Reports

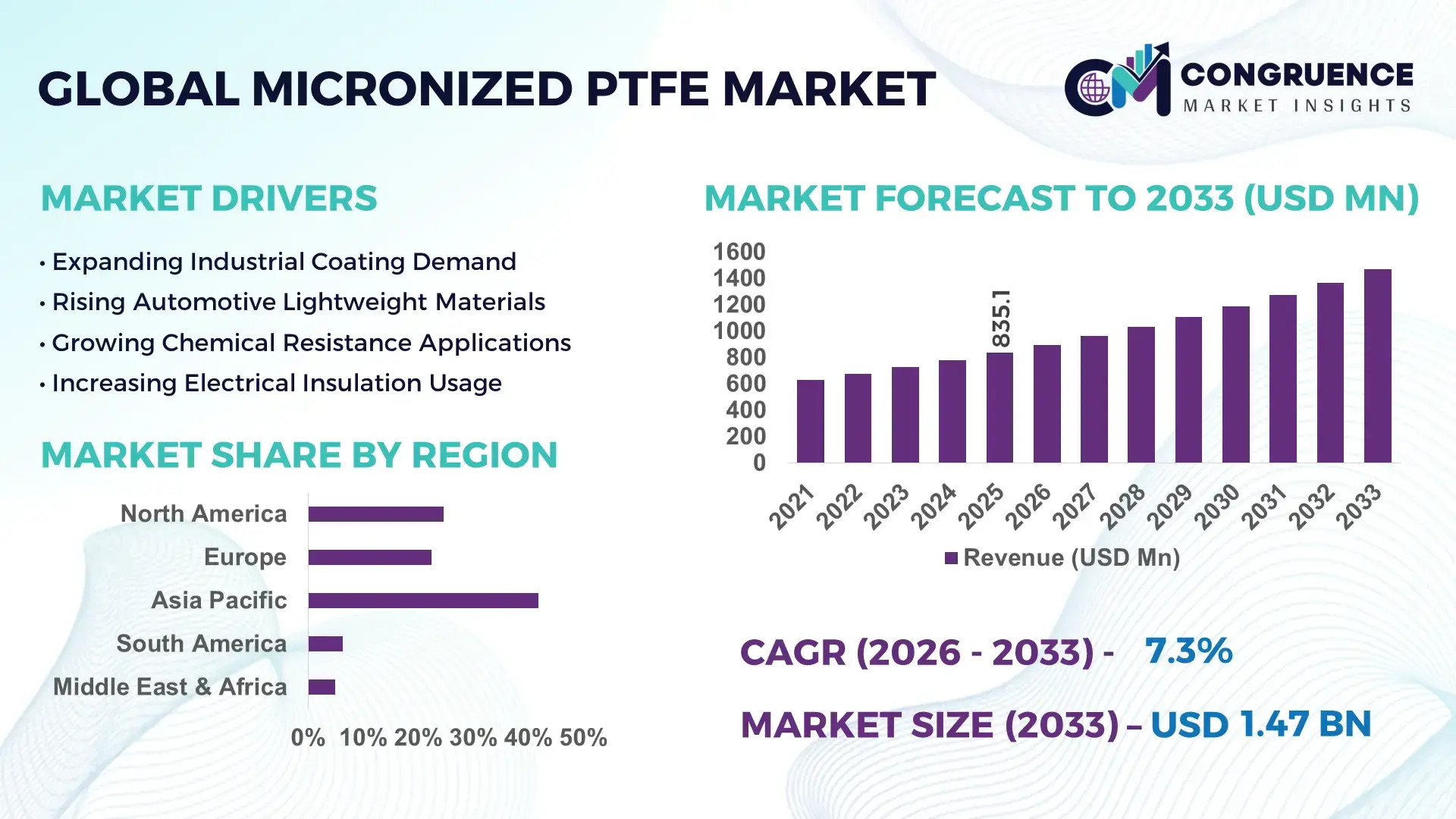

The Global Micronized PTFE Market was valued at USD 835.1 Million in 2025 and is anticipated to reach a value of USD 1,467.4 Million by 2033 expanding at a CAGR of 7.3% between 2026 and 2033. Growth is being driven by rising use of micronized PTFE additives in high-performance coatings, engineering plastics, and low-friction industrial lubrication systems requiring superior wear resistance and surface modification.

China dominates the market with an estimated 34% share of global micronized PTFE consumption, supported by over 65% of Asia’s fluoropolymer processing capacity and sustained investment in advanced coatings, electronics, and automotive manufacturing. Compared with Germany, China operates more than three times the fluoropolymer production volume, while industrial coatings adoption exceeds 40% across key manufacturing clusters. Ongoing supply-chain diversification following global trade realignments has further strengthened domestic value-chain integration and export competitiveness.

For market participants, securing raw material access and application-specific formulation expertise remains the most effective strategy for strengthening competitive positioning.

Market Size & Growth: USD 835.1 Million in 2025 reaching USD 1,467.4 Million by 2033, supported by expanding use in advanced coatings, engineering polymers, and industrial lubrication technologies.

Top Growth Drivers: Coatings demand +18%, engineering plastics adoption +15%, industrial lubricant consumption +12% across key manufacturing sectors.

Short-Term Forecast: By 2028, wear resistance performance in premium coating formulations improves by nearly 20% through optimized additive integration.

Emerging Technologies: AI-assisted formulation design, advanced dispersion technologies, and precision particle engineering improve consistency and application efficiency.

Regional Leaders: Asia Pacific exceeds USD 620 Million, Europe approaches USD 340 Million, and North America surpasses USD 280 Million, driven by automotive, electronics, and industrial modernization.

Consumer/End-User Trends: More than 55% of premium industrial coatings now incorporate performance-enhancing fluoropolymer additives for durability gains.

Pilot/Case Example: In 2024, a specialty coatings project achieved 22% lower friction coefficients and 17% longer service life through micronized PTFE integration.

Competitive Landscape: Leading suppliers collectively control nearly 45% market share, with major participation from Shamrock Technologies, Chemours, Solvay, Daikin, and AGC.

Regulatory & ESG Impact: Low-VOC coating adoption increased by 19%, encouraging advanced additive utilization and improved material efficiency.

Investment & Funding: More than USD 250 Million has been directed toward fluoropolymer capacity expansion and specialty materials partnerships since 2023.

Innovation & Future Outlook: Next-generation ultra-fine particle grades and multifunctional surface-modification additives are reshaping high-performance materials strategies.

Micronized PTFE has become an essential performance additive across industrial coatings, inks, thermoplastics, and lubricant formulations where low friction, scratch resistance, and durability are critical. Recent innovations in particle-size control and dispersion technology have improved formulation efficiency by nearly 15%, while manufacturers increasingly prioritize localized sourcing strategies amid evolving fluorochemical regulations and global supply-chain restructuring. This transition is creating new opportunities for application-specific product development and strategic portfolio expansion.

Micronized PTFE is becoming strategically important as manufacturers pursue longer product life cycles, lower maintenance costs, and enhanced material performance across industrial value chains. The market sits at the intersection of advanced materials engineering and industrial productivity, making it increasingly relevant for coatings, plastics, electronics, and automotive applications. Supply-chain restructuring following geopolitical trade adjustments has encouraged companies to diversify sourcing networks and establish regional processing capabilities.

Compared with conventional wax additives, micronized PTFE formulations can improve abrasion resistance by more than 20% while reducing friction coefficients by up to 30% in selected industrial applications. China maintains a scale advantage through extensive fluoropolymer infrastructure, whereas Germany and Japan focus on precision-engineered specialty grades for high-value manufacturing sectors. Over the next two to three years, adoption in advanced coatings and engineering compounds is expected to accelerate as manufacturers prioritize durability and operational efficiency.

A practical example can be seen in industrial coating producers integrating micronized PTFE into premium formulations to reduce equipment wear and extend maintenance intervals. Companies are expanding application laboratories, strengthening distributor partnerships, and investing in customized additive solutions. Organizations that secure technical differentiation and resilient supply networks will gain stronger competitive positioning as performance materials become increasingly critical to industrial innovation.

Demand for durable coatings and engineered materials continues to accelerate across automotive, electronics, and industrial manufacturing sectors. More than 55% of premium industrial coatings now incorporate advanced performance additives, while wear-resistant coating adoption has increased by approximately 18% in major manufacturing economies. Engineering plastics applications utilizing friction-reduction technologies have expanded by nearly 15% over the past few years. Following global manufacturing relocation trends, producers in China and India have expanded specialty materials investments to support localized production. The result is stronger demand for micronized PTFE as a surface-modification component. Companies are responding through capacity expansions, application-specific product development, and collaborative partnerships with coating formulators to capture higher-value industrial opportunities and strengthen technical differentiation.

The market remains exposed to fluctuations in fluoropolymer feedstock availability and specialty chemical pricing. Raw material expenses can account for 35%–45% of production costs, creating significant margin pressure during supply disruptions. Regulatory scrutiny surrounding fluorochemical processing has increased compliance expenditures by approximately 10%–15% for some manufacturers. China’s dominant position in fluoropolymer production also creates concentration risks across international supply networks. These structural constraints affect procurement planning, inventory management, and long-term contract negotiations. To reduce exposure, companies are diversifying supplier bases, investing in regional production assets, and securing multi-year procurement agreements. Firms that successfully localize critical supply chains gain stronger operational resilience and improved pricing stability.

The emergence of multifunctional materials presents substantial opportunities beyond traditional coatings and lubricants. Demand for high-performance engineering compounds has increased by nearly 16%, while specialty additive usage in electronics applications has grown by approximately 13%. Ultra-fine particle technologies and advanced dispersion systems are improving formulation efficiency and material utilization rates. In Japan and South Korea, manufacturers are investing in precision-engineered materials for electronics and semiconductor-related applications requiring enhanced surface performance. Companies are positioning through research partnerships, pilot-scale innovation programs, and customized additive platforms. A particularly attractive opportunity lies in combining micronized PTFE with next-generation polymer systems to deliver simultaneous improvements in wear resistance, processing efficiency, and product longevity.

Maintaining consistent product performance across multiple industries remains a complex execution challenge. Customer specifications can vary by more than 25% between coatings, plastics, inks, and lubrication applications, requiring extensive formulation customization. Quality-control requirements have intensified as manufacturers target tighter particle-size distributions and improved dispersion characteristics. In advanced manufacturing environments, even small formulation inconsistencies can affect durability and operational reliability. Companies must invest heavily in laboratory infrastructure, technical support capabilities, and process optimization systems to meet increasingly demanding performance standards. Strategic success depends on balancing scalability with customization while maintaining product consistency across global production networks, a challenge that directly influences competitiveness and long-term customer retention.

Ultra-Fine Particle Grade Expansion Advanced coatings and engineering plastics manufacturers are increasingly shifting toward ultra-fine micronized PTFE grades, with adoption rising by nearly 22% across industrial formulations. Particle-size optimization has reduced dispersion time by 15% while improving scratch resistance by over 18%. Chinese and Japanese producers are expanding specialty product portfolios and upgrading milling technologies to meet precision-performance requirements, strengthening differentiation in high-value industrial applications.

Localized Supply Network Development Supply-chain restructuring continues to reshape procurement strategies, with over 35% of large specialty chemical buyers increasing regional sourcing commitments. Inventory lead times have improved by approximately 12%, while logistics-related cost exposure has declined by 8% among localized operators. In response to trade uncertainties and fluorochemical compliance requirements, manufacturers are establishing regional distribution hubs and expanding toll-processing partnerships to improve operational continuity.

Advanced Coatings Integration Growth Industrial coatings remain a focal point for innovation, with more than 55% of premium wear-resistant formulations incorporating performance-enhancing fluoropolymer additives. Coating service life improvements of 20% and friction reduction of nearly 25% are accelerating adoption in automotive, machinery, and metal-processing applications. Companies are strengthening technical collaboration with coating formulators and investing in application laboratories to accelerate commercial deployment cycles.

Automation-Driven Production Optimization Specialty material producers are integrating digital process controls and automated particle-classification systems, improving batch consistency by nearly 17% and reducing production deviations by 12%. Labor constraints and stricter quality requirements are accelerating automation investments across fluoropolymer processing facilities. Leading manufacturers are deploying real-time monitoring platforms and predictive maintenance systems to improve throughput, reduce waste, and support scalable production of customized micronized PTFE grades.

Virgin micronized PTFE remains the leading type segment, accounting for an estimated 48% of total market demand due to its superior purity, low-friction performance, and compatibility with high-performance coatings, inks, and engineering polymers. Its ability to deliver consistent particle morphology and enhanced wear resistance makes it the preferred choice in automotive, electronics, and industrial manufacturing applications. Companies continue to prioritize virgin-grade production through capacity upgrades and process optimization initiatives aimed at improving dispersion characteristics and product consistency. Modified micronized PTFE is emerging as the fastest-growing type segment, supported by increasing demand for customized surface properties and enhanced processing performance. Adoption of modified grades has increased by nearly 16% in advanced industrial applications where specialized friction control and durability are required. Reprocessed and recycled grades continue to gain strategic relevance in cost-sensitive formulations, particularly within industrial coatings and lubricant applications. Manufacturers are investing in application-specific product development, strategic partnerships, and advanced particle-engineering technologies to address evolving customer requirements and strengthen competitive positioning across premium and value-oriented segments.

Coatings represent the largest application segment, contributing approximately 42% of total micronized PTFE consumption due to widespread use in industrial equipment, automotive components, architectural surfaces, and corrosion-resistant systems. Demand remains concentrated in applications requiring low friction, improved scratch resistance, and longer maintenance cycles. More than 55% of premium industrial coating formulations now incorporate performance-enhancing fluoropolymer additives, reinforcing the segment’s dominant position. Manufacturers are expanding technical service capabilities and collaborating with coating formulators to accelerate product qualification and deployment. Engineering plastics are the fastest-growing application segment, supported by increasing requirements for lightweight materials, improved wear performance, and component longevity. Adoption within engineering compounds has increased by approximately 15% as manufacturers seek to improve mechanical performance without significantly increasing material weight. Inks, lubricants, and specialty composites continue to expand steadily, particularly in industrial printing and machinery applications. Companies are investing in customized additive technologies, automation-enabled production systems, and application-specific formulations to capture emerging demand and strengthen market penetration across diverse industrial sectors.

Industrial manufacturing remains the dominant end-user segment, representing approximately 45% of overall demand due to extensive use of micronized PTFE in coatings, engineered materials, lubricants, and production equipment. Heavy machinery, metal processing, industrial automation, and equipment maintenance applications continue to generate substantial consumption volumes. Increasing focus on operational efficiency and asset longevity has encouraged manufacturers to adopt advanced material technologies capable of reducing wear and maintenance frequency. Suppliers are responding through customized product portfolios and expanded technical support programs. Automotive manufacturing is emerging as the fastest-growing end-user segment, with adoption increasing by nearly 14% as producers prioritize lightweight materials, durability enhancement, and friction reduction technologies. Electronics and electrical equipment manufacturers are also increasing utilization of micronized PTFE in specialty materials and precision components. Chemical processing, construction materials, and specialty manufacturing industries remain important contributors, particularly where corrosion resistance and surface performance are operational priorities. Companies are strengthening partnerships with OEMs, investing in localized distribution networks, and developing sector-specific formulations to improve customer retention and expand application reach.

Asia-Pacific accounted for the largest market share at 41.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.1% between 2026 and 2033.

North America accounted for approximately 24.6% of global market activity in 2025, supported by strong demand from industrial coatings, engineered plastics, specialty lubricants, and advanced manufacturing applications. The region benefits from a mature fluoropolymer value chain, extensive R&D infrastructure, and high adoption of performance-enhancing additives across automotive and aerospace production. More than 60% of premium industrial coating manufacturers in the United States incorporate advanced fluoropolymer technologies into wear-resistant formulations. Capacity optimization initiatives and strategic supply agreements have increased domestic material availability while reducing procurement volatility. Companies are focusing on product customization, application engineering, and technical service expansion to support high-specification industrial customers.

United States Market Outlook: The United States remains the region’s largest market due to its advanced manufacturing ecosystem, strong aerospace presence, and extensive industrial coatings sector. More than 70% of North American fluoropolymer-related research activity is concentrated in the country, supporting continuous innovation in specialty additive technologies. Major manufacturers are expanding application laboratories and strengthening OEM partnerships to improve product performance, accelerate qualification cycles, and support increasingly demanding industrial specifications across automotive, defense, and electronics industries.

Europe represented nearly 22.4% of global market activity in 2025, supported by strong industrial manufacturing capabilities and increasing emphasis on durable, resource-efficient material solutions. Regulatory focus on product longevity and maintenance reduction is encouraging broader use of advanced additive technologies in coatings and engineering compounds. Industrial coating modernization programs have increased adoption of wear-resistant formulations by approximately 18% across key manufacturing sectors. The region’s specialty chemicals industry continues to invest in process efficiency improvements and high-performance materials development. Companies are prioritizing advanced formulation technologies and strategic collaborations to align with evolving industrial performance requirements.

Germany Market Outlook: Germany serves as the technological center of the European market due to its leadership in automotive engineering, industrial machinery, and specialty chemical manufacturing. The country accounts for a significant share of Europe’s high-performance coatings production and continues to invest in advanced materials research. More than 45% of industrial machinery exporters utilize enhanced surface engineering technologies to improve component durability. Strong integration between manufacturers, research institutes, and industrial end users supports continuous innovation and rapid commercialization of specialty micronized PTFE applications.

Asia-Pacific led the global market with a 41.8% share in 2025, supported by extensive fluoropolymer processing infrastructure, expanding industrial manufacturing, and strong demand from coatings, plastics, electronics, and automotive sectors. The region produces a substantial portion of global fluoropolymer intermediates and maintains a dominant position in downstream processing activities. Industrial coatings adoption has increased by more than 20% across key manufacturing economies, while specialty materials investments continue to accelerate. Manufacturers are expanding production facilities, strengthening export networks, and integrating advanced particle-processing technologies to improve efficiency and support growing international demand.

China Market Outlook: China remains the most influential country market due to its large-scale fluoropolymer production ecosystem and extensive industrial manufacturing base. The country accounts for an estimated 34% of global micronized PTFE consumption and operates more than 65% of Asia’s fluoropolymer processing capacity. Strong demand from automotive, electronics, and industrial coatings sectors continues to support capacity expansion. Domestic producers are investing heavily in advanced milling technologies, product quality improvements, and export-oriented production strategies to strengthen competitiveness across global specialty materials markets.

South America accounted for approximately 6.3% of global market activity in 2025, driven primarily by industrial coatings, mining equipment maintenance, and manufacturing modernization initiatives. Demand is increasing as companies seek improved wear resistance and lower maintenance costs in harsh operating environments. Adoption of advanced industrial coating systems has risen by nearly 14% among major manufacturing facilities. However, dependence on imported specialty materials and limited regional production capacity continue to influence procurement strategies. Market participants are addressing these constraints through distribution partnerships, localized inventory management, and expanded technical support capabilities.

Brazil Market Outlook: Brazil represents the largest market in South America due to its diversified industrial sector, mining operations, and automotive manufacturing footprint. Industrial maintenance programs increasingly utilize advanced surface-modification technologies to improve equipment reliability and reduce downtime. More than 40% of regional industrial output originates from Brazil, creating significant demand for specialty additives and performance materials. Manufacturers and distributors are expanding local technical service networks to support growing requirements across industrial processing, infrastructure, and heavy-equipment applications.

The Middle East & Africa accounted for approximately 4.9% of global market activity in 2025, supported by infrastructure development, industrial diversification programs, and expanding energy-sector investments. Demand is particularly strong in corrosion-resistant coatings, industrial maintenance applications, and equipment protection systems used in challenging operating environments. Industrial modernization initiatives have increased deployment of advanced coating technologies by nearly 12% across major energy and processing facilities. Companies are strengthening regional partnerships and establishing distribution networks to improve product accessibility and technical support capabilities.

Saudi Arabia Market Outlook: Saudi Arabia is the most strategically significant market within the region due to large-scale industrial diversification initiatives and ongoing investments in petrochemicals, manufacturing, and infrastructure. Industrial operators are increasingly adopting advanced material technologies to enhance equipment durability and reduce lifecycle maintenance costs. More than 30% of the region’s large industrial expansion projects are concentrated in the country, supporting sustained demand for specialty coatings and engineered material solutions. Continued investment in manufacturing localization and industrial development strengthens long-term opportunities for micronized PTFE suppliers and technology partners.

The competitive landscape is led by global fluoropolymer specialists including Chemours, Daikin Industries, AGC Inc., Shamrock Technologies, and Solvay. Global technology leaders compete directly with regional cost-focused suppliers, while specialty additive innovators compete against large-scale integrated fluoropolymer producers. The top five players collectively control approximately 45–50% of global market activity.

Competition is driven by particle-size consistency, formulation performance, supply reliability, and customization capability rather than price alone. Premium micronized PTFE grades can command 15–25% higher pricing when delivering superior wear resistance and dispersion performance. Lead-time reductions of 10–15% and formulation efficiency gains exceeding 20% increasingly influence purchasing decisions.

Market participants are expanding specialty production, strengthening distributor partnerships, integrating downstream processing, and developing application-specific grades. The competitive shift is moving toward technical differentiation and fluoropolymer supply security. Regulatory pressure and fluorochemical sourcing complexity create significant entry barriers. Winning requires advanced processing expertise, resilient supply chains, and customer-specific performance innovation.

Solvay

Micro Powders Inc.

3M Company

Dongyue Group Ltd.

HaloPolymer OJSC

Gujarat Fluorochemicals Limited

Asahi Yukizai Corporation

KITAMURA LIMITED

Fluoroadditive GmbH

Micronized PTFE technology is rapidly advancing from conventional grinding and classification methods toward precision particle-engineering platforms. Modern ultra-fine particle production systems improve particle-size consistency by nearly 18% while reducing formulation variability by approximately 15%. More than 55% of premium industrial coatings now utilize engineered micronized PTFE grades designed for enhanced scratch resistance and friction control. These technologies deliver measurable performance improvements across coatings, plastics, and lubrication applications while enabling manufacturers to target higher-value specialty markets.

Advanced dispersion technology and automated particle-classification systems are emerging as key competitive differentiators. Compared with traditional dispersion methods, next-generation processing technologies improve additive distribution efficiency by up to 25% and reduce processing time by nearly 12%. Digital process monitoring and automated quality-control systems are now deployed across approximately 40% of large fluoropolymer processing facilities. Specialty additive manufacturers and integrated fluoropolymer producers benefit most through improved product consistency, reduced waste, and faster customer qualification cycles.

Between 2026 and 2028, surfactant-reduced fluoropolymer processing, recycled fluorine feedstock integration, and AI-assisted formulation development are expected to reshape product innovation strategies. Companies adopting these technologies early will gain stronger regulatory positioning, improved production efficiency, and greater access to advanced electronics, industrial coatings, and engineered materials applications. Technology leadership is increasingly becoming the primary factor separating premium suppliers from commodity-focused competitors.

August 2024 – AGC Inc. developed a fluoropolymer manufacturing process that eliminates surfactants while maintaining conventional material performance and significantly reducing fluorinated byproduct generation. The innovation strengthens long-term regulatory readiness and sustainable fluoropolymer production capabilities. Source: www.agcchem.com

March 2025 – AGC Inc. commenced planned operations from its fluorochemical capacity expansion program at the Chiba facility, supported by an investment of approximately ¥35 billion. The expansion improves supply availability for semiconductor and advanced industrial applications.

December 2025 – AGC Inc. completed the world's first UL2809 third-party verification for PTFE resin manufactured using recycled fluorite. The development advances circular fluorine resource utilization and strengthens sustainability credentials for semiconductor-grade fluoropolymer materials.

December 2025 – AGC Inc. announced expansion of UL2809 verification coverage across additional fluoropolymer product lines following successful validation of Fluon PTFE G grade materials. The initiative supports traceability, recycled-content certification, and customer compliance requirements.

The Micronized PTFE Market Report provides comprehensive analysis of industry structure, competitive dynamics, technology evolution, and demand patterns across the global value chain. The study evaluates major type categories including virgin, modified, recycled, and specialty micronized PTFE grades, alongside key applications such as coatings, engineering plastics, inks, lubricants, and advanced industrial materials. Coverage extends across industrial manufacturing, automotive, electronics, chemical processing, and other strategic end-user segments. Regional assessment spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, representing more than 95% of global industry activity.

The report incorporates evaluation of advanced particle-engineering technologies, automated processing systems, sustainability-focused fluoropolymer innovations, and emerging specialty-material opportunities. Analysis includes market concentration trends, adoption patterns, supply-chain developments, and competitive positioning strategies. More than 40% of the assessment focuses on technology-driven applications and high-performance industrial use cases. The findings support investment prioritization, product development planning, expansion decisions, partnership evaluation, and long-term strategic positioning across the 2026–2033 planning horizon.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 835.1 Million |

| Market Revenue (2033) | USD 1,467.4 Million |

| CAGR (2026–2033) | 7.3% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Chemours; Daikin Industries; AGC Inc.; Shamrock Technologies; Solvay; Micro Powders Inc.; 3M Company; Dongyue Group Ltd.; HaloPolymer OJSC; Gujarat Fluorochemicals Limited; Asahi Yukizai Corporation; KITAMURA LIMITED; Fluoroadditive GmbH |

| Customization & Pricing | Available on Request (10% Customization Free) |