Reports

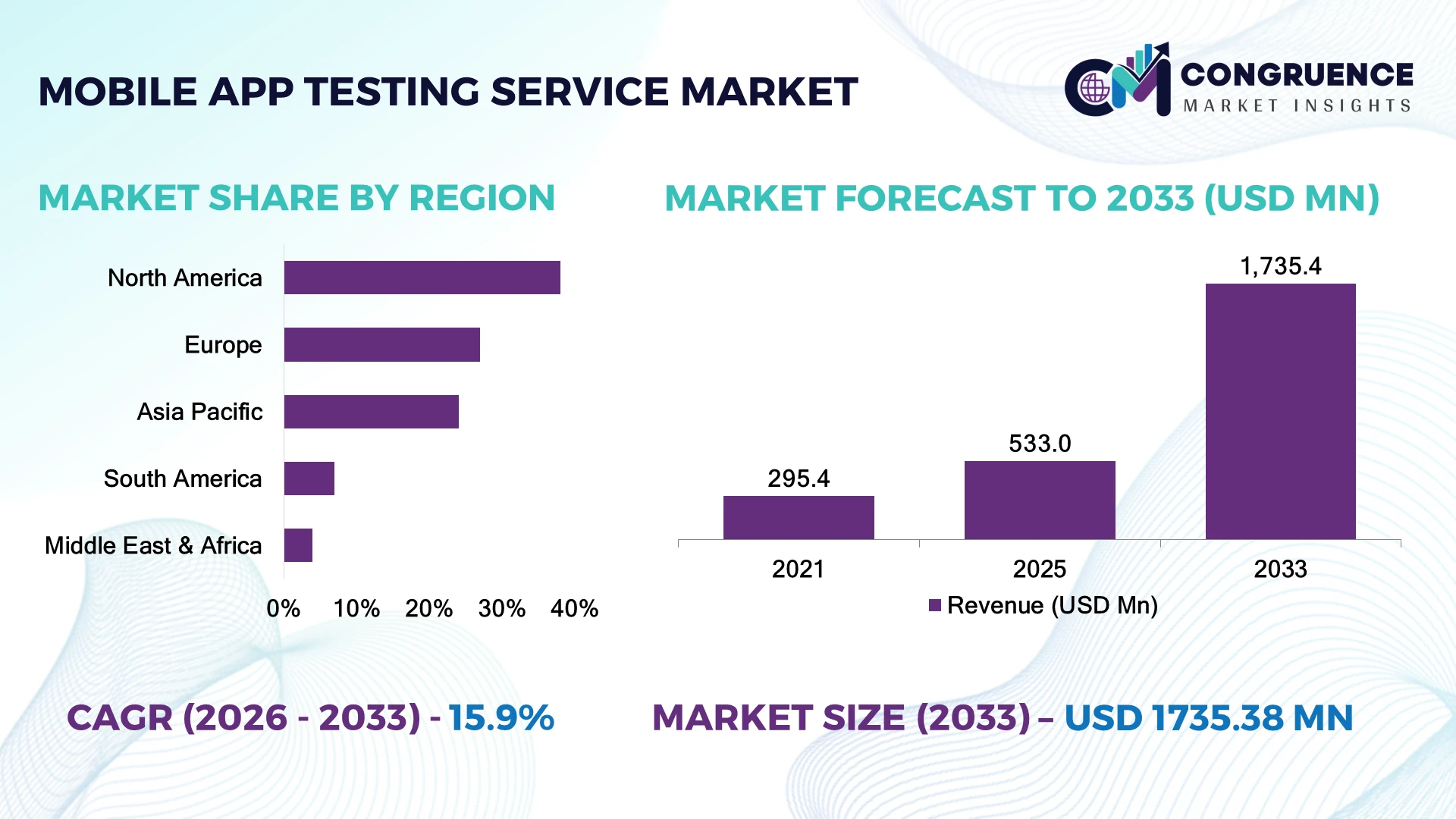

The Global Mobile App Testing Service Market was valued at USD 533.0 Million in 2025 and is anticipated to reach a value of USD 1,735.4 Million by 2033 expanding at a CAGR of 15.9% between 2026 and 2033. Growth is driven by AI-powered testing automation, rising mobile-first banking and healthcare applications, and increasing demand for faster cross-platform releases across enterprise ecosystems.

The United States leads the global landscape with nearly 35% market share, supported by strong investments from technology firms, cloud providers, and financial services companies. China follows with over 25% share, driven by large-scale mobile commerce and 5G-enabled application ecosystems. The U.S. enterprise sector deploys automated testing in more than 60% of software workflows, while China’s mobile payment platforms process billions of transactions annually. Europe is advancing through strict digital compliance requirements introduced under frameworks such as the EU Digital Services Act, accelerating secure app validation.

Strategic investment in AI-based testing platforms and regional delivery centers will define competitive advantage.

Market Size & Growth: USD 533.0 Million in 2025 expanding to USD 1,735.4 Million by 2033 at 15.9% CAGR, driven by AI automation and enterprise mobile transformation.

Top Growth Drivers: AI testing adoption (40%+), cloud-based testing demand (35%+), mobile enterprise applications (30%+).

Short-Term Forecast: By 2028, automated testing workflows are expected to reduce release cycles by 40% and improve defect detection efficiency by 50%.

Emerging Technologies: AI-driven test generation, robotic process automation, and cloud device labs are reshaping advanced mobile application validation.

Regional Leaders: North America projected near USD 600 Million, Asia Pacific above USD 700 Million, and Europe exceeding USD 350 Million by 2033, supported by cloud adoption and digital modernization.

Consumer/End-User Trends: Over 70% of enterprises prioritize mobile app quality testing to improve user experience and reduce application failures.

Pilot/Case Example: In 2024, AI-based testing deployments improved regression testing speed by approximately 60% for large-scale software teams.

Competitive Landscape: Leading providers include Accenture, Capgemini, Cognizant, IBM, and Infosys, competing through automation platforms and global delivery networks.

Regulatory & ESG Impact: Secure testing practices help organizations achieve up to 30% lower compliance-related risks through improved data protection and application governance.

Investment & Funding: More than USD 5 Billion has been directed toward AI software infrastructure and automation partnerships, accelerating next-generation testing capabilities.

Innovation & Future Outlook: Autonomous testing agents, predictive analytics, and continuous testing pipelines are driving the next phase of mobile software quality management.

The Mobile App Testing Service Market is expanding as enterprises prioritize reliable digital experiences across banking, healthcare, retail, and government applications. Recent innovations include AI-assisted test case creation, real-device cloud platforms, and predictive defect analytics, with automated approaches improving testing productivity by more than 50%. Global companies are also adapting to operational changes caused by distributed software teams and stricter application security requirements, creating new opportunities for advanced testing providers.

The Mobile App Testing Service Market is becoming strategically important as organizations compete through seamless digital experiences, application reliability, and faster software delivery. Businesses are shifting from traditional manual validation toward continuous testing models to support rapid mobile releases, particularly as cloud-native development and cybersecurity requirements reshape technology strategies.

Modern AI-driven testing platforms improve efficiency by automatically generating test scenarios and identifying defects, reducing validation time by nearly 50% compared with conventional manual processes. North America maintains strong adoption due to mature enterprise software ecosystems, while Asia Pacific is expanding rapidly through mobile commerce growth, 5G infrastructure deployment, and large-scale digital service adoption. Regulatory developments such as stricter privacy requirements in Europe are also increasing demand for secure application testing frameworks.

Companies are deploying cloud-based device testing environments to support global development teams, reduce hardware dependency, and accelerate release cycles. Leading technology providers are strengthening partnerships around automation, artificial intelligence, and managed testing services to improve scalability. Over the next few years, competitive positioning will depend on the ability to deliver intelligent, secure, and continuously optimized mobile application quality solutions across diverse digital ecosystems.

The rapid adoption of AI-powered testing platforms is becoming a major growth catalyst as enterprises prioritize faster and more reliable mobile application releases. Automated testing solutions now improve test execution efficiency by 50%–70% while reducing repetitive validation workloads by nearly 40%. In the United States, financial services and healthcare companies are expanding continuous testing frameworks to meet rising digital service expectations and cybersecurity requirements. The shift toward cloud-based development and DevOps integration is pushing providers to invest in AI test generation, predictive analytics, and global delivery capabilities. Companies are responding through strategic partnerships, automation-focused R&D, and expansion of managed testing services to support complex mobile ecosystems.

Mobile application testing providers face increasing operational pressure from device fragmentation, security requirements, and infrastructure expenses. More than 15,000 mobile device configurations globally create significant compatibility testing challenges, while enterprises allocate 20%–30% of software budgets toward quality assurance activities. In countries such as India and the Philippines, expanding testing operations requires continuous investment in skilled engineering resources and advanced device laboratories. Data privacy regulations in Europe and North America further increase compliance workloads, affecting deployment timelines and service costs. Companies are reducing exposure through cloud-based device farms, localized testing centers, automation adoption, and long-term enterprise contracts to improve scalability and cost control.

The integration of artificial intelligence, machine learning, and autonomous testing workflows is creating significant opportunities for service providers. AI-based test automation can reduce regression testing efforts by 60% while improving defect identification accuracy by more than 45%. Countries including Japan and South Korea are increasing investments in mobile AI ecosystems, smart devices, and advanced digital platforms, creating demand for specialized testing capabilities. The growth of low-code development is also expanding testing requirements among non-technical business teams. Companies are positioning through AI research, strategic alliances with cloud providers, and ecosystem partnerships to deliver predictive quality management, enabling faster releases and improved application performance.

The increasing complexity of mobile ecosystems creates execution challenges for testing service providers, particularly around security validation, API integration, and multi-platform compatibility. More than 70% of enterprises identify application security as a critical priority, while over 50% of mobile applications require continuous updates across multiple operating systems and connected services. In markets such as the United States and Germany, stricter cybersecurity frameworks are increasing testing requirements and operational workloads. The shortage of advanced automation specialists further impacts service consistency and delivery speed. Companies must strengthen cybersecurity testing capabilities, invest in skilled engineering teams, and develop advanced AI-driven frameworks to maintain competitiveness and ensure reliable deployment across global mobile platforms.

AI-Powered Testing Expansion AI-driven testing platforms are transforming mobile quality assurance workflows, with more than 50% of enterprises adopting intelligent automation for test creation, defect prediction, and regression analysis. Companies are integrating machine learning models with DevOps pipelines to reduce testing cycles by 40%–60% and improve release accuracy. The growing use of generative AI in software development is accelerating investments in autonomous testing frameworks, especially among technology firms in the United States and India.

Cloud Device Testing Growth Cloud-based mobile testing environments are replacing physical device labs as enterprises seek scalable validation across thousands of device and operating system combinations. More than 60% of large software teams now prioritize cloud testing infrastructure to improve accessibility and reduce hardware maintenance costs by nearly 30%. Companies are expanding partnerships with cloud providers and investing in remote testing platforms to support globally distributed development teams.

Security Testing Integration Mobile application security testing is becoming a core operational requirement as data privacy regulations and cyber threats increase. Over 70% of enterprises include security validation within mobile application testing workflows, while automated vulnerability detection adoption has increased by more than 35%. Organizations are restructuring testing processes to combine performance, compliance, and security assessments within unified platforms.

Continuous Testing Adoption Continuous testing models are reshaping software delivery as businesses move toward faster mobile application updates and shorter development cycles. Enterprises implementing continuous testing achieve approximately 45% faster deployment workflows and improved defect identification rates. Companies are expanding automation capabilities and restructuring quality teams to support agile development, particularly as supply-chain digitization increases dependency on reliable mobile platforms.

Automated testing dominates the Mobile App Testing Service Market, accounting for approximately 65% of adoption due to its scalability, faster execution, and ability to handle complex application environments. Enterprises prefer automated frameworks because they reduce repetitive testing workloads by nearly 50% and support continuous integration across Android, iOS, and hybrid platforms. Manual testing remains important for usability analysis and exploratory testing, holding strategic value in customer-facing applications where human evaluation is critical. AI-powered testing is the fastest-growing segment, expanding as companies adopt intelligent test generation, predictive analytics, and self-healing automation capabilities. Adoption among large enterprises has increased by more than 40% as software teams seek faster release cycles and improved defect management. Companies are increasing investment in AI testing platforms, cloud-based automation tools, and specialized partnerships to strengthen quality assurance operations.

Enterprise mobile applications represent the leading application segment with nearly 45% market share, supported by widespread adoption across banking, healthcare, retail, and corporate mobility solutions. Organizations rely on testing services to ensure application stability, regulatory compliance, and seamless user experiences across multiple devices. Mobile banking and healthcare applications are particularly testing-intensive, with security and performance validation representing more than 50% of testing priorities. Consumer applications are the fastest-growing application area as companies compete through digital engagement, personalization, and rapid feature releases. The expansion of mobile commerce, digital payments, and subscription platforms is increasing demand for continuous testing capabilities. Gaming, social platforms, and on-demand services are also strengthening adoption through advanced performance testing requirements. Companies are expanding automated testing coverage, integrating analytics tools, and deploying cloud testing environments to manage increasing application complexity and user expectations.

Large enterprises account for approximately 60% of Mobile App Testing Service adoption due to extensive application portfolios, higher security requirements, and complex technology environments. Financial institutions, healthcare providers, and multinational corporations require continuous testing capabilities to maintain compliance and operational reliability. These organizations typically allocate larger technology budgets toward automation platforms, managed testing services, and specialized quality engineering teams. Small and medium-sized enterprises represent the fastest-growing end-user segment as cloud-based testing services lower entry barriers and reduce infrastructure requirements. More than 35% of SMEs are increasing investment in outsourced testing solutions to access advanced capabilities without maintaining large internal teams. Technology startups are also adopting flexible testing models to accelerate product launches and improve application reliability. Service providers are responding through customized packages, subscription-based testing models, and partnerships with cloud infrastructure companies to address diverse enterprise requirements. The market is shifting toward scalable testing ecosystems that support both large digital enterprises and emerging software companies.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of17.2% between 2026 and 2033.

North America represents the leading Mobile App Testing Service Market due to strong enterprise software adoption, advanced cloud infrastructure, and high investment in digital application quality management. The region contributes approximately 38% of global demand, supported by large technology companies, financial institutions, healthcare providers, and government digital platforms. More than 65% of large enterprises in the United States integrate automated testing into software development workflows to accelerate deployment and improve application reliability. Cloud-based device testing, AI-powered validation, and continuous integration frameworks are becoming standard practices. Companies are expanding automation capabilities, strengthening cybersecurity testing partnerships, and investing in managed quality engineering services to support increasingly complex mobile ecosystems.

United States Market Outlook: The United States remains the dominant country market due to its concentration of software enterprises, cloud providers, and digital-first industries. Over 70% of large U.S. organizations prioritize mobile application performance and security testing as part of their digital transformation programs. Strong adoption across banking, healthcare, retail, and enterprise mobility sectors continues to drive demand for advanced testing platforms, AI-based automation, and specialized engineering services.

Europe is witnessing steady expansion in mobile application testing services as enterprises prioritize secure software delivery, privacy compliance, and reliable digital platforms. The region accounts for nearly 27% of market demand, supported by Germany, the United Kingdom, France, and Nordic technology hubs. Increasing enforcement of data protection requirements and cybersecurity standards is encouraging organizations to integrate security testing throughout development workflows. More than 60% of European enterprises emphasize application quality assurance to reduce operational risks and improve customer experience. Companies are investing in automated compliance testing, cloud-based validation environments, and partnerships with specialized testing providers to address complex regulatory requirements.

Germany Market Outlook: Germany leads European adoption due to its strong industrial digitalization ecosystem and enterprise software investments. Over 50% of large German companies are accelerating automation across software operations, including application testing and quality management. The country’s manufacturing, automotive, and financial sectors are increasing demand for reliable mobile platforms that support connected services, workforce applications, and digital customer interactions.

Asia-Pacific is the fastest-growing market for Mobile App Testing Services, driven by rapid mobile adoption, expanding software development centers, and large-scale digital transformation programs. The region contributes approximately 24% of global demand, with China, India, Japan, and South Korea representing major deployment hubs. More than 70% of enterprises in leading Asian technology markets are increasing investment in automated testing solutions to support frequent application releases. Growing 5G deployment, mobile commerce expansion, and cloud migration are creating demand for scalable testing environments. Companies are expanding offshore testing centers, forming technology partnerships, and deploying AI-enabled platforms to improve software delivery efficiency.

India Market Outlook: India has become a strategic testing hub due to its large IT services ecosystem, engineering workforce, and global software delivery capabilities. Over 40% of outsourced application testing activities are supported by Indian service providers serving international enterprises. Increasing investments in AI engineering, cloud platforms, and digital infrastructure are strengthening the country’s position as a preferred destination for mobile testing operations.

South America is developing as an emerging Mobile App Testing Service Market supported by fintech growth, mobile banking adoption, and enterprise digitalization initiatives. The region contributes around 7% of global demand, with Brazil and Argentina representing key technology markets. Increasing smartphone penetration and digital payment adoption are encouraging companies to improve application stability, security, and performance. More than 50% of financial technology companies in major South American economies prioritize application testing to maintain reliable digital services. However, infrastructure variation and limited specialized testing resources continue to influence deployment strategies. Companies are addressing these challenges through cloud testing platforms, regional partnerships, and outsourced quality engineering models.

Brazil Market Outlook: Brazil is the largest South American market due to its expanding fintech sector, large mobile user base, and enterprise digitization efforts. Digital banking platforms account for a significant portion of mobile application testing demand, with more than 60% of financial institutions increasing investments in application security and performance validation. Local technology partnerships are supporting broader adoption of advanced testing solutions.

The Middle East & Africa market is expanding through government digital transformation programs, smart city initiatives, and enterprise modernization projects. The region represents approximately 4% of global demand, with the United Arab Emirates, Saudi Arabia, and South Africa emerging as important technology centers. Investments in cloud infrastructure, digital government platforms, and financial technology services are increasing the need for secure and scalable application testing. More than 45% of organizations in major Middle Eastern technology markets are adopting automation-driven software quality processes. Companies are strengthening regional delivery capabilities, partnering with global testing specialists, and deploying cloud-based solutions to support faster application development.

United Arab Emirates Market Outlook: The UAE leads regional adoption through advanced digital infrastructure, smart government initiatives, and strong enterprise technology investment. More than 80% of government services have transitioned to digital platforms, increasing demand for reliable mobile applications and continuous testing capabilities. The country’s focus on AI adoption, cybersecurity, and smart services is creating opportunities for specialized mobile testing providers.

The Mobile App Testing Service Market features global quality engineering leaders competing with regional testing specialists, automation innovators, and cost-focused outsourcing providers. Major players such as Accenture, Capgemini, IBM, Cognizant, Infosys, and Tricentis compete through AI automation, cloud testing, and enterprise customization. The top five providers collectively account for approximately 35%–40% of market activity, reflecting a fragmented but technology-driven structure. Competition is based on automation capability (60%+ enterprise adoption), delivery speed improvements (40%–50% faster testing cycles), pricing flexibility, and specialized industry expertise. Companies are expanding global delivery centers, forming cloud partnerships, and integrating AI-powered testing platforms. The competitive shift is moving from labor-based testing toward autonomous quality engineering, increasing pressure on traditional service models. High entry barriers include enterprise relationships, security compliance, device infrastructure, and skilled automation teams. Winning players must combine AI innovation, scalable delivery, and deep industry specialization.

Capgemini

Cognizant

IBM

Infosys

Wipro

Tata Consultancy Services (TCS)

Tricentis

Applause

Sauce Labs

BrowserStack

Keysight Technologies

Qualitest

EPAM Systems

Artificial intelligence and machine learning are becoming central technologies in mobile application testing by enabling automated test creation, predictive defect detection, and self-healing workflows. AI-based testing platforms improve test maintenance efficiency by 40%–60% compared with traditional scripted approaches, while adoption among large software teams has exceeded 50%. Companies benefit through faster releases, reduced manual workloads, and improved application reliability across complex digital environments.

Cloud-based device testing is replacing physical testing labs as enterprises require access to diverse smartphones, operating systems, and global deployment environments. Cloud platforms reduce infrastructure requirements by approximately 30% and improve testing coverage by more than 40% through scalable device access. Technology leaders and service providers are expanding cloud partnerships to support distributed development teams and continuous delivery models.

Between 2026 and 2028, autonomous testing agents, generative AI, and advanced analytics will reshape competitive positioning. Compared with legacy manual validation, intelligent testing workflows deliver significant efficiency improvements by automating repetitive activities and prioritizing high-risk defects. Global technology providers with AI capabilities, cloud ecosystems, and industry-specific testing expertise will gain the strongest advantage as enterprises shift toward continuous quality engineering.

June 2025Tricentis introduced agentic AI testing capabilities, including MCP servers and autonomous test automation workflows, improving enterprise testing productivity with reported early-user test creation time savings of up to 85%. The launch strengthens AI-driven quality engineering adoption for large software teams. Source: www.tricentis.com

April 2025Tricentis expanded Tosca with cloud-based test data capabilities, enabling automated test data management and reducing manual preparation efforts for enterprise testing environments. The update supports faster automation deployment and improves scalability for complex application validation workflows. Source: www.tricentis.com

2025Wipro and HeadSpin strengthened their digital testing collaboration by combining global IT delivery capabilities with AI-powered mobile performance insights across more than 60 deployment locations. The partnership improves enterprise application monitoring, automation coverage, and digital experience optimization. Source: www.wipro.co

July 2025Drizz secured USD 2.7 million in funding to expand its AI-based mobile testing platform, supporting product development and global scaling initiatives. The investment highlights rising demand for automated mobile quality solutions among emerging technology providers.

The Mobile App Testing Service Market Report covers comprehensive analysis across testing types, applications, end-users, regional markets, competitive positioning, and technology developments. The study evaluates automated testing, manual testing, AI-powered solutions, enterprise applications, consumer applications, and industry-specific deployment patterns across North America, Europe, Asia-Pacific, South America, and Middle East & Africa.

The report provides strategic insights into adoption trends, cloud testing expansion, automation integration, cybersecurity requirements, and emerging intelligent testing platforms. It evaluates major service providers, competitive strategies, investment priorities, and innovation pathways to support business expansion, partnership decisions, and technology planning. The analysis highlights enterprise adoption patterns and market opportunities shaping the industry direction from 2026 to 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 533.0 Million |

| Market Revenue (2033) | USD 1,735.4 Million |

| CAGR (2026–2033) | 15.9% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Accenture; Capgemini; Cognizant; IBM; Infosys; Wipro; Tata Consultancy Services (TCS); Tricentis; Applause; Sauce Labs; BrowserStack; Keysight Technologies; Qualitest; EPAM Systems |

| Customization & Pricing | Available on Request (10% Customization Free) |