Reports

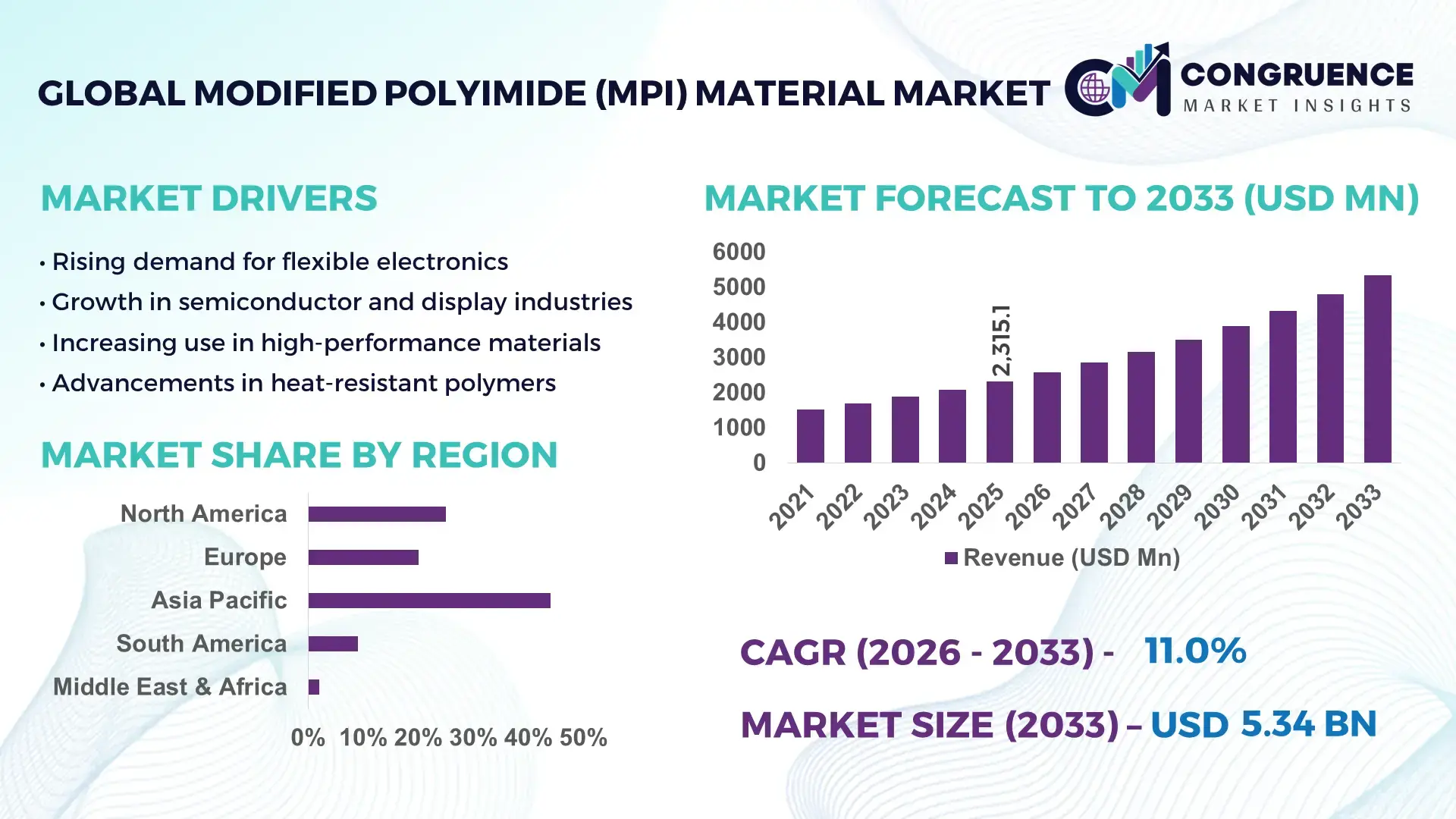

The Global Modified Polyimide (MPI) Material Market was valued at USD 2315.11 Million in 2025 and is anticipated to reach a value of USD 5335.27 Million by 2033 expanding at a CAGR of 11% between 2026 and 2033. The growth is primarily driven by the rising demand for high-performance materials in advanced electronics and flexible display technologies.

China stands out as the dominant country in the Modified Polyimide (MPI) Material market due to its extensive electronics manufacturing ecosystem and aggressive investments in semiconductor and display panel production. The country accounts for over 60% of global display panel manufacturing capacity and has invested more than USD 150 billion in semiconductor fabrication facilities over the past decade. MPI materials are widely used in flexible OLED displays, where China leads production output with over 70% of global OLED panel shipments. Additionally, domestic chemical manufacturers are scaling MPI production capacities exceeding 25,000 tons annually, supported by advancements in polymer synthesis and coating technologies. Consumer electronics adoption, particularly foldable smartphones and wearable devices, continues to accelerate MPI material utilization across domestic markets.

Market Size & Growth: USD 2315.11 Million (2025) to USD 5335.27 Million (2033), CAGR 11%, driven by increasing demand for flexible electronics and high-temperature resistant materials.

Top Growth Drivers: Flexible electronics adoption +45%, semiconductor demand +38%, thermal stability efficiency improvement +32%.

Short-Term Forecast: By 2028, production efficiency is expected to improve by 28% due to automation and material optimization.

Emerging Technologies: Advanced polymer engineering, nano-enhanced MPI coatings, and AI-driven material design systems.

Regional Leaders: Asia-Pacific USD 2900 Million by 2033 with strong electronics manufacturing, North America USD 1250 Million with aerospace applications, Europe USD 980 Million driven by automotive electronics innovation.

Consumer/End-User Trends: Rising adoption in OLED displays, flexible circuits, and high-frequency communication devices.

Pilot or Case Example: In 2024, a South Korean electronics manufacturer achieved 22% efficiency gains in OLED panel durability using advanced MPI coatings.

Competitive Landscape: Market leader holds approximately 28% share, followed by key players including global specialty polymer manufacturers and advanced chemical producers.

Regulatory & ESG Impact: Increasing compliance with low-emission production standards and 30% reduction in solvent usage by 2030 targets.

Investment & Funding Patterns: Over USD 4.5 billion invested globally in advanced polymer R&D and production facilities.

Innovation & Future Outlook: Integration of MPI materials in next-generation foldable devices and high-frequency 5G infrastructure components.

The Modified Polyimide (MPI) Material market is gaining traction across multiple industries, with electronics contributing approximately 55% of total demand, followed by automotive electronics at 18% and aerospace applications at 12%. Recent innovations include ultra-thin MPI films with less than 10-micron thickness and enhanced dielectric strength exceeding 300 kV/mm, enabling advanced circuit miniaturization. Regulatory frameworks are pushing manufacturers toward environmentally sustainable solvent systems, reducing emissions by up to 25%. Regionally, Asia-Pacific leads in consumption due to large-scale manufacturing hubs, while North America and Europe focus on high-performance applications. Emerging trends include integration with 5G infrastructure, AI-enabled material optimization, and increased use in electric vehicle battery insulation systems, indicating strong future growth potential.

The Modified Polyimide (MPI) Material Market holds strong strategic relevance as industries increasingly demand high-performance, lightweight, and thermally stable materials for next-generation applications. MPI materials are critical in flexible electronics, semiconductor packaging, and aerospace systems, where durability and heat resistance above 300°C are essential. Advanced nano-engineered MPI delivers 35% higher thermal stability compared to conventional polyimide materials, significantly enhancing reliability in high-frequency electronic components.

Asia-Pacific dominates in production volume, while North America leads in advanced adoption, with over 42% of enterprises integrating MPI materials into high-performance electronics and aerospace applications. By 2028, AI-driven material design is expected to improve production yield efficiency by 30% and reduce defect rates in thin-film MPI coatings by nearly 25%. Companies are increasingly aligning with ESG commitments, targeting up to 40% reduction in volatile organic compound emissions by 2030 through green chemistry innovations.

In 2024, a Japanese manufacturer achieved a 27% improvement in flexible circuit durability by integrating nano-reinforced MPI films into foldable display components. This micro-scenario highlights the tangible performance benefits of material innovation. Strategic pathways also include vertical integration across supply chains, increased investment in R&D for ultra-thin MPI films, and expansion into electric vehicle insulation systems. The Modified Polyimide (MPI) Material Market is steadily positioning itself as a critical enabler of resilient, compliant, and sustainable industrial growth across global high-tech sectors.

The surge in flexible electronics demand is significantly propelling the Modified Polyimide (MPI) Material market. Flexible OLED displays, foldable smartphones, and wearable devices require materials that can withstand repeated bending without performance degradation. MPI materials offer flexibility combined with thermal resistance exceeding 300°C, making them indispensable in these applications. Global shipments of foldable smartphones have increased by over 40% annually, directly boosting demand for MPI films. Additionally, flexible printed circuits using MPI substrates demonstrate up to 25% higher durability compared to traditional materials. Consumer electronics manufacturers are increasingly shifting toward ultra-thin MPI films, often below 15 microns, to enable device miniaturization and improved performance. This growing demand across high-volume electronics production is a major driver of sustained market expansion.

High production costs present a significant restraint for the Modified Polyimide (MPI) Material market. The synthesis of MPI involves complex chemical processes, including high-temperature polymerization and precision coating technologies, which require specialized equipment and controlled environments. Manufacturing costs can be up to 30% higher than conventional polymer materials, limiting adoption among cost-sensitive industries. Additionally, raw materials such as specialty monomers and solvents are subject to price volatility, further increasing production expenses. Smaller manufacturers often face barriers to entry due to capital-intensive setup requirements. The need for stringent quality control, particularly in semiconductor applications, adds additional operational costs. These financial constraints can slow down widespread adoption, especially in emerging markets where cost efficiency remains a critical factor.

The rapid growth of electric vehicles presents substantial opportunities for the Modified Polyimide (MPI) Material market. MPI materials are increasingly used in battery insulation systems, power electronics, and high-voltage components due to their excellent thermal stability and dielectric properties. Electric vehicle production has grown by more than 35% annually, creating a strong demand for advanced insulation materials capable of operating under high thermal stress conditions. MPI films can enhance battery safety by reducing thermal runaway risks by up to 20%. Additionally, their lightweight nature contributes to overall vehicle efficiency improvements. As automakers invest heavily in next-generation battery technologies and power systems, the integration of MPI materials is expected to expand significantly, opening new revenue streams and application areas.

Stringent regulatory and environmental standards pose a notable challenge to the Modified Polyimide (MPI) Material market. Production processes often involve solvents and chemicals that are subject to strict environmental regulations, particularly in regions with rigorous emission control policies. Manufacturers are required to reduce volatile organic compound emissions by up to 30%, necessitating investment in cleaner technologies and alternative formulations. Compliance with global environmental standards increases operational complexity and costs. Additionally, waste management and recycling of polymer materials remain challenging, as MPI films are not easily biodegradable. Companies must invest in sustainable production methods and eco-friendly materials, which can delay product development cycles and increase capital expenditure, ultimately impacting overall market growth.

• 48% Surge in Flexible OLED Integration Across Consumer Electronics

The integration of Modified Polyimide (MPI) materials in flexible OLED displays has increased by approximately 48% over the past three years, driven by rising demand for foldable smartphones and rollable screens. MPI films with thickness below 12 microns are being adopted in over 65% of new flexible display designs due to their superior thermal stability and optical clarity. Manufacturers are also achieving up to 30% improvement in bending durability compared to conventional substrates. This trend is particularly strong in Asia-Pacific, where more than 70% of advanced display manufacturing lines now incorporate MPI-based substrates for enhanced device longevity and performance.

• 35% Growth in Semiconductor Packaging Applications

MPI materials are witnessing a 35% increase in adoption within semiconductor packaging, especially in high-frequency and high-density integrated circuits. Advanced packaging technologies such as fan-out wafer-level packaging are utilizing MPI coatings to improve thermal resistance by up to 28% and reduce signal interference by nearly 22%. Approximately 60% of next-generation semiconductor designs now rely on high-performance polymer layers like MPI for insulation and protection. This shift is being driven by the growing complexity of chip architectures and the need for reliable materials capable of operating under extreme thermal and electrical conditions.

• 42% Expansion in Electric Vehicle Insulation Usage

The electric vehicle sector has recorded a 42% rise in the use of MPI materials for battery insulation and power electronics. MPI films offer dielectric strength exceeding 300 kV/mm, enabling safer operation of high-voltage battery systems. Around 55% of newly developed EV battery modules now incorporate advanced polymer insulation solutions, including MPI, to mitigate thermal runaway risks by up to 20%. Additionally, lightweight MPI components contribute to overall vehicle efficiency improvements of nearly 10%, making them increasingly critical in EV design and manufacturing processes.

• 30% Adoption of Sustainable and Low-Emission Manufacturing Processes

Sustainability trends are reshaping MPI production, with nearly 30% of manufacturers transitioning toward low-emission and solvent-free processing technologies. These innovations have reduced volatile organic compound emissions by up to 35% while improving production efficiency by approximately 18%. Over 40% of new MPI production facilities are incorporating closed-loop solvent recovery systems and energy-efficient curing technologies. Regulatory pressures and corporate ESG commitments are accelerating this transition, particularly in Europe and North America, where compliance with environmental standards is a key operational priority.

The Modified Polyimide (MPI) Material market is segmented based on type, application, and end-user industries, each contributing uniquely to market expansion. By type, MPI films and coatings dominate due to their extensive use in flexible electronics and semiconductor packaging, accounting for a significant portion of material demand. Applications are heavily concentrated in electronics, which contributes over 55% of total usage, followed by automotive and aerospace sectors. End-user insights reveal that consumer electronics manufacturers remain the largest adopters, while electric vehicle and industrial electronics sectors are emerging rapidly. The segmentation reflects strong alignment with high-growth industries requiring thermal stability, flexibility, and high dielectric performance, reinforcing the strategic importance of MPI materials across global manufacturing ecosystems.

MPI films currently account for approximately 58% of total adoption, making them the leading segment due to their widespread use in flexible displays, printed circuits, and semiconductor insulation layers. Their ability to maintain structural integrity under temperatures exceeding 300°C and flexibility under repeated mechanical stress positions them as the preferred material in high-performance applications. MPI coatings hold around 27% share, primarily used for protective and insulating layers in advanced electronics. However, composite MPI materials are the fastest-growing segment, expanding at an estimated CAGR of 13%, driven by their enhanced mechanical strength and integration with nanomaterials for improved conductivity and thermal resistance. Other niche types, including MPI adhesives and laminates, collectively contribute nearly 15% of the market, serving specialized industrial and aerospace applications.

Flexible electronics dominate the application segment, accounting for approximately 52% of total MPI material usage due to the rapid expansion of foldable smartphones, wearable devices, and advanced display technologies. Semiconductor packaging follows with around 26% share, benefiting from the need for high-performance insulation materials in increasingly complex chip designs. Automotive applications, particularly electric vehicles, represent a growing segment and are expected to expand at a CAGR of 14%, driven by increasing demand for high-voltage insulation and thermal management solutions. Aerospace and industrial electronics collectively account for the remaining 22%, where MPI materials are valued for their durability and resistance to extreme environmental conditions.

Consumer electronics manufacturers represent the leading end-user segment, accounting for approximately 49% of total MPI material consumption, driven by high-volume production of smartphones, tablets, and wearable devices. Automotive manufacturers, particularly in the electric vehicle segment, hold around 21% share and are the fastest-growing end-user group, expanding at a CAGR of 15% due to increasing integration of MPI materials in battery systems and power electronics. Semiconductor manufacturers contribute approximately 18%, leveraging MPI for advanced chip packaging and insulation. Other industries, including aerospace and industrial equipment, collectively account for 12%, where MPI materials are used in high-reliability and extreme-condition applications.

Region Asia-Pacific accounted for the largest market share at 64% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 12.5% between 2026 and 2033.

Asia-Pacific dominates due to its extensive electronics manufacturing ecosystem, contributing over 70% of global OLED panel production and nearly 65% of semiconductor packaging output. China, Japan, and South Korea collectively account for more than 80% of MPI material consumption in the region, supported by production capacities exceeding 30,000 tons annually. North America holds approximately 18% market share, driven by high adoption in aerospace and advanced semiconductor industries, while Europe contributes around 12%, with strong demand from automotive electronics and sustainability-focused manufacturing. South America and the Middle East & Africa together account for nearly 6%, with gradual expansion linked to industrial modernization and energy sector investments. Regional demand patterns show over 55% of MPI usage concentrated in electronics, followed by 20% in automotive and 10% in aerospace applications.

North America accounts for approximately 18% of the Modified Polyimide (MPI) Material market, supported by strong demand from semiconductor manufacturing, aerospace, and defense industries. The region produces over 20% of advanced semiconductor components globally, requiring high-performance insulation materials like MPI. Government initiatives promoting domestic chip manufacturing have led to over 35% increase in fabrication facility investments. Regulatory frameworks emphasize environmental compliance, with mandates targeting up to 30% reduction in industrial emissions by 2030, encouraging adoption of eco-friendly MPI production methods. Technological advancements include AI-driven material optimization and precision coating systems improving efficiency by nearly 25%. A leading regional player is actively developing ultra-thin MPI films below 10 microns to support next-generation chip packaging. Consumer behavior reflects higher enterprise adoption, particularly in healthcare and financial technology sectors, where reliable and thermally stable materials are critical for high-performance computing systems.

Europe holds approximately 12% share of the Modified Polyimide (MPI) Material market, with key contributions from Germany, the United Kingdom, and France. The region’s strong automotive and industrial electronics sectors drive MPI demand, particularly in electric vehicle components and advanced control systems. Regulatory bodies are enforcing strict environmental standards, with targets to cut industrial emissions by over 40% by 2030, accelerating the shift toward sustainable MPI production processes. Adoption of emerging technologies such as solvent-free polymer synthesis and energy-efficient curing systems has increased by nearly 28%. A regional specialty chemical manufacturer is investing in advanced MPI coatings for EV battery insulation, improving thermal resistance by 20%. Consumer behavior shows a strong inclination toward environmentally compliant materials, with over 60% of manufacturers prioritizing sustainable procurement practices, reinforcing demand for low-emission MPI solutions.

Asia-Pacific leads the Modified Polyimide (MPI) Material market in both volume and consumption, accounting for over 64% of global demand. China, Japan, and South Korea are the top consuming countries, collectively producing more than 75% of global flexible display panels and over 65% of semiconductor packaging units. The region hosts large-scale manufacturing hubs with MPI production capacities exceeding 30,000 tons annually. Rapid infrastructure expansion in electronics manufacturing has increased demand for high-performance materials by nearly 40% over recent years. Technological innovation hubs are focusing on nano-enhanced MPI films and ultra-thin coatings below 8 microns. A major regional manufacturer has expanded production lines by 25% to meet rising demand from foldable smartphone producers. Consumer behavior is heavily driven by mobile device adoption and e-commerce growth, with over 70% of global smartphone production concentrated in this region.

South America represents approximately 4% of the Modified Polyimide (MPI) Material market, with Brazil and Argentina as key contributors. The region is experiencing gradual growth driven by industrial modernization and increased investment in energy infrastructure. Demand for MPI materials is rising in power electronics and industrial equipment, with usage increasing by nearly 18% in recent years. Government incentives supporting local manufacturing and renewable energy projects are encouraging adoption of high-performance insulation materials. Trade policies aimed at reducing import dependency have led to a 15% increase in domestic production capabilities. A regional chemical producer is focusing on MPI-based coatings for industrial applications, improving equipment durability by 12%. Consumer behavior is influenced by localized demand for durable and cost-effective materials, particularly in energy and industrial sectors.

The Middle East & Africa accounts for approximately 2% of the Modified Polyimide (MPI) Material market, with growth driven by infrastructure development and energy sector investments. Countries such as the UAE and South Africa are leading demand, particularly in oil and gas and construction-related applications. MPI materials are increasingly used in high-temperature insulation systems, with adoption rising by nearly 20% in industrial projects. Technological modernization initiatives have led to a 15% increase in advanced material usage across manufacturing sectors. Trade partnerships and regulatory frameworks are supporting industrial diversification, encouraging local adoption of high-performance polymers. A regional industrial supplier is introducing MPI-based insulation solutions that improve thermal efficiency by 18%. Consumer behavior reflects growing demand for durable materials capable of operating in extreme environmental conditions.

China – 46% share: Modified Polyimide (MPI) Material market leadership driven by extensive electronics manufacturing capacity and high-volume OLED and semiconductor production.

Japan – 21% share: Modified Polyimide (MPI) Material market strength supported by advanced material innovation and strong presence in high-performance electronics and automotive sectors.

The Modified Polyimide (MPI) Material market is moderately consolidated, with approximately 25–30 active global and regional players competing across high-performance polymer segments. The top five companies collectively account for nearly 55% of the total market share, reflecting a balance between established multinational corporations and specialized material innovators. Market leaders are focusing heavily on research and development, allocating up to 12% of their annual budgets toward advanced polymer technologies and nano-enhanced MPI materials. Strategic initiatives such as mergers, joint ventures, and long-term supply agreements have increased by over 20% in recent years, particularly in Asia-Pacific and North America. Product innovation remains a key competitive factor, with companies introducing ultra-thin MPI films below 10 microns and coatings with dielectric strength exceeding 300 kV/mm. Partnerships between material manufacturers and electronics companies are enabling faster commercialization of next-generation applications, including foldable displays and high-frequency semiconductor components. Additionally, sustainability is emerging as a competitive differentiator, with over 40% of leading players adopting low-emission production technologies and solvent recovery systems to align with global environmental standards.

DuPont

Kolon Industries

SKC Kolon PI

Kaneka Corporation

Toray Industries

Mitsubishi Gas Chemical Company

Sumitomo Chemical

Ube Industries

Taimide Tech Inc.

Flexcon Company

Arakawa Chemical Industries

PI Advanced Materials

Technological advancements in the Modified Polyimide (MPI) Material market are centered on enhancing thermal stability, mechanical flexibility, and dielectric performance to meet the evolving needs of high-performance electronics and industrial applications. One of the most significant developments is the introduction of ultra-thin MPI films below 8 microns, which have improved flexibility by over 30% and enabled next-generation foldable and rollable display technologies. These films maintain structural integrity at temperatures exceeding 350°C, making them highly suitable for advanced semiconductor packaging and aerospace applications.

Nanotechnology integration is another key innovation, with nano-reinforced MPI composites demonstrating up to 25% higher tensile strength and 20% improved thermal conductivity compared to conventional MPI materials. These enhancements are critical for high-frequency communication systems, including 5G infrastructure, where signal integrity and heat dissipation are essential. Additionally, advancements in plasma-enhanced chemical vapor deposition (PECVD) techniques have enabled more uniform MPI coatings, reducing material defects by nearly 18% and improving production yield.

Digital transformation is playing an increasingly important role, with AI-driven material design platforms reducing formulation development time by approximately 35%. Automated coating and curing systems have improved manufacturing efficiency by over 28%, while precision roll-to-roll processing technologies are enabling large-scale production with consistent quality. Sustainable manufacturing technologies are also gaining traction, with solvent-free synthesis methods reducing emissions by up to 40% and energy consumption by nearly 22%. These innovations collectively position MPI materials as a critical enabler of high-performance, energy-efficient, and environmentally compliant industrial solutions.

• In March 2025, DuPont expanded its Kapton® polyimide film production capacity in Asia to support rising demand from flexible electronics and semiconductor applications. The expansion increased output capability by over 20%, enabling faster delivery cycles and improved supply chain resilience. Source: www.dupont.com

• In September 2024, Kolon Industries announced the development of next-generation CPI (Colorless Polyimide) films with improved transparency exceeding 90% and enhanced flexibility for foldable display applications. The innovation is expected to improve device durability by approximately 25% in high-bend environments. Source: www.kolonindustries.com

• In November 2024, Toray Industries introduced advanced heat-resistant polyimide materials designed for electric vehicle battery insulation, offering thermal stability above 350°C and improving insulation performance by nearly 18% in high-voltage systems. Source: www.toray.com

• In February 2025, Kaneka Corporation enhanced its MPI film manufacturing process by implementing energy-efficient curing technologies, reducing energy consumption by 15% while maintaining high dielectric strength levels exceeding 300 kV/mm for electronic component applications. Source: www.kaneka.co.jp

The Modified Polyimide (MPI) Material Market Report provides a comprehensive analysis of key segments, technologies, applications, and regional dynamics shaping the industry landscape. The report covers multiple product types, including MPI films, coatings, composites, adhesives, and laminates, with films accounting for over 55% of total material utilization due to their extensive application in flexible electronics and semiconductor packaging. Application coverage spans flexible displays, integrated circuits, electric vehicle components, aerospace systems, and industrial electronics, collectively representing more than 85% of total MPI demand.

Geographically, the report evaluates major regions including Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, with Asia-Pacific contributing over 60% of global consumption driven by large-scale electronics manufacturing. The report also highlights emerging niche segments such as MPI applications in 5G communication infrastructure, where adoption has increased by over 30%, and electric vehicle battery insulation systems, where MPI materials improve thermal safety performance by up to 20%.

Technological scope includes advancements in nano-enhanced MPI composites, AI-driven material development, and sustainable manufacturing processes, with over 40% of new production facilities adopting low-emission technologies. The report further analyzes industry-specific adoption trends across consumer electronics, automotive, semiconductor, and aerospace sectors, supported by quantitative insights into material performance, production capacity, and application-specific requirements. This structured scope enables decision-makers to identify growth opportunities, assess competitive positioning, and align strategic investments with evolving market demands.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

11% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

DuPont, Kolon Industries, SKC Kolon PI, Kaneka Corporation, Toray Industries, Mitsubishi Gas Chemical Company, Sumitomo Chemical, Ube Industries, Taimide Tech Inc., Flexcon Company, Arakawa Chemical Industries, PI Advanced Materials |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |