Reports

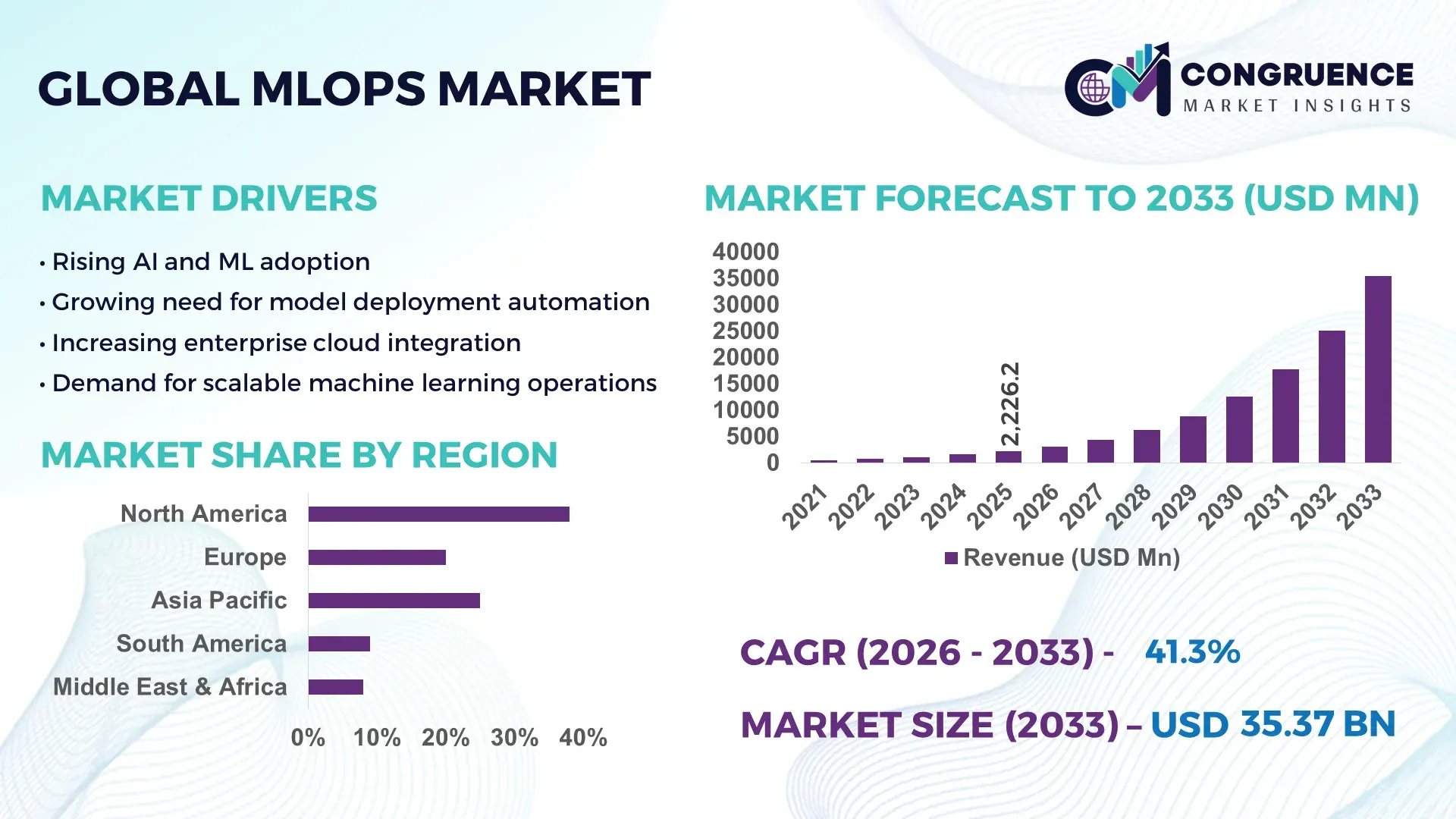

The Global MLOps Market was valued at USD 2226.17 Million in 2025 and is anticipated to reach a value of USD 35375 Million by 2033 expanding at a CAGR of 41.3% between 2026 and 2033. Rapid enterprise-scale AI deployment is driving the need for automated model lifecycle management and governance.

The United States represents the most technologically advanced environment for MLOps implementation, supported by over USD 25 Billion in annual enterprise AI infrastructure investments and more than 60% of large enterprises operating dedicated ML platforms. Cloud-native ML workloads exceed 70% adoption among Fortune 1000 firms, while hyperscale data center capacity surpassed 12 GW dedicated to AI and analytics processing. Key applications include financial risk modeling, precision healthcare diagnostics, autonomous systems testing, and real-time retail analytics. Over 55% of AI development teams utilize automated CI/CD pipelines for model deployment, and more than 40% have implemented model monitoring frameworks integrating drift detection and explainability tools, reflecting strong technological maturity in orchestration, governance, and scalable ML infrastructure.

Market Size & Growth: Valued at USD 2226.17 Million in 2025, projected to reach USD 35375 Million by 2033 at a CAGR of 41.3%, driven by enterprise AI operationalization.

Top Growth Drivers: AI adoption rate increase 48%, model deployment automation efficiency gain 35%, cloud ML workload expansion 52%.

Short-Term Forecast: By 2028, automated pipelines expected to reduce ML deployment costs by 30% and improve model performance stability by 25%.

Emerging Technologies: Federated learning operations, automated model observability platforms, and generative AI lifecycle orchestration.

Regional Leaders: North America USD 14200 Million by 2033 with cloud-native ML adoption surge; Europe USD 9200 Million driven by AI governance frameworks; Asia-Pacific USD 8300 Million supported by industrial AI scaling.

Consumer/End-User Trends: BFSI and healthcare lead adoption, with over 45% of enterprises standardizing model monitoring and governance workflows.

Pilot or Case Example: 2025 manufacturing pilot achieved 28% predictive maintenance accuracy improvement and 22% downtime reduction via automated retraining pipelines.

Competitive Landscape: Microsoft holds approximately 18% share, followed by Google, AWS, IBM, and Databricks.

Regulatory & ESG Impact: AI governance mandates and data privacy regulations accelerating demand for explainability, auditability, and sustainable cloud operations.

Investment & Funding Patterns: Over USD 18 Billion in recent AI infrastructure and MLOps-focused venture funding, with rising investment in platform automation.

Innovation & Future Outlook: Integration of AI governance automation, low-code ML orchestration, and edge AI lifecycle management shaping next-generation platforms.

Financial services, healthcare, retail, and manufacturing collectively account for over 65% of MLOps adoption, with BFSI contributing roughly 22% through fraud detection and risk analytics workloads. Recent innovations include automated feature stores, real-time model observability dashboards, and policy-driven AI governance layers. Regulatory pressure for transparent AI, combined with sustainability goals for energy-efficient data centers, is influencing platform design. North America and Asia-Pacific exhibit the highest consumption growth due to hyperscale cloud expansion and industrial AI deployment, while Europe emphasizes compliance-driven implementations. Emerging trends include edge-based MLOps, synthetic data pipelines, and autonomous retraining systems, indicating strong long-term enterprise integration of AI lifecycle management.

MLOps has become a strategic backbone for enterprises transitioning from experimental artificial intelligence initiatives to fully operational, revenue-impacting AI systems. Organizations deploying structured MLOps frameworks report up to 45% faster model deployment cycles and 30% improvement in model reliability compared with fragmented development approaches. Automated model monitoring combined with continuous integration pipelines delivers a 40% improvement in production stability compared to manual deployment standards. North America dominates in deployment volume due to hyperscale cloud infrastructure, while Europe leads in regulated adoption, with over 58% of large enterprises implementing formal AI governance frameworks.

By 2028, AI-driven automation in model retraining is expected to cut operational ML maintenance costs by 32% while improving prediction accuracy consistency by 27%. Firms are committing to ESG-aligned digital infrastructure improvements, targeting 35% reductions in data center energy intensity by 2030 through optimized AI workload orchestration. In 2025, a large-scale banking deployment in the United States achieved a 26% reduction in fraud detection latency through real-time model monitoring and automated rollback systems. Future pathways emphasize low-code ML orchestration, edge AI lifecycle automation, and explainable AI governance platforms. As enterprises prioritize resilience, auditability, and sustainable computing, the MLOps Market is emerging as a critical pillar enabling scalable innovation, regulatory compliance, and long-term digital competitiveness.

Enterprise AI deployment has expanded beyond pilot phases, with over 65% of large organizations operating multiple production ML models. Each model requires lifecycle management, including validation, monitoring, and retraining, creating operational complexity that manual systems cannot handle efficiently. Automated MLOps pipelines reduce deployment errors by nearly 35% and improve cross-team collaboration through standardized workflows. Industries such as banking and healthcare rely on real-time decision models where system downtime directly impacts service continuity. The need for explainability and traceability further drives adoption of governance-integrated MLOps platforms. Additionally, multi-cloud strategies adopted by more than 50% of enterprises require unified orchestration layers, strengthening demand for centralized ML operations frameworks capable of maintaining performance, compliance, and scalability.

Despite strong demand, implementation complexity remains a barrier. Nearly 48% of organizations report difficulty integrating MLOps tools with legacy IT systems and fragmented data environments. Skilled professionals capable of bridging data science, software engineering, and DevOps expertise remain limited, with AI engineering roles growing faster than supply. Toolchain fragmentation, involving multiple open-source and proprietary platforms, increases operational overhead and slows standardization. Security concerns also restrain adoption, particularly in regulated industries where model pipelines must align with strict audit requirements. Smaller enterprises face challenges in justifying infrastructure investments and managing ongoing platform maintenance, limiting broader market penetration despite technological readiness.

Edge computing expansion is creating new operational requirements, with over 40% of industrial AI workloads expected to run outside centralized data centers. This shift opens opportunities for edge-focused MLOps platforms capable of remote monitoring and autonomous model updates. Automated governance tools are also gaining traction as enterprises seek to comply with emerging AI regulations. Model explainability frameworks and bias detection modules integrated into pipelines enable regulatory alignment and risk reduction. Growth in synthetic data generation further enhances opportunities by enabling faster model training cycles. Emerging sectors such as autonomous mobility, smart manufacturing, and digital health monitoring require continuous model optimization, positioning advanced MLOps capabilities as essential infrastructure.

Evolving global AI regulations introduce operational burdens, as enterprises must document model lineage, validation procedures, and risk mitigation strategies. Compliance processes can increase deployment timelines by 20–25%. Infrastructure costs also present challenges, particularly for high-performance computing environments required for large-scale model training and monitoring. Energy consumption of AI workloads has drawn scrutiny, prompting investment in efficiency optimization. Data sovereignty rules restrict cross-border data transfers, complicating centralized MLOps implementations. Additionally, maintaining consistent performance across multi-cloud and hybrid environments requires advanced orchestration capabilities, increasing operational overhead and technical complexity for organizations managing large AI portfolios.

• Automated Model Observability Adoption Surpasses 60% in Enterprise AI Environments

More than 60% of enterprises running production ML workloads have integrated automated observability platforms that track data drift, model bias, and performance degradation in real time. Organizations using continuous monitoring report 35% fewer model failures and 28% faster issue resolution cycles. Over 50% of AI teams now deploy automated alerting mechanisms, enabling response times under 15 minutes for critical model anomalies.

• Cloud-Native MLOps Pipelines Handling Over 70% of New ML Deployments

Cloud-based orchestration frameworks now support over 70% of newly deployed machine learning models, driven by scalability and cross-regional workload balancing. Enterprises leveraging containerized ML pipelines achieve 32% faster deployment times and 25% improvement in resource utilization. Multi-cloud MLOps strategies have grown by 40% in adoption, reducing infrastructure dependency risks while enhancing operational continuity.

• Automated Retraining Frameworks Improving Model Accuracy by 30%

Continuous learning systems are becoming standard, with 55% of organizations implementing scheduled or event-triggered model retraining. These frameworks deliver up to 30% improvement in predictive accuracy consistency while reducing manual intervention by 45%. In data-intensive sectors such as finance and manufacturing, retraining cycles have shortened from quarterly to weekly intervals, increasing responsiveness to data shifts.

• AI Governance Integration Expands Beyond 50% of Regulated Industries

Over 50% of enterprises in regulated sectors have embedded AI governance modules directly into MLOps workflows, ensuring traceability and audit readiness. Explainability tools now cover approximately 48% of deployed enterprise models, supporting compliance with algorithm transparency mandates. Automated documentation and policy enforcement systems reduce audit preparation time by 33%, strengthening operational accountability.

The MLOps market segmentation reflects how organizations structure machine learning operations across infrastructure, lifecycle functions, and industry use cases. By type, platforms and integrated toolchains dominate adoption as enterprises consolidate model development, deployment, monitoring, and governance into unified environments; more than 65% of production ML teams now use end-to-end orchestration stacks rather than isolated tools. By application, model deployment and monitoring together account for over 50% of operational focus, as enterprises prioritize reliability, drift control, and performance optimization in live environments. Data management and CI/CD automation are expanding rapidly, with over 55% of AI teams formalizing version control and reproducibility standards. From an end-user perspective, BFSI, healthcare, and retail collectively represent more than 60% of demand due to real-time analytics, regulatory oversight, and customer personalization requirements. Manufacturing and telecom sectors are increasing adoption for predictive maintenance and network optimization, reflecting broader industrial AI operationalization.

MLOps platforms represent the leading type, accounting for approximately 46% of adoption, as enterprises prefer unified environments combining experiment tracking, pipeline orchestration, and monitoring. These platforms reduce deployment errors by nearly 35% and improve cross-team productivity by 30%, supporting large-scale AI portfolios. Cloud-based MLOps environments follow with about 32% share, driven by elastic compute and multi-region deployment needs. However, managed MLOps services are the fastest-growing type, expanding at an estimated 38% CAGR as organizations address skill shortages and outsource lifecycle management to specialized providers. Professional services, including consulting and integration, hold roughly 14%, while on-premise systems account for 8%, mainly in regulated sectors requiring strict data residency. Combined, these remaining segments contribute 22% of deployments, serving niche security and customization needs.

Model deployment and lifecycle management lead applications with nearly 34% share, as enterprises shift from experimentation to scalable production systems. Automated monitoring and performance management follow at 27%, reflecting the need to control drift and maintain reliability in dynamic data environments. Governance, risk, and compliance functions are expanding rapidly and represent the fastest-growing application area, rising at approximately 36% CAGR due to global AI oversight requirements. Data management and feature engineering contribute about 21%, supporting reproducibility and data lineage tracking, while CI/CD automation and retraining workflows account for a combined 18%, enhancing agility. Together, these remaining applications form 39% of use cases, supporting end-to-end ML lifecycle maturity.

Banking, Financial Services, and Insurance lead adoption with approximately 28% share, supported by fraud detection, credit risk scoring, and algorithmic trading models requiring continuous monitoring and governance. Healthcare and life sciences follow at 22%, where clinical AI validation and regulatory oversight demand structured lifecycle controls. Retail and e-commerce account for 16%, leveraging recommendation engines and demand forecasting. Manufacturing is the fastest-growing end-user segment, expanding at an estimated 37% CAGR as predictive maintenance and quality analytics scale across Industry 4.0 initiatives. IT & telecommunications, government, and energy sectors collectively contribute around 34%, focusing on network optimization, digital public services, and smart grid analytics.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 44% between 2026 and 2033.

Over 70% of enterprises in North America operate production AI workloads, with more than 55% integrating automated model monitoring systems. Europe represents 27% of global adoption, driven by regulatory-compliant AI frameworks across more than 40% of large enterprises. Asia-Pacific holds 24% share, supported by rapid digitalization across China, India, and Japan, where enterprise AI pilot-to-production conversion rates exceed 50%. South America contributes 6%, while the Middle East & Africa account for 5%, with increasing demand from energy, telecom, and public-sector digital transformation programs. Cloud-based ML infrastructure supports over 68% of regional deployments globally, and more than 48% of organizations are adopting multi-cloud MLOps strategies to ensure resilience and compliance.

How is enterprise AI industrialization transforming operational ML pipelines?

This region holds approximately 38% of global MLOps adoption, with strong demand from BFSI, healthcare, and retail sectors where over 60% of AI models operate in real-time decision environments. Government-backed AI initiatives and updated data governance frameworks are encouraging responsible AI deployment across federal and private sectors. More than 65% of enterprises use automated CI/CD pipelines for model lifecycle management. A leading cloud provider headquartered in this region expanded its AI platform capabilities in 2025 by integrating advanced model observability tools, improving enterprise deployment efficiency by 28%. Consumer behavior reflects higher enterprise spending on compliance-driven AI systems, particularly in finance and healthcare analytics.

Why are compliance-first AI frameworks accelerating structured ML operations?

Europe accounts for roughly 27% of the market, with Germany, the UK, and France representing over 60% of regional AI infrastructure investment. Regulatory frameworks emphasizing algorithm transparency have led to 58% of large enterprises implementing explainability and audit-ready ML pipelines. Sustainability initiatives targeting 30% reductions in digital infrastructure emissions by 2030 are influencing energy-efficient model orchestration. Adoption of automated governance tools has risen by 35% across financial institutions. A prominent European enterprise software firm introduced AI lifecycle compliance modules in 2025, enabling automated documentation for over 10,000 enterprise ML deployments. Regional consumer behavior shows preference for privacy-centric AI operations.

What is driving scalable AI lifecycle automation across emerging digital economies?

Asia-Pacific ranks second in volume, representing 24% of adoption, with China, India, and Japan leading consumption. Over 50% of enterprises in these countries are transitioning AI pilots into production systems. Growth is linked to expanding hyperscale data center capacity, exceeding 9 GW dedicated to AI and analytics processing. Innovation hubs in Bangalore, Shenzhen, and Tokyo support rapid ML engineering advancements. A major regional technology firm deployed automated ML monitoring across its e-commerce ecosystem in 2025, reducing model downtime by 22%. Consumer patterns emphasize mobile-first AI services, digital payments, and large-scale e-commerce analytics.

How is digital transformation modernizing AI operations across emerging sectors?

South America represents around 6% of the global landscape, with Brazil and Argentina accounting for more than 70% of regional demand. Adoption is driven by financial services digitization and energy sector analytics, where predictive models improve operational efficiency. Government-led digital transformation incentives are supporting AI infrastructure modernization. Cloud adoption in enterprise ML workflows exceeds 58%. A regional fintech firm automated fraud detection pipelines in 2025, improving transaction anomaly detection speed by 24%. Consumer demand aligns with localized media analytics and multilingual AI services.

How are industrial modernization and smart infrastructure boosting AI operations?

This region contributes nearly 5% of global adoption, led by the UAE, Saudi Arabia, and South Africa. Oil & gas analytics, smart city initiatives, and telecom network optimization are primary drivers. Over 45% of enterprises in advanced Gulf economies have deployed AI governance frameworks. Investments in digital infrastructure modernization programs exceed 20 national initiatives. A regional telecom operator implemented automated ML performance monitoring in 2025, reducing service disruption incidents by 26%. Consumer behavior shows rising reliance on AI-powered digital government and urban mobility services.

United States MLOps Market – 32% share: High enterprise AI production capacity and advanced cloud infrastructure adoption.

China MLOps Market – 18% share: Strong industrial AI scaling and rapid digital commerce ecosystem expansion.

The MLOps market demonstrates a moderately fragmented competitive structure with over 120 active global vendors offering platforms, orchestration tools, monitoring systems, and managed lifecycle services. The top five companies collectively account for approximately 48% of total market activity, reflecting a mix of hyperscale cloud providers and specialized AI platform firms. Competition is shaped by platform consolidation, with nearly 60% of enterprises preferring integrated toolchains over single-function tools. Strategic partnerships between cloud providers and AI software firms increased by 35% between 2024 and 2025, focusing on governance automation and model observability integration.

Product innovation cycles have accelerated, with more than 50 new MLOps feature releases recorded industry-wide in the past year, primarily in automated retraining, explainable AI modules, and pipeline security. Around 42% of vendors now offer low-code or no-code orchestration layers to address the 48% industry-reported AI talent shortage. Mergers and acquisitions activity remains steady, with over 15 notable transactions focused on expanding monitoring, feature store, and compliance capabilities. Open-source ecosystem influence is strong, as nearly 55% of enterprises deploy hybrid stacks combining proprietary and community tools. Competitive differentiation increasingly centers on governance depth, scalability across multi-cloud environments (adopted by 46% of enterprises), and energy-efficient AI workload optimization.

Microsoft

IBM

Amazon Web Services

Databricks

DataRobot

H2O.ai

Cloudera

Domino Data Lab

SAS Institute

DataRobot

Databricks

TIBCO Software

Hewlett Packard Enterprise

Oracle

The MLOps market is being shaped by rapid advances in automation, cloud-native engineering, and AI governance technologies that enhance the scalability and reliability of machine learning systems. Over 70% of enterprise ML workloads now run in containerized environments, enabling consistent deployment across hybrid and multi-cloud infrastructures. Kubernetes-based orchestration frameworks support more than 65% of automated ML pipelines, reducing environment inconsistencies and improving deployment repeatability by nearly 30%. Feature store technologies are also expanding, with adoption exceeding 50% among advanced AI teams, improving data reuse efficiency and reducing model training preparation time by 35%.

Model observability platforms represent a major technological shift, as approximately 60% of organizations implement real-time monitoring tools that detect data drift, concept drift, and bias anomalies. Automated alerting mechanisms reduce model failure response times by up to 40%. Explainable AI modules are now embedded into over 45% of production ML systems, supporting transparency mandates and risk management. In parallel, serverless ML execution environments have grown by 38% in enterprise adoption, optimizing compute utilization and reducing idle resource overhead.

Emerging technologies include federated learning frameworks, which enable distributed model training across decentralized data sources while maintaining privacy compliance; pilot implementations have demonstrated up to 25% improvement in model generalization without centralizing sensitive data. Edge MLOps is gaining momentum as well, with more than 30% of industrial AI deployments requiring localized model management. Automated retraining systems using event-driven triggers now operate in nearly 55% of large-scale AI environments, improving prediction stability by 28%. Together, these technologies are enabling resilient, compliant, and continuously optimized AI operations across enterprise ecosystems.

• In March 2024, Microsoft and Databricks deepened their strategic partnership to accelerate AI lifecycle management on Azure by integrating MLflow-based workflows with Azure analytics and governance tooling, creating enhanced end-to-end MLOps capabilities for joint enterprise customers.

• In June 2025, Databricks and Microsoft announced a multi-year early extension of their strategic partnership focused on advancing unified data and AI innovation with tighter integrations between Azure Databricks, Azure AI Foundry, and Microsoft Power Platform to streamline machine learning operations. (

• In Q1 2025, IBM launched Watsonx.governance, a specialized MLOps offering aimed at helping enterprises manage machine learning risk, compliance, and transparency across operational model fleets, strengthening governance controls in production environments.

• In 2024, Arize AI raised $43 million in Series B funding to expand its machine learning observability platform, accelerating capabilities for real-time performance diagnostics and error analysis in MLOps pipelines used by enterprise clients worldwide.

The MLOps Market Report encompasses comprehensive analysis across technology components, deployment models, application areas, and industry verticals critical to enterprise machine learning operations. It examines platforms, services, and hybrid architectures that support experiment tracking, model deployment, automated monitoring, and governance frameworks. The report also delineates cloud-native versus on-premise MLOps ecosystems and identifies patterns in adoption of CI/CD pipelines, feature stores, retraining systems, and observability tools. Geographic scope includes detailed regional insights into North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting variation in digital infrastructure maturity, regulatory environments, and industry specialization.

Application analysis covers functions such as deployment automation, continuous monitoring, data management, model lifecycle governance, and risk controls in sectors such as banking, healthcare, retail, telecom, and manufacturing. Technology assessment addresses both established and emerging MLOps trends, including federated learning operations, serverless execution, hybrid multi-cloud orchestration, edge MLOps, and explainable AI integration. The report also provides end-user segmentation, exploring how enterprise size and industry use cases influence tooling preferences and procedural maturity in operationalizing machine learning. Finally, the report includes competitive landscape mapping, innovation trend tracking, and strategic benchmarking to support decision makers in evaluating vendor positioning, partnership activity, and technology roadmaps within the evolving MLOps ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

41.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Microsoft, IBM, Amazon Web Services, Google, Databricks, DataRobot, H2O.ai, Cloudera, Domino Data Lab, SAS Institute, DataRobot, Databricks, TIBCO Software, Hewlett Packard Enterprise, Oracle |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |