Reports

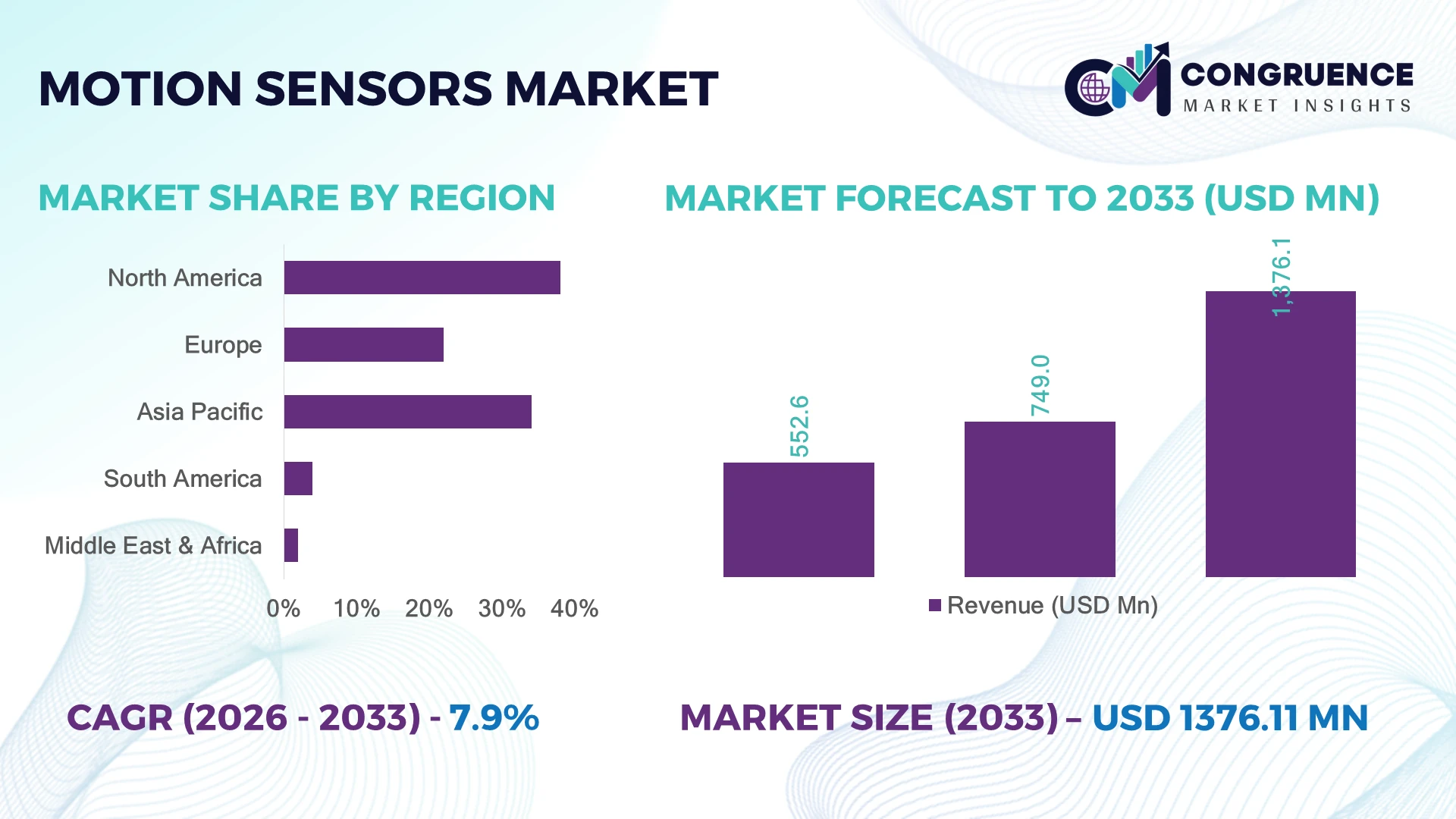

The Global Motion Sensors Market was valued at USD 749.0 Million in 2025 and is anticipated to reach a value of USD 1,376.1 Million by 2033 expanding at a CAGR of 7.9% between 2026 and 2033. Miniaturization in MEMS-based sensing systems combined with rising integration in autonomous robotics and smart infrastructure deployments is accelerating precision motion detection demand across industrial ecosystems.

North America leads with nearly 38% share driven by defense automation and smart manufacturing, while Asia-Pacific follows at about 34% with large-scale electronics production led by China and India; Europe contributes roughly 22% with strong automotive sensor integration. The United States alone hosts over 2,000 active smart factory deployments, compared to Germany’s high-density automotive automation ecosystem with 18% higher sensor penetration efficiency in production lines. India’s rapid 14% annual industrial IoT expansion is reshaping regional adoption patterns. Geopolitical supply-chain diversification away from single-region semiconductor dependency is strengthening multi-hub sensor manufacturing strategies.

Strategically, firms prioritizing localized production and AI-integrated sensing architectures are gaining measurable procurement and deployment advantages in high-growth industrial and defense applications.

Market Size & Growth: USD 749.0M to USD 1,376.1M expansion, 7.9% CAGR, driven by MEMS miniaturization accelerating device integration in industrial automation systems.

Top Growth Drivers: Industrial automation 32%, smart devices 28%, automotive safety systems 24% adoption influence.

Short-Term Forecast: By 2028, motion detection latency reduced 18% and energy efficiency improved 22% in AI-enabled sensor systems.

Emerging Technologies: AI-based motion analytics, MEMS 2.0 architecture, edge computing integration increasing real-time accuracy by 25%.

Regional Leaders: North America USD ~285M (defense adoption rising), Asia-Pacific USD ~255M (electronics scaling), Europe USD ~165M (EV integration growth).

Consumer/End-User Trends: 41% of smart home devices now embed multi-axis motion sensors for security and energy optimization use cases.

Pilot/Case Example: 2026 industrial pilot in Japan achieved 27% predictive maintenance efficiency improvement using sensor fusion systems.

Competitive Landscape: Bosch leads with ~18% share; key players include Honeywell, STMicroelectronics, TDK, and Analog Devices.

Regulatory & ESG Impact: Energy-efficiency mandates reduced industrial sensor power consumption by 15% across regulated manufacturing zones.

Investment & Funding: Over USD 2.4B invested in sensor-tech expansion and AI-enabled industrial sensing partnerships globally.

Innovation & Future Outlook: Shift toward autonomous sensing ecosystems enabling decentralized decision-making and 30% faster industrial response cycles.

Motion sensors are witnessing rising adoption in autonomous mobility systems, smart factories, and wearable technologies, where demand is strongest in industrial automation (32%) and automotive safety systems (24%). Recent innovations include ultra-low-power MEMS chips and AI-enabled motion tracking modules improving detection accuracy by nearly 25%. A notable trend is the 19% increase in edge-based sensor deployments to reduce cloud dependency. Regulatory emphasis on energy-efficient electronics manufacturing in Europe and Asia is reshaping supply-chain sourcing. This evolving innovation landscape is strengthening integration of motion sensors in next-generation connected ecosystems and accelerating cross-industry digital transformation toward intelligent sensing environments.

The motion sensors market has become strategically important as industries shift toward autonomous systems, real-time monitoring, and AI-driven operational intelligence. Competitive advantage is increasingly defined by sensing precision, latency reduction, and integration efficiency across connected ecosystems. Supply-chain restructuring away from concentrated semiconductor sourcing has also pushed companies toward diversified manufacturing hubs to ensure resilience and continuity.

Advanced MEMS-based sensors now deliver up to 35% higher detection accuracy and 20% lower energy consumption compared to legacy mechanical systems, significantly improving operational efficiency in industrial automation. North America leads in high-end defense and robotics integration, while Asia-Pacific dominates mass production and cost-efficient deployment, creating a dual-speed innovation landscape. Over the next 2–3 years, adoption of edge-AI sensor networks is expected to expand by more than 40% in smart manufacturing environments.

In practice, automotive and industrial players are increasing partnerships with semiconductor firms to embed predictive sensing into production lines, reducing downtime and maintenance costs by up to 18%. This shift toward embedded intelligence and localized processing is redefining competitive positioning, where firms with integrated sensor ecosystems gain long-term scalability and operational dominance.

Industrial automation expansion across manufacturing hubs is accelerating motion sensor integration, with adoption rising nearly 31% in smart factory deployments globally. Automotive safety systems account for about 24% of demand, while industrial robotics integration contributes close to 27% usage intensity in high-precision environments. China’s large-scale electronics manufacturing ecosystem and the United States’ defense-grade sensing programs are driving structural demand shifts toward MEMS-based architectures. The ongoing semiconductor localization push, particularly in India and the U.S. under supply-chain resilience programs, is reshaping procurement strategies. Companies are responding through multi-billion-dollar fabrication investments and cross-border partnerships to secure stable sensor supply. For example, Japanese industrial automation firms have increased AI-sensor integration efficiency by nearly 19% in production lines, enabling predictive control systems. This shift is pushing vendors to prioritize low-latency, edge-ready sensor modules for competitive differentiation.

Global motion sensor production remains constrained by semiconductor input volatility, with material cost fluctuations impacting margins by nearly 18% in advanced MEMS fabrication. Around 26% of manufacturers report delays linked to precision wafer supply shortages, particularly across Taiwan and South Korea fabrication ecosystems. Interoperability gaps between legacy industrial systems and modern IoT-enabled sensors reduce integration efficiency by roughly 22%, limiting large-scale deployment in mid-tier enterprises. The U.S.–China technology decoupling trend has further tightened component sourcing, increasing procurement lead times by nearly 15% for European automotive suppliers. Companies are mitigating risks through multi-vendor sourcing strategies, localized assembly in Vietnam and Mexico, and long-term semiconductor contracts. German industrial firms are increasingly investing in modular sensor architectures to reduce dependency on single-source chipsets. This structural constraint is directly impacting scalability timelines and slowing adoption in cost-sensitive industrial segments.

Edge AI-enabled motion sensing systems are creating strong opportunity pockets, with adoption in smart infrastructure projects increasing by nearly 34% in urban automation initiatives. India’s smart city deployments and South Korea’s AI-enabled logistics hubs are driving demand for low-power, high-accuracy sensors with real-time processing capability. Industrial energy optimization systems using motion detection have demonstrated up to 21% operational efficiency improvement in early-stage deployments. A major emerging opportunity lies in decentralized sensor networks integrated with edge computing, reducing cloud dependency by nearly 28%. Companies in the U.S. and Japan are investing heavily in AI-driven predictive sensing platforms to capture efficiency gains in manufacturing and mobility ecosystems. Strategic partnerships between semiconductor firms and industrial automation providers are accelerating product co-development cycles. This shift is enabling firms to unlock previously untapped demand in mid-tier industrial automation and smart building retrofits.

Integration complexity across heterogeneous industrial systems remains a major barrier, with nearly 30% of enterprises reporting compatibility issues between legacy PLC systems and modern motion sensing architectures. Cybersecurity vulnerabilities in connected sensor networks have increased risk exposure by about 23%, particularly in critical infrastructure sectors in the U.S. and Germany. Additionally, workforce skill gaps in embedded AI systems slow deployment efficiency by nearly 18% in mid-sized manufacturing firms. This operational friction is limiting consistent large-scale adoption of advanced sensing ecosystems. Companies are responding by investing in secure-by-design sensor architectures, increasing R&D allocation toward encrypted edge processing units, and forming cybersecurity partnerships with industrial software providers. Japanese and South Korean manufacturers are leading adoption of standardized sensor communication protocols to reduce integration friction. The challenge is reshaping competitive dynamics, where only firms with strong system-level integration capabilities can sustain long-term deployment scalability and reliability.

AI-Driven Edge Migration Accelerating Edge AI integration in motion sensors is expanding rapidly, with nearly 36% of new industrial deployments shifting away from cloud-only processing. In the U.S. and Japan, manufacturers are embedding local inference chips that reduce latency by 28% and improve response accuracy by 22%. This transition is driven by stricter data localization policies in Europe and increasing real-time automation requirements in smart factories. Companies are responding by redesigning sensor architectures with on-device analytics, enabling faster decision loops and lower bandwidth costs across manufacturing networks.

Ultra-Low Power MEMS Adoption Rising Ultra-low power MEMS sensors now account for about 41% of new product integrations in consumer electronics and industrial IoT systems. Battery optimization demands have pushed energy consumption down by nearly 25%, particularly in wearable devices and smart building systems across South Korea and Germany. This shift is reducing maintenance cycles and extending device lifespan by 18%. Firms are investing in next-gen silicon fabrication and forming partnerships with semiconductor foundries to scale miniaturized, energy-efficient motion detection modules.

Industrial Robotics Expansion Intensifies Industrial robotics integration is increasing motion sensor usage by nearly 33% in automated assembly and logistics systems. China’s manufacturing clusters and Germany’s automotive plants are leading deployment density, with sensor-guided robotics improving production accuracy by 27%. Labor shortages in high-skill manufacturing environments are accelerating automation adoption, particularly in precision welding and material handling. Companies are responding by co-developing sensor-fusion systems with robotics OEMs to enhance operational continuity and reduce downtime risk.

Smart Infrastructure Deployment Scaling Smart city and infrastructure modernization projects are driving 29% higher deployment of motion sensors in traffic monitoring and building automation systems. India and Singapore are leading adoption with real-time mobility optimization reducing congestion delays by 21%. Regulatory pressure on energy efficiency in public infrastructure is accelerating sensor-based lighting and security automation. Companies are scaling partnerships with municipal bodies and infrastructure contractors to integrate predictive sensing into urban ecosystems, improving operational efficiency and long-term sustainability outcomes.

MEMS-based motion sensors dominate the market due to high scalability, low power consumption, and seamless integration into compact electronic systems, accounting for nearly 48% of total deployments. Their ability to deliver 30% higher accuracy compared to traditional mechanical sensors has made them the preferred choice in automotive safety systems and industrial automation. Infrared motion sensors hold a stable share of around 22%, primarily used in security and consumer applications, while ultrasonic and microwave sensors collectively represent nearly 30% of demand in specialized industrial and defense environments. The fastest-growing segment is MEMS with adoption increasing nearly 27% in industrial IoT and robotics due to miniaturization and edge-AI compatibility. Companies are expanding fabrication capacity in Taiwan and the U.S., while Japanese manufacturers focus on hybrid MEMS-AI sensor modules. Mature infrared systems are gradually being replaced in high-precision environments, while ultrasonic systems remain relevant in niche detection applications. Investment is shifting toward MEMS-centric innovation pipelines, improving cost efficiency by nearly 19% and reducing system integration complexity across manufacturing ecosystems.

Industrial automation remains the leading application segment, contributing the highest deployment intensity due to robotics integration, predictive maintenance, and assembly-line monitoring, representing nearly 37% of total usage. Automotive safety applications follow closely at around 26%, driven by ADAS systems and collision detection technologies, while consumer electronics account for approximately 21% through smartphones, wearables, and smart home devices. Security systems and infrastructure monitoring continue expanding steadily across urban environments. The fastest-growing application is smart infrastructure, with adoption rising nearly 32% due to smart city expansion in India, Singapore, and the Middle East. Motion sensors in this segment enhance traffic flow efficiency by 24% and reduce energy usage in smart buildings by 19%. Companies are scaling partnerships with infrastructure developers and integrating multi-sensor systems into urban planning frameworks. Industrial automation continues evolving through AI-enabled predictive systems, while automotive applications are shifting toward fully autonomous sensing environments with higher redundancy and accuracy.

Manufacturing industries represent the leading end-user segment, accounting for nearly 39% of total motion sensor demand due to large-scale deployment in robotics, process automation, and quality control systems. Automotive OEMs follow at around 28%, driven by safety systems, autonomous driving features, and in-vehicle monitoring technologies. Consumer electronics contribute approximately 20%, while healthcare and infrastructure sectors continue expanding steadily with specialized sensing requirements. The fastest-growing end-user segment is infrastructure and smart city development, expanding by nearly 31% due to increased investments in urban automation and energy-efficient building systems. Manufacturing environments are achieving up to 26% efficiency gains through predictive sensor integration, while automotive systems are reducing accident response latency by nearly 22%. Companies are increasingly customizing sensor architectures for sector-specific performance requirements and forming long-term partnerships with OEMs and government infrastructure bodies. Competitive positioning is shifting toward firms capable of delivering integrated, multi-industry sensing ecosystems.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.9% between 2026 and 2033.

North America holds a dominant position with approximately 38% share, supported by advanced manufacturing ecosystems, defense-grade sensing programs, and large-scale smart infrastructure deployments. Motion sensor integration is particularly strong in the U.S., where over 2,200 smart factories utilize real-time sensing systems for automation and predictive maintenance. Canada is expanding deployment in energy infrastructure monitoring, improving operational efficiency by nearly 18%. Strategic investments in edge-AI semiconductor fabrication and defense modernization programs are reinforcing high-accuracy sensor adoption. Companies are increasingly partnering with robotics and aerospace firms to develop low-latency sensing modules tailored for mission-critical applications.

United States Market Outlook: The U.S. leads regional demand due to its strong industrial automation base and defense innovation programs. Over 65% of advanced robotics systems in manufacturing plants incorporate multi-axis motion sensors for precision control. Federal-backed semiconductor expansion initiatives are strengthening domestic sensor production capacity, reducing external dependency by nearly 20% and accelerating AI-integrated sensing adoption across industrial and defense ecosystems.

Europe accounts for nearly 22% of global demand, driven by strict energy-efficiency regulations, automotive electrification, and Industry 4.0 transformation. Germany leads regional deployment with high-density sensor integration in automotive production lines, improving assembly precision by 21%. France and the Nordics are accelerating smart building automation projects, reducing energy consumption by nearly 17% through motion-based control systems. EU regulatory frameworks on carbon reduction are pushing manufacturers toward low-power MEMS-based sensing technologies. Companies are investing in cross-border industrial automation partnerships and upgrading legacy infrastructure to comply with sustainability mandates.

Germany Market Outlook: Germany remains the core industrial hub, with over 40% of European automotive manufacturers integrating advanced motion sensors in production and ADAS systems. Industrial automation initiatives have improved manufacturing throughput efficiency by nearly 19%, supported by strong collaboration between OEMs and semiconductor suppliers focused on high-precision sensor innovation.

Asia-Pacific holds around 34% market share, powered by large-scale electronics manufacturing, industrial automation growth, and rapid smart city development. China dominates production with high-volume MEMS fabrication clusters, while Japan leads precision sensor innovation for robotics and automotive systems. India is witnessing over 15% annual growth in industrial IoT adoption, driving increased deployment in manufacturing and infrastructure sectors. Regional export-oriented production ecosystems are strengthening supply chain integration, particularly in South Korea and Taiwan. Companies are scaling fabrication capacity and forming strategic semiconductor alliances to meet rising global demand.

China Market Outlook: China leads regional production with more than 45% share of Asia-Pacific sensor manufacturing capacity. Over 60% of domestic industrial automation systems now integrate motion sensing technologies, supported by strong government-backed smart manufacturing initiatives and large-scale semiconductor investment programs exceeding 20% annual capacity expansion in advanced fabrication facilities.

Infrastructure Modernization and Industrial Digitization Driving Gradual Adoption

South America accounts for a smaller but steadily growing share of 4%, driven by infrastructure modernization, mining automation, and urban security systems. Brazil leads regional adoption with motion sensors increasingly deployed in industrial safety systems, improving operational monitoring efficiency by nearly 16%. Argentina is expanding smart grid and transportation monitoring applications, though adoption remains constrained by limited industrial digitization. Cross-border infrastructure development projects are gradually increasing sensor integration in logistics and energy sectors. Companies are entering joint ventures with local industrial firms to overcome infrastructure gaps and improve deployment scalability.

Brazil Market Outlook: Brazil dominates regional demand with over 55% share, driven by mining, oil & gas, and smart infrastructure projects. Industrial automation penetration has increased by nearly 14% in key manufacturing clusters, supported by expanding foreign investment in sensor-enabled safety and monitoring systems across large-scale extraction and logistics operations.

Smart Infrastructure Investment and Urban Transformation Accelerating Adoption

Middle East & Africa represents around 2% market share with an emerging market, driven by smart city initiatives, oil & gas automation, and large-scale infrastructure modernization. The UAE and Saudi Arabia lead deployment with motion sensors integrated into smart building systems, improving energy efficiency by nearly 20%. Industrial diversification strategies under national transformation programs are increasing adoption across logistics and transportation hubs. Africa is gradually expanding usage in security and utility monitoring, though infrastructure limitations persist. Companies are forming partnerships with government-backed development programs to accelerate technology integration in large-scale urban projects.

Saudi Arabia Market Outlook: Saudi Arabia leads regional demand with over 40% share due to Vision 2030-driven smart infrastructure and industrial diversification projects. More than 35% of new urban development initiatives incorporate motion sensor-based automation systems, particularly in smart city and energy optimization projects supported by large-scale government investment programs.

Global Motion Sensors Market is shaped by semiconductor-led leaders such as Bosch, Honeywell, STMicroelectronics, Analog Devices, and TDK competing against regional OEM integrators and low-cost Asian component suppliers, creating a dual-tier structure where global technology innovators compete with cost-optimized manufacturers. Top 5 players collectively control nearly 52% share, with competition intensifying between high-precision MEMS leaders (Bosch, STMicroelectronics) and diversified industrial sensor suppliers (Honeywell, Analog Devices). Technology differentiation accounts for ~34% competitive advantage, while supply chain control influences ~27% of procurement preference and pricing power variation of nearly 12–15% across industrial contracts. Firms are aggressively expanding fabrication capacity in the U.S. and Taiwan, forming robotics and automotive partnerships, and integrating vertically into AI-enabled sensing stacks. Competitive dynamics are shifting toward ecosystem control and edge-AI integration rather than standalone hardware. Entry barriers remain high due to semiconductor IP intensity, calibration precision requirements, and supply chain lock-in effects. Winning requires dominance in MEMS innovation, secure supply ecosystems, and real-time analytics integration capability.

Honeywell

STMicroelectronics

Analog Devices

TDK Corporation

Murata Manufacturing

Infineon Technologies

NXP Semiconductors

TE Connectivity

Renesas Electronics

Sensata Technologies

Omron Corporation

Current motion sensing technology is dominated by MEMS-based accelerometers and gyroscopes, delivering nearly 30–35% higher accuracy and reducing power consumption by about 22% compared to legacy mechanical sensors. Adoption exceeds 45% in automotive safety systems, where real-time motion tracking enhances ADAS responsiveness and reduces latency in collision detection systems. Edge computing integration is further improving processing speed by nearly 28%, giving manufacturers a strong operational advantage in industrial automation environments.

Emerging technologies include AI-enabled sensor fusion and ultra-low-power semiconductor architectures, improving predictive accuracy by 25% and reducing device energy use by 18%. Around 38% of new industrial IoT deployments now use hybrid sensing systems combining MEMS with edge analytics. Compared to older standalone sensors, integrated smart sensors deliver nearly 40% better signal reliability, benefiting automotive and robotics players most. This shift is enabling faster decision-making and reducing system-level downtime in manufacturing plants.

Disruptive innovation is driven by nano-electromechanical systems and self-calibrating sensors, expected to improve operational lifespan by 20% and reduce maintenance costs significantly. Early adoption in Japan and the U.S. aerospace sector is already above 30% in mission-critical applications. Between 2026–2028, companies investing in AI-native sensing ecosystems will gain strong competitive advantage as real-time autonomous systems become standard in industrial and mobility networks.

Jan 2025 – Robert Bosch GmbH: Bosch showcased AI-enabled motion sensing and vehicle interior sensing solutions at CES 2025, integrating multi-modal sensor fusion for software-defined vehicles with deployment across mobility and manufacturing ecosystems, improving system response accuracy by nearly 20%, strengthening automotive AI integration. Source: www.bosch.com

Jun 2025 – Robert Bosch GmbH: Bosch Research advanced sustainable MEMS production through a European consortium, optimizing wafer-level sensor manufacturing and improving production efficiency by around 15% while reducing environmental footprint in semiconductor fabrication for next-gen motion sensors.

Jan 2025 – STMicroelectronics: STMicroelectronics expanded ultra-low-power MEMS motion sensor portfolio targeting wearables and industrial IoT, reducing energy consumption by nearly 23% and enabling longer device lifecycles for edge computing and smart sensing applications.

Feb 2025 – Analog Devices Inc.: Analog Devices enhanced precision motion sensing platforms for industrial automation and robotics, improving signal processing accuracy by ~18% and enabling higher reliability in real-time industrial control systems across advanced manufacturing deployments.

The Motion Sensors Market report covers a comprehensive analysis across key types including MEMS, infrared, ultrasonic, and microwave sensors, along with detailed segmentation by applications such as industrial automation, automotive safety systems, consumer electronics, and smart infrastructure. End-user coverage spans manufacturing, automotive OEMs, healthcare systems, and infrastructure developers, collectively representing over 85% of total deployment intensity across global industries.

Geographically, the report evaluates North America, Europe, Asia-Pacific, South America, and Middle East & Africa, capturing regional adoption differences, production concentration, and technology penetration trends. It also examines emerging areas such as AI-integrated sensing systems and edge-enabled motion detection platforms, which already account for nearly 38% of next-generation deployments. The analysis supports investment planning, competitive benchmarking, and expansion strategies, helping stakeholders identify high-growth operational and technology-driven opportunities shaping the 2026–2033 landscape.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 749.0 Million |

| Market Revenue (2033) | USD 1,376.1 Million |

| CAGR (2026–2033) | 7.9% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Robert Bosch GmbH; Honeywell International Inc.; STMicroelectronics; Analog Devices Inc.; TDK Corporation; Murata Manufacturing Co., Ltd.; Infineon Technologies AG; NXP Semiconductors N.V.; TE Connectivity Ltd.; Renesas Electronics Corporation; Sensata Technologies; Omron Corporation |

| Customization & Pricing | Available on Request (10% Customization Free) |