Reports

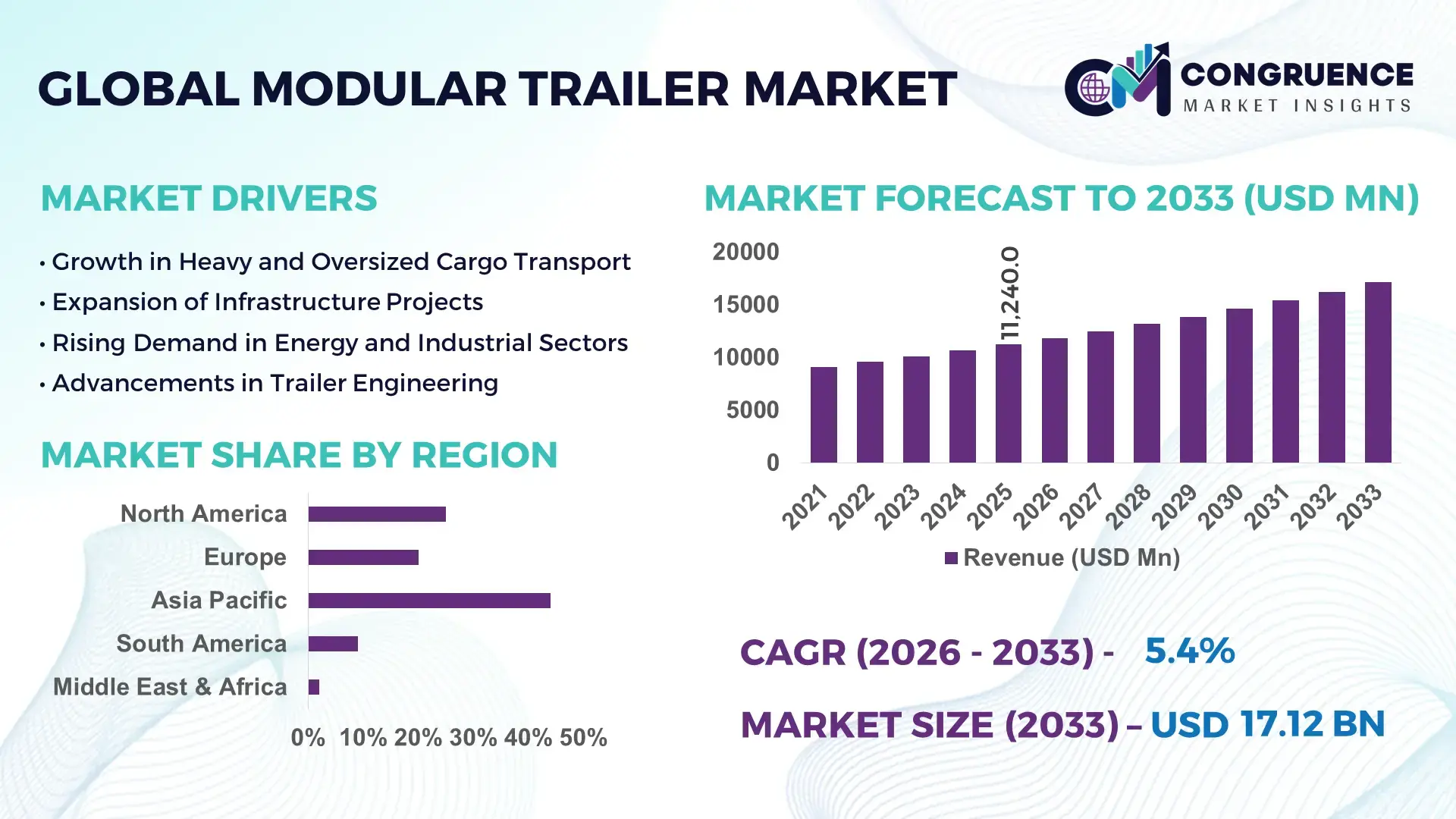

The Global Modular Trailer Market was valued at USD 11240 Million in 2025 and is anticipated to reach a value of USD 17119.5 Million by 2033 expanding at a CAGR of 5.4% between 2026 and 2033. This growth is primarily driven by increasing demand for heavy-duty transport solutions across infrastructure, energy, and industrial project logistics.

China continues to play a dominant role in the modular trailer market with extensive manufacturing capacity and large-scale infrastructure deployment. The country produces over 35% of global heavy transport equipment, supported by strong domestic demand from sectors such as wind energy, petrochemicals, and construction. Investments in transport engineering exceeded USD 150 billion annually in recent years, enabling rapid adoption of self-propelled modular trailers (SPMTs) for complex cargo movement. Additionally, more than 60% of large-scale bridge and offshore component transportation projects in Asia utilize modular trailer systems, supported by advancements in hydraulic axle configurations and digital load-balancing technologies.

Market Size & Growth: USD 11240 Million in 2025 to USD 17119.5 Million by 2033 at a CAGR of 5.4%, driven by rising infrastructure megaprojects and heavy cargo logistics demand.

Top Growth Drivers: Infrastructure expansion projects (42%), renewable energy installations (36%), and oil & gas equipment transport demand (31%).

Short-Term Forecast: By 2028, operational efficiency in heavy transport logistics is expected to improve by 18% due to optimized modular configurations and automation.

Emerging Technologies: Integration of telematics-based fleet monitoring, advanced hydraulic suspension systems, and autonomous steering modules for precision transport.

Regional Leaders: Asia-Pacific projected at USD 6.8 Billion by 2033 with strong infrastructure demand; Europe at USD 4.1 Billion driven by wind energy logistics; North America at USD 3.7 Billion supported by industrial transport modernization.

Consumer/End-User Trends: High adoption among EPC contractors, logistics firms, and energy companies focusing on oversized cargo mobility and cost optimization.

Pilot or Case Example: In 2024, a European wind project deployment improved transport efficiency by 22% using SPMT systems with synchronized axle control.

Competitive Landscape: Market leader holds approximately 18% share, followed by key players including Goldhofer, Scheuerle, Faymonville, Nicolas, and TII Group.

Regulatory & ESG Impact: Stricter emission norms and road safety regulations are encouraging adoption of energy-efficient and digitally controlled modular trailers.

Investment & Funding Patterns: Over USD 2.3 Billion invested globally in heavy transport equipment upgrades and smart logistics infrastructure in the past three years.

Innovation & Future Outlook: Increasing focus on electrified trailer modules, AI-driven load optimization, and integration with smart infrastructure for real-time route planning.

The modular trailer market is strongly influenced by key industry sectors such as construction, energy, and heavy engineering, which collectively account for over 70% of equipment demand. Recent innovations include multi-axle hydraulic systems capable of handling loads exceeding 10,000 tons and modular designs allowing flexible configuration for diverse cargo types. Regulatory frameworks emphasizing transport safety and emissions compliance are shaping product development, particularly in Europe and North America. Regionally, Asia-Pacific leads in consumption due to rapid urbanization and industrial expansion, while Europe is witnessing increased demand from offshore wind projects. Emerging trends such as digital fleet integration, predictive maintenance, and automation-driven logistics optimization are expected to redefine operational efficiency and scalability in the modular trailer market.

The Modular Trailer Market holds significant strategic relevance within global heavy logistics, enabling efficient transport of oversized and high-value industrial components across infrastructure, energy, mining, and defense sectors. As project sizes expand, modular trailer systems are increasingly integrated into end-to-end logistics planning, reducing reliance on fixed transport infrastructure. Advanced self-propelled modular trailers (SPMTs) equipped with digital synchronization and load-balancing capabilities are transforming operational efficiency. For instance, AI-enabled fleet management systems deliver 28% improvement in route optimization compared to conventional manual planning methods.

From a regional perspective, Asia-Pacific dominates in volume due to extensive infrastructure and industrial activity, while Europe leads in adoption with over 65% of heavy transport enterprises integrating digitally controlled modular trailers into their operations. Short-term projections indicate that by 2028, AI-driven predictive maintenance and telematics integration are expected to improve fleet uptime by 20%, significantly lowering operational disruptions.

Compliance and ESG considerations are also shaping future pathways. Firms are committing to sustainability targets such as a 30% reduction in transport-related emissions by 2030 through optimized load distribution and fuel-efficient transport technologies. In a notable micro-scenario, in 2024, a German heavy logistics company achieved a 25% reduction in transport time through real-time route analytics and automated steering systems. As global industries demand safer, faster, and more sustainable heavy transport solutions, the Modular Trailer Market is emerging as a critical pillar supporting infrastructure resilience, regulatory compliance, and long-term sustainable growth strategies.

Large-scale infrastructure development across emerging and developed economies is a primary driver for the Modular Trailer Market. Governments worldwide are allocating substantial budgets for highways, rail corridors, energy plants, and smart city projects, all of which require transportation of oversized components such as turbines, transformers, and bridge sections. For example, over 40% of global infrastructure projects involve heavy cargo exceeding standard transport limits, necessitating modular trailer usage. The expansion of renewable energy installations, particularly wind energy, has further increased demand, as turbine components often exceed 80 meters in length and require specialized transport solutions. Modular trailers with multi-axle configurations provide flexibility and load distribution efficiency, reducing logistical constraints and enabling safe delivery across challenging terrains.

The high initial acquisition cost of modular trailers, especially advanced SPMTs, remains a significant restraint for market growth. A single modular trailer unit with advanced hydraulic and digital systems can cost up to 40% more than traditional heavy transport equipment, making it less accessible for small and mid-sized logistics providers. Additionally, maintenance requirements for hydraulic systems, electronic control units, and multi-axle configurations increase operational expenses. Skilled workforce requirements for operating and maintaining these systems further add to costs, with training expenses rising by nearly 20% in specialized logistics firms. These financial barriers limit widespread adoption, particularly in developing regions where budget constraints and lack of technical expertise hinder market penetration.

The integration of digital technologies presents significant opportunities for the Modular Trailer Market, particularly in enhancing operational efficiency and safety. Telematics, IoT-enabled sensors, and AI-based route planning systems are increasingly being adopted to monitor load conditions, optimize routes, and reduce downtime. Studies indicate that real-time monitoring systems can improve transport efficiency by up to 25% and reduce accident risks by 18%. Additionally, the emergence of autonomous steering and remote-controlled trailer systems is opening new avenues for precision transport in complex environments such as offshore platforms and industrial plants. The growing adoption of digital twins and simulation tools also allows logistics companies to plan and execute heavy transport operations with greater accuracy, reducing project delays and improving overall performance.

Regulatory challenges and infrastructure limitations pose significant obstacles to the growth of the Modular Trailer Market. Transporting oversized loads requires compliance with varying regional regulations, including road permits, axle load restrictions, and safety standards, which differ across countries and even within regions. Obtaining approvals can delay project timelines by several weeks, affecting operational efficiency. Additionally, inadequate infrastructure such as narrow roads, weak bridges, and limited turning radii in developing regions restrict the movement of modular trailers. Approximately 30% of logistics projects face delays due to infrastructure constraints and regulatory bottlenecks. These challenges necessitate additional planning, route modifications, and sometimes costly infrastructure reinforcements, increasing overall project complexity and limiting seamless market expansion.

• Expansion of Self-Propelled Modular Trailer (SPMT) Adoption: The use of SPMTs has increased significantly, with over 48% of heavy transport projects globally now relying on self-propelled systems for complex cargo handling. These trailers offer multi-directional movement and precise load balancing, improving operational efficiency by nearly 30% compared to conventional hydraulic trailers. Industries such as offshore wind and petrochemicals are key adopters, where over 65% of large-scale component movements now depend on SPMT technology due to its ability to handle loads exceeding 10,000 tons with enhanced safety and reduced manual intervention.

• Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Modular Trailer market. Approximately 55% of new infrastructure projects report cost optimization benefits when integrating prefabricated construction techniques. Pre-engineered components are increasingly manufactured off-site, leading to a 35% reduction in on-site labor requirements and a 25% decrease in project timelines. This trend is particularly prominent in Europe and North America, where over 60% of contractors are shifting toward modular construction to enhance efficiency and reduce material wastage, driving consistent demand for high-capacity transport solutions.

• Integration of Digital Telematics and Smart Logistics: Around 52% of modular trailer fleets are now equipped with telematics and IoT-enabled systems for real-time monitoring and predictive maintenance. These technologies have demonstrated a 20% reduction in downtime and a 15% improvement in fleet utilization rates. Advanced analytics platforms allow logistics providers to optimize routing, monitor axle load distribution, and ensure compliance with transport regulations. The adoption of AI-driven logistics platforms is further increasing, with nearly 40% of large fleet operators implementing automation tools to enhance operational visibility and decision-making accuracy.

• Growing Focus on Sustainable and Low-Emission Transport Solutions: Sustainability initiatives are increasingly influencing the Modular Trailer market, with nearly 45% of manufacturers investing in energy-efficient and low-emission transport systems. Hybrid and electric-assisted modular trailers are emerging, offering up to 18% reduction in fuel consumption compared to traditional diesel-powered systems. Additionally, over 50% of logistics companies are aligning with environmental targets, aiming to reduce transport-related emissions by at least 25% by 2030. This shift is supported by regulatory mandates and corporate ESG commitments, driving innovation in lightweight materials and energy-efficient trailer designs.

The Modular Trailer Market is segmented based on type, application, and end-user industries, each contributing distinctively to overall demand patterns. By type, self-propelled modular trailers dominate due to their flexibility and high load-bearing capacity, while conventional hydraulic trailers continue to serve cost-sensitive operations. In terms of application, infrastructure and construction projects account for the largest share, driven by increasing demand for transporting oversized structural components. Energy sector applications, particularly in wind and oil & gas, are witnessing rapid adoption due to the need for specialized heavy transport solutions. From an end-user perspective, engineering, procurement, and construction (EPC) firms lead the market, followed by logistics service providers and industrial manufacturers. Regional variations in adoption are influenced by infrastructure investment levels, regulatory frameworks, and industrial growth, with Asia-Pacific leading in volume demand and Europe focusing on technologically advanced transport solutions.

The Modular Trailer Market by type is primarily categorized into Self-Propelled Modular Trailers (SPMTs), Hydraulic Modular Trailers, and Other Specialized Trailers. SPMTs currently account for approximately 46% of total adoption due to their superior maneuverability, automated steering systems, and ability to transport extremely heavy loads with precision. In comparison, hydraulic modular trailers hold around 32% share, primarily used in less complex transport operations where cost efficiency is prioritized. However, SPMTs are also the fastest-growing segment, expanding at an estimated CAGR of 6.8%, driven by increasing demand for automated and digitally controlled heavy transport systems.

Other specialized trailers, including extendable and platform-based modular systems, collectively contribute nearly 22% of the market, serving niche applications such as aerospace component transport and defense logistics. These systems offer customization capabilities but are limited by higher operational complexity.

By application, the Modular Trailer Market is segmented into Infrastructure & Construction, Energy (including wind and oil & gas), Industrial Manufacturing, and Others. Infrastructure & Construction leads with approximately 41% share, as large-scale projects require the movement of oversized components such as bridge segments and precast structures. Energy applications account for around 34%, driven by the transport of wind turbine blades, nacelles, and heavy oil & gas equipment. However, the energy segment is the fastest-growing, with an estimated CAGR of 7.2%, fueled by global expansion in renewable energy installations.

Industrial manufacturing and other applications collectively contribute about 25%, including transport of heavy machinery, mining equipment, and aerospace components. These segments benefit from modular trailer flexibility but operate on comparatively smaller scales.

End-user segmentation of the Modular Trailer Market includes Engineering, Procurement, and Construction (EPC) companies, Logistics Service Providers, Energy Companies, and Industrial Manufacturers. EPC firms dominate with approximately 44% share, as they manage large-scale infrastructure and industrial projects requiring heavy transport solutions. Logistics service providers follow with around 27%, offering specialized transport services to multiple industries. Energy companies account for nearly 19%, with increasing reliance on modular trailers for renewable energy and oil & gas operations.

Among these, energy companies represent the fastest-growing end-user segment, expanding at an estimated CAGR of 7.5%, driven by the rapid deployment of wind and offshore energy projects. Industrial manufacturers and other end-users collectively contribute about 10%, focusing on niche applications such as heavy machinery relocation and defense logistics.

Region Asia-Pacific accounted for the largest market share at 46% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2026 and 2033.

Asia-Pacific’s dominance is supported by large-scale infrastructure investments exceeding 55% of global megaproject activity, particularly across China and India where over 70% of heavy cargo logistics involves modular transport systems. Europe holds approximately 28% share, driven by renewable energy projects, with more than 60% of offshore wind components transported using modular trailers. North America accounts for nearly 18% share, supported by industrial modernization and oil & gas transport demand. Meanwhile, South America and the Middle East & Africa collectively contribute around 8%, with growing investments in energy and mining sectors. Across all regions, over 50% of logistics providers are integrating advanced modular trailer systems to handle loads exceeding 3,000 tons, highlighting a global shift toward high-capacity, flexible transport solutions.

North America holds approximately 18% of the Modular Trailer Market, driven by strong demand from oil & gas, infrastructure, and renewable energy sectors. The U.S. accounts for over 75% of regional demand, with more than 65% of heavy transport projects involving modular trailer systems. Regulatory frameworks focusing on road safety and axle load compliance have led to a 20% increase in adoption of digitally controlled trailers. Technological advancements such as telematics integration and AI-based route optimization are implemented by nearly 48% of logistics companies, improving delivery precision and reducing downtime. A notable example includes a U.S.-based heavy transport firm deploying automated modular trailer fleets, achieving a 22% increase in operational efficiency. Regional consumer behavior indicates higher enterprise adoption across industrial and energy sectors, with over 60% of large contractors preferring modular systems for oversized cargo handling.

Europe represents nearly 28% of the Modular Trailer Market, with Germany, the UK, and France collectively contributing over 65% of regional demand. The region is heavily influenced by sustainability regulations, with more than 55% of logistics companies adopting low-emission transport solutions. The expansion of offshore wind projects has led to over 70% utilization of modular trailers for transporting turbine components. Advanced hydraulic systems and digital steering technologies are widely adopted, with nearly 50% of fleets equipped with smart monitoring systems. A leading regional manufacturer has introduced modular trailers with enhanced load distribution technology, improving transport stability by 25%. Consumer behavior in Europe is shaped by regulatory pressure, with enterprises prioritizing compliant, energy-efficient transport systems that meet stringent environmental and safety standards.

Asia-Pacific dominates the Modular Trailer Market in terms of volume, accounting for approximately 46% of global demand. China, India, and Japan are the top consuming countries, with China alone contributing over 60% of regional usage due to extensive industrial and infrastructure projects. More than 75% of large-scale construction and energy projects in the region require modular trailer systems for transporting heavy components. Rapid urbanization and manufacturing expansion have increased demand for trailers capable of handling loads above 5,000 tons. Technological innovation hubs in Japan and South Korea are driving advancements in automation and smart trailer systems, with over 40% of new units featuring digital control technologies. A regional manufacturer has expanded production capacity by 30% to meet rising demand, reflecting strong market momentum. Consumer behavior in this region is driven by cost efficiency and large-scale project execution requirements.

South America accounts for approximately 5% of the Modular Trailer Market, with Brazil and Argentina being the key contributors. The region’s demand is largely driven by mining and energy projects, which represent over 60% of modular trailer usage. Infrastructure development initiatives have increased the need for heavy transport solutions, particularly for moving mining equipment and energy components. Government policies supporting industrial growth and foreign investment have led to a 15% increase in heavy logistics activity. A regional logistics provider has adopted modular trailer systems to improve transport efficiency by 18% in mining operations. Consumer behavior reflects a strong reliance on cost-effective transport solutions, with over 50% of companies prioritizing durability and operational efficiency over advanced digital features.

The Middle East & Africa region holds approximately 3% of the Modular Trailer Market, with demand concentrated in the UAE, Saudi Arabia, and South Africa. Oil & gas projects account for nearly 65% of regional demand, followed by large-scale construction initiatives. Infrastructure modernization programs have increased the adoption of modular trailers capable of handling loads exceeding 4,000 tons. Technological advancements, including hydraulic suspension systems and remote-controlled steering, are being adopted by around 35% of logistics providers. Trade partnerships and government investments in industrial projects have boosted demand for heavy transport solutions. A regional operator has implemented modular trailer systems for refinery projects, achieving a 20% improvement in transport efficiency. Consumer behavior is influenced by large project requirements, with companies prioritizing reliability and load capacity over customization.

China – 34% share in the Modular Trailer Market, driven by high manufacturing capacity and extensive infrastructure project demand.

United States – 21% share in the Modular Trailer Market, supported by strong industrial logistics and energy sector transport requirements.

The Modular Trailer Market is moderately fragmented, with over 35 active global and regional players competing across different segments and geographies. The top five companies collectively account for approximately 52% of the market, indicating a balanced mix of consolidation and competitive diversity. Leading players are focusing on product innovation, with more than 60% of new product launches incorporating advanced hydraulic systems and digital control technologies. Strategic partnerships and mergers have increased by nearly 18% over the past three years, aimed at expanding geographic presence and enhancing technological capabilities.

Companies are investing heavily in research and development, with an estimated 12% of operational budgets allocated to innovation in areas such as automation, telematics, and energy-efficient trailer systems. Customization has emerged as a key competitive factor, with over 45% of manufacturers offering tailored modular solutions for specific industry applications. Additionally, after-sales services and maintenance support are becoming critical differentiators, influencing nearly 30% of purchasing decisions among logistics providers. The competitive landscape is further shaped by regional players catering to localized demand, particularly in Asia-Pacific and Europe, where infrastructure and regulatory requirements vary significantly.

Goldhofer AG

Faymonville Group

TII Group (Scheuerle)

Nicolas Industrie

Broshuis B.V.

Cometto S.p.A.

KAMAG Transporttechnik GmbH

DOLL Fahrzeugbau GmbH

Tratec Engineers Pvt. Ltd.

Andover Trailers Ltd.

Technological advancements are significantly reshaping the Modular Trailer Market, with increasing emphasis on automation, digital integration, and high-capacity engineering. One of the most impactful innovations is the adoption of self-propelled modular trailers (SPMTs) equipped with advanced electronic steering systems, enabling 360-degree maneuverability and precise positioning accuracy within ±5 mm tolerance. These systems are widely used in transporting ultra-heavy loads exceeding 10,000 tons, improving operational safety by nearly 35% compared to conventional transport methods.

Telematics and IoT integration are becoming standard, with over 50% of modern modular trailer fleets now equipped with real-time monitoring systems. These technologies allow operators to track axle load distribution, tire pressure, and route conditions, reducing maintenance-related downtime by approximately 20% and improving asset utilization rates by 15%. Predictive maintenance powered by AI algorithms is also gaining traction, enabling early fault detection and reducing unexpected equipment failures by up to 25%.

Hydraulic suspension technology has evolved to support multi-axle configurations with load distribution accuracy exceeding 98%, ensuring stability during transport of oversized industrial components. Additionally, modular trailers now feature synchronized lifting and lowering systems, allowing for vertical adjustments of up to 600 mm, which enhances adaptability across uneven terrains.

Emerging innovations include electrified modular trailer units and hybrid propulsion systems, which can reduce fuel consumption by nearly 18% while lowering emissions. Digital twin technology is also being adopted by approximately 30% of large logistics firms, enabling simulation-based planning that improves route efficiency and reduces project delays by over 20%. These technological developments are positioning modular trailers as critical assets in modern heavy logistics ecosystems.

• In March 2025, Goldhofer AG expanded its heavy-duty transport portfolio by introducing a new generation of PST/SL-E split modular trailers with enhanced electronic steering precision and increased payload capacity, enabling transport of loads exceeding 12,000 tons. Source: www.goldhofer.com

• In September 2024, Faymonville Group launched an upgraded CombiMAX PA-X modular trailer featuring reinforced chassis design and optimized axle load distribution, improving transport efficiency by up to 15% for oversized industrial cargo. Source: www.faymonville.com

• In January 2025, TII Group (Scheuerle) deployed advanced SPMT solutions for a large-scale infrastructure project in Europe, utilizing over 300 axle lines to transport heavy bridge sections, achieving significant improvements in operational precision and load handling safety. Source: www.tii-group.com

• In July 2024, Broshuis B.V. introduced a new extendable semi low-loader trailer designed for wind turbine transport, capable of accommodating blade lengths exceeding 90 meters while improving stability and reducing transport time by approximately 20%. Source: www.broshuis.com

The Modular Trailer Market Report provides a comprehensive analysis of key segments, technologies, applications, and regional dynamics shaping the global industry landscape. The report covers multiple product categories, including self-propelled modular trailers, hydraulic modular trailers, and specialized transport systems, which collectively address over 90% of heavy cargo transport requirements across industries. It evaluates application areas such as infrastructure construction, energy (including wind, oil, and gas), industrial manufacturing, and mining, which together account for more than 80% of total equipment utilization.

Geographically, the report analyzes five major regions—Asia-Pacific, North America, Europe, South America, and the Middle East & Africa—covering over 30 key countries with diverse infrastructure and industrial development patterns. Asia-Pacific alone represents nearly half of global demand in terms of volume, while Europe leads in technology adoption, with over 60% of fleets equipped with advanced digital systems.

The report also examines technological trends such as telematics integration, AI-driven logistics optimization, and electrification, which are being adopted by more than 40% of large fleet operators globally. It further explores regulatory frameworks, including road safety standards and emission compliance requirements, influencing product design and market adoption.

Additionally, the scope includes emerging segments such as autonomous modular transport systems and digital twin-based planning tools, which are gaining traction among leading logistics providers. With coverage of over 35 major market participants and detailed insights into operational practices, innovation strategies, and end-user adoption patterns, the report serves as a strategic resource for stakeholders seeking to understand market structure, competitive positioning, and future growth opportunities.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

5.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Goldhofer AG, Faymonville Group, TII Group (Scheuerle), Nicolas Industrie, Broshuis B.V., Cometto S.p.A., KAMAG Transporttechnik GmbH, DOLL Fahrzeugbau GmbH, Tratec Engineers Pvt. Ltd., Andover Trailers Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |