Reports

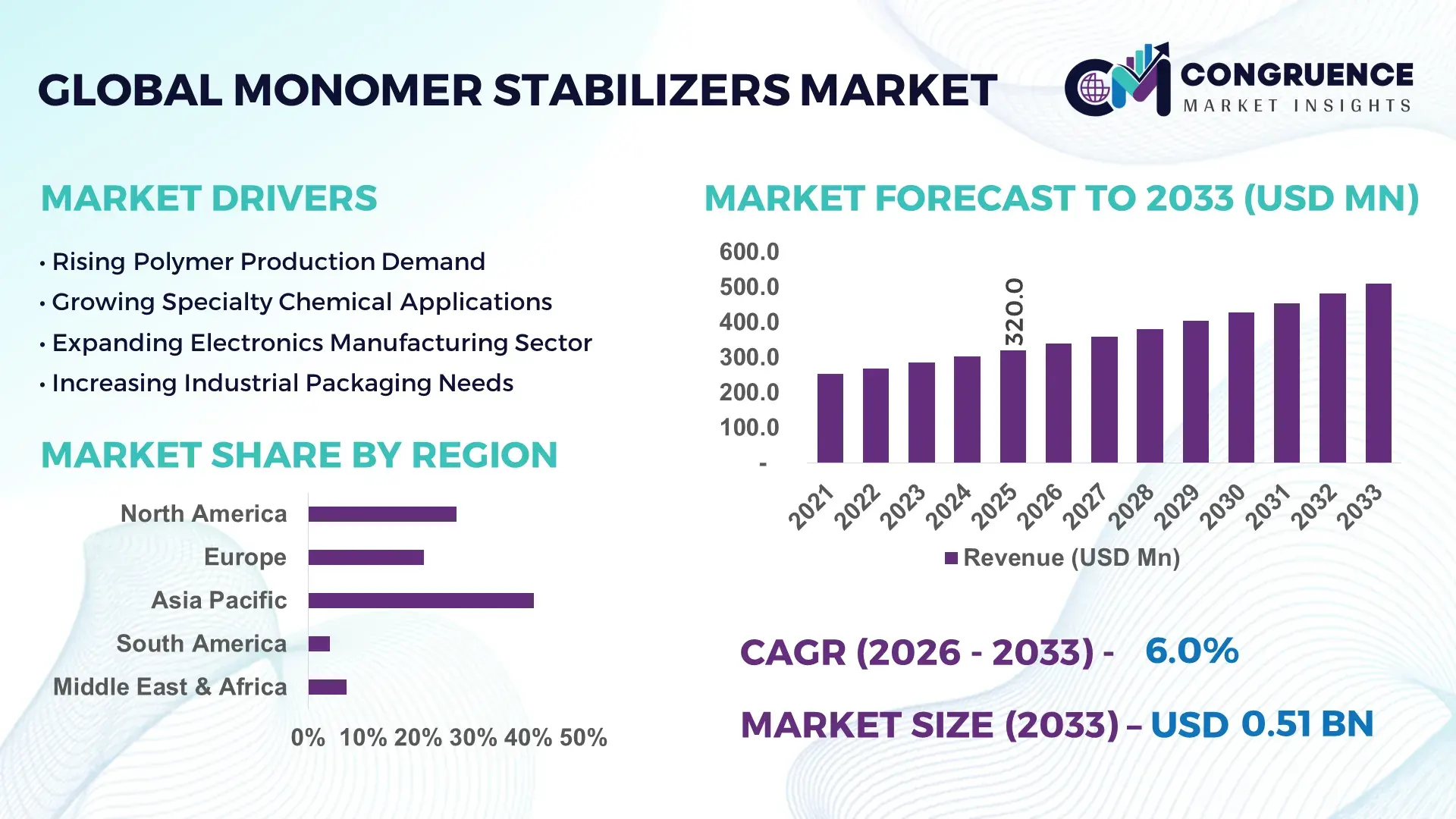

The Global Monomer Stabilizers Market was valued at USD 320.0 Million in 2025 and is anticipated to reach a value of USD 510.0 Million by 2033 expanding at a CAGR of 6.0% between 2026 and 2033. Rising adoption of high-performance acrylics, styrene, and vinyl-based polymers across automotive coatings, electronics encapsulation, and industrial packaging is accelerating the use of advanced monomer stabilizers capable of extending shelf life by over 25% while reducing premature polymerization losses. The market is also benefiting from the transition toward continuous polymer processing systems, where thermal stability and inhibitor precision have become critical for maintaining production efficiency and lowering waste generation by nearly 18%. Between 2024 and 2026, tightening chemical storage regulations in North America and Europe, combined with Red Sea shipping disruptions and feedstock volatility, forced manufacturers to regionalize stabilizer sourcing and increase strategic inventory buffers by nearly 12%.

Asia-Pacific continues to strengthen its role in polymer production, with China accounting for more than 38% of global acrylic monomer capacity and over 45% of downstream packaging-grade polymer exports. The United States remains dominant in specialty stabilizer innovation, supported by large-scale petrochemical investments exceeding USD 30 billion across Gulf Coast facilities and rising demand from EV coatings and semiconductor materials. Compared with conventional inhibitor systems, next-generation phenolic and nitroxide stabilizers improve thermal endurance by nearly 20% and reduce material degradation risks during long-distance transport.

Strategic competition is increasingly shifting toward customized stabilizer formulations, regional supply resilience, and low-toxicity performance optimization, forcing manufacturers to prioritize application-specific innovation over commodity-scale production.

Market Size & Growth: USD 320.0 million in 2025 to USD 510.0 million by 2033, driven by 28% higher demand from advanced polymer processing and specialty coatings.

Top Growth Drivers: EV coatings demand up 31%, high-purity polymer production up 27%, and chemical storage compliance adoption up 22%.

Short-Term Forecast: By 2028, automated inhibitor dosing systems are projected to reduce polymerization losses by 18% and storage downtime by 15%.

Emerging Technologies: AI-enabled process monitoring, nitroxide stabilizers, and continuous-flow polymerization are improving thermal efficiency by over 20%.

Regional Leaders: Asia-Pacific exceeds USD 180 million demand value, North America leads specialty adoption, while Europe accelerates bio-based stabilizer integration by 24%.

Consumer/End-User Trends: More than 42% of specialty polymer producers now prioritize low-toxicity stabilizers for compliance-sensitive applications.

Pilot/Case Example: In 2025, a major Gulf Coast chemical facility improved monomer storage stability by 19% through automated inhibitor optimization deployment.

Competitive Landscape: Top five players control nearly 48% market share, led by SI Group, BASF, Eastman, LANXESS, and Solenis.

Regulatory & ESG Impact: VOC-control policies and REACH compliance initiatives reduced hazardous stabilizer usage by nearly 16% across Europe.

Investment & Funding: Global petrochemical and polymer infrastructure investments surpassed USD 12 billion, accelerating localized stabilizer production partnerships.

Innovation & Future Outlook: High-purity, low-residue stabilizers are redefining advanced semiconductor and biomedical polymer manufacturing strategies worldwide.

The monomer stabilizers market is increasingly shaped by specialty chemicals, packaging polymers, and automotive coatings, which collectively contribute over 65% of total demand. Advanced phenolic stabilizers now improve oxidation resistance by nearly 20%, while automated inhibitor systems reduce material waste by 15%. Asia-Pacific dominates bulk consumption, whereas North America leads premium-grade adoption driven by electronics and EV manufacturing. Growing emphasis on regionalized chemical supply chains and stricter transport safety standards is accelerating investment into customized, low-toxicity stabilizer formulations, positioning innovation and operational resilience as the next competitive frontier.

Monomer stabilizers are becoming strategically critical as polymer manufacturers, specialty chemical producers, and advanced materials suppliers race to secure production continuity, transport stability, and regulatory compliance in increasingly volatile global supply chains. The market is transforming from a commodity-driven chemical segment into a precision-performance industry where storage safety, thermal control, and formulation compatibility directly influence manufacturing uptime and profitability. Rising demand from EV batteries, semiconductor encapsulation, industrial coatings, and medical-grade polymers is accelerating the need for advanced inhibitor systems capable of maintaining monomer integrity across long transport cycles and high-temperature environments.

Global chemical supply chain restructuring and stricter hazardous material regulations are forcing manufacturers to redesign storage and transportation strategies. Advanced nitroxide-based stabilizer technologies improve thermal efficiency by 24% while reducing inhibitor consumption costs by 17% compared to legacy hydroquinone systems. Asia-Pacific leads in production volume with more than 46% of global monomer processing capacity, while North America leads innovation adoption with nearly 35% higher deployment of automated stabilization systems across specialty chemical facilities.

Over the next three years, digital dosing and AI-integrated monitoring platforms are projected to reduce polymerization incidents by 21% and improve storage efficiency by 18%. ESG positioning is becoming a measurable competitive advantage, as low-toxicity stabilizers lower hazardous handling costs by nearly 14% and improve compliance access across European markets. In 2025, a major acrylic monomer producer reported a 16% reduction in product degradation after integrating real-time inhibitor optimization systems into bulk storage terminals.

Leading chemical companies are shifting capital allocation toward specialty-grade stabilizers, regional production hubs, and customized formulations optimized for electronics and high-performance coatings. The competitive pathway is no longer defined by volume alone; it is being reshaped by precision chemistry, operational resilience, and application-specific performance optimization that directly strengthens long-term market positioning.

The Monomer Stabilizers Market is being reshaped by rapid expansion in specialty polymer manufacturing, stricter chemical handling standards, and increasing demand for high-purity monomer storage solutions. Industrial producers are prioritizing stabilizers that extend shelf life, minimize uncontrolled polymerization, and improve transport safety across global supply chains. The market is witnessing rising integration of automated dosing systems and precision inhibitor technologies that improve operational reliability by nearly 20% in large-scale polymer processing environments. Demand concentration remains strongest in packaging, coatings, adhesives, and electronics manufacturing, where production interruptions generate significant operational losses. At the same time, regulatory shifts surrounding VOC emissions, hazardous chemical handling, and low-toxicity additives are redefining supplier strategies and accelerating formulation innovation. Manufacturers are increasingly balancing performance optimization with sustainability compliance, while regional supply diversification and feedstock cost management continue influencing procurement and production decisions globally.

The expansion of high-performance polymer manufacturing is forcing chemical producers to adopt precision stabilization technologies capable of maintaining monomer integrity during extended processing and transportation cycles. Specialty coatings, EV materials, and industrial packaging applications now account for more than 58% of premium stabilizer demand due to their sensitivity to oxidation and thermal degradation. Automated inhibitor dosing systems improve storage efficiency by nearly 18% while reducing polymerization-related waste by 15%, creating measurable operational advantages for large-scale manufacturers. Global petrochemical supply chain restructuring after Red Sea shipping disruptions further accelerated regional inventory expansion and localized production investments across Asia-Pacific and North America. This shift is directly impacting business strategy. Chemical companies are increasing investment into low-residue stabilizers, advanced phenolic inhibitors, and AI-based monitoring platforms to improve reliability and reduce shutdown risks. Major producers are expanding specialty stabilizer capacity, forming technology partnerships, and integrating real-time storage analytics into processing facilities. The market is no longer driven purely by volume demand; it is being accelerated by operational continuity, precision chemistry, and production risk optimization.

The Monomer Stabilizers Market remains heavily exposed to fluctuations in petrochemical feedstock availability, energy pricing, and regulatory compliance costs. Raw material prices for key inhibitor compounds fluctuated by more than 22% between 2024 and 2025, directly impacting production economics and procurement stability. Europe’s tightening chemical safety and VOC compliance standards increased reformulation and testing expenses by nearly 14%, particularly for suppliers dependent on legacy stabilizer chemistries. In addition, supply concentration across limited specialty chemical hubs continues to create sourcing bottlenecks and delivery delays. These structural pressures are constraining scalability and compressing operating margins for mid-sized producers. Transportation disruptions across major maritime trade routes extended average chemical shipment lead times by approximately 11%, forcing manufacturers to increase buffer inventories and working capital exposure. Companies are responding by diversifying supplier networks, securing long-term feedstock contracts, and accelerating development of bio-based or low-toxicity alternatives. Some firms are also regionalizing production to reduce dependence on volatile import channels. Competitive resilience increasingly depends on supply security, compliance agility, and the ability to control formulation costs without compromising stabilization performance.

Rapid adoption of smart manufacturing technologies is creating significant opportunities for advanced monomer stabilizer solutions integrated with predictive analytics and automated process control. AI-enabled inhibitor monitoring systems improve dosing precision by nearly 23% while reducing chemical overuse by approximately 16%, generating measurable cost savings for polymer manufacturers. High-growth sectors such as semiconductor packaging, medical polymers, and EV coatings are increasingly demanding ultra-low contamination stabilizers capable of supporting high-temperature and precision-engineered applications. A major innovation shift is emerging around multifunctional stabilizers that combine oxidation control, thermal resistance, and storage optimization within a single formulation platform. This transition is unlocking new demand pockets in specialty chemicals and high-purity industrial materials. Companies are aggressively expanding R&D pipelines, building regional application laboratories, and partnering with automation providers to strengthen integration capabilities. Asia-Pacific manufacturers are scaling localized production to capture export-driven demand, while North American firms are prioritizing specialty-grade customization. The strongest future advantage will belong to suppliers capable of combining chemistry innovation with digital process optimization and application-specific engineering support.

Maintaining stabilization performance across diverse monomer chemistries, transport conditions, and industrial applications remains a major execution challenge for market participants. Approximately 19% of industrial polymer losses still originate from improper inhibitor calibration, contamination exposure, or thermal instability during bulk storage and shipment. Large-scale processing facilities face increasing pressure to balance aggressive production schedules with stringent safety compliance and precision dosing requirements. Infrastructure limitations in emerging markets further constrain deployment consistency and storage quality standards. At the same time, regulatory fragmentation across regions is complicating product standardization and increasing validation timelines by nearly 13%. High-performance stabilizers often require customized formulations for specific polymer systems, creating scalability challenges and slowing commercialization cycles. Companies are being forced to invest heavily in testing infrastructure, digital monitoring systems, and technical support capabilities to maintain competitive positioning. Strategic partnerships with logistics providers, automation specialists, and downstream polymer manufacturers are becoming essential for improving execution reliability. Long-term competitiveness will depend on solving formulation adaptability, transport resilience, and operational consistency at industrial scale.

35% Rise in Automated Inhibitor Monitoring Deployment Across Polymer Facilities is reshaping operational execution as manufacturers integrate AI-enabled dosing systems to reduce polymerization losses by 18% and storage downtime by 14%. Chemical producers are restructuring plant operations around predictive stabilization analytics, particularly after supply chain disruptions increased the cost of monomer spoilage and transport inefficiencies.

28% Increase in Low-Toxicity Stabilizer Adoption Across Europe and North America is redefining formulation priorities as compliance-driven industries shift away from legacy inhibitor chemistries. Manufacturers are accelerating development of phenolic and nitroxide-based alternatives that improve thermal endurance by nearly 20% while lowering hazardous handling requirements. This transition is forcing suppliers to redesign product portfolios around regulatory alignment and export flexibility.

41% Expansion in Asia-Pacific Localized Production Capacity is shifting the global supply structure as China, South Korea, and India increase regional stabilizer manufacturing to reduce import dependency and improve delivery speed. Producers are optimizing vertically integrated chemical operations and scaling bulk storage infrastructure, enabling faster response cycles and nearly 12% lower regional logistics costs for downstream polymer processors.

22% Growth in Application-Specific Stabilizer Customization is redefining competitive positioning as electronics, EV coatings, and biomedical polymer manufacturers demand precision-engineered inhibitor systems. Companies are forming technical partnerships and expanding application laboratories to accelerate formulation adaptation. A non-obvious shift is emerging where specialty performance and compatibility now outweigh price competition in premium industrial segments.

The Monomer Stabilizers Market is segmented by type, application, and end-user, reflecting the expanding performance requirements across polymer manufacturing, coatings, packaging, and specialty chemical processing industries. Demand remains heavily concentrated in high-efficiency stabilizer formulations used for acrylics, styrene, and vinyl monomers, where storage integrity and thermal resistance directly impact production continuity. More than 48% of overall demand originates from industrial polymer processing applications, while specialty coatings and adhesives continue gaining share due to higher adoption of low-toxicity stabilizers and precision inhibitor systems. Market demand is increasingly shifting toward customized stabilizer solutions designed for advanced materials and long-duration transport environments. Automated polymer production facilities are accelerating adoption of high-purity inhibitor technologies that improve storage efficiency by nearly 18% and reduce degradation-related waste. At the same time, manufacturers are prioritizing application-specific formulations and regional supply flexibility to strengthen operational resilience. Strategic competition is intensifying around premium-grade stabilizers, specialty applications, and compliance-oriented product innovation.

Hydroquinone-based stabilizers continue dominating the Monomer Stabilizers Market with nearly 39% share due to their strong oxidation resistance, cost efficiency, and broad compatibility across acrylic and vinyl monomer applications. Their structural dominance is reinforced by established industrial integration, stable performance in bulk storage systems, and lower operational replacement frequency. However, phenolic stabilizers are emerging as the fastest-growing segment, expanding adoption by nearly 24% as manufacturers prioritize low-toxicity formulations, enhanced thermal endurance, and regulatory-compliant stabilization technologies for specialty polymers and high-purity applications. Nitroxide stabilizers are gaining traction in advanced polymer manufacturing due to superior temperature stability and improved precision in continuous processing environments. Compared with conventional hydroquinone systems, nitroxide technologies improve stabilization consistency by approximately 20% in high-temperature operations. Remaining stabilizer categories, including amine-based and sulfur-based variants, collectively account for nearly 28% of demand and maintain niche relevance in specialty coatings, adhesives, and chemical transport applications requiring customized inhibitor performance. Manufacturers are shifting investment toward premium stabilizer chemistries, application-specific formulations, and automated dosing compatibility. Capacity expansion and R&D spending are increasingly concentrated around low-residue and high-purity solutions, signaling a strategic transition away from commodity-grade stabilizer competition toward specialized industrial performance optimization.

Polymer manufacturing remains the leading application segment with approximately 44% market share, driven by high-volume consumption across acrylics, styrene derivatives, and vinyl compound production. Demand concentration exists because polymer processors require continuous stabilization during storage, transport, and high-temperature processing to prevent uncontrolled polymerization and production losses. Coatings and adhesives applications are rapidly strengthening their market position as manufacturers prioritize longer shelf life, improved formulation stability, and compatibility with low-VOC industrial systems. Electronics and semiconductor materials represent the fastest-growing application segment, with adoption increasing by nearly 26% due to rising demand for high-purity monomer systems used in encapsulation materials, specialty resins, and advanced electronic coatings. Compared with mature packaging-oriented polymer applications, semiconductor-focused applications require significantly higher thermal precision and contamination control. Remaining applications, including industrial packaging and specialty chemical transport, collectively contribute close to 32% of market demand and continue benefiting from stricter chemical handling regulations. Usage patterns are shifting toward customized stabilization systems integrated with automated monitoring platforms and predictive dosing technologies. Companies are repositioning product portfolios around high-value industrial applications, strengthening technical support capabilities, and investing in precision-engineered formulations optimized for electronics, EV materials, and specialty coatings markets.

Chemical manufacturers remain the dominant end-user segment, accounting for nearly 47% of total market demand due to their large-scale dependency on stabilized monomers for polymer synthesis, coatings, adhesives, and specialty material production. Demand concentration is strongest among integrated petrochemical and polymer producers where uninterrupted processing cycles and long-distance monomer transportation require advanced inhibitor performance and storage optimization. These enterprises prioritize stabilizers capable of reducing operational losses and maintaining production reliability under fluctuating thermal conditions.Electronics and advanced materials manufacturers are emerging as the fastest-growing end-user group, with adoption increasing by approximately 25% as semiconductor packaging, EV components, and precision coatings demand ultra-high-purity monomer stabilization systems. Compared with traditional industrial chemical users focused on scale and cost efficiency, electronics-focused buyers prioritize contamination control, low-residue formulations, and automated stabilization integration. Remaining end-users, including packaging, construction materials, and industrial coatings producers, collectively contribute nearly 34% of overall demand while increasingly shifting toward compliance-driven and sustainability-oriented purchasing strategies.Companies are responding through customized pricing models, application-specific formulations, and strategic partnerships with downstream manufacturers. Producers are also expanding regional technical support and localized supply networks to capture demand from high-growth specialty chemical and electronics segments where reliability and precision increasingly outweigh commodity pricing advantages.

Asia-Pacific accounted for the largest market share at 41% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2026 and 2033.

Asia-Pacific leads global monomer stabilizer demand due to large-scale polymer production capacity, integrated petrochemical infrastructure, and rapidly expanding specialty chemical exports from China, South Korea, and India. North America accounts for nearly 27% of market demand and leads in advanced stabilization technologies, automated inhibitor systems, and specialty polymer applications linked to EV materials and semiconductor manufacturing. Europe contributes approximately 21% share, driven by regulatory-led demand for low-toxicity and REACH-compliant stabilizer formulations. Meanwhile, Middle East & Africa and South America are witnessing rising adoption through infrastructure expansion and downstream chemical investments. Global supply chain regionalization and tightening chemical transport regulations are forcing manufacturers to diversify production hubs, accelerate localized sourcing strategies, and prioritize high-performance specialty stabilizers across growth-intensive industrial regions.

North America holds nearly 27% of the global Monomer Stabilizers Market, supported by strong demand from specialty polymers, EV coatings, semiconductor materials, and industrial packaging applications. The United States dominates regional consumption due to large-scale petrochemical processing infrastructure and rising investment in advanced chemical storage technologies. Regulatory pressure around hazardous material handling and VOC emissions is accelerating adoption of low-toxicity stabilizer systems, with advanced phenolic formulations witnessing more than 22% growth in specialty applications. Manufacturers are integrating AI-enabled inhibitor monitoring systems that improve storage efficiency by approximately 18% while reducing material degradation risks. Gulf Coast petrochemical investments and localized supply chain strategies continue strengthening regional production capabilities. Enterprise buyers increasingly prioritize reliability, precision stabilization, and compliance-driven formulations over low-cost commodity solutions, positioning North America as a critical innovation and premium-value expansion region.

Europe accounts for nearly 21% of global Monomer Stabilizers Market demand, led by Germany, France, and the Netherlands where advanced polymer processing and specialty coatings industries remain highly concentrated. REACH regulations and aggressive VOC reduction policies are reshaping stabilizer selection strategies, accelerating adoption of low-residue and environmentally compliant formulations. More than 31% of regional chemical manufacturers have shifted toward advanced phenolic and nitroxide stabilizers to strengthen compliance readiness and export competitiveness. Operational transformation is increasingly focused on automated dosing precision and waste reduction, improving material efficiency by nearly 15% across specialty chemical facilities. European buyers demonstrate strong quality-first and compliance-driven purchasing behavior, prioritizing long-term performance stability over pricing advantages. Manufacturers are expanding sustainable formulation portfolios and strengthening regional R&D capabilities, making Europe a decisive market for regulatory-driven innovation and next-generation stabilizer development.

Asia-Pacific commands approximately 41% of global Monomer Stabilizers Market demand and remains the largest production and consumption hub globally. China leads regional dominance through extensive acrylic, vinyl, and styrene monomer manufacturing capacity, while India and South Korea continue expanding specialty polymer and electronics material production. Integrated petrochemical supply chains and lower operational costs provide the region with nearly 20% faster production scalability compared with Western markets. Localized stabilizer manufacturing and vertically integrated chemical operations are accelerating rapidly, reducing regional logistics costs by approximately 12%. Producers are expanding automated processing systems and export-focused specialty chemical facilities to strengthen global competitiveness. Enterprise buyers prioritize cost efficiency, production speed, and secure regional supply access, driving continuous investment into bulk stabilization technologies and customized industrial formulations. Asia-Pacific remains strategically critical for manufacturers seeking production scale, export leverage, and downstream polymer demand expansion.

South America contributes nearly 4% of global Monomer Stabilizers Market demand, with Brazil and Argentina leading consumption through expanding packaging, construction materials, and industrial coatings industries. Regional demand is supported by increasing polymer processing activity and rising investment in localized chemical manufacturing. However, infrastructure limitations and dependence on imported specialty chemicals continue constraining supply stability and cost competitiveness across several markets. Industrial buyers remain highly price-sensitive, with nearly 38% prioritizing cost-efficient stabilization systems over premium formulations. At the same time, localized demand for safer and longer-lasting monomer storage solutions is accelerating among medium-scale polymer producers. Companies are strengthening distributor partnerships and regional warehousing capabilities to reduce delivery delays and improve market penetration. South America presents a balanced opportunity-risk profile where long-term expansion potential exists, but operational resilience and pricing adaptability remain critical competitive factors.

Middle East & Africa accounts for approximately 7% of global Monomer Stabilizers Market demand, supported primarily by petrochemical expansion, infrastructure modernization, and downstream industrial diversification initiatives. Saudi Arabia and the UAE remain central growth markets due to large-scale refinery integration and increasing specialty chemical investments linked to industrial development programs. Construction materials and industrial coatings applications continue generating strong stabilizer demand across regional manufacturing sectors. Strategic partnerships and petrochemical modernization projects are accelerating adoption of advanced stabilization technologies, with automated processing integration improving storage efficiency by nearly 14%. Regional enterprises increasingly favor scalable, high-durability stabilizers optimized for extreme temperature environments and long-distance chemical transport. Governments and industrial groups are prioritizing downstream chemical value-chain expansion, positioning the region as an emerging strategic hub for industrial polymer and specialty chemical development.

China – 34% Market share: driven by massive polymer production capacity, integrated petrochemical infrastructure, and dominant export-oriented specialty chemical manufacturing.

United States – 22% Market share: supported by advanced specialty polymer demand, high adoption of automated stabilization technologies, and strong investment in premium chemical processing facilities.

The Monomer Stabilizers Market is characterized by intense competition between global specialty chemical leaders, regional formulation suppliers, and technology-focused stabilizer innovators. Major companies including BASF, SI Group, Eastman Chemical, LANXESS, and Solenis compete aggressively across premium stabilization technologies, supply reliability, and application-specific formulation capabilities. The top five players collectively account for nearly 48% of global market share, with dominance strongest in high-purity polymer processing and specialty industrial applications.

Competition is increasingly shifting beyond pricing toward performance optimization, thermal stability precision, and compliance-driven product differentiation. Advanced stabilizer systems improve storage efficiency by nearly 18% while reducing polymer degradation risks by approximately 15%, forcing suppliers to accelerate R&D and automated processing integration. Global leaders are expanding production capacity, strengthening regional supply chains, and pursuing vertical integration strategies to secure feedstock access and improve delivery reliability.

A major competitive shift is emerging around low-toxicity and customized stabilizer technologies designed for electronics, EV materials, and semiconductor applications. High technical validation requirements and regulatory compliance complexity continue creating strong entry barriers. Winning in this market increasingly depends on precision chemistry expertise, localized production resilience, and the ability to deliver application-engineered stabilization solutions at industrial scale.

Eastman Chemical Company

LANXESS

SI Group

Solenis

Clariant

ADEKA Corporation

Songwon Industrial Co., Ltd.

PMC Group

Everspring Chemical Co., Ltd.

Arkema

Akzo Nobel N.V.

Dorf Ketal

Nouryon

Advanced stabilization chemistry is rapidly transforming the Monomer Stabilizers Market as manufacturers shift from conventional inhibitor systems toward precision-engineered, low-residue formulations optimized for high-performance polymers and specialty chemical processing. Automated inhibitor dosing systems integrated with AI-based monitoring platforms are improving storage accuracy by nearly 23% while reducing polymerization-related material loss by approximately 17%. Adoption of real-time monitoring technologies has crossed 36% among large-scale specialty polymer facilities, particularly in North America and Asia-Pacific.

Nitroxide-based stabilizers and advanced phenolic formulations are emerging as key disruptive technologies due to their superior thermal endurance and extended monomer storage capabilities. Compared with traditional hydroquinone systems, advanced nitroxide technologies improve stabilization consistency by nearly 20% and reduce inhibitor consumption costs by approximately 14%. These technologies are becoming increasingly critical in semiconductor materials, EV coatings, and medical-grade polymer manufacturing where contamination control and thermal precision directly impact product performance.

Integration trends are increasingly centered around predictive process analytics, automated chemical handling, and digitalized storage optimization systems. Large petrochemical operators and specialty chemical manufacturers benefit most from these upgrades due to their high-volume transport and continuous processing requirements. Between 2026 and 2028, next-generation smart stabilization platforms are expected to accelerate operational automation, improve supply chain resilience, and strengthen compliance efficiency across global polymer manufacturing networks. Companies investing early in digital stabilization ecosystems and customized inhibitor technologies are positioning themselves for stronger competitive differentiation and long-term industrial scalability.

February 2026 – BASF partnered with Xfloat to integrate Tinuvin® 2730 ED light stabilizer technology into floating solar systems, extending HDPE structural durability beyond 30 years under harsh outdoor exposure conditions. The collaboration strengthened BASF’s position in advanced polymer stabilization for renewable infrastructure applications. [Solar Durability] Source: www.basf.com

October 2025 – BASF launched Tinuvin® NOR® 600, a next-generation NOR-HALS stabilizer designed for PVC and polyolefin applications requiring enhanced UV and heat resistance. The innovation improved weatherability performance and optimized low-dust handling for converters and masterbatch producers, supporting long-life plastics manufacturing. [UV Protection]

September 2025 – LANXESS expanded its Stabaxol hydrolysis stabilizer portfolio with low-emission carbodiimide technologies including Stabaxol L and Stabaxol P LF. The products improved hydrolysis resistance and thermal stability for TPU, PET monofilaments, cable sheathing, and engineering plastics while supporting low-emission processing requirements. [Hydrolysis Shift]

September 2025 – LANXESS announced expansion of rubber additives and processing promoter production at its South Carolina facility, with new U.S. output scheduled for November 2025. The move strengthened domestic supply reliability and reduced import dependence for automotive, pharmaceutical, and industrial rubber applications. [Supply Localization]

The Monomer Stabilizers Market Report delivers comprehensive coverage across stabilizer types, industrial applications, end-user industries, regional demand structures, and evolving technology trends influencing specialty chemical and polymer manufacturing ecosystems. The study evaluates key stabilizer categories including hydroquinone-based, phenolic, nitroxide, and specialty inhibitor formulations used across polymer processing, coatings, adhesives, packaging, electronics, and advanced materials manufacturing. Geographic analysis spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, capturing both mature industrial markets and high-growth production hubs.

The report provides deep analytical insight into more than 20 strategic market variables including demand concentration patterns, technology adoption rates, supply chain restructuring trends, regulatory impacts, and competitive positioning strategies. Over 48% of industry demand concentration across polymer manufacturing and specialty chemical processing is evaluated alongside regional adoption shifts, operational efficiency metrics, and evolving customer procurement behavior. The analysis also assesses automation integration, AI-enabled stabilization systems, and low-toxicity inhibitor technologies reshaping industrial performance benchmarks.

From a strategic perspective, the report supports investment prioritization, production expansion planning, supply chain optimization, and competitive benchmarking decisions for manufacturers, distributors, investors, and industrial chemical stakeholders. It further highlights emerging specialty applications and future-facing technology pathways expected to redefine operational competitiveness and regional market leadership between 2026 and 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 320.0 Million |

| Market Revenue (2033) | USD 510.0 Million |

| CAGR (2026–2033) | 6.0% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | BASF; Eastman Chemical Company; LANXESS; SI Group; Solenis; Clariant; ADEKA Corporation; Songwon Industrial Co., Ltd.; PMC Group; Everspring Chemical Co., Ltd.; Arkema; Akzo Nobel N.V.; Dorf Ketal; Nouryon |

| Customization & Pricing | Available on Request (10% Customization Free) |