Reports

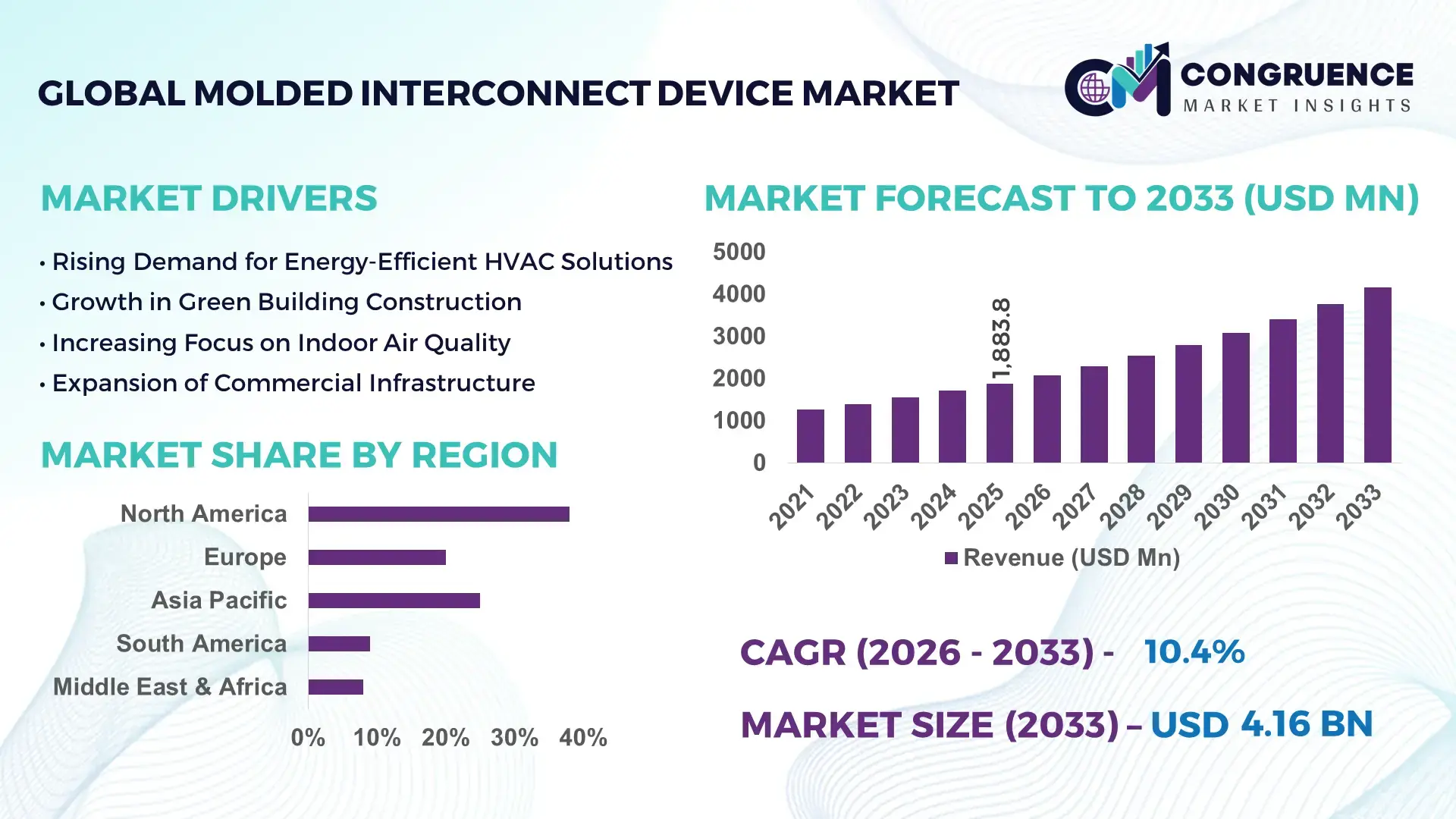

The Global Molded Interconnect Device Market was valued at USD 1883.8 Million in 2025 and is anticipated to reach a value of USD 4157.07 Million by 2033 expanding at a CAGR of 10.4% between 2026 and 2033. This growth is primarily driven by the rising integration of electronic components into compact and lightweight devices across automotive, healthcare, and consumer electronics sectors.

Germany stands out as a dominant country in the Molded Interconnect Device market due to its advanced manufacturing infrastructure and strong automotive electronics ecosystem. The country produces over 30% of Europe’s automotive electronics components, with MID technology increasingly embedded in sensors, control units, and lighting systems. Investments exceeding USD 500 million annually in precision engineering and additive manufacturing have accelerated MID production capabilities. Approximately 65% of German Tier-1 automotive suppliers have integrated MID solutions into next-generation electric vehicle platforms. Additionally, industrial automation adoption in Germany exceeds 70% across manufacturing plants, further driving demand for compact circuit integration technologies like MID.

Market Size & Growth: USD 1883.8 Million (2025) to USD 4157.07 Million (2033), CAGR 10.4%, driven by miniaturization and multi-functional integration demand.

Top Growth Drivers: 45% increase in automotive electronics adoption, 38% rise in compact consumer devices, 30% efficiency improvement in circuit integration.

Short-Term Forecast: By 2028, manufacturing efficiency is expected to improve by 25% due to automation and laser structuring technologies.

Emerging Technologies: Laser Direct Structuring (LDS), 3D printing integration, advanced polymer substrates.

Regional Leaders: Europe projected at USD 1400 Million by 2033 with strong automotive adoption; Asia-Pacific at USD 1700 Million driven by electronics manufacturing hubs; North America at USD 900 Million with aerospace integration trends.

Consumer/End-User Trends: Automotive OEMs and medical device manufacturers account for over 60% of total MID usage due to demand for lightweight and compact circuitry.

Pilot or Case Example: In 2024, a European automotive supplier achieved 20% weight reduction and 15% cost savings using MID-based sensor modules.

Competitive Landscape: Market leader holds approximately 18% share, followed by key players including leading electronics component manufacturers and precision engineering firms.

Regulatory & ESG Impact: Increasing focus on recyclable polymers and reduction of electronic waste by up to 25% by 2030.

Investment & Funding Patterns: Over USD 1 billion invested globally in advanced manufacturing and MID-related R&D between 2023–2025.

Innovation & Future Outlook: Integration of IoT-enabled components and hybrid manufacturing techniques is shaping next-generation MID applications.

The Molded Interconnect Device market is witnessing strong cross-industry integration, particularly in automotive electronics (accounting for nearly 40% of applications), healthcare devices (around 20%), and consumer electronics (over 25%). Technological innovations such as laser direct structuring and high-performance thermoplastics are enabling complex 3D circuit designs with improved durability and conductivity. Regulatory frameworks emphasizing sustainability are pushing manufacturers toward recyclable materials and energy-efficient production processes. Asia-Pacific continues to lead in consumption due to high-volume electronics production, while Europe drives innovation in automotive applications. Future growth is expected to be influenced by smart device proliferation, electric vehicle expansion, and increasing demand for miniaturized electronic components.

The Molded Interconnect Device market holds strategic importance as industries increasingly prioritize compact design, functional integration, and cost-efficient manufacturing. MID technology enables the consolidation of mechanical and electrical functions into a single component, reducing assembly steps by up to 35% and lowering overall product weight by nearly 25%. Laser Direct Structuring delivers approximately 40% improvement in design flexibility compared to traditional printed circuit board assembly methods, making it a preferred solution in high-precision industries.

Europe dominates in production volume due to its strong automotive and industrial base, while Asia-Pacific leads in adoption with over 60% of electronics manufacturers incorporating MID solutions into consumer and industrial devices. By 2028, the integration of AI-driven design optimization and advanced additive manufacturing is expected to improve production efficiency by 30% while reducing material waste by nearly 20%.

