing mega infrastructure projects, and competitive domestic manufacturing.

The Motor Grader Market is characterized by the presence of more than 25 active global and regional players, each competing on the basis of innovation, product reliability, and aftermarket support. The market is moderately consolidated, with leading OEMs such as Caterpillar, Komatsu, and John Deere maintaining strong brand positioning through expansive product portfolios, dealer networks, and continuous technological upgrades. These companies focus heavily on R&D to integrate advanced features like autonomous grade control, real-time diagnostics, and fuel-efficient engines.

Strategic initiatives, such as joint ventures and distribution partnerships, are shaping the competitive environment. For example, some manufacturers have entered into agreements with AI and IoT firms to offer predictive maintenance solutions and machine learning-powered performance analytics. The market has also seen a rise in product launches focused on hybrid-electric systems and emissions-compliant machines. Furthermore, tier-2 players from China and India are gaining traction by offering cost-effective, durable alternatives and targeting price-sensitive markets in Asia-Pacific, Africa, and South America.

Innovation in automation and rental-friendly design is increasingly becoming a differentiator, particularly as construction companies demand smarter, more agile solutions. The competitive intensity is expected to rise as sustainability, digital transformation, and user-centric design become standard industry expectations.

Caterpillar Inc.

Komatsu Ltd.

CNH Industrial N.V.

Deere & Company

SANY Group

Doosan Infracore Co., Ltd.

LiuGong Machinery Co., Ltd.

XCMG Construction Machinery Co., Ltd.

Volvo Construction Equipment

Shantui Construction Machinery Co., Ltd.

Mahindra Construction Equipment

Bell Equipment Limited

The Motor Grader Market is undergoing a technological evolution fueled by the growing integration of automation, telematics, and energy-efficient systems. One of the most transformative developments is the integration of GPS-based grade control systems, allowing operators to achieve millimeter-level precision in leveling tasks. These systems reduce the need for manual staking, enhance job site productivity, and minimize material usage.

IoT-enabled graders are gaining popularity due to their ability to transmit real-time performance data, fuel usage patterns, and maintenance alerts. Fleet operators and contractors benefit from predictive maintenance algorithms that reduce machine downtime and extend equipment lifespan. Manufacturers are also investing in AI-driven machine control systems that enable semi-autonomous or fully autonomous operations, especially useful in high-volume road construction or repetitive grading applications.

Hybrid-electric powertrains are also gaining momentum, particularly in markets with stringent emissions regulations. These systems not only lower carbon footprints but also reduce operational costs by optimizing fuel consumption. Another emerging trend is the integration of Building Information Modeling (BIM) compatibility, allowing graders to operate in digitally synchronized construction environments.

Digital operator assistance features such as touchscreen interfaces, adjustable blade sensitivity, and real-time terrain mapping are becoming standard in premium-grade models. Collectively, these technological advancements are redefining productivity benchmarks and shaping future procurement criteria across construction and infrastructure sectors.

In March 2024, John Deere launched its 620G SmartGrade™ Motor Grader equipped with integrated 3D grade control, improving operational precision and eliminating the need for external grade control systems.

In July 2023, Komatsu unveiled a new semi-autonomous motor grader series for mining applications, featuring advanced blade control and obstacle detection systems for enhanced site safety.

In February 2024, XCMG introduced an electric motor grader prototype designed for low-emission urban construction projects, equipped with lithium-ion battery packs and regenerative braking.

In October 2023, Caterpillar partnered with a major telematics provider to integrate AI-based predictive maintenance tools across its grader fleet, resulting in a reported 18% decrease in unexpected service events.

The Motor Grader Market Report offers a comprehensive analysis of the global landscape, covering product types, applications, end-user segments, and key geographies. The report examines both articulated and rigid frame graders, along with compact and AI-enabled variants, evaluating their performance across sectors such as construction, mining, public infrastructure, and municipal services.

Regional insights span North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, each with unique growth drivers, regulatory environments, and consumption patterns. The report also provides a deep dive into technological advancements including telematics integration, hybrid-electric systems, and autonomous control technologies.

From a segmentation perspective, the report addresses applications ranging from road construction and snow removal to quarrying and airport maintenance. It highlights end-users such as governments, construction firms, and equipment rental companies, evaluating evolving procurement strategies and machine requirements.

Additional insights include the market’s competitive landscape, emerging trends like smart construction adoption, and sustainability efforts influencing equipment design. The report supports strategic planning by offering forward-looking intelligence on market opportunities, regional growth pockets, and product innovation pipelines. It is structured to aid equipment manufacturers, policymakers, fleet operators, and investors in making data-driven decisions aligned with evolving market dynamics.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 720.0 Million |

| Market Revenue (2032) | USD 1,043.7 Million |

| CAGR (2025–2032) | 4.75% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Caterpillar Inc., Komatsu Ltd., CNH Industrial N.V., Deere & Company, SANY Group, Doosan Infracore Co., Ltd., LiuGong Machinery Co., Ltd., XCMG Construction Machinery Co., Ltd., Volvo Construction Equipment, Shantui Construction Machinery Co., Ltd., Mahindra Construction Equipment, Bell Equipment Limited |

| Customization & Pricing | Available on Request (10% Customization is Free) |