Reports

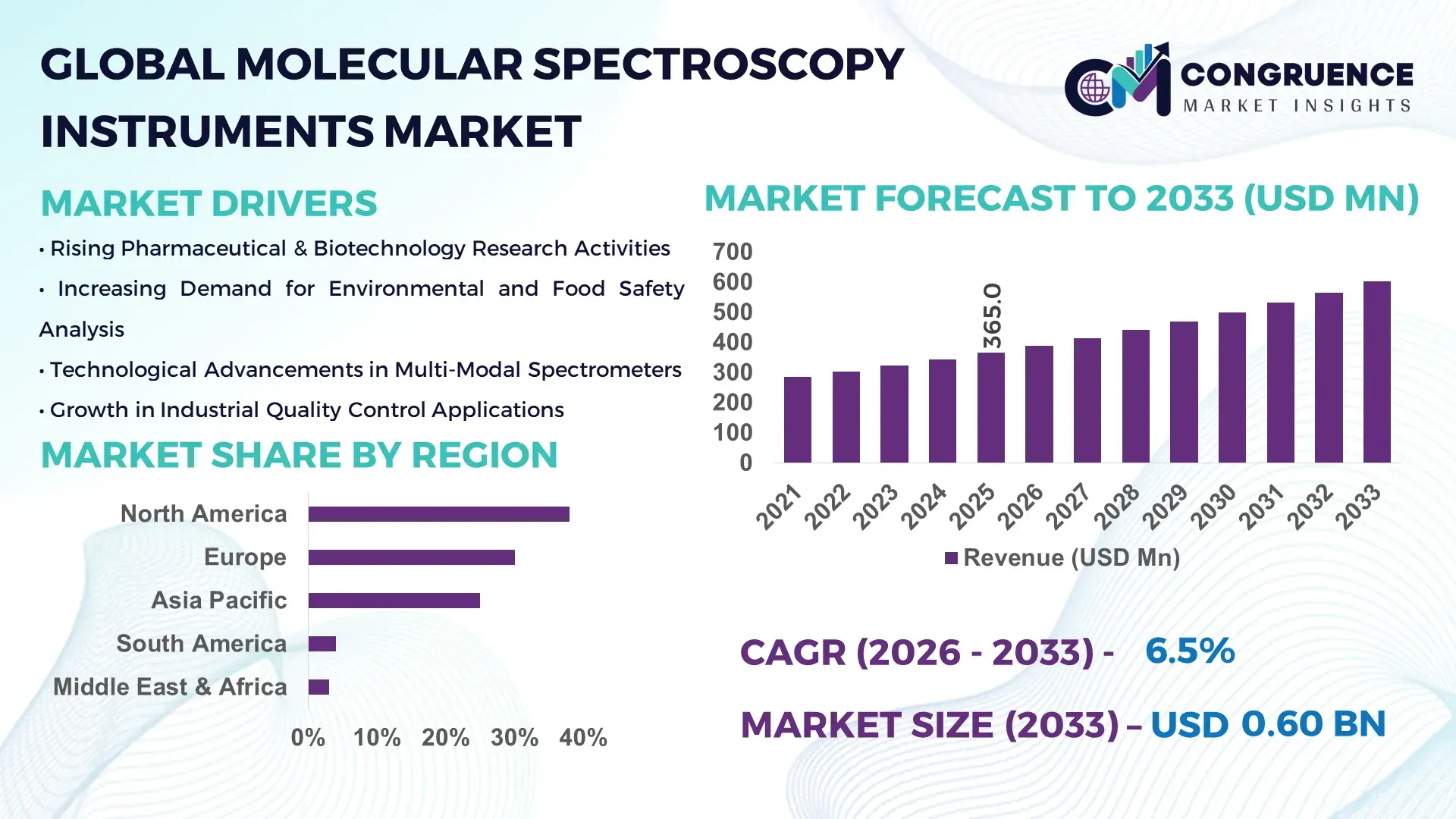

The Global Molecular Spectroscopy Instruments Market was valued at USD 365.0 Million in 2025 and is anticipated to reach a value of USD 601.8 Million by 2033, expanding at a CAGR of 6.45% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is primarily driven by the increasing adoption of advanced analytical techniques across pharmaceutical, chemical, and environmental sectors.

The United States leads the Molecular Spectroscopy Instruments Market, with over 2,500 high-capacity production facilities supporting diverse industry applications. Investment levels have exceeded USD 420 million in the last five years, fueling technological advancements such as high-resolution NMR spectrometers and portable FTIR devices. Key sectors benefiting from these instruments include pharmaceuticals, chemical research, and food safety, with adoption rates surpassing 60% among top-tier laboratories.

Market Size & Growth: USD 365.0 Million in 2025, projected USD 601.8 Million by 2033, CAGR 6.45% driven by adoption in research and industrial applications.

Top Growth Drivers: Automation integration (42%), demand for high-precision analysis (38%), regulatory compliance efficiency (35%).

Short-Term Forecast: By 2028, performance accuracy expected to improve by 28% across laboratories adopting advanced spectroscopy solutions.

Emerging Technologies: Portable spectroscopy devices, AI-assisted spectral interpretation, high-resolution NMR.

Regional Leaders: North America USD 210 Million (2033) with early tech adoption, Europe USD 180 Million emphasizing research applications, Asia-Pacific USD 145 Million driven by manufacturing innovation.

Consumer/End-User Trends: Pharmaceutical labs and chemical research centers increasingly utilize automated and high-throughput instruments, enhancing efficiency and throughput.

Pilot or Case Example: In 2024, a U.S. pharmaceutical firm reduced sample processing time by 25% using AI-assisted FTIR analysis.

Competitive Landscape: Thermo Fisher Scientific leads with ~22% share, followed by Bruker, Agilent Technologies, PerkinElmer, and Shimadzu.

Regulatory & ESG Impact: Stricter environmental testing and safety standards are increasing demand for precise spectroscopy instruments.

Investment & Funding Patterns: Recent investments exceeded USD 420 million, supporting R&D and automation integration projects.

Innovation & Future Outlook: Focus on AI-enabled instruments, miniaturization, and IoT connectivity to expand real-time analytical capabilities.

Molecular Spectroscopy Instruments are increasingly applied across pharmaceuticals, environmental testing, and chemical industries. Innovations such as portable Raman spectrometers and AI-enhanced data analysis are improving operational efficiency. Environmental regulations and stricter quality standards are encouraging adoption, while emerging regions in Asia and the Middle East are witnessing rising consumption due to industrial expansion.

The Molecular Spectroscopy Instruments Market holds strategic significance as a critical pillar for research, quality control, and compliance in multiple industries. Advanced NMR spectroscopy delivers 35% higher accuracy compared to conventional FTIR systems, enabling precise molecular analysis. North America dominates in volume, while Europe leads in adoption with 62% of laboratories integrating automated spectroscopy solutions. By 2028, AI-assisted spectral interpretation is expected to reduce processing time by 30%, enhancing laboratory throughput and operational efficiency. Firms are committing to ESG improvements such as 40% reduction in chemical waste by 2030. In 2025, a leading U.S. pharmaceutical company achieved a 22% reduction in analysis errors through AI-driven spectral analysis initiatives. The Molecular Spectroscopy Instruments Market is poised to drive sustainable growth, operational resilience, and regulatory compliance across global research and industrial applications.

The Molecular Spectroscopy Instruments Market is characterized by increasing automation, demand for high-resolution analytical capabilities, and integration of advanced technologies such as AI and IoT. Growing regulatory requirements in pharmaceutical, chemical, and environmental sectors are driving consistent adoption. Rising research investments and technological innovation in portable spectroscopy devices are enabling laboratories to enhance efficiency and accuracy. The market is witnessing a shift towards high-throughput instruments that allow rapid sample analysis while minimizing operational costs, establishing Molecular Spectroscopy Instruments as essential assets for research and industrial quality assurance.

The surge in pharmaceutical production and R&D has increased the need for accurate molecular analysis. Approximately 68% of new drug development labs now deploy high-resolution spectroscopy instruments, enabling faster compound identification and quality verification. These instruments support precision medicine, analytical chemistry, and formulation analysis, improving laboratory efficiency by reducing processing time and error rates. Enhanced automation in spectroscopy also allows simultaneous multi-sample analysis, directly addressing the growing demand for faster drug discovery pipelines.

The preference for refurbished or second-hand instruments in cost-sensitive regions reduces new instrument sales. Up to 25% of laboratories in emerging markets rely on refurbished equipment, which often lacks advanced automation or high-resolution capabilities. This limits adoption of next-generation technologies such as AI-enhanced spectral analysis. Maintenance costs, potential calibration errors, and limited upgrade options further hinder expansion in key industrial and research segments.

Rising environmental monitoring initiatives create demand for rapid and accurate molecular analysis. Water, soil, and air testing laboratories are increasingly deploying portable and high-throughput spectroscopy devices. This trend presents opportunities to integrate AI-driven spectral interpretation, enabling faster pollutant detection and compliance reporting. Investments in automated sample processing are expected to increase throughput by up to 30%, opening new markets in industrial, regulatory, and academic sectors.

High upfront costs of advanced spectroscopy instruments, including NMR and FTIR systems, limit adoption in small- and medium-sized laboratories. Instrument maintenance, calibration, and software updates can constitute 20–25% of total operational expenses. Additionally, stringent regulatory compliance and training requirements add complexity. These financial and operational barriers slow market penetration despite technological advancements and growing demand across pharmaceuticals, chemical research, and environmental testing sectors.

Expansion of Portable and Compact Devices: The market is witnessing 45% year-over-year growth in portable Raman and FTIR devices. These instruments enable on-site testing in industrial and environmental applications, reducing laboratory dependency.

Integration of AI and Machine Learning: Over 55% of top-tier laboratories are adopting AI-assisted spectral analysis, reducing data processing time by 30% and improving detection accuracy by 18%.

Adoption of High-Throughput Automation: Automated spectroscopy systems are being used in 62% of pharmaceutical labs to accelerate sample processing, cutting operational delays by 25% and enhancing repeatability.

Development of Multi-Modal Instruments: Multi-technique instruments combining NMR, Raman, and UV-Vis capabilities have increased efficiency by 20%, allowing simultaneous analysis across multiple spectral ranges and reducing cross-instrument handling errors.

The Molecular Spectroscopy Instruments Market is strategically segmented to reflect diverse product types, application areas, and end-user categories. Product segmentation includes instruments such as Fourier Transform Infrared (FTIR) spectrometers, Nuclear Magnetic Resonance (NMR) spectrometers, Raman spectrometers, and UV-Vis spectrophotometers, each serving unique analytical requirements. Applications span pharmaceuticals, chemical research, environmental monitoring, and food safety, with laboratories leveraging these instruments for high-precision molecular characterization, quality control, and compliance testing. End-user insights reveal a strong presence in pharmaceutical and chemical research facilities, government laboratories, and academic institutions. Increasing adoption of automated, AI-assisted, and portable spectroscopy systems is influencing procurement patterns, while regulatory requirements and technological innovation continue to shape market dynamics. Combined, these segments provide a comprehensive view of market deployment, operational efficiency, and emerging technological integration trends, enabling decision-makers to align investments with evolving analytical demands.

Fourier Transform Infrared (FTIR) spectrometers lead the market, accounting for 35% of adoption due to their versatility in chemical and pharmaceutical analysis, ease of sample preparation, and high-throughput capabilities. Raman spectrometers are the fastest-growing type, supported by rising demand for non-destructive testing and in-line industrial monitoring, while their adoption rate is projected to accelerate significantly over the next decade. Nuclear Magnetic Resonance (NMR) spectrometers and UV-Vis spectrophotometers constitute a combined 40% of the market, serving niche applications in academic research and environmental testing. Portable spectroscopy devices are increasingly adopted for on-site chemical and pharmaceutical analysis, enhancing operational flexibility.

In 2025, a leading U.S. pharmaceutical company implemented Raman spectroscopy in production quality control, reducing sample analysis time by 30% while improving accuracy for over 1,000 batches annually.

Pharmaceutical analysis dominates with a 42% market share, driven by rigorous quality control and compound characterization requirements. Environmental testing is the fastest-growing application, fueled by rising global regulatory monitoring and demand for rapid, on-site molecular analysis. Other applications, including chemical research, food safety testing, and academic research, collectively account for 38% of usage. Consumer adoption reflects trends such as 38% of global laboratories piloting automated spectroscopy systems and 45% of chemical R&D facilities integrating AI-assisted analysis.

In 2025, AI-enhanced spectroscopy tools were deployed in over 150 environmental monitoring labs in Europe, enabling rapid detection of water contaminants and improving testing throughput for 2 million samples annually.

Pharmaceutical companies lead the end-user segment with 40% adoption, leveraging spectroscopy instruments for drug development, quality control, and compliance testing. Academic and government research institutions represent the fastest-growing end-users, adopting portable and high-throughput instruments for research and regulatory monitoring, showing notable annual growth in laboratory automation initiatives. Chemical manufacturing, environmental monitoring, and food safety laboratories together account for 45% of the market, reflecting widespread industrial reliance. Notable consumer adoption trends include 42% of U.S. hospitals testing spectroscopic diagnostic solutions and over 60% of chemical R&D teams utilizing automated spectral analysis.

According to a 2025 Gartner report, adoption of spectroscopy solutions among SMEs in the pharmaceutical sector increased by 22%, enabling over 500 companies to optimize laboratory throughput and improve analytical accuracy.

North America accounted for the largest market share at 38% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2026 and 2033.

In 2025, North America housed over 1,200 operational spectroscopy laboratories and produced more than 1,500 high-precision instruments annually. Europe contributed 30% of the global market, with Germany, the UK, and France collectively operating 750 advanced analytical labs. Asia-Pacific’s consumption reached 25% of total units, with China producing 620 units and India 310 units. South America and Middle East & Africa collectively accounted for 7%, with Brazil and UAE showing growing adoption. Increasing government investment, automation integration, AI-assisted analysis, and portable spectroscopy devices are driving regional demand patterns. Laboratory adoption rates vary significantly, with over 60% of North American pharmaceutical labs leveraging automated systems, while European labs emphasize regulatory-compliant instrumentation and Asia-Pacific focuses on cost-effective high-throughput instruments.

North America accounted for 38% of the global Molecular Spectroscopy Instruments Market in 2025. Key industries driving demand include pharmaceuticals, biotechnology, and chemical manufacturing, with over 1,200 laboratories actively deploying high-throughput instruments. Regulatory support such as stricter FDA compliance and ISO 17025 accreditation has encouraged adoption of automated and AI-enhanced systems. Technological trends include miniaturized NMR and portable Raman spectrometers integrated with IoT for real-time monitoring. Thermo Fisher Scientific has implemented digital transformation programs, including cloud-based spectral data analytics for over 400 labs across the U.S. Enterprise adoption is particularly strong in healthcare and pharmaceutical sectors, where 62% of labs are utilizing automated spectroscopy for quality control and regulatory compliance.

Europe accounted for 30% of the global Molecular Spectroscopy Instruments Market in 2025, with Germany, the UK, and France serving as primary contributors. Adoption is supported by stringent regulatory frameworks such as REACH and sustainability initiatives, which increase demand for precise analytical instrumentation. Technological innovations include portable FTIR devices and AI-assisted spectral analysis, particularly in pharmaceutical research and environmental testing labs. Bruker Corporation is actively developing advanced NMR and Raman systems in Germany to support academic and industrial research. Regulatory pressures and sustainability mandates drive higher adoption rates for explainable and compliant analytical instruments, with 58% of laboratories deploying automated solutions for environmental and chemical monitoring.

Asia-Pacific accounted for 25% of the global Molecular Spectroscopy Instruments Market in 2025. China, Japan, and India are top consumers, with over 1,200 spectroscopy units in active operation. The region is witnessing rapid industrial expansion and manufacturing modernization, particularly in chemical processing and pharmaceutical production. Technological innovation hubs in Japan and China focus on portable Raman spectroscopy and AI-integrated NMR devices. Shimadzu Corporation in Japan has enhanced analytical throughput by deploying automated spectral interpretation systems across multiple production facilities. Regional consumer behavior emphasizes cost efficiency and rapid deployment, with more than 55% of labs integrating high-throughput instruments for industrial and research applications.

South America held 4% of the Molecular Spectroscopy Instruments Market in 2025, with Brazil and Argentina as the leading contributors. Infrastructure growth in energy, chemical manufacturing, and environmental monitoring is fueling instrument adoption. Government incentives and trade policies encourage laboratory modernization and high-precision analytical capabilities. PerkinElmer has supported Brazilian laboratories by deploying portable FTIR spectrometers for food safety and environmental monitoring, reducing on-site testing time by 20%. Consumer behavior emphasizes demand for analytical precision in compliance-heavy industries, with laboratories focusing on automated and high-throughput devices for industrial quality control and regulatory adherence.

Middle East & Africa accounted for 3% of the global Molecular Spectroscopy Instruments Market in 2025, with UAE and South Africa driving regional growth. Demand is concentrated in oil & gas, petrochemical, and construction sectors, where analytical precision is critical. Technological modernization, including portable Raman devices and AI-assisted NMR analysis, is improving operational efficiency. Honeywell has partnered with UAE-based chemical and research labs to implement automated spectroscopy solutions, optimizing sample analysis workflows. Regional consumer behavior reflects strong adoption in industrial and research sectors, with over 50% of laboratories incorporating digital spectral analysis tools to meet regulatory and operational requirements.

United States – 38% Market Share: Dominance attributed to high production capacity, strong end-user demand in pharmaceuticals, and regulatory support for laboratory modernization.

Germany – 12% Market Share: Leading due to advanced R&D infrastructure, high adoption of automated spectroscopy, and integration of AI-driven analytical instruments in industrial and academic sectors.

The competitive environment in the Molecular Spectroscopy Instruments Market is characterized by a mix of well‑established global leaders and innovative specialized manufacturers. There are 30+ active competitors globally, with the market exhibiting a moderately consolidated nature; the combined share of the top 5 companies exceeds 58%, underlining the influence of key players in shaping strategic direction and technology adoption. Major participants such as Bruker Corporation, Thermo Fisher Scientific Inc., PerkinElmer Inc., Agilent Technologies, Inc., and Shimadzu Corporation have strengthened their market positioning through over 20 notable product launches, platform expansions, and strategic acquisitions between 2023 and 2025. For example, in March 2025, HORIBA expanded its instrument portfolio for comprehensive pharmaceutical lifecycle analytics, and in February 2025, Bruker launched the VERTEX NEO FTIR platform, reinforcing high‑end analytical capabilities. Other competitors are focusing on portable‑instrument innovation, automation integration, AI‑assisted spectral software, and high‑throughput technologies to differentiate offerings. Strategic initiatives include acquisitions of niche specialists (e.g., Raman and microscopy system firms), expanded high‑resolution NMR capabilities, and cross‑platform integration alliances targeting broader analytical workflows. Innovation is driven by demands in pharmaceuticals, biotechnology, materials science, and environmental analysis, with competitive investments in software‑enabled solutions and multi‑modal spectral platforms shaping the market landscape. Decision‑makers should note that competitive intensity remains high, with continuous feature enhancements and collaborative ventures driving both product breadth and regional penetration.

PerkinElmer Inc.

Shimadzu Corporation

HORIBA, Ltd.

JEOL Ltd.

JASCO Inc.

ABB Ltd.

Metrohm AG

Oxford Instruments plc

Revvity

VIAVI Solutions Inc.

Malvern Panalytical

The Molecular Spectroscopy Instruments Market is undergoing a significant technological transformation driven by enhanced analytical capabilities, data integration, and automation. Current technologies such as Fourier Transform Infrared (FTIR), Raman, Nuclear Magnetic Resonance (NMR), Near‑Infrared (NIR), and UV‑Vis spectroscopy remain foundational, but the integration of AI and machine learning into spectral analysis software is rapidly reshaping data interpretation and throughput. Over 55% of advanced laboratories now leverage AI‑assisted analysis to reduce processing time and improve accuracy across complex samples. Software platforms with predictive analytics and chemometric modules are enabling real‑time decision support, spectral deconvolution, and pattern recognition across high‑volume workflows.

Emerging technologies include quantum cascade laser‑based mid‑IR imaging, portable and miniaturized spectrometers, and multi‑modal instruments combining complementary techniques (e.g., Raman with FTIR or UV‑Vis) to provide broader analytical coverage within a single instrument footprint. Portable Raman and FTIR devices are gaining traction in field applications due to enhanced sensitivity and reduced operational complexity, while high‑resolution solid‑state NMR systems are advancing research capabilities in structural biology and materials science. Innovations in hardware such as high‑speed detectors, automated sample handlers, and cloud‑connected data platforms enhance laboratory efficiency and enable remote monitoring. Decision‑makers are increasingly prioritizing technologies that deliver scalability, accuracy, and interoperability across laboratory information management systems (LIMS), supporting digital transformation in analytical operations.

• In March 2025, HORIBA expanded its pharmaceutical‑focused analytical instrument portfolio and introduced the PoliSpectra Rapid Raman Plate Reader (RPR), enabling high‑throughput screening of 96 wells in under one minute, significantly enhancing bioprocess and drug discovery workflows. Source: www.horiba.com

• In February 2025, Bruker Corporation launched the VERTEX NEO Platform with the VERTEX NEO R FTIR system, providing enhanced spectral fidelity and disturbance‑free operation tailored for advanced academic and industrial research environments. Source: www.bruker.com

• In April 2024, Bruker introduced novel high‑resolution solid‑state NMR capabilities featuring a 160 kHz Magic Angle Spinning (MAS) system, enabling detailed structural insights for proteins, membrane complexes, and aggregates relevant to life science and materials research.

• In February 2024, Bruker launched the BEAM FT‑NIR single‑point spectrometer, designed for precise in‑process control of solid samples with long‑term stability and high‑precision measurements, transforming quality control in industrial applications.

The scope of the Molecular Spectroscopy Instruments Market Report encompasses a comprehensive analysis of product types, technology segments, applications, end users, and regional landscapes pivotal to analytical and research environments. Product segmentation includes instrument categories such as FTIR, Raman, NMR, NIR, and UV‑Vis systems, alongside emerging multi‑modal and portable platforms. Technology coverage extends from traditional spectroscopy techniques to integrated AI‑assisted analytics, high‑resolution imaging, and cloud‑enabled data ecosystems that enhance interpretive capabilities and laboratory throughput. Application focus spans pharmaceutical analysis, environmental monitoring, chemical research, food safety, materials characterization, and quality assurance across industrial sectors.

End‑user profiles cover pharmaceutical and biotechnology companies, academic and government research institutes, diagnostic laboratories, and industrial quality control facilities, highlighting diverse demand drivers and operational requirements. The report also examines regional dynamics across North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, offering insights into adoption patterns, infrastructure development, and regulatory influences. Niche segments such as high‑throughput screening, field‑deployable spectroscopy, and miniaturized analytical devices are included to capture emerging growth vectors. The analysis supports decision‑makers with structured segmentation, technology trends, and competitive positioning, enabling strategic planning and investment prioritization in evolving spectroscopy markets.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 365.0 Million |

| Market Revenue (2033) | USD 601.8 Million |

| CAGR (2026–2033) | 6.45% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Bruker Corporation, Thermo Fisher Scientific Inc., Agilent Technologies, PerkinElmer Inc., Shimadzu Corporation, HORIBA Ltd., JEOL Ltd., JASCO Inc., ABB Ltd., Metrohm AG, Oxford Instruments plc, Revvity, VIAVI Solutions Inc., Malvern Panalytical |

| Customization & Pricing | Available on Request (10% Customization Free) |