From an ESG perspective, firms are committing to sustainability targets such as 25% reduction in carbon emissions and increased use of recyclable thermoplastics by 2030. These commitments are influencing procurement strategies and supplier partnerships across the value chain. In 2024, a leading electronics manufacturer in Japan achieved a 22% reduction in production costs and a 15% improvement in product reliability through automated MID fabrication techniques.

As industries transition toward electrification, smart systems, and miniaturized architectures, the Molded Interconnect Device market is positioned as a critical enabler of innovation. Its role in enhancing design efficiency, supporting sustainability goals, and enabling next-generation electronic integration establishes it as a cornerstone for resilient and future-ready manufacturing ecosystems.

The Molded Interconnect Device market is shaped by rapid technological advancements, increasing demand for compact electronics, and evolving industrial requirements. The growing complexity of electronic systems in automotive, medical, and consumer applications has accelerated the adoption of MID technology, which enables three-dimensional circuit integration. Manufacturing trends indicate a shift toward automation and digitalization, with over 60% of manufacturers incorporating advanced production techniques such as laser structuring and robotic assembly. Additionally, the increasing penetration of electric vehicles and smart medical devices is driving demand for lightweight, space-efficient components. Supply chain optimization, material innovation, and sustainability regulations are also influencing market dynamics, pushing companies toward eco-friendly production processes and high-performance materials.

The demand for compact and multifunctional electronic devices is a primary driver of the Molded Interconnect Device market. Modern consumer electronics have witnessed a size reduction of nearly 30% over the past decade while increasing functionality, necessitating advanced integration solutions like MID. In automotive applications, over 70% of new electronic modules now require space-saving designs, particularly in electric vehicles and advanced driver-assistance systems. MID technology enables integration of circuits directly onto three-dimensional plastic components, reducing assembly complexity by up to 40%. Additionally, the medical device industry has seen a 25% increase in demand for miniaturized diagnostic and wearable devices, further boosting MID adoption. These trends highlight the critical role of MID in enabling next-generation compact electronics.

High initial investment requirements remain a significant restraint for the Molded Interconnect Device market. Setting up MID production facilities involves advanced equipment such as laser structuring systems and precision molding machines, which can increase capital expenditure by up to 35% compared to conventional PCB manufacturing setups. Additionally, the cost of specialized materials, including high-performance polymers and conductive inks, adds to overall production expenses. Small and medium-sized enterprises often face barriers to entry due to these financial constraints. Furthermore, the complexity of MID design and manufacturing requires skilled labor, increasing operational costs by approximately 20%. These factors collectively limit widespread adoption, particularly in cost-sensitive industries and emerging markets.

The rapid expansion of electric vehicles and Internet of Things (IoT) devices presents substantial growth opportunities for the Molded Interconnect Device market. Electric vehicle production has increased by over 50% in recent years, with each vehicle incorporating multiple compact electronic modules requiring efficient circuit integration. MID technology offers up to 25% weight reduction and improved thermal management, making it ideal for EV applications. Similarly, the global IoT ecosystem is expected to surpass 30 billion connected devices, driving demand for miniaturized, high-performance components. MID solutions enable seamless integration of sensors, antennas, and connectors within a single structure, enhancing device functionality and reliability. These emerging applications are expected to significantly expand the scope of MID adoption across industries.

Design complexity and lack of standardization pose significant challenges to the Molded Interconnect Device market. MID components require precise coordination between mechanical design and electronic circuitry, increasing design complexity by nearly 30% compared to traditional PCB-based systems. The absence of universal design standards leads to compatibility issues and longer development cycles, often extending product launch timelines by 15–20%. Additionally, integrating MID into existing manufacturing processes can be challenging, requiring modifications to production lines and quality control systems. Variability in material properties and process parameters further complicates large-scale production, impacting consistency and reliability. These challenges necessitate continuous innovation and collaboration across the supply chain to ensure efficient and standardized MID implementation.

• 3D Circuit Integration Achieves 35% Space Optimization in Compact Electronics

The transition toward three-dimensional circuit integration is significantly transforming product design strategies across industries. Molded Interconnect Device solutions are enabling up to 35% space reduction in electronic modules while improving component density by nearly 40%. This trend is particularly visible in automotive sensor systems, where over 65% of newly designed modules incorporate 3D MID structures for improved functionality. Additionally, integration efficiency has increased by approximately 28%, allowing manufacturers to reduce assembly steps and improve reliability. The growing complexity of smart devices is further accelerating demand for advanced MID configurations that support multi-layer circuit designs.

• Adoption of Laser Direct Structuring (LDS) Expands by Over 50% in Precision Manufacturing

Laser Direct Structuring technology has emerged as a cornerstone in MID production, with adoption rates increasing by more than 50% across high-precision industries. LDS enables circuit patterning accuracy within ±10 microns, improving electrical performance consistency by 30%. Approximately 70% of MID manufacturers now utilize LDS processes for high-volume production, particularly in automotive and medical applications. This trend is driving improvements in production speed by nearly 20% while reducing material wastage by up to 15%, making it a preferred manufacturing method for advanced electronic integration.

• Rise in Modular and Prefabricated Electronics Design Driving 55% Efficiency Gains

The adoption of modular and prefabricated design approaches is reshaping demand dynamics in the Molded Interconnect Device market. Around 55% of new electronic system projects report measurable cost and time benefits through modular integration strategies. Pre-designed MID components are increasingly manufactured off-site using automated systems, reducing labor requirements by nearly 30% and shortening production timelines by 25%. Demand for high-precision MID components is particularly strong in Europe and North America, where over 60% of manufacturers prioritize efficiency-driven production models. This trend is accelerating the shift toward standardized, scalable electronic architectures.

• Sustainable Materials and Recycling Initiatives Increase Adoption by 45%

Environmental considerations are driving the adoption of sustainable materials in MID manufacturing, with usage of recyclable thermoplastics increasing by approximately 45% over recent years. Manufacturers are focusing on reducing carbon emissions by up to 25% through energy-efficient production processes and material optimization. Around 50% of MID producers have implemented closed-loop recycling systems to minimize waste and improve resource efficiency. This trend is particularly strong in regions with stringent environmental regulations, where compliance requirements are pushing companies toward greener production methods while maintaining high-performance standards.

The Molded Interconnect Device market segmentation reflects a diverse landscape driven by technological complexity and application-specific requirements. By type, the market includes Laser Direct Structuring (LDS), Two-Shot Molding, and Film Technique variants, each catering to different precision and cost requirements. Application-wise, automotive electronics dominate due to increasing integration of sensors and control systems, followed by consumer electronics and healthcare devices. End-user segmentation highlights strong adoption among automotive OEMs, electronics manufacturers, and medical device producers. Approximately 40% of MID demand originates from automotive applications, while consumer electronics contribute over 25%, driven by miniaturization trends. Regional consumption patterns show Asia-Pacific leading in volume production, while Europe focuses on high-performance applications. The segmentation highlights a balance between high-volume manufacturing and specialized, high-value applications.

Laser Direct Structuring (LDS) remains the leading product type, accounting for approximately 48% of total adoption due to its high precision and ability to create complex 3D circuit layouts. Its dominance is supported by its capability to reduce production steps by nearly 30% while improving circuit reliability by 25%. Two-Shot Molding follows with around 28% share, offering cost-effective solutions for high-volume manufacturing but with slightly lower design flexibility. Film Technique-based MID accounts for nearly 14%, primarily used in niche applications requiring flexible circuit integration. The remaining 10% consists of hybrid and emerging MID fabrication methods, which are gaining traction in specialized industrial and aerospace applications.

Among these, Laser Direct Structuring is also the fastest-growing segment, expanding at an estimated rate of 11.5% annually due to increasing adoption in automotive and medical electronics. Its ability to support miniaturization and high-density circuit integration is driving this growth.

Automotive electronics dominate the Molded Interconnect Device market, contributing approximately 40% of total usage due to increasing demand for advanced driver-assistance systems, sensors, and electric vehicle components. Consumer electronics follow with nearly 27% share, driven by the need for compact and multifunctional devices such as smartphones and wearable technology. Healthcare applications account for around 18%, supported by rising demand for miniaturized diagnostic and monitoring devices. Industrial electronics and telecommunications collectively represent the remaining 15%, focusing on specialized and high-reliability applications.

Healthcare applications are emerging as the fastest-growing segment, expanding at an estimated rate of 12.2% annually due to increasing adoption of wearable and implantable medical devices. The demand for precision and compactness in medical electronics is a key growth factor.

Automotive OEMs represent the leading end-user segment, accounting for approximately 38% of total MID consumption due to the increasing integration of electronic components in vehicles. Electronics manufacturers follow closely with around 32% share, driven by demand for compact and high-performance consumer devices. Medical device manufacturers contribute nearly 18%, reflecting the growing importance of precision electronics in healthcare. The remaining 12% includes aerospace, industrial automation, and telecommunications sectors, which utilize MID for specialized and high-reliability applications.

Medical device manufacturers are the fastest-growing end-user segment, expanding at an estimated rate of 12.8% annually due to increasing demand for wearable health monitoring systems and minimally invasive diagnostic tools. Adoption rates in this segment have increased by over 35% in recent years.

Region Asia-Pacific accounted for the largest market share at 41% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 11.2% between 2026 and 2033.

Asia-Pacific’s dominance is supported by high-volume electronics manufacturing, with China alone contributing over 55% of regional production output. Japan and South Korea collectively account for nearly 25% of advanced MID applications, particularly in automotive and semiconductor industries. North America holds approximately 24% share, driven by strong demand in healthcare and aerospace sectors, where over 60% of advanced electronic modules require compact integration. Europe contributes close to 22% share, with Germany, France, and the UK leading adoption in automotive electronics, where MID integration in electric vehicles exceeds 65%. South America and the Middle East & Africa together represent around 13%, with increasing investments in industrial automation and telecommunications infrastructure. Across regions, over 70% of MID demand is concentrated in automotive and consumer electronics, highlighting the importance of regional industrial ecosystems in shaping market expansion.

How are advanced electronics integration trends reshaping industrial demand patterns?

North America accounts for approximately 24% of the global Molded Interconnect Device market, with strong demand driven by healthcare, aerospace, and high-end consumer electronics sectors. The region has witnessed over 50% adoption of miniaturized electronic components in medical devices, particularly wearable diagnostics and imaging systems. Government initiatives supporting advanced manufacturing and semiconductor production have increased funding allocations by nearly 30% in recent years. Technological advancements such as AI-driven design optimization and automated laser structuring are improving production efficiency by over 25%. A key regional player, Molex, has expanded its MID capabilities by integrating advanced antenna solutions into automotive and communication systems, improving signal efficiency by 18%. Consumer behavior in this region shows higher enterprise adoption, with over 65% of large-scale manufacturers integrating MID technology into next-generation product designs.

What role does precision engineering innovation play in driving next-generation electronics integration?

Europe holds nearly 22% of the Molded Interconnect Device market, with Germany, the UK, and France leading adoption. Germany alone contributes over 40% of regional MID production, largely due to its strong automotive manufacturing base. Regulatory frameworks emphasizing sustainability and circular economy practices have led to a 35% increase in the use of recyclable thermoplastics in MID production. The region has also seen over 60% adoption of Laser Direct Structuring technology in high-precision applications. Companies such as LPKF Laser & Electronics have introduced advanced LDS systems capable of improving circuit accuracy by 30%. Consumer behavior reflects regulatory-driven demand, where over 55% of manufacturers prioritize environmentally compliant MID solutions. The integration of MID in electric vehicles across Europe has surpassed 65%, reinforcing the region’s leadership in innovation-driven adoption.

How is large-scale manufacturing accelerating compact electronics innovation globally?

Asia-Pacific dominates the Molded Interconnect Device market in terms of volume, accounting for over 41% of global production. China, Japan, and South Korea are the top consuming countries, collectively contributing more than 70% of regional demand. China leads with over 55% share in electronics manufacturing, while Japan focuses on high-precision automotive and industrial applications. The region has experienced a 45% increase in smart device production, driving demand for compact circuit integration technologies. Advanced manufacturing hubs are adopting automation at rates exceeding 65%, improving MID production efficiency by nearly 28%. A notable example includes a Japanese electronics firm deploying MID-based antenna modules in over 10 million smartphones annually, enhancing signal performance by 20%. Consumer behavior is strongly influenced by mobile and IoT adoption, with over 75% of devices incorporating miniaturized electronic components.

How are industrial modernization efforts influencing electronic component demand?

South America represents approximately 7% of the global Molded Interconnect Device market, with Brazil and Argentina being key contributors. Brazil accounts for nearly 60% of regional demand, driven by growth in automotive assembly and consumer electronics manufacturing. Infrastructure development initiatives have increased industrial automation adoption by over 20%, creating demand for compact electronic components. Government incentives supporting local manufacturing have reduced import dependency by approximately 15%. A regional electronics manufacturer in Brazil has implemented MID-based components in automotive lighting systems, improving durability by 18% and reducing component weight by 12%. Consumer behavior in this region is closely tied to affordability and localized production, with over 50% of manufacturers focusing on cost-efficient MID solutions for domestic markets.

What factors are accelerating adoption of advanced electronic integration technologies?

The Middle East & Africa account for around 6% of the Molded Interconnect Device market, with the UAE and South Africa emerging as key growth countries. Demand is largely driven by oil & gas automation, telecommunications, and smart infrastructure projects, where electronic component integration has increased by nearly 25%. Technological modernization initiatives have boosted adoption of advanced manufacturing techniques by over 30%. Trade partnerships and government policies supporting industrial diversification have led to a 20% increase in electronics production capabilities. A UAE-based technology firm has introduced MID-integrated smart monitoring systems for industrial applications, improving operational efficiency by 22%. Consumer behavior reflects growing demand for smart technologies, with over 40% of enterprises investing in IoT-enabled devices incorporating compact circuitry.

China – 32% share: Molded Interconnect Device market dominance driven by high-volume electronics manufacturing and large-scale production infrastructure.

Germany – 19% share: Molded Interconnect Device market leadership supported by advanced automotive electronics integration and precision engineering capabilities.

The Molded Interconnect Device market exhibits a moderately consolidated competitive landscape, with the top five companies accounting for approximately 52% of the total market share. Over 40 active global and regional players compete across different segments, ranging from high-precision manufacturing to cost-efficient production solutions. Leading companies are focusing on technological innovation, particularly in Laser Direct Structuring and advanced polymer materials, which have improved production efficiency by up to 30% and reduced material waste by 15%. Strategic partnerships and collaborations have increased by over 25% in recent years, enabling companies to expand their product portfolios and geographic presence. Mergers and acquisitions activity has also intensified, with more than 10 significant deals recorded between 2023 and 2025 aimed at strengthening capabilities in automotive and healthcare applications. Product innovation remains a key competitive factor, with over 60% of companies investing heavily in R&D to develop next-generation MID solutions. The market is characterized by strong competition in Europe and Asia-Pacific, where over 70% of manufacturers are engaged in continuous process optimization and digital transformation initiatives to maintain competitive advantage.

Molex

LPKF Laser & Electronics

HARTING Technology Group

TE Connectivity

Amphenol Corporation

Panasonic Industry

Mitsumi Electric

SelectConnect Technologies

Cicor Group

Paragon Rapid Technologies

The Molded Interconnect Device market is being transformed by a convergence of advanced manufacturing technologies, material innovations, and digital design tools. Laser Direct Structuring (LDS) remains the most influential technology, enabling circuit patterning precision within ±10 microns and supporting complex three-dimensional geometries. Over 70% of MID manufacturers now rely on LDS for high-volume production, particularly in automotive sensors and communication modules. This technology has improved production efficiency by nearly 25% while reducing assembly steps by up to 40%.

Additive manufacturing is emerging as a complementary technology, with adoption increasing by approximately 35% in prototyping and low-volume production. Hybrid manufacturing techniques combining 3D printing with traditional injection molding are enabling faster design iterations, reducing development cycles by nearly 30%. Additionally, advanced thermoplastic materials such as polycarbonate blends and liquid crystal polymers are improving thermal resistance by up to 20% and enhancing electrical conductivity by 15%, making MID suitable for high-performance applications.

Automation and digitalization are also reshaping the production landscape. Smart factories equipped with AI-driven quality control systems have reduced defect rates by over 18%, while real-time monitoring systems have improved operational efficiency by 22%. Integration of IoT-enabled sensors within MID components is expanding rapidly, with over 60% of new designs incorporating connectivity features for data transmission and system monitoring.

Emerging technologies such as nano-coating and conductive ink printing are further enhancing circuit durability and flexibility, increasing component lifespan by approximately 25%. These innovations are particularly relevant in healthcare and aerospace sectors, where reliability and miniaturization are critical. Collectively, these technological advancements are positioning MID as a key enabler of next-generation electronic integration across industries.

• In March 2025, LPKF Laser & Electronics announced the expansion of its LDS system portfolio with enhanced laser structuring accuracy and automation capabilities, enabling up to 30% faster production cycles for MID components. The upgrade supports high-volume automotive and electronics manufacturing. Source: www.lpkf.com

• In September 2024, Molex introduced advanced MID-based antenna solutions for 5G applications, designed to improve signal efficiency by 20% and reduce device size by 15%. These solutions are targeted at automotive connectivity and next-generation communication systems. Source: www.molex.com

• In May 2025, HARTING Technology Group expanded its industrial connectivity solutions by integrating MID technology into compact connectors, improving space utilization by 25% and enhancing durability in harsh industrial environments. Source: www.harting.com

• In November 2024, TE Connectivity launched new MID-enabled sensor modules for automotive safety systems, achieving 18% weight reduction and 22% improvement in signal reliability, supporting the growing demand for advanced driver-assistance systems. Source: www.te.com

The Molded Interconnect Device Market Report provides a comprehensive analysis of a highly specialized segment within the electronics manufacturing industry, covering a wide range of technologies, applications, and geographic regions. The report examines key product types, including Laser Direct Structuring, Two-Shot Molding, and Film Techniques, which collectively account for over 85% of MID manufacturing processes. It also explores emerging hybrid manufacturing approaches that are gaining traction in high-precision industries.

From an application perspective, the report covers automotive electronics, consumer devices, healthcare equipment, industrial automation, and telecommunications, with automotive applications alone representing approximately 40% of total demand. The study further analyzes end-user industries such as automotive OEMs, electronics manufacturers, and medical device companies, which together contribute over 80% of MID adoption globally.

Geographically, the report provides detailed insights into Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, highlighting regional production capacities, consumption patterns, and technology adoption rates. Asia-Pacific accounts for more than 40% of global production volume, while Europe leads in high-performance and automotive-focused applications.

In addition to core market segments, the report includes analysis of technological advancements such as laser structuring, additive manufacturing, and advanced polymer materials, which are driving innovation in MID design and production. It also addresses regulatory frameworks, sustainability initiatives, and supply chain dynamics influencing market growth. The scope extends to emerging niche segments, including IoT-enabled MID components and miniaturized medical devices, providing decision-makers with a holistic view of current trends, competitive positioning, and future opportunities within the Molded Interconnect Device market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

10.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Molex, LPKF Laser & Electronics, HARTING Technology Group, TE Connectivity, Amphenol Corporation, Panasonic Industry, Mitsumi Electric, SelectConnect Technologies, Cicor Group, Paragon Rapid Technologies |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |