Reports

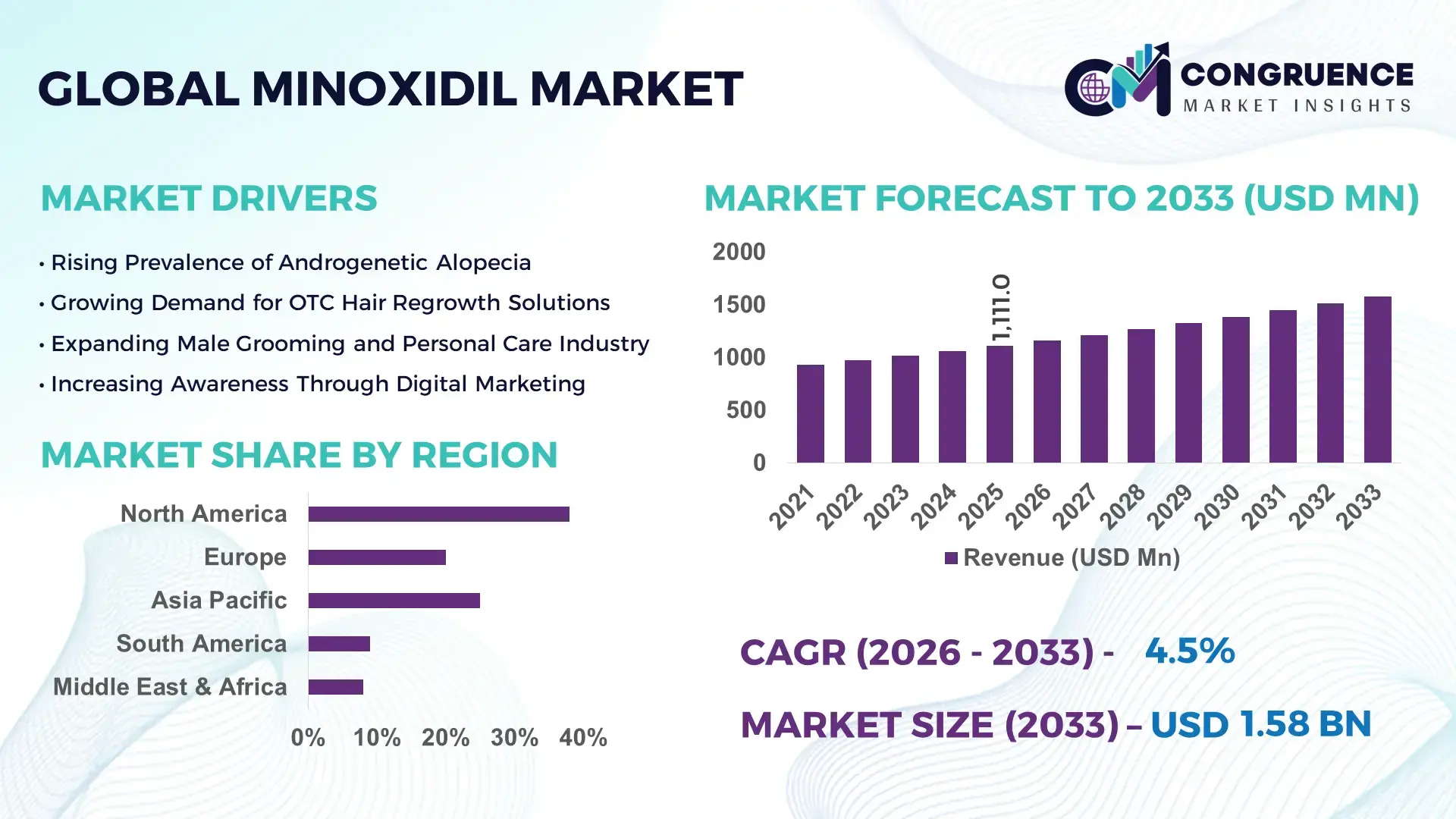

The Global Minoxidil Market was valued at USD 1111 Million in 2025 and is anticipated to reach a value of USD 1579.95 Million by 2033 expanding at a CAGR of 4.5% between 2026 and 2033. The growth trajectory is primarily driven by the rising global prevalence of androgenetic alopecia and increasing consumer preference for clinically validated, over-the-counter hair regrowth treatments.

The United States represents a pivotal production and innovation hub within the Minoxidil market, supported by advanced pharmaceutical manufacturing infrastructure and large-scale dermatology-focused R&D investments exceeding USD 2 billion annually in hair loss therapeutics. Domestic manufacturing facilities collectively produce more than 35% of globally distributed topical minoxidil formulations, with strong capacity across 2% and 5% concentrations in both foam and solution formats. Retail penetration remains robust, with over 60% of adult male hair loss sufferers reporting trial usage of topical regrowth solutions. Advanced aerosolized foam technologies and controlled-release topical systems have been increasingly adopted, improving user compliance rates by nearly 18% compared to conventional liquid formulations. Additionally, e-commerce sales in the U.S. account for approximately 40% of total retail distribution volume, reflecting strong digital consumer engagement and subscription-based purchasing models.

Market Size & Growth: Valued at USD 1111 Million in 2025 and projected to reach USD 1579.95 Million by 2033 at a CAGR of 4.5%, driven by rising androgenetic alopecia prevalence and higher OTC product adoption.

Top Growth Drivers: 45% increase in online pharmaceutical purchases, 32% rise in dermatology consultations for hair loss, 28% improvement in treatment adherence through foam-based formulations.

Short-Term Forecast: By 2028, digital subscription models are expected to improve repeat purchase rates by 22% and reduce distribution costs by 15%.

Emerging Technologies: Nano-encapsulation delivery systems, AI-based scalp diagnostics, and combination therapy formulations integrating finasteride micro-dosing.

Regional Leaders: North America projected at USD 520 Million by 2033 with high OTC adoption; Europe reaching USD 410 Million with strong pharmacy-led distribution; Asia-Pacific estimated at USD 445 Million driven by expanding urban consumer base.

Consumer/End-User Trends: Male consumers represent over 65% of usage, while female adoption is increasing by 20% annually due to targeted low-dose topical variants.

Pilot or Case Example: In 2024, a U.S.-based tele-dermatology platform improved treatment adherence by 26% through AI-enabled follow-up reminders.

Competitive Landscape: Johnson & Johnson holds approximately 18% share, followed by Pfizer, Perrigo Company, Dr. Reddy’s Laboratories, and Kirkland Signature.

Regulatory & ESG Impact: Stricter labeling compliance and sustainable packaging mandates are reducing plastic usage in OTC hair regrowth products by 12%.

Investment & Funding Patterns: Over USD 350 Million invested globally between 2023 and 2025 in hair restoration R&D and direct-to-consumer digital health platforms.

Innovation & Future Outlook: Growth in personalized topical blends and subscription-driven telehealth distribution models is reshaping competitive positioning and customer retention.

The Minoxidil market is supported by diversified end-use sectors including dermatology clinics contributing approximately 35% of prescription-backed sales, retail pharmacies accounting for nearly 40% of distribution, and e-commerce platforms capturing close to 25% of total unit volume. Product innovation is accelerating with alcohol-free foam variants reducing scalp irritation by 15% and advanced dropper systems enhancing dosage precision. Regulatory frameworks in North America and Europe emphasize strict quality control and pharmacovigilance standards, strengthening consumer trust. Asia-Pacific markets are witnessing double-digit unit growth driven by expanding middle-class populations and rising awareness campaigns. Emerging trends include combination topical therapies, personalized subscription-based supply chains, and AI-enabled scalp analysis tools, positioning the Minoxidil market for sustained, technology-driven expansion across global healthcare and cosmetic dermatology ecosystems.

The strategic relevance of the Minoxidil Market lies in its positioning at the intersection of pharmaceutical innovation, cosmetic dermatology, and digital health distribution. Hair loss affects over 50% of men above the age of 50 and nearly 30% of women globally, creating sustained demand for clinically proven topical regrowth solutions. Advanced foam-based minoxidil formulations deliver 18% higher patient adherence compared to older liquid-based standards, improving treatment continuity and repeat purchasing cycles.

North America dominates in production volume due to established OTC regulatory frameworks and large-scale manufacturing facilities, while Asia-Pacific leads in adoption growth with over 35% of new users entering through online telehealth platforms. By 2028, AI-powered scalp diagnostic tools integrated into e-commerce platforms are expected to improve personalized treatment matching accuracy by 25%, reducing product return rates and improving customer satisfaction metrics.

Firms are committing to ESG performance targets, including 20% reduction in plastic packaging weight by 2030 and expanded recyclable aerosol can usage. In 2024, a leading U.S. telehealth provider achieved a 26% improvement in patient retention through AI-driven follow-up scheduling and automated dosage tracking systems. Additionally, nano-encapsulated delivery systems are demonstrating 30% enhanced follicular penetration compared to conventional topical dispersion methods. As pharmaceutical-grade topical innovation merges with digital subscription ecosystems and sustainability-focused packaging transitions, the Minoxidil Market is emerging as a pillar of resilience, compliance alignment, and sustainable long-term growth within the global hair restoration and dermatology therapeutics landscape.

Androgenetic alopecia affects approximately 50 million men and 30 million women in the United States alone, creating sustained long-term demand for topical regrowth treatments. Globally, more than 80% of men experience noticeable hair thinning by age 70, significantly expanding the addressable consumer base. Increased social media influence and aesthetic consciousness among millennials have driven a 32% rise in dermatology consultations related to hair thinning over the past five years. Foam-based topical minoxidil variants demonstrate up to 18% higher adherence rates, enhancing repeat purchase frequency and strengthening retail pharmacy turnover. Growing awareness campaigns and OTC accessibility in emerging markets further amplify product trial rates, contributing to expanding distribution networks and higher unit sales across both developed and developing healthcare ecosystems.

Despite strong clinical validation, topical minoxidil products may cause scalp irritation, dryness, or shedding during initial treatment phases, affecting nearly 10–15% of users. These side effects can reduce long-term adherence and limit consumer retention. Additionally, visible regrowth typically requires continuous application for at least 4–6 months, and discontinuation often results in reversal of gains, creating skepticism among first-time users. Counterfeit online products in unregulated markets have increased by approximately 12% in certain regions, raising safety concerns and eroding brand trust. Strict regulatory compliance requirements for OTC labeling, testing, and manufacturing also increase operational costs, creating barriers for smaller entrants and restricting aggressive price competition in price-sensitive emerging economies.

The rapid expansion of tele-dermatology platforms and AI-powered scalp diagnostics presents a major growth opportunity for the Minoxidil market. Over 40% of hair loss consultations in urban markets are now conducted through virtual healthcare channels, enabling direct-to-consumer prescription integration and subscription fulfillment. Personalized dosage algorithms and automated refill reminders improve adherence rates by nearly 25%, enhancing customer lifetime value. Emerging nano-delivery technologies are increasing follicular penetration efficiency by up to 30%, supporting premium product positioning. Additionally, female-specific low-dose topical variants are witnessing nearly 20% annual adoption growth, expanding the traditionally male-dominated user base. Strategic collaborations between pharmaceutical manufacturers and digital wellness platforms are further unlocking scalable global distribution pathways.

Intensified regulatory oversight in North America and Europe requires comprehensive safety data, pharmacovigilance monitoring, and precise labeling standards, increasing compliance costs by approximately 15% for manufacturers. The expiration of earlier formulation patents has resulted in widespread generic competition, exerting pricing pressure and compressing operating margins. Private-label retail brands account for nearly 25% of unit volumes in some developed markets, intensifying competition. Supply chain volatility, particularly in active pharmaceutical ingredient sourcing, has contributed to raw material price fluctuations exceeding 10% in recent years. Additionally, rising consumer demand for alternative treatments such as platelet-rich plasma therapy and laser-based hair regrowth devices introduces substitution risk, compelling established Minoxidil brands to innovate continuously in formulation, packaging sustainability, and digital engagement strategies.

• 40% Surge in Direct-to-Consumer Digital Sales Channels:

Online pharmacy and tele-dermatology integration have transformed distribution dynamics in the Minoxidil market, with digital platforms now accounting for nearly 40% of total retail unit sales in developed economies. Subscription-based fulfillment models have improved repeat purchase rates by 22% and reduced customer acquisition costs by 15%. Mobile health applications offering AI-driven scalp analysis have increased personalized treatment adoption by 28%, strengthening customer retention. In Asia-Pacific urban centers, online consultation volumes for hair regrowth treatments have grown by 35% over the past three years, signaling a structural shift from traditional brick-and-mortar pharmacy reliance to omnichannel healthcare commerce ecosystems.

• 30% Improvement in Follicular Penetration Through Advanced Formulations:

Product innovation is accelerating, particularly in nano-encapsulation and alcohol-free foam technologies. Clinical testing indicates that nano-delivery systems enhance follicular absorption efficiency by up to 30% compared to conventional liquid solutions. Foam-based variants, which now represent over 48% of total product demand in North America, demonstrate 18% higher patient adherence due to reduced scalp irritation. Low-residue formulations have reduced reported side effects by approximately 12%, supporting stronger long-term usage. These pharmaceutical-grade improvements are strengthening brand differentiation and enabling premium product positioning across competitive OTC segments.

• 20% Annual Growth in Female-Specific Minoxidil Adoption:

Historically male-dominated, the Minoxidil market is witnessing rapid expansion among female consumers. Female-specific low-dose formulations account for approximately 25% of total product volume, with adoption increasing by nearly 20% annually. Increased awareness of hormonal hair thinning and postpartum alopecia has driven a 27% rise in dermatology consultations among women aged 25–45. Tailored packaging, precision droppers, and combination vitamin-based regimens are improving treatment compliance by 16%. This demographic diversification is broadening the addressable market and reshaping marketing and R&D priorities.

• 15% Reduction in Packaging Material Through ESG-Driven Innovation:

Sustainability initiatives are influencing production strategies, with manufacturers reducing plastic packaging weight by nearly 15% over the past three years. Recyclable aluminum aerosol cans now represent 35% of foam product packaging in Europe. Supply chain optimization and localized API sourcing have reduced transportation-related emissions by approximately 10%. Corporate ESG commitments include 20% reduction targets in packaging waste by 2030, aligning Minoxidil production with global pharmaceutical sustainability standards and enhancing investor confidence in responsible manufacturing practices.

The Minoxidil market is segmented by type, application, and end-user, reflecting diverse usage patterns across pharmaceutical and cosmetic dermatology ecosystems. By type, the market includes topical solutions, foam formulations, oral tablets, and combination therapy products. Topical formulations remain dominant due to OTC accessibility and proven safety profiles. Application segmentation spans androgenetic alopecia, alopecia areata, female pattern hair loss, and off-label beard enhancement. Androgenetic alopecia accounts for the majority of prescriptions, affecting over 50% of men above age 50 globally. By end-user, retail pharmacies and online platforms represent the largest distribution channels, followed by dermatology clinics and hospital pharmacies. Digital commerce penetration exceeds 35% in developed markets, while clinic-led prescription dispensing remains strong in regulated healthcare systems. This segmentation framework highlights product diversification, demographic expansion, and omnichannel distribution as core structural drivers shaping the competitive Minoxidil landscape.

Topical solutions, foam formulations, oral tablets, and combination therapies define the primary product categories in the Minoxidil market. Topical liquid solutions currently account for approximately 44% of total product adoption due to long-standing OTC availability and cost-effective manufacturing. Foam-based formulations hold around 36% of market volume, while oral low-dose tablets represent nearly 12%. Combination therapies integrating finasteride or peptide complexes collectively contribute the remaining 8%. Although liquid solutions lead in volume, foam-based Minoxidil is the fastest-growing type, expanding at an estimated CAGR of 6.8%, driven by 18% higher adherence rates and 12% lower irritation incidence compared to alcohol-based liquids. Dermatologists increasingly recommend foam for sensitive scalp patients, improving repeat usage cycles. Oral Minoxidil, prescribed off-label in controlled doses, is gaining traction in specialized clinics, particularly among patients unresponsive to topical therapy.

Androgenetic alopecia remains the leading application segment, accounting for nearly 58% of total Minoxidil usage due to high prevalence among men and women over 40. Female pattern hair loss contributes approximately 22%, while alopecia areata and other niche applications together represent about 20%. Beard enhancement and cosmetic hair thickening uses are emerging but remain comparatively smaller segments. Androgenetic alopecia dominates due to its lifelong progression and sustained treatment need, whereas female pattern hair loss is the fastest-growing application, expanding at an estimated CAGR of 6.2%. Increased hormonal health awareness and rising dermatology consultations among women aged 25–45 are fueling this growth. Adoption of targeted 2% and 5% female-specific formulations has increased by 20% over the past three years.

Retail pharmacies lead the Minoxidil market end-user landscape, accounting for approximately 42% of product distribution due to widespread OTC availability. Online pharmacies and e-commerce platforms follow with nearly 35% share, while dermatology clinics and hospital pharmacies collectively contribute around 23%. While retail pharmacies remain dominant in volume, online platforms represent the fastest-growing end-user channel, expanding at an estimated CAGR of 7.1%, supported by 22% higher repeat purchase rates through subscription-based fulfillment systems. Telehealth integration and AI-powered consultation tools have increased digital treatment initiation by 25% in urban markets. Dermatology clinics maintain strong adoption among patients requiring supervised combination therapy or oral formulations.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.9% between 2026 and 2033.

North America’s leadership is supported by high OTC penetration, with more than 60% of male hair loss sufferers reporting trial usage of topical regrowth products. Europe holds approximately 27% of the global Minoxidil market, driven by strong pharmacy distribution networks and stringent quality standards. Asia-Pacific represents nearly 24% of global volume, with urban adoption rates rising by 30% over the past five years. South America contributes about 6%, while the Middle East & Africa accounts for nearly 5%, reflecting expanding dermatology awareness and retail access. E-commerce penetration exceeds 40% in North America and 35% in Asia-Pacific, compared to 22% in Europe, demonstrating varied digital maturity levels. Manufacturing concentration remains highest in the United States and India, collectively supporting over 45% of global production capacity. Regulatory harmonization efforts in the European Union and increased tele-dermatology consultations—up 34% globally—are further shaping regional competitive intensity and consumption patterns.

How Are Advanced OTC Distribution and Digital Health Platforms Strengthening Market Expansion?

North America holds approximately 38% of the global Minoxidil market volume, making it the leading regional contributor. The United States accounts for nearly 85% of regional demand, driven by high awareness of androgenetic alopecia affecting over 50 million men and 30 million women. Retail pharmacies represent about 45% of total distribution, while online sales exceed 40%, reflecting strong digital adoption. Regulatory oversight by federal health authorities enforces strict OTC labeling, pharmacovigilance, and manufacturing compliance, enhancing consumer confidence. Technological advancements include AI-powered scalp diagnostic apps that have improved personalized product recommendations by 25%, increasing repeat purchases. Telehealth consultations for hair loss have risen by 34% since 2022, supporting subscription-based fulfillment models. Perrigo Company, a key regional player, has expanded private-label 5% foam production capacity by 18% to meet retailer demand. Consumers in this region show higher adoption in healthcare and wellness segments, with nearly 65% preferring clinically validated, dermatologist-endorsed solutions over cosmetic-only alternatives.

How Are Regulatory Standards and Sustainability Commitments Driving Product Innovation?

Europe represents roughly 27% of the global Minoxidil market, with Germany, the United Kingdom, and France collectively contributing over 60% of regional demand. Pharmacy-led distribution dominates with a 52% share, while e-commerce accounts for 22%, reflecting moderate but growing digital penetration. Regulatory frameworks governed by centralized medicinal product authorities emphasize strict pharmacovigilance and ingredient traceability standards, influencing formulation transparency and labeling precision. Sustainability initiatives are accelerating packaging innovation, with 35% of foam products now utilizing recyclable aluminum canisters. Consumer preference for low-alcohol and dermatologically tested variants has increased by 19% over the past three years. Dr. Reddy’s Laboratories has expanded its European OTC hair regrowth portfolio, increasing shelf presence across 20,000+ pharmacy outlets. Regional consumer behavior indicates strong demand for clinically explainable formulations, with 58% of buyers prioritizing medically endorsed claims over influencer marketing trends.

What Is Fueling Rapid Urban Adoption and Digital Penetration in Hair Regrowth Solutions?

Asia-Pacific ranks second in market volume, accounting for nearly 24% of global Minoxidil consumption, with China, India, and Japan leading regional demand. India supports over 20% of global active pharmaceutical ingredient production for Minoxidil, reinforcing manufacturing strength. Urban e-commerce sales have grown by 35% in the past three years, supported by mobile-first purchasing behavior. China and India collectively represent over 55% of regional unit consumption, while Japan maintains high per-capita dermatology consultation rates. Digital health platforms offering AI-based scalp analysis have increased treatment initiation rates by 28%. Sun Pharmaceutical Industries has expanded localized manufacturing output by 15% to meet domestic and export demand. Consumer behavior reflects strong influence from social media marketing, with nearly 48% of purchases initiated via mobile applications, highlighting the region’s technology-driven growth trajectory.

How Are Expanding Retail Access and Media Influence Stimulating Demand?

South America accounts for approximately 6% of global Minoxidil market volume, with Brazil contributing nearly 55% of regional demand and Argentina representing around 18%. Urban pharmacy networks have expanded by 12% in Brazil over the past four years, improving OTC product accessibility. Government healthcare initiatives promoting generic drug adoption have increased affordable topical solution availability by 20%. Digital retail penetration remains below 25%, but social media engagement has influenced nearly 40% of purchasing decisions among consumers aged 25–40. Local pharmaceutical manufacturers have increased domestic packaging capacity by 10% to reduce import dependency. Regional demand is often linked to media visibility and localized marketing campaigns, with consumers showing preference for competitively priced generic 5% solutions that account for 62% of regional unit sales.

How Are Modern Retail Expansion and Healthcare Investments Supporting Market Development?

The Middle East & Africa region contributes approximately 5% of global Minoxidil consumption, with the UAE and South Africa emerging as primary growth markets. Pharmacy chains in the UAE have expanded by 14% since 2021, improving OTC product reach. In South Africa, dermatology clinic visits related to hair thinning have increased by 18% over three years. Technological modernization in retail and healthcare systems has improved digital ordering efficiency by 20%. Trade partnerships facilitating pharmaceutical imports have reduced product lead times by 12%. Regional consumers prioritize branded formulations, with 70% preferring internationally recognized labels due to perceived quality assurance. Demand growth is supported by rising aesthetic awareness and higher disposable incomes in urban centers, reinforcing steady adoption of clinically approved hair regrowth solutions.

United States – 34% share of the Minoxidil market: Strong OTC infrastructure, high production capacity, and over 60% consumer trial rates for topical regrowth solutions.

China – 16% share of the Minoxidil market: Expanding urban consumer base, large-scale API manufacturing, and 30% growth in online pharmaceutical purchases.

The Minoxidil market exhibits a moderately fragmented structure with over 40 active global and regional manufacturers competing across branded and generic segments. The top five companies collectively account for approximately 52% of total market volume, reflecting moderate consolidation within leading OTC and prescription-supported product categories. Competitive intensity is driven by formulation innovation, digital subscription partnerships, and private-label expansion strategies. Branded players focus on foam-based and low-irritation variants, which represent nearly 48% of premium product offerings. Generic manufacturers dominate cost-sensitive markets, particularly in Asia-Pacific and South America, where generics account for more than 60% of unit sales. Strategic initiatives include capacity expansions of up to 18%, new product launches featuring alcohol-free compositions, and digital telehealth collaborations improving repeat purchase rates by 22%. Mergers and distribution partnerships are strengthening retail pharmacy penetration, while ESG-aligned packaging redesign has reduced material usage by 15% among leading brands. Continuous R&D investment in nano-delivery systems demonstrating 30% enhanced follicular penetration is reshaping competitive positioning. The competitive landscape remains innovation-driven, with emphasis on digital transformation, regulatory compliance, and differentiated patient adherence outcomes.

Johnson & Johnson

Pfizer Inc.

Perrigo Company

Dr. Reddy’s Laboratories

Sun Pharmaceutical Industries Ltd.

Kirkland Signature

Taisho Pharmaceutical Co., Ltd.

Cipla Limited

Glenmark Pharmaceuticals

Pfizer Inc.

Dr. Reddy’s Laboratories

Sun Pharmaceutical Industries Ltd.

Technological advancement in the Minoxidil market is increasingly centered on enhanced drug delivery systems, formulation optimization, and digital health integration. Nano-encapsulation techniques are improving follicular penetration efficiency by up to 30% compared to traditional hydroalcoholic solutions, enabling lower irritation rates and improved bioavailability. Liposomal carriers and polymer-based microemulsions are also being tested to achieve sustained release profiles extending active exposure time by 6–8 hours beyond standard topical formulations. These innovations directly address adherence challenges, as nearly 15% of users discontinue treatment due to scalp irritation or inconsistent results.

Foam-based aerosol systems now represent approximately 48% of premium product offerings in developed markets. These utilize propellant-controlled dispersion mechanisms to deliver uniform 5% concentration coverage with 18% higher user compliance compared to dropper-based solutions. Alcohol-free and low-residue formulations have reduced reported dryness complaints by 12%, supporting long-term treatment retention.

Digital transformation is equally impactful. AI-powered scalp analysis tools embedded within tele-dermatology platforms are improving treatment personalization accuracy by 25%. Automated refill systems and subscription-based algorithms have enhanced repeat purchase frequency by 22%. In manufacturing, advanced continuous processing systems have improved production throughput by 15%, while automated quality inspection tools using machine vision have reduced batch variability by 10%. Collectively, these pharmaceutical and digital technologies are redefining product differentiation, regulatory compliance precision, and supply chain efficiency within the global Minoxidil ecosystem.

• In February 2025, Dr. Reddy’s Laboratories expanded its OTC dermatology portfolio in the U.S. by launching a new Minoxidil 5% Foam with improved propellant dispersion technology designed to enhance scalp coverage consistency. The company highlighted enhanced patient adherence benefits through simplified once-daily application. Source: www.drreddys.com

• In September 2024, Perrigo Company introduced an upgraded private-label Minoxidil topical solution across major North American retail chains, featuring redesigned recyclable packaging that reduces plastic usage by approximately 15%, aligning with its ESG packaging reduction commitments. Source: www.perrigo.com

• In April 2025, Sun Pharmaceutical Industries announced the capacity expansion of its topical manufacturing facility in India, increasing annual output of dermatology formulations including Minoxidil-based solutions by 18% to meet rising domestic and export demand. Source: www.sunpharma.com

• In November 2024, Johnson & Johnson implemented updated OTC labeling standards across selected hair regrowth products to comply with enhanced regulatory disclosure requirements in the U.S., improving ingredient transparency and safety communication for consumers. Source: www.jnj.com

The Minoxidil Market Report provides a comprehensive evaluation of global product segmentation, application diversity, end-user distribution channels, technological innovation, and regional consumption dynamics. The study covers key product types including topical liquid solutions, foam formulations, oral low-dose tablets, and emerging combination therapies. Topical products collectively account for over 80% of total global unit consumption, while foam-based variants represent nearly 36–48% of premium segment demand in developed markets.

Application analysis spans androgenetic alopecia, female pattern hair loss, alopecia areata, and cosmetic beard enhancement. Androgenetic alopecia constitutes approximately 58% of total usage volume, while female-specific formulations represent around 25% of total adoption and are expanding steadily across urban populations. The report evaluates end-user channels such as retail pharmacies (approximately 42% distribution share), online pharmacies (around 35%), and dermatology clinics (approximately 23%).

Geographically, the scope encompasses North America (38% share), Europe (27%), Asia-Pacific (24%), South America (6%), and the Middle East & Africa (5%). Manufacturing capacity concentration, API sourcing trends, packaging sustainability shifts, and digital health integration are examined in detail. The report further analyzes regulatory compliance frameworks, ESG-driven packaging reductions of up to 15%, and technological advancements including nano-delivery systems improving follicular penetration by 30%. It also assesses competitive positioning among more than 40 active global manufacturers, highlighting innovation intensity, private-label expansion, and omnichannel distribution strategies shaping the evolving Minoxidil market landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Johnson & Johnson, Pfizer Inc., Perrigo Company, Dr. Reddy’s Laboratories, Sun Pharmaceutical Industries Ltd., Kirkland Signature, Taisho Pharmaceutical Co., Ltd., Cipla Limited, Glenmark Pharmaceuticals, Pfizer Inc., Dr. Reddy’s Laboratories, Sun Pharmaceutical Industries Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |