Reports

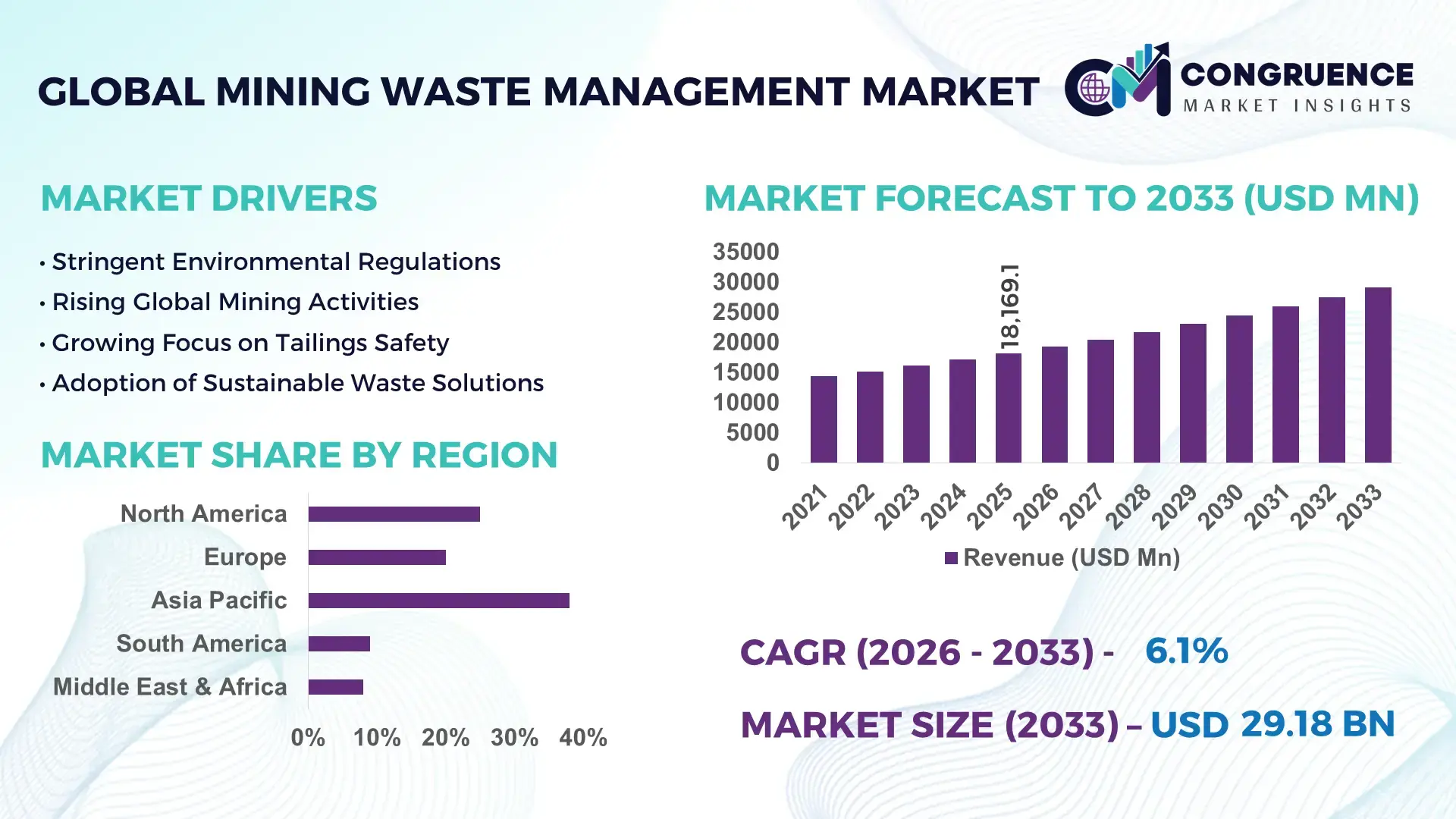

The Global Mining Waste Management Market was valued at USD 18169.13 Million in 2025 and is anticipated to reach a value of USD 29178.12 Million by 2033 expanding at a CAGR of 6.1% between 2026 and 2033. Rising mineral extraction activities and stricter environmental compliance frameworks are accelerating demand for advanced, sustainable mining waste management solutions across major mining economies.

China continues to lead large-scale mining waste management deployment, supported by its extensive coal, iron ore, and rare earth production base exceeding 4.5 billion metric tons of mineral output annually. The country operates over 12,000 active mines, generating significant volumes of tailings and overburden that require engineered containment, dry stacking, and recycling systems. Government-backed investments in green mining initiatives surpassed USD 5 billion in recent years, driving the adoption of intelligent tailings monitoring systems and automated slurry treatment technologies. Additionally, more than 60% of large Chinese mining enterprises have integrated real-time environmental monitoring platforms, enhancing operational safety, improving waste reuse rates by nearly 18%, and strengthening compliance with national ecological restoration mandates.

• Market Size & Growth: Valued at USD 18169.13 Million in 2025, projected to reach USD 29178.12 Million by 2033, growing at a CAGR of 6.1%, driven by stricter environmental regulations and increased mineral production.

• Top Growth Drivers: Regulatory compliance adoption (42%), tailings recycling efficiency improvements (35%), and digital monitoring system integration (28%).

• Short-Term Forecast: By 2028, advanced tailings management systems are expected to reduce operational waste handling costs by 15% and improve processing efficiency by 12%.

• Emerging Technologies: AI-powered tailings monitoring, dry stack tailings technology, and IoT-enabled water recovery systems enhancing sustainable mining waste operations.

• Regional Leaders: Asia-Pacific projected to exceed USD 11,200 Million by 2033 with rapid mine expansion; North America to surpass USD 7,800 Million driven by ESG compliance upgrades; Europe to reach USD 5,900 Million supported by circular mining policies.

• Consumer/End-User Trends: Large-scale metal and coal mining operators account for over 65% of advanced waste treatment adoption, with growing preference for environmentally responsible and cost-optimized solutions.

• Pilot or Case Example: In 2024, a large copper mining operation implemented dry stack tailings technology, achieving 20% water recovery improvement and reducing tailings dam footprint by 25%.

• Competitive Landscape: The market leader holds approximately 18% share, followed by major participants such as Veolia, Hatch Ltd., Tetra Tech, Metso, and Golder Associates.

• Regulatory & ESG Impact: Stricter tailings dam safety standards, carbon neutrality targets, and mandatory environmental impact reporting are accelerating sustainable mining waste management adoption.

• Investment & Funding Patterns: Recent global investments exceeded USD 3.2 Billion in mine rehabilitation projects, digital waste monitoring systems, and water recycling infrastructure upgrades.

• Innovation & Future Outlook: Integration of predictive analytics, automated sludge dewatering, and circular economy models is reshaping long-term mining waste management strategies.

Mining waste management demand is largely driven by the coal, iron ore, copper, gold, and rare earth mining sectors, which collectively contribute more than 70% of total waste generation volumes globally. Tailings management and water treatment services account for nearly half of industry spending, while waste recycling and mine site rehabilitation services are expanding at faster rates. Recent technological advancements, including geosynthetic liners, advanced thickening systems, and automated environmental risk monitoring platforms, are transforming operational efficiency. Regulatory pressures related to tailings dam safety, carbon emissions reduction, and land restoration mandates continue to influence procurement strategies. Asia-Pacific leads consumption due to expanding mineral extraction activities, while North America and Europe focus on modernization and ESG-driven upgrades. The future outlook emphasizes circular mining practices, increased waste reuse ratios, and climate-resilient infrastructure investments.

The Mining Waste Management Market holds strategic relevance as global mining output exceeds 18 billion metric tons annually, generating substantial volumes of tailings, overburden, and process water requiring engineered containment and sustainable treatment systems. For mining operators, effective waste management is no longer a compliance formality but a risk mitigation and value-optimization strategy directly linked to operational continuity, ESG credibility, and capital access. Advanced dry stack tailings technology delivers up to 30% improvement in water recovery compared to conventional slurry-based tailings dams, while AI-enabled predictive monitoring systems reduce tailings dam failure risk indicators by nearly 25% compared to manual inspection standards.

Asia-Pacific dominates in volume due to extensive coal and metal extraction activities, while North America leads in technology adoption with over 55% of large mining enterprises deploying digital tailings monitoring and automated water treatment solutions. By 2028, AI-driven geotechnical risk analytics is expected to cut unplanned environmental compliance incidents by 20% and improve reporting efficiency by 18%. Firms are committing to ESG performance metrics such as 40% water recycling rates and 25% reduction in waste-related emissions by 2030. In 2024, a major Australian mining operator achieved a 22% reduction in freshwater withdrawal through IoT-based water recovery systems integrated with thickened tailings processes.

As regulatory scrutiny intensifies and investors prioritize responsible mining, the Mining Waste Management Market is emerging as a foundational pillar of operational resilience, regulatory compliance, and long-term sustainable growth across global mineral supply chains.

Global mineral demand for electrification, infrastructure, and battery production has increased significantly, with copper demand alone projected to exceed 30 million metric tons annually within the decade. Higher ore processing volumes generate greater quantities of tailings and waste rock, intensifying the need for advanced containment and treatment systems. Over 70% of newly approved large-scale mining projects now incorporate engineered tailings storage and water recycling technologies at the feasibility stage. ESG compliance requirements are also driving investment, as institutional investors representing trillions in assets require transparent environmental risk reporting. More than 60% of multinational mining companies have adopted enhanced tailings management standards aligned with global safety frameworks, accelerating deployment of digital monitoring tools, dry stacking systems, and sustainable mine rehabilitation programs.

Implementing advanced mining waste management infrastructure involves substantial upfront investment, particularly for dry stack tailings facilities, water treatment plants, and geotechnical monitoring systems. Construction of engineered tailings storage facilities can account for up to 20% of total mine development costs. Additionally, environmental permitting processes in several jurisdictions extend beyond 24 months, delaying project timelines. Small and mid-sized mining operators often face financial constraints in adopting state-of-the-art waste treatment technologies. Technical complexity, including site-specific geotechnical assessments and seismic risk evaluations, further increases project planning expenses. Insurance premiums for tailings facilities have also risen in recent years, placing additional financial pressure on operators and slowing widespread technology adoption in cost-sensitive markets.

Digitalization and circular economy initiatives are creating significant growth avenues within the Mining Waste Management Market. IoT-based tailings sensors and AI-driven risk modeling systems can improve early-warning accuracy by over 30%, enhancing operational reliability. Reprocessing legacy tailings for valuable mineral recovery presents additional revenue streams, particularly in gold, copper, and rare earth segments. Studies indicate that secondary recovery from tailings can extract up to 10% additional mineral value from previously discarded material. Water recycling technologies capable of recovering more than 80% of process water are gaining traction in arid mining regions. Moreover, mine site rehabilitation and land reclamation services are expanding as governments enforce post-closure restoration obligations, encouraging long-term environmental stewardship and sustainable project design.

Operational risks associated with tailings dam stability, extreme weather events, and seismic activity remain significant challenges. Climate change has intensified rainfall variability, increasing hydraulic pressure on tailings storage facilities and elevating failure risks. More than 10% of existing global tailings dams are classified as high consequence facilities, requiring continuous monitoring and structural upgrades. Integrating advanced monitoring systems into legacy infrastructure presents technical difficulties and compatibility constraints. Furthermore, public scrutiny and community opposition following past tailings incidents have increased reputational risk for mining operators. Balancing cost efficiency with stringent environmental safeguards while maintaining uninterrupted mineral production creates a complex operational landscape for stakeholders in the Mining Waste Management Market.

• Accelerated Adoption of Dry Stack Tailings Technology Enhancing Water Recovery by Over 30%: Mining operators are rapidly transitioning from conventional slurry-based tailings dams to dry stack systems that improve water recovery rates by 30% to 40% while reducing tailings storage footprints by nearly 50%. More than 35% of newly commissioned large-scale metal mines now integrate filtered tailings solutions at the design stage. This shift significantly lowers long-term dam stability risks and cuts closure liabilities by approximately 20%, making dry stacking a preferred solution in water-stressed mining regions across Australia, Chile, and Canada.

• AI-Enabled Real-Time Monitoring Reducing Safety Incidents by 25%: The integration of IoT sensors, satellite surveillance, and AI-based predictive analytics is transforming tailings facility oversight. Over 60% of Tier-1 mining companies have deployed automated geotechnical monitoring platforms capable of processing thousands of stability data points per hour. These intelligent systems reduce response times to structural anomalies by nearly 40% and have contributed to a 25% decline in reportable tailings-related safety incidents across digitally enabled sites.

• Water Recycling Systems Achieving Recovery Rates Above 80% in Arid Regions: Advanced thickening and filtration technologies are enabling mining sites to recover more than 80% of process water from tailings streams. In regions experiencing chronic water scarcity, such as parts of Latin America, recycled water now accounts for over 50% of total operational water use in several large copper mines. This trend supports regulatory compliance targets and lowers freshwater withdrawal volumes by up to 35%, strengthening long-term operational sustainability.

• Expansion of Tailings Reprocessing Unlocking Up to 10% Additional Mineral Yield: Secondary recovery from legacy tailings deposits is emerging as a strategic value-creation pathway. Modern flotation and bioleaching techniques allow operators to extract up to 8% to 10% additional recoverable metals from previously discarded material. Nearly 20% of active gold and copper producers are evaluating tailings retreatment projects to extend mine life by 5 to 7 years while minimizing new waste generation. This approach enhances resource efficiency and aligns with circular mining objectives.

The Mining Waste Management Market is segmented by type, application, and end-user, each reflecting distinct operational priorities across the global mining value chain. By type, tailings management, waste rock management, water treatment, and mine site rehabilitation form the core service categories, with tailings-related solutions accounting for the largest operational focus due to safety and environmental risk exposure. Application-wise, metal mining represents the dominant segment given higher ore processing intensity and associated waste volumes, followed by coal and industrial minerals. From an end-user perspective, large-scale multinational mining corporations drive the majority of advanced technology adoption, while mid-tier and junior mining firms are increasingly investing in modular, cost-optimized waste management systems. Regulatory enforcement, ESG disclosure requirements, and water scarcity challenges continue to influence segmentation trends, with measurable shifts toward digital monitoring, dry stacking systems, and closed-loop water recycling infrastructure across high-production mining jurisdictions.

Tailings management remains the leading segment, accounting for approximately 48% of total Mining Waste Management Market adoption due to the high-risk profile of tailings storage facilities and strict global safety standards. Conventional slurry-based systems still operate widely; however, filtered dry stack tailings technologies are expanding rapidly. Tailings management currently accounts for nearly half of all infrastructure upgrades, while water treatment systems represent around 27% of installations. However, dry stack and advanced filtration systems are the fastest-growing type, expanding at an estimated CAGR of 8.4%, driven by water recovery rates exceeding 30% compared to traditional impoundments. Waste rock management contributes roughly 15% of the market, focusing on overburden stabilization and acid mine drainage prevention. Mine site rehabilitation and closure services collectively account for the remaining 10%, gaining traction as governments enforce mandatory restoration bonds and post-closure compliance audits.

Metal mining dominates application demand, accounting for nearly 52% of total Mining Waste Management Market deployment due to high ore throughput and complex tailings composition in copper, gold, iron ore, and lithium operations. Coal mining represents approximately 28% of waste management activity, largely concentrated in overburden handling and slurry pond stabilization. However, demand within rare earth and battery mineral extraction is rising fastest, expanding at an estimated CAGR of 7.9%, supported by the energy transition and electric vehicle supply chain growth. Industrial minerals, including phosphate and potash, contribute the remaining 20%, requiring specialized brine and slurry containment systems. Compared to coal mining’s 28% share, metal mining’s 52% dominance reflects higher water treatment intensity and stricter ESG scrutiny.

Large multinational mining corporations represent the leading end-user segment, accounting for approximately 58% of total Mining Waste Management Market technology adoption. These enterprises typically operate multi-site assets and allocate dedicated capital toward digital tailings monitoring, dry stacking, and ESG compliance systems. Mid-tier mining companies hold around 27% of adoption, increasingly investing in modular water treatment units and automated geotechnical monitoring. However, junior mining firms are the fastest-growing end-user segment, expanding at an estimated CAGR of 9.1%, as regulatory obligations require even smaller operators to implement standardized waste containment solutions. Government-owned mining enterprises and state-backed mineral development agencies collectively contribute nearly 15% of overall adoption, particularly in emerging economies. Adoption among top-tier mining firms exceeds 70% for real-time tailings monitoring platforms, compared to less than 40% among smaller operators.

Asia-Pacific accounted for the largest market share at 38% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2026 and 2033.

Asia-Pacific’s dominance is supported by mineral production exceeding 10 billion metric tons annually, with China, India, and Australia operating more than 6,000 active large-scale mines combined. Over 45% of new tailings storage facilities commissioned in 2025 were located in this region, reflecting strong infrastructure expansion. North America holds approximately 26% market share, driven by stringent tailings dam regulations and over 70% adoption of digital monitoring systems among Tier-1 miners. Europe accounts for nearly 18%, emphasizing rehabilitation and circular mining, with more than 60% of mining enterprises integrating advanced water recycling systems. South America represents 12%, largely influenced by copper and lithium extraction, while the Middle East & Africa collectively contribute 6%, supported by gold and phosphate mining developments and modernization initiatives.

How Are Advanced Compliance Mandates and Digital Monitoring Transforming Industrial Waste Strategies?

North America represents approximately 26% of the global Mining Waste Management Market, with the United States and Canada leading deployment across metal and coal mining operations. More than 70% of large mining companies in this region utilize real-time tailings monitoring systems integrated with satellite and IoT sensors. Copper, gold, and iron ore mining are key demand drivers, collectively generating over 2 billion metric tons of waste annually. Regulatory frameworks now require detailed tailings disclosure and emergency preparedness reporting, increasing capital allocation toward engineered dry stack facilities and advanced water treatment units. Technological transformation is evident, with automated geotechnical analytics improving risk detection accuracy by nearly 35%. A leading regional environmental engineering firm has deployed AI-based dam stability platforms across over 50 mine sites, reducing manual inspection time by 30%. Enterprise adoption patterns indicate higher digital integration among large corporations compared to mid-sized operators, reflecting stronger ESG-linked financing requirements and investor scrutiny.

Why Is Sustainability-Led Modernization Driving Demand for Safer Tailings Solutions?

Europe accounts for nearly 18% of the Mining Waste Management Market, with Germany, the United Kingdom, Sweden, and Finland serving as principal mining jurisdictions. More than 65% of European mining operations have implemented advanced water recycling systems achieving reuse rates above 70%. Strict environmental oversight and mandatory land restoration bonds are reshaping procurement strategies across the sector. Regulatory directives emphasize circular economy principles, requiring measurable waste reduction targets and transparent environmental reporting. Emerging technologies such as automated thickening systems and predictive environmental risk modeling are gaining traction, particularly in Nordic mining clusters. A Scandinavian mining operator recently upgraded its tailings facility with filtered stacking technology, reducing water consumption by 28% and lowering long-term closure liabilities. Regional behavior reflects strong preference for compliant, auditable, and environmentally transparent Mining Waste Management solutions, with sustainability certifications influencing supplier selection decisions across over 60% of enterprises.

How Is Large-Scale Mineral Extraction Accelerating Infrastructure Investment in Waste Solutions?

Asia-Pacific holds the largest share at 38%, driven by China, India, and Australia, which collectively produce more than 55% of global coal and significant volumes of iron ore and rare earth minerals. The region operates thousands of active tailings facilities, with over 40% of new mining infrastructure projects incorporating advanced containment systems. Industrial expansion and infrastructure development continue to intensify waste generation volumes across copper, lithium, and bauxite mining. Technological innovation hubs in Australia and China are advancing AI-enabled monitoring and high-efficiency filtration units capable of improving water recovery by over 30%. A major Australian mining company implemented integrated water management systems across multiple sites, achieving freshwater withdrawal reductions of nearly 25%. Adoption behavior indicates strong infrastructure-led investment, with governments mandating environmental monitoring systems for large-scale mines exceeding defined production thresholds.

What Role Do Copper and Lithium Expansions Play in Modern Waste Strategies?

South America contributes approximately 12% to the Mining Waste Management Market, primarily driven by Brazil, Chile, and Argentina. Chile alone accounts for over 25% of global copper output, generating substantial tailings volumes requiring engineered containment and water recycling solutions. Lithium extraction projects in Argentina have increased tailings and brine management investments by more than 20% over recent years. Infrastructure upgrades focus on seismic-resistant tailings storage facilities due to regional geological conditions. Governments have introduced stricter dam safety evaluations and cross-border environmental reporting standards. A Brazilian mining operator recently deployed advanced thickening systems to improve water reuse efficiency by 32%, enhancing operational sustainability. Regional demand patterns are closely tied to commodity export cycles, with heightened attention to environmental transparency and community engagement in mining-intensive provinces.

How Are Resource Diversification and Industrial Modernization Shaping Waste Policies?

The Middle East & Africa region accounts for nearly 6% of the global Mining Waste Management Market, with South Africa, the United Arab Emirates, and Saudi Arabia emerging as key contributors. Gold, phosphate, and industrial mineral extraction drive regional waste generation volumes exceeding hundreds of millions of metric tons annually. Modernization initiatives emphasize digitized environmental monitoring and improved tailings containment infrastructure. South Africa has strengthened mine closure regulations, requiring detailed rehabilitation planning and financial provisioning. In the Gulf region, mining diversification strategies aligned with industrial development plans have increased investment in advanced water treatment facilities capable of recycling more than 75% of process water. A South African mining services provider recently integrated remote sensing systems across multiple gold operations, reducing inspection response times by 20%. Adoption behavior reflects gradual but steady transition toward compliance-driven, technology-enabled waste management practices.

• China – 24% share in the Mining Waste Management Market: High mineral production exceeding 4.5 billion metric tons annually and large-scale government-backed environmental modernization programs drive extensive deployment of advanced tailings and water treatment systems.

• United States – 19% share in the Mining Waste Management Market: Strong regulatory enforcement, over 70% adoption of digital tailings monitoring among major mining firms, and advanced infrastructure investments support its leadership position.

The Mining Waste Management market is moderately fragmented, with more than 150 active global and regional service providers competing across tailings management, water treatment, waste rock stabilization, and mine rehabilitation services. The top 5 companies collectively account for approximately 38% of the global market share, reflecting a competitive yet innovation-driven landscape. Large multinational engineering and environmental service firms maintain strong positioning through integrated project delivery models, digital monitoring platforms, and long-term mine lifecycle service contracts.

Strategic initiatives such as cross-border partnerships, technology licensing agreements, and targeted acquisitions are intensifying competition. Over 25 strategic collaborations were announced globally between 2023 and 2025, primarily focused on AI-enabled tailings monitoring, advanced filtration systems, and ESG compliance analytics. Product innovation is centered on dry stack tailings systems capable of improving water recovery by more than 30% and automated geotechnical surveillance platforms that enhance structural risk detection accuracy by nearly 35%.

Competitive differentiation increasingly depends on digital transformation capabilities, sustainability credentials, and the ability to deliver end-to-end mine waste lifecycle solutions. Companies investing over 5% of annual operational budgets into R&D for environmental technologies are gaining preference in high-regulation markets. Additionally, integrated engineering-procurement-construction (EPC) contracts exceeding 3 to 5 years are becoming common, strengthening client retention and recurring service revenues.

Veolia

Hatch Ltd.

Tetra Tech, Inc.

Metso Corporation

WSP Global Inc.

GHD Group

SRK Consulting

Knight Piésold

FLSmidth

Ausenco

SNC-Lavalin Group Inc.

Klohn Crippen Berger

Worley Limited

DRA Global

Stantec Inc.

Technological innovation is fundamentally transforming the Mining Waste Management Market, with operators prioritizing risk reduction, water efficiency, and regulatory compliance. One of the most significant advancements is filtered dry stack tailings technology, which reduces tailings storage volume by up to 50% and improves water recovery rates by 30% to 40% compared to conventional slurry impoundments. More than 35% of newly approved large-scale metal mining projects now integrate filtered tailings systems at the design stage, particularly in water-scarce regions.

Digital transformation is accelerating through IoT-enabled geotechnical sensors and satellite-based deformation monitoring systems. Modern tailings facilities can deploy over 1,000 real-time sensors measuring pore pressure, slope stability, and seismic activity, transmitting data continuously to centralized control rooms. AI-powered predictive analytics platforms are capable of analyzing millions of data points daily, reducing anomaly detection time by nearly 40% and lowering incident response delays by approximately 25%.

Advanced water treatment and recycling technologies are also gaining strategic importance. High-density thickeners and membrane filtration systems enable mining operations to recover more than 80% of process water, reducing freshwater withdrawal by up to 35%. Automated sludge dewatering systems further decrease residual moisture content by 15% to 20%, improving transportation efficiency and reducing environmental risk.

Emerging technologies include autonomous drones for aerial tailings inspections, reducing manual inspection time by nearly 30%, and blockchain-enabled environmental reporting platforms that enhance transparency and traceability of compliance documentation. Together, these technologies are reshaping operational resilience, ESG performance measurement, and lifecycle cost optimization across the Mining Waste Management Market.

• In March 2024, Metso expanded its tailings filtration portfolio by launching a high-capacity Larox® FFP filter unit designed for large-scale mining operations, enabling up to 10% higher throughput and improved water recovery efficiency in filtered tailings applications. Source: www.metso.com

• In September 2024, Veolia Water Technologies secured a multi-year contract to deliver advanced mine water treatment solutions for a major copper mining project in South America, incorporating high-density sludge processes capable of treating over 2,500 m³/hour of mine-affected water. Source: www.veoliawatertechnologies.com

• In February 2025, FLSmidth announced the deployment of its next-generation EIMCO® deep cone thickener technology at a large gold mining operation, increasing underflow density by up to 20% and significantly reducing water losses from tailings storage facilities. Source: www.flsmidth.com

• In April 2025, Tetra Tech was awarded a tailings dam safety and environmental monitoring contract supporting multiple North American mine sites, integrating digital geotechnical instrumentation and real-time data analytics to enhance compliance reporting and risk mitigation performance. Source: www.tetratech.com

The Mining Waste Management Market Report provides a comprehensive evaluation of operational, technological, regulatory, and strategic dimensions across the global mining ecosystem. The report covers core segments including tailings management, waste rock management, mine water treatment, and site rehabilitation, which collectively address billions of metric tons of annual mining waste generated worldwide. It assesses infrastructure categories such as conventional slurry impoundments, dry stack tailings facilities, high-density thickening systems, and membrane-based water treatment plants. Geographically, the report analyzes five primary regions—Asia-Pacific, North America, Europe, South America, and the Middle East & Africa—covering over 30 key mining countries responsible for more than 85% of global mineral output. It evaluates metal mining, coal extraction, rare earth processing, and industrial mineral applications, highlighting differences in waste intensity, water usage patterns, and regulatory compliance requirements.

The scope further includes digital monitoring technologies such as IoT-based tailings sensors, satellite deformation tracking, AI-driven predictive analytics, and automated environmental reporting systems, now adopted by over 60% of large multinational mining enterprises. Emerging niche segments, including legacy tailings reprocessing and circular mineral recovery solutions capable of extracting up to 10% additional value from historical waste deposits, are also examined. Additionally, the report outlines regulatory frameworks, ESG performance metrics, dam safety compliance protocols, and mine closure obligations that influence capital allocation decisions. It provides strategic insights into infrastructure modernization, climate resilience planning, and water recycling systems achieving recovery rates above 80%, offering a structured foundation for investment, risk management, and long-term operational planning within the Mining Waste Management Market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

6.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Veolia, Hatch Ltd., Tetra Tech, Inc., Metso Corporation , WSP Global Inc., GHD Group, SRK Consulting, Knight Piésold, FLSmidth , Ausenco, SNC-Lavalin Group Inc., Klohn Crippen Berger, Worley Limited , DRA Global, Stantec Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |