Reports

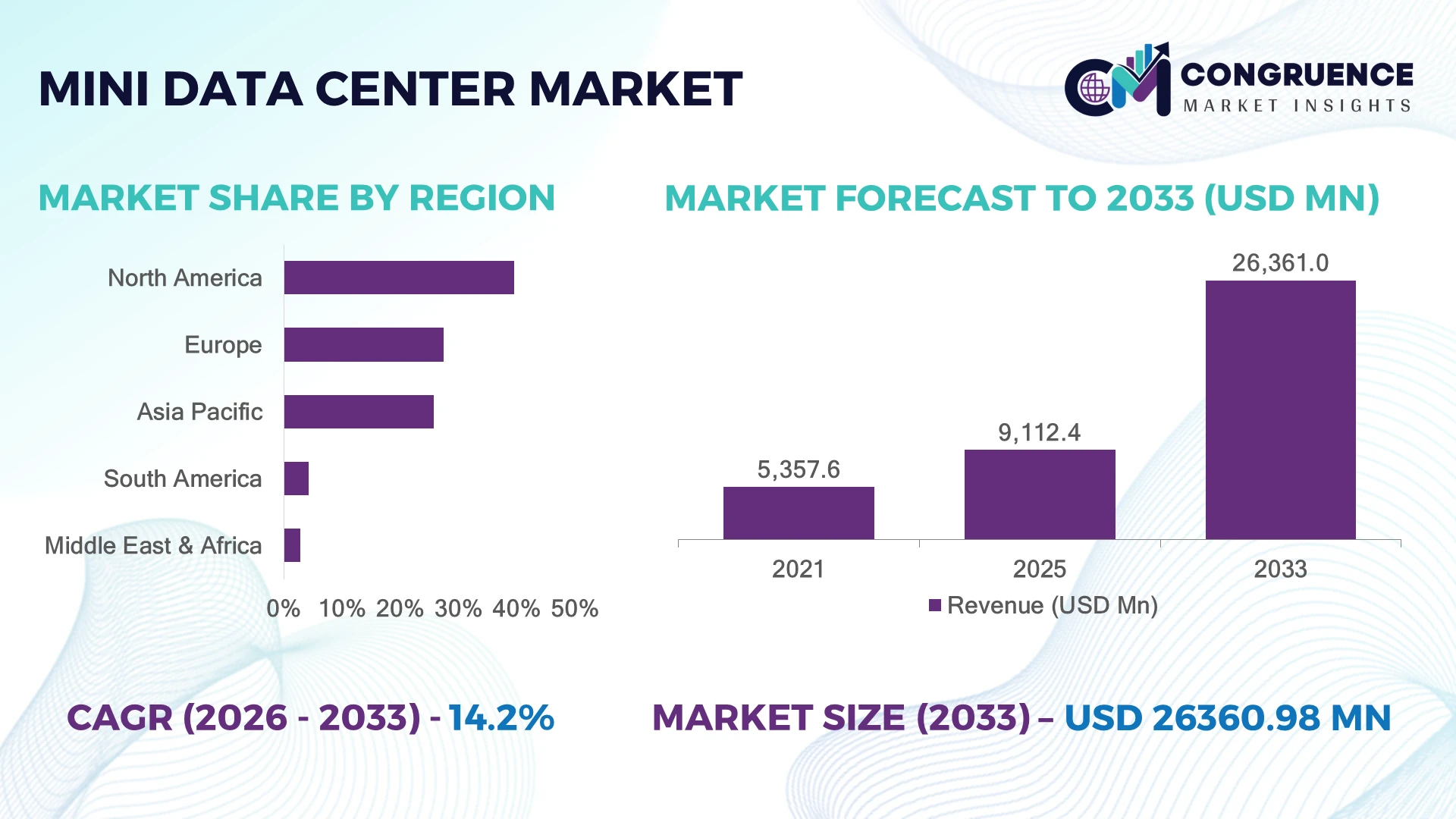

The Global Mini Data Center Market was valued at USD 9,112.4 Million in 2025 and is anticipated to reach a value of USD 26,361.0 Million by 2033 expanding at a CAGR of 14.2% between 2026 and 2033. Increasing edge computing adoption, AI workload expansion, IoT connectivity, and enterprise demand for low-latency digital infrastructure are accelerating Mini Data Center Market growth.

The United States dominated the Mini Data Center Market with nearly 38% share in 2025, supported by hyperscale technology ecosystems, enterprise digitization, and edge infrastructure investments. More than 55% of advanced edge deployments in the United States are linked to AI processing, telecom networks, and distributed computing applications, compared with approximately 42% adoption across leading European digital hubs. Global data localization strategies and supply-chain resilience initiatives have increased investment in decentralized computing infrastructure.

Enterprises adopting mini data center solutions are strengthening processing speed, operational continuity, and competitive advantage through localized digital infrastructure.

• Market Size & Growth: The market reached USD 9,112.4 Million in 2025 and is projected at USD 26,361.0 Million by 2033 with 14.2% CAGR, driven by edge computing expansion.

• Top Growth Drivers: Edge infrastructure adoption increased 45%, AI workload deployment rose 38%, and IoT connectivity expanded 35% globally.

• Short-Term Forecast: By 2028, advanced mini data centers are expected to reduce data processing latency by nearly 40%.

• Emerging Technologies: AI-enabled infrastructure, liquid cooling, automation, and modular designs are transforming distributed computing ecosystems.

• Regional Leaders: North America, Asia-Pacific, and Europe are projected to reach USD 9.8 Billion, USD 8.7 Billion, and USD 5.9 Billion respectively through enterprise adoption.

• Consumer/End-User Trends: Enterprises and telecom operators represent over 60% adoption due to increasing demand for localized computing.

• Pilot/Case Example: In 2025, edge infrastructure deployments improved real-time processing efficiency by nearly 35%.

• Competitive Landscape: Leading providers hold nearly 48% share, including Schneider Electric, Vertiv, Eaton, and Huawei.

• Regulatory & ESG Impact: Energy-efficient infrastructure designs are reducing data center power consumption by approximately 25%.

• Investment & Funding: Over USD 15 Billion investments focus on AI infrastructure, edge networks, and digital transformation projects.

• Innovation & Future Outlook: Next-generation mini data centers are shifting toward autonomous, scalable, and sustainable computing environments.

Mini data centers are enabling enterprises, telecom operators, and industrial facilities to deploy localized computing infrastructure closer to data sources. Advanced modular systems and intelligent power management solutions are improving deployment efficiency by nearly 30%. Growing AI workloads, data sovereignty requirements, and distributed network architectures are reshaping enterprise infrastructure strategies.

The Mini Data Center Market is becoming strategically important as enterprises transition from centralized infrastructure toward distributed, low-latency computing models. Growth in AI applications, smart manufacturing, and connected devices is increasing demand for compact, scalable, and rapidly deployable infrastructure. Data localization policies across major economies are encouraging businesses to strengthen regional computing capabilities.

Compared with traditional data center deployments, advanced modular mini data centers reduce installation timelines by nearly 40% and improve infrastructure scalability by approximately 35%. North America leads through AI infrastructure investments and enterprise cloud integration, while Asia-Pacific is expanding through 5G networks, industrial digitization, and smart city projects.

Telecom providers, manufacturing companies, and healthcare organizations are deploying mini data centers to support real-time analytics, automation, and secure data processing. Companies are increasing investment in prefabricated modules, intelligent monitoring, and energy-efficient technologies. Long-term competitiveness will depend on faster deployment capability, operational resilience, and optimized edge computing performance.

Rising demand for real-time data processing is accelerating mini data center adoption across telecom, manufacturing, healthcare, and enterprise environments. Nearly 50% of organizations implementing digital transformation strategies are investing in edge computing infrastructure to reduce latency and improve application performance. AI-enabled workloads have increased distributed computing requirements by approximately 38%. Enterprise infrastructure strategies in the United States are shifting toward decentralized architectures due to data security and operational continuity priorities. Companies are responding through modular product expansion, edge partnerships, and integrated power and cooling innovations.

Mini data center adoption faces limitations from upfront infrastructure investment, power management requirements, and integration challenges with existing IT environments. Nearly 32% of enterprises identify deployment cost and technical complexity as barriers during distributed infrastructure expansion. Advanced cooling, security, and monitoring requirements increase operational planning needs by approximately 25%. Supply-chain fluctuations affecting electronic components and power systems continue influencing project timelines. Companies are reducing risks through standardized modular designs, localized sourcing strategies, and managed infrastructure service models.

Increasing adoption of AI applications, automation platforms, and connected industrial ecosystems is creating opportunities for next-generation mini data centers. Nearly 45% of future enterprise workloads are expected to require faster localized processing to support real-time decision-making. Intelligent infrastructure technologies can improve energy efficiency by approximately 30% through automation and optimized resource management. Companies in Japan, South Korea, and the United States are expanding investments in AI-ready edge facilities. Providers are positioning through R&D, strategic partnerships, and integrated hardware-software ecosystems.

Managing large networks of distributed mini data centers creates challenges related to monitoring, cybersecurity, maintenance, and operational consistency. Nearly 35% of IT leaders identify edge infrastructure management complexity as a key deployment concern. Increasing connected environments require stronger automation, remote management, and security frameworks. Cybersecurity requirements across critical industries are creating pressure for advanced protection and compliance capabilities. Companies must strengthen AI-driven monitoring, predictive maintenance, and integrated management platforms to ensure reliable large-scale deployment.

• AI-Ready Edge Infrastructure: Mini data centers are increasingly optimized for AI workloads requiring faster processing near data sources. Nearly 45% of enterprise edge projects now prioritize AI compatibility and workload acceleration. Companies are integrating advanced processors, automation software, and intelligent cooling systems to improve infrastructure performance.

• Modular Deployment Expansion: Prefabricated and modular mini data centers are gaining adoption due to faster installation and flexible capacity scaling. Around 40% of new distributed infrastructure projects prefer modular configurations. Providers are standardizing designs, improving supply chains, and expanding deployment services to reduce implementation complexity.

• Advanced Cooling Innovation: Rising computing density is accelerating adoption of improved cooling technologies and intelligent energy management systems. Nearly 35% of new infrastructure upgrades include advanced thermal optimization solutions. Companies are developing efficient cooling platforms to manage AI-driven power requirements and operational costs.

• Telecom Edge Integration: 5G networks are increasing demand for localized computing capacity across telecom environments. More than 50% of telecom edge strategies include distributed infrastructure deployment. Operators are partnering with infrastructure providers to expand low-latency services, improve network reliability, and support connected applications.

Modular mini data centers dominate the Mini Data Center Market due to their scalability, faster deployment capability, standardized architecture, and ability to support distributed enterprise infrastructure. Modular systems account for nearly 58% of adoption, driven by demand from edge computing, telecom networks, and businesses requiring flexible capacity expansion. Containerized mini data centers are witnessing the fastest adoption shift as organizations prioritize mobility, rapid installation, and infrastructure deployment in remote or space-constrained locations.

Rack-level and micro data center solutions continue gaining relevance across branch offices, industrial facilities, retail networks, and localized computing environments requiring compact IT infrastructure. Nearly 45% of enterprise edge deployments are shifting toward pre-integrated systems to reduce installation complexity and improve operational efficiency. Companies are responding through advanced cooling integration, AI-based monitoring, modular designs, and strategic partnerships focused on improving deployment speed and lifecycle performance.

• A 2025 enterprise infrastructure assessment highlighted that organizations adopting modular and edge-ready data center systems reduced deployment timelines by nearly 40%, supporting faster digital transformation across manufacturing, telecom, and distributed business environments.

Edge computing represents the leading application segment in the Mini Data Center Market due to increasing requirements for low-latency processing, localized analytics, and real-time digital services. The segment accounts for nearly 42% of adoption as enterprises, telecom operators, and industrial facilities move computing resources closer to data generation points. Artificial intelligence and machine learning applications are witnessing the fastest adoption growth as organizations require high-performance localized infrastructure for data-intensive workloads.

Cloud computing support, IoT processing, disaster recovery, and remote IT operations continue expanding as businesses modernize infrastructure strategies. Nearly 50% of digital infrastructure projects are integrating distributed computing capabilities to improve responsiveness and reduce network dependency. Companies are adapting through AI-ready infrastructure solutions, automated management platforms, and scalable deployment models that strengthen operational flexibility and support evolving enterprise workloads.

• A 2026 digital infrastructure industry review indicated that enterprises deploying edge-based computing environments improved data processing efficiency by nearly 35%, accelerating adoption across smart manufacturing, telecommunications, and connected infrastructure applications.

IT and telecom companies represent the dominant end-user group in the Mini Data Center Market due to extensive requirements for network expansion, edge computing, and high-performance digital service delivery. This segment accounts for approximately 46% of demand as operators deploy localized infrastructure to support 5G networks, cloud services, and increasing data traffic. Manufacturing enterprises are becoming the fastest-growing end-user segment due to rising adoption of smart factories, automation systems, and industrial IoT applications.

Healthcare organizations, BFSI companies, government agencies, retail enterprises, and energy sectors are increasing investments in mini data centers to improve data security, continuity, and localized processing capabilities. Around 40% of enterprise infrastructure buyers are prioritizing compact and automated data center solutions. Providers are targeting these sectors through customized configurations, managed services, and industry-specific solutions to strengthen competitive positioning.

• A 2025 enterprise technology survey reported that organizations implementing distributed data center infrastructure improved operational resilience by nearly 30%, supporting wider adoption across telecom, manufacturing, financial services, and mission-critical business environments.

North America accounted for the largest market share at 39.6% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 15.8% between 2026 and 2033.

North America dominates the Mini Data Center Market due to rapid edge computing deployment, AI infrastructure investments, and strong adoption of distributed digital architectures. The region accounted for 39.6% market share in 2025, supported by hyperscale operators, telecom companies, and enterprises expanding localized computing capacity. Nearly 55% of advanced edge deployments are concentrated across AI processing, IoT networks, and real-time analytics environments. Increasing data localization priorities and resilient infrastructure planning have accelerated investment in modular systems. Companies are expanding mini data center deployments through AI-ready designs, advanced cooling solutions, and integrated infrastructure management platforms.

United States Market Outlook: The United States leads regional adoption through strong cloud ecosystems, advanced enterprise digitization, and large-scale edge infrastructure expansion. Technology providers and telecom operators are deploying mini data centers closer to users for faster processing. More than 60% of enterprise edge initiatives involve distributed computing solutions supporting AI applications, automation platforms, and latency-sensitive digital services.

Europe’s Mini Data Center Market is shaped by data sovereignty requirements, industrial digitization, and increasing demand for energy-efficient distributed infrastructure. The region accounted for nearly 27.4% market share in 2025, with Germany, the United Kingdom, and France leading adoption across manufacturing, telecom, and enterprise IT environments. Around 45% of digital infrastructure modernization programs include edge-based computing solutions to improve operational control and reduce latency. Companies are focusing on modular deployments, efficient cooling technologies, and intelligent monitoring systems aligned with evolving sustainability and data management priorities.

Germany Market Outlook: Germany represents the leading European market due to strong industrial automation, smart factory adoption, and advanced IT infrastructure. Manufacturing enterprises are deploying mini data centers to support real-time analytics and connected production systems. Nearly 50% of Industry 4.0 initiatives involve edge computing capabilities, strengthening demand for compact and scalable digital infrastructure.

Asia-Pacific is rapidly expanding in the Mini Data Center Market through increasing cloud adoption, 5G expansion, smart city programs, and industrial digitalization. The region accounted for approximately 25.8% market share in 2025, supported by China, Japan, India, and South Korea’s investment in connected infrastructure. More than 50% of new telecom edge deployments are linked to high-speed networks, IoT ecosystems, and localized processing requirements. Companies are scaling manufacturing partnerships, modular infrastructure solutions, and AI-enabled data center technologies to support rising digital workloads.

China Market Outlook: China leads Asia-Pacific adoption through large-scale digital infrastructure development, manufacturing automation, and expanding cloud ecosystems. Enterprises are increasing investment in distributed computing platforms to support AI, smart factories, and connected services. Over 55% of advanced technology infrastructure projects include edge computing integration, accelerating deployment of mini data center solutions.

South America’s Mini Data Center Market is expanding through increasing cloud adoption, telecom modernization, and enterprise demand for localized processing capabilities. The region accounted for nearly 4.3% market share in 2025, with adoption concentrated across financial services, telecom, and industrial sectors. Around 30% of large organizations are adopting distributed infrastructure to improve connectivity and business continuity. Limited advanced infrastructure availability creates deployment challenges; however, providers are strengthening partnerships, managed services, and modular solutions to improve accessibility.

Brazil Market Outlook: Brazil represents the leading regional market due to expanding digital services, financial technology adoption, and telecom infrastructure investments. Enterprises are deploying mini data centers to improve application performance and data availability. Nearly 40% of major digital transformation projects include edge infrastructure components, supporting demand for compact, secure, and scalable computing environments.

Middle East & Africa adoption is increasing through smart city development, cloud infrastructure expansion, and enterprise technology modernization. The region accounted for approximately 2.9% market share in 2025, with demand concentrated across government, telecom, energy, and financial sectors. More than 35% of large digital infrastructure initiatives include distributed computing technologies to support connected services and secure data processing. Companies are expanding regional partnerships, modular deployment capabilities, and managed infrastructure solutions to improve market accessibility.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional adoption through smart city investments, advanced connectivity initiatives, and enterprise cloud transformation. Organizations are implementing mini data centers across government, logistics, and commercial environments. Nearly 45% of major digital infrastructure projects include edge technologies, supporting faster processing, improved reliability, and next-generation connected services.

The Mini Data Center Market is led by Schneider Electric, Vertiv, Eaton, Huawei Technologies, and Dell Technologies, where global infrastructure providers compete with IT hardware specialists and edge computing innovators. The top five players collectively hold approximately 48% share, reflecting a competitive structure focused on modular design, energy efficiency, and rapid deployment capability. Competition is based on cooling efficiency, infrastructure reliability, integration speed, and customization, with advanced modular systems reducing deployment timelines by nearly 40% and improving energy efficiency by around 25%. Companies are competing through edge infrastructure expansion, AI-ready solutions, strategic partnerships, and integrated power management technologies. The competitive shift is moving toward intelligent monitoring, sustainable infrastructure, and pre-engineered data center platforms. Technical expertise, supply-chain control, and enterprise-grade reliability requirements create strong entry barriers. Winning against established players requires scalable designs, advanced automation, and efficient edge infrastructure solutions.

• Schneider Electric SE

• Vertiv Holdings Co.

• Eaton Corporation plc

• Huawei Technologies Co., Ltd.

• Dell Technologies Inc.

• Hewlett Packard Enterprise Company

• Rittal GmbH & Co. KG

• Delta Electronics Inc.

• IBM Corporation

• Panduit Corporation

• Cannon Technologies Ltd.

• Zella DC

• ScaleMatrix Holdings Inc.

• Instant Data Centers LLC

Mini data center technologies are advancing through modular infrastructure, AI-powered management platforms, intelligent cooling systems, and edge computing integration. Current solutions focus on faster deployment, remote monitoring, and optimized resource utilization for enterprises, telecom networks, and industrial environments. Nearly 50% of new distributed infrastructure deployments are integrating automation capabilities to improve reliability and reduce operational complexity.

Compared with traditional data center construction, next-generation modular mini data centers reduce deployment time by approximately 40% and improve power management efficiency by nearly 25% through prefabricated architectures, advanced cooling, and intelligent monitoring systems. AI-based infrastructure management enables predictive maintenance, workload optimization, and improved uptime. Providers with strong power, cooling, software, and edge ecosystem capabilities are gaining competitive advantages.

Between 2026 and 2028, technology development will focus on AI-ready edge facilities, liquid cooling integration, autonomous infrastructure management, and sustainable modular designs. Enterprises adopting these technologies will strengthen digital resilience, reduce latency, and improve operational scalability across distributed computing environments.

• March 2025 – Schneider Electric expanded its modular data center solutions with AI-ready infrastructure enhancements, improving deployment efficiency by nearly 30%. The development strengthened enterprise edge computing capabilities and supported faster implementation of distributed digital infrastructure. Source: se.com

• October 2024 – Vertiv introduced advanced prefabricated and modular infrastructure solutions designed for AI and edge workloads, improving scalability and deployment speed by approximately 25%. The expansion supported enterprises managing higher computing density requirements. Source: vertiv.com

• February 2025 – Eaton enhanced its intelligent power management solutions for distributed data center environments, improving energy optimization capabilities by nearly 20%. The advancement supported reliable operation of compact infrastructure deployments and enterprise edge facilities. Source: eaton.com

• June 2024 – Rittal expanded its edge data center infrastructure portfolio with modular IT systems and integrated cooling technologies, improving infrastructure deployment flexibility by approximately 25%. The initiative strengthened support for industrial digitization and decentralized computing applications. Source: rittal.com

The Mini Data Center Market Report provides detailed analysis across types, applications, end-users, regional developments, technology advancements, and competitive strategies. The study covers modular mini data centers, containerized systems, rack-level solutions, and micro data centers deployed across edge computing, cloud support, IoT processing, disaster recovery, and remote IT operations. More than 60% of adoption is driven by enterprises and telecom operators requiring distributed infrastructure.

The report evaluates North America, Europe, Asia-Pacific, South America, and Middle East & Africa with insights into AI infrastructure expansion, digital transformation, and edge computing adoption. It examines intelligent cooling, automation platforms, modular architecture, and next-generation infrastructure technologies shaping market direction between 2026 and 2033. The analysis supports investment planning, technology selection, competitive positioning, and expansion strategies across evolving digital infrastructure ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 9,112.4 Million |

|

Market Revenue in 2033 |

USD 26,361.0 Million |

|

CAGR (2026 - 2033) |

14.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Schneider Electric SE, Vertiv Holdings Co., Eaton Corporation plc, Huawei Technologies Co., Ltd., Dell Technologies Inc., Hewlett Packard Enterprise Company, Rittal GmbH & Co. KG, Delta Electronics Inc., IBM Corporation, Panduit Corporation, Cannon Technologies Ltd., Zella DC, ScaleMatrix Holdings Inc., Instant Data Centers LLC |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |