Reports

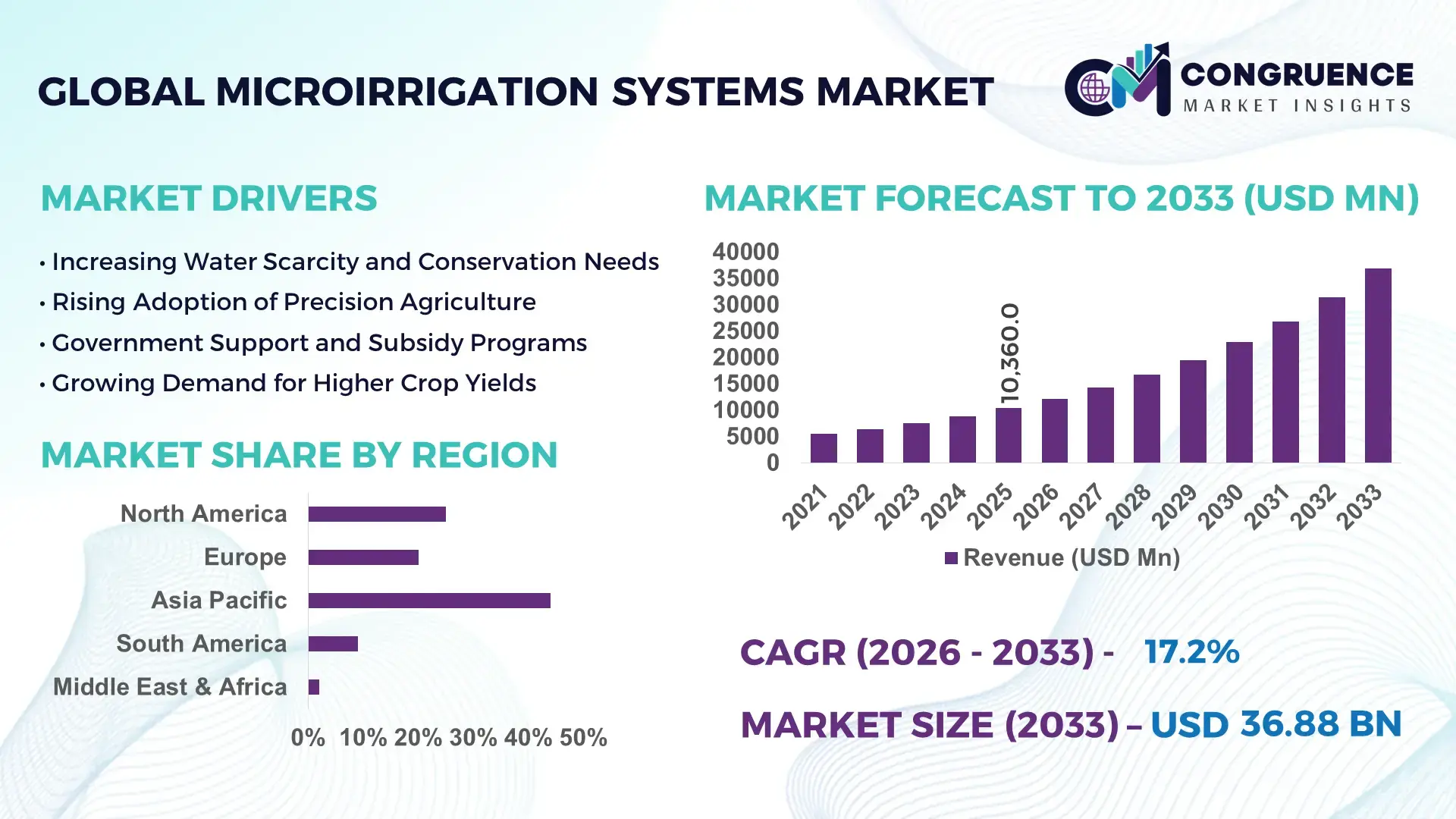

The Global Microirrigation Systems Market was valued at USD 10359.98 Million in 2025 and is anticipated to reach a value of USD 36879.06 Million by 2033 expanding at a CAGR of 17.2% between 2026 and 2033. This growth is driven by increasing demand for water-efficient precision agriculture solutions amid rising water scarcity and the need to enhance crop productivity.

India stands out as a dominant country in the microirrigation systems market, supported by extensive agricultural land exceeding 140 million hectares and strong government-backed irrigation initiatives. Over 15 million hectares are already under microirrigation coverage, with annual expansion rates surpassing 8–10% in key states such as Maharashtra, Gujarat, and Karnataka. Public and private investments in drip and sprinkler irrigation infrastructure have crossed USD 1.5 billion annually, while subsidy schemes cover up to 55% of installation costs for small farmers. Advanced fertigation technologies and IoT-enabled irrigation controllers are increasingly adopted, with over 20% of large-scale farms integrating smart irrigation systems. The horticulture sector accounts for more than 40% of microirrigation adoption, reflecting high-value crop dependency and efficiency-driven farming practices.

Market Size & Growth: Valued at USD 10,359.98 million in 2025 and projected to reach USD 36,879.06 million by 2033, growing at 17.2% CAGR due to rising adoption of water-saving irrigation technologies.

Top Growth Drivers: Water savings efficiency up to 50%, crop yield improvement by 30%, and fertilizer usage reduction by 25%.

Short-Term Forecast: By 2028, smart irrigation systems are expected to reduce water consumption by 20% and operational costs by 15%.

Emerging Technologies: IoT-enabled irrigation controllers, AI-driven soil moisture analytics, and automated drip fertigation systems.

Regional Leaders: Asia-Pacific projected at USD 15 billion by 2033 with strong smallholder adoption; North America at USD 8 billion driven by precision agriculture; Europe at USD 6 billion focusing on sustainability compliance.

Consumer/End-User Trends: Increasing adoption among horticulture farmers, greenhouse operators, and commercial agriculture enterprises prioritizing water efficiency.

Pilot or Case Example: In 2024, a large-scale farm deployment achieved 35% water savings and 28% yield improvement using sensor-based drip irrigation.

Competitive Landscape: Market leader holds approximately 18% share, followed by key players focusing on integrated irrigation technologies and global expansion strategies.

Regulatory & ESG Impact: Government subsidies covering up to 50% installation costs and mandates for water conservation driving adoption.

Investment & Funding Patterns: Over USD 2 billion invested globally in irrigation infrastructure and agri-tech innovations in recent years.

Innovation & Future Outlook: Integration of AI, satellite monitoring, and climate-responsive irrigation systems shaping next-generation farming practices.

The microirrigation systems market is characterized by strong contributions from sectors such as horticulture, which accounts for over 40% of installations, followed by field crops at approximately 35% and greenhouse farming at nearly 15%. Innovations such as pressure-compensated drip lines, automated fertigation units, and solar-powered irrigation pumps are transforming operational efficiency. Regulatory frameworks promoting water conservation and sustainable agriculture are accelerating adoption, especially in drought-prone regions. Asia-Pacific leads in consumption volume, while North America and Europe show higher penetration of advanced precision irrigation technologies. Emerging trends include integration with satellite-based weather forecasting and AI-driven irrigation scheduling, enabling data-driven agriculture and optimized resource utilization for long-term sustainability.

The microirrigation systems market holds significant strategic relevance as global agriculture transitions toward resource-efficient and climate-resilient practices. Precision irrigation technologies are enabling farmers to optimize water usage, improve crop yields, and reduce input costs, positioning the market as a critical enabler of sustainable food production. Advanced IoT-enabled irrigation systems deliver up to 45% improvement in water efficiency compared to traditional flood irrigation methods, while AI-based soil monitoring systems enhance irrigation accuracy by nearly 30% over manual scheduling.

Asia-Pacific dominates in volume due to large agricultural landholdings and widespread adoption in developing economies, while North America leads in technological adoption with over 60% of commercial farms utilizing smart irrigation solutions. By 2028, AI-integrated irrigation platforms are expected to improve water-use efficiency by 25% and reduce labor dependency by 20%, supporting scalable precision agriculture models.

From an ESG perspective, firms are committing to measurable sustainability goals, including reducing agricultural water consumption by 30% and minimizing fertilizer runoff by 20% by 2030. In 2024, a large agricultural initiative in Israel achieved a 40% reduction in water usage through sensor-driven drip irrigation combined with predictive analytics, demonstrating measurable impact and scalability. Strategically, the market is evolving toward fully automated, data-driven irrigation ecosystems integrated with climate intelligence platforms. These advancements position the Microirrigation Systems Market as a foundational pillar for agricultural resilience, regulatory compliance, and long-term sustainable growth across global food systems.

Water scarcity has become a critical global concern, with agriculture accounting for nearly 70% of freshwater withdrawals. Microirrigation systems offer up to 50% water savings compared to conventional irrigation methods, making them essential for sustainable farming. Countries facing acute water shortages are rapidly adopting drip and sprinkler systems to optimize water usage. In regions such as India and China, government-backed irrigation programs have expanded coverage significantly, with millions of hectares transitioning to microirrigation annually. Additionally, climate variability and irregular rainfall patterns are forcing farmers to adopt controlled irrigation systems to ensure consistent crop output. These factors collectively drive strong demand for advanced microirrigation technologies across both developed and developing agricultural economies.

Despite long-term benefits, the high upfront cost of microirrigation systems remains a significant barrier, particularly for small and marginal farmers. Installation costs can range between USD 1,000 to USD 2,500 per hectare depending on system complexity and crop type. Maintenance requirements, including periodic replacement of drip lines and filters, add to operational expenses. Limited access to financing and credit facilities in rural areas further restricts adoption. Additionally, lack of technical awareness and training among farmers reduces effective utilization, leading to suboptimal performance. While subsidies help offset costs, inconsistent policy implementation and delayed disbursements in some regions continue to hinder widespread adoption of microirrigation systems.

The integration of microirrigation systems with smart agriculture technologies presents significant growth opportunities. IoT-based irrigation systems enable real-time monitoring of soil moisture, weather conditions, and crop requirements, improving irrigation precision by up to 35%. The adoption of AI-driven analytics allows predictive irrigation scheduling, reducing water wastage and increasing crop yields. Expanding use of satellite imagery and remote sensing technologies further enhances farm-level decision-making. Emerging markets are witnessing increasing investments in agri-tech startups, fostering innovation in automated irrigation solutions. Additionally, the growing demand for organic and high-value crops is encouraging farmers to adopt microirrigation systems for better quality control and resource optimization, opening new revenue streams across the agricultural value chain.

Infrastructure gaps and technical limitations pose significant challenges to the microirrigation systems market. In many rural regions, inadequate water storage facilities and inconsistent power supply hinder the efficient operation of irrigation systems. Lack of standardized installation practices leads to uneven water distribution and reduced system efficiency. Furthermore, limited availability of skilled technicians for installation and maintenance creates operational inefficiencies. Data integration challenges also persist, as many farms lack the digital infrastructure required to fully leverage smart irrigation technologies. Environmental factors such as clogging due to poor water quality and sediment buildup further reduce system lifespan and performance. Addressing these challenges requires coordinated efforts in infrastructure development, farmer education, and technological standardization.

• Rapid adoption of IoT-enabled smart irrigation systems improving efficiency by 35%: The integration of IoT sensors and connected irrigation platforms is transforming traditional farming operations into data-driven ecosystems. Over 30% of large-scale farms globally have deployed smart irrigation controllers, enabling real-time monitoring of soil moisture, weather conditions, and crop health. These systems reduce water wastage by up to 40% and improve irrigation precision by nearly 35%, significantly enhancing crop productivity. In developed agricultural markets, nearly 55% of commercial farms are transitioning toward automated irrigation solutions, driven by labor optimization and digital agriculture initiatives.

• Expansion of drip irrigation systems covering over 60% of microirrigation installations: Drip irrigation continues to dominate the microirrigation systems market, accounting for more than 60% of total installations globally due to its high efficiency and targeted water delivery capabilities. Adoption has increased by approximately 25% in water-stressed regions, where precision irrigation is essential for maintaining crop yields. In horticulture, drip systems have improved water-use efficiency by up to 50% and increased yield quality by 20–30%. Governments are actively supporting this trend through subsidy programs covering up to 50% of installation costs, further accelerating adoption across small and medium-sized farms.

• Growing use of solar-powered irrigation systems reducing energy costs by 30%: Renewable energy integration is emerging as a key trend, with solar-powered microirrigation systems gaining traction in off-grid and rural agricultural areas. Around 20% of new irrigation installations in developing economies now incorporate solar pumping solutions, reducing dependence on conventional energy sources. These systems lower operational costs by approximately 30% and provide consistent water supply even in regions with unreliable electricity infrastructure. Solar-driven irrigation is particularly impactful in regions with high solar irradiance, where adoption rates are increasing by over 15% annually.

• Increasing demand for precision fertigation systems improving nutrient efficiency by 25%: Fertigation technologies, which combine irrigation with nutrient delivery, are gaining widespread adoption among commercial farmers. Approximately 40% of advanced microirrigation systems now include fertigation capabilities, allowing precise control of nutrient application. This approach reduces fertilizer usage by 20–25% while enhancing nutrient uptake efficiency and crop yields. In greenhouse and high-value crop cultivation, fertigation systems have improved productivity by nearly 30%, making them a critical component of modern precision agriculture strategies focused on sustainability and resource optimization.

The microirrigation systems market is segmented based on type, application, and end-user, each contributing uniquely to overall market expansion. By type, drip irrigation systems dominate due to their precision and water-saving capabilities, followed by sprinkler systems and other niche technologies. In terms of application, agriculture remains the primary segment, accounting for a significant share due to increasing demand for efficient irrigation in crop production, while horticulture and greenhouse farming are emerging as high-growth areas. From an end-user perspective, small and medium-scale farmers represent a substantial portion of adoption, supported by government subsidies, while large commercial farms and agribusiness enterprises are rapidly integrating advanced irrigation technologies. Regional segmentation indicates strong adoption in Asia-Pacific due to large agricultural bases, while North America and Europe exhibit higher penetration of technologically advanced systems, reflecting a shift toward precision agriculture practices.

Drip irrigation systems represent the leading segment in the microirrigation systems market, accounting for approximately 62% of total adoption due to their superior efficiency in water delivery and ability to minimize evaporation losses. In comparison, sprinkler irrigation systems hold around 28% share, primarily used for field crops and large-scale farming, while other systems such as micro-sprayers and bubblers collectively contribute nearly 10% to the market. Drip irrigation is particularly favored in horticulture and high-value crop cultivation, where it enhances water-use efficiency by up to 50% and improves yield consistency.

Sprinkler irrigation is currently the fastest-growing type, expanding at an estimated CAGR of around 14% due to its versatility across different crop types and ease of installation in varied terrains. Increasing adoption in large-scale grain and cereal production is a key growth driver. Meanwhile, niche systems such as subsurface drip irrigation are gaining traction for their ability to reduce water losses by up to 20% compared to surface systems, although their adoption remains limited due to higher installation complexity.

Agriculture remains the dominant application segment, accounting for nearly 68% of total microirrigation system usage due to the widespread need for efficient irrigation in staple crop production. Horticulture follows with approximately 20% share, driven by the increasing demand for fruits, vegetables, and high-value crops requiring precise water management. Greenhouse cultivation accounts for about 12%, benefiting from controlled irrigation environments that enhance productivity and resource efficiency.

Greenhouse farming is the fastest-growing application segment, expanding at an estimated CAGR of around 16%, supported by rising adoption of controlled environment agriculture and urban farming practices. Microirrigation systems in greenhouses improve water efficiency by up to 40% and increase crop yields by nearly 30%, making them essential for high-density farming systems. Other applications, including landscaping and turf irrigation, collectively contribute around 10% of the market, with increasing adoption in urban infrastructure projects and commercial landscaping.

Small and medium-scale farmers represent the leading end-user segment, accounting for approximately 55% of microirrigation system adoption due to extensive government support and subsidy programs. Large commercial farms hold around 30% share, leveraging advanced irrigation technologies to optimize productivity and reduce operational costs. Institutional users, including agricultural cooperatives and research farms, contribute the remaining 15%, focusing on demonstration projects and technology validation.

Large commercial farms are the fastest-growing end-user segment, expanding at an estimated CAGR of around 15%, driven by increasing investments in precision agriculture and automation technologies. These farms are adopting IoT-enabled irrigation systems at a rate exceeding 35%, enabling real-time monitoring and data-driven decision-making. Other end-users, such as greenhouse operators and landscaping companies, collectively account for nearly 20% of market demand, with adoption rates increasing steadily due to the need for efficient water management solutions.

Region Asia-Pacific accounted for the largest market share at 48% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 18.5% between 2026 and 2033.

Asia-Pacific’s dominance is supported by over 20 million hectares under microirrigation, with India and China contributing more than 65% of the regional installations. North America, with more than 55% of large-scale farms using precision irrigation technologies, is witnessing rapid digital transformation. Europe holds approximately 22% of the market, driven by sustainability mandates and advanced agricultural practices across Germany, France, and Spain. South America accounts for nearly 10%, with Brazil alone contributing over 60% of regional demand due to extensive soybean and sugarcane cultivation. The Middle East & Africa region represents around 8%, with high adoption in arid regions where over 70% of irrigation projects incorporate water-efficient technologies. Globally, more than 45 million hectares are now equipped with microirrigation systems, reflecting increasing adoption driven by water scarcity, technological innovation, and policy support.

How are precision agriculture technologies transforming irrigation efficiency across advanced farming ecosystems?

North America accounts for approximately 20% of the global microirrigation systems market, with the United States representing nearly 75% of regional demand. The region’s agricultural sector is highly mechanized, with over 60% of farms adopting advanced irrigation technologies. Key industries driving demand include large-scale crop farming, horticulture, and greenhouse cultivation, where water efficiency improvements of up to 40% are achieved through microirrigation. Regulatory support such as water conservation policies and federal funding programs has accelerated adoption, with incentives covering up to 30% of system installation costs in certain states. Technological advancements include widespread deployment of AI-driven irrigation controllers and satellite-based monitoring systems. A leading regional player has introduced cloud-integrated irrigation platforms, improving farm-level water management efficiency by 25%. Consumer behavior in the region reflects high adoption of data-driven agriculture, with enterprises prioritizing automation and sustainability to optimize operational performance.

What factors are driving sustainable irrigation adoption across highly regulated agricultural systems?

Europe holds around 22% of the global microirrigation systems market, with key countries such as Germany, France, Italy, and Spain leading adoption. The region benefits from strong regulatory frameworks focused on water conservation and environmental sustainability, with policies mandating efficient irrigation practices across agricultural operations. Approximately 50% of farms in Southern Europe have adopted microirrigation systems, particularly in water-scarce regions. Emerging technologies such as automated fertigation and AI-based irrigation scheduling are gaining traction, improving water-use efficiency by up to 35%. A regional manufacturer has developed advanced pressure-compensated drip systems, enhancing irrigation uniformity by 20% across varied terrains. Consumer behavior is heavily influenced by regulatory compliance, with farmers prioritizing sustainable irrigation solutions to meet environmental standards and reduce water consumption by at least 25% in agricultural activities.

Why is large-scale agricultural expansion accelerating precision irrigation adoption across developing economies?

Asia-Pacific represents the largest market by volume, with over 48% share and more than 25 million hectares under microirrigation systems. Key countries including India, China, and Japan drive regional demand, with India alone contributing over 15 million hectares of installations. Rapid expansion of agricultural infrastructure and increasing government investments exceeding USD 2 billion annually are supporting widespread adoption. The region is also emerging as a manufacturing hub, producing over 60% of global microirrigation components. Technological trends include the integration of mobile-based irrigation control systems and low-cost sensor technologies, improving accessibility for smallholder farmers. A prominent regional company has deployed smart irrigation solutions across 1 million hectares, achieving water savings of nearly 35%. Consumer behavior in the region is characterized by strong adoption among small and medium-scale farmers, driven by subsidies and increasing awareness of water conservation practices.

How is agricultural intensification shaping efficient irrigation adoption in high-yield farming regions?

South America accounts for approximately 10% of the global microirrigation systems market, with Brazil and Argentina as key contributors. Brazil alone represents nearly 60% of regional demand, driven by large-scale cultivation of crops such as soybeans, sugarcane, and coffee. Infrastructure improvements, including expanded irrigation networks covering over 5 million hectares, are supporting market growth. Government incentives promoting sustainable agriculture and export-oriented farming have increased adoption rates by nearly 20% in recent years. Technological advancements include the use of automated sprinkler systems and remote monitoring solutions, improving irrigation efficiency by up to 30%. A regional irrigation provider has implemented large-scale drip systems across commercial farms, enhancing yield productivity by 25%. Consumer behavior reflects a strong focus on maximizing crop output and optimizing water usage, particularly in export-driven agricultural sectors.

What role do water scarcity solutions play in advancing efficient irrigation technologies across arid regions?

The Middle East & Africa region holds approximately 8% of the global microirrigation systems market, with significant adoption in countries such as the UAE, Israel, and South Africa. Over 70% of irrigation projects in arid regions utilize microirrigation systems due to severe water scarcity and limited freshwater resources. Government initiatives promoting water conservation and sustainable agriculture have increased adoption rates by nearly 25% over the past few years. Technological modernization includes the deployment of desalination-integrated irrigation systems and AI-driven water management platforms, improving efficiency by up to 40%. A regional player has introduced advanced drip irrigation solutions tailored for desert agriculture, enabling crop cultivation with 50% less water usage. Consumer behavior is driven by necessity, with farmers and agribusinesses prioritizing highly efficient irrigation systems to sustain agricultural productivity under extreme climatic conditions.

India – 32% market share: Microirrigation Systems market growth driven by large agricultural base, extensive government subsidies, and over 15 million hectares under microirrigation.

China – 21% market share: Microirrigation Systems market expansion supported by strong manufacturing capacity and rapid adoption of precision irrigation across large-scale farming operations.

The microirrigation systems market is moderately fragmented, with over 150 active global and regional competitors operating across different segments of the value chain. The top five companies collectively account for approximately 45% of the total market share, indicating a competitive yet partially consolidated landscape. Market leaders focus on technological innovation, product diversification, and geographic expansion to strengthen their market position. Strategic initiatives such as mergers and acquisitions have increased by nearly 20% in recent years, enabling companies to enhance their product portfolios and expand into emerging markets.

Product innovation remains a key competitive factor, with over 30% of companies investing in research and development to introduce advanced irrigation solutions such as IoT-enabled systems, automated fertigation units, and AI-driven analytics platforms. Partnerships between irrigation companies and agri-tech firms have grown by approximately 25%, facilitating the integration of digital technologies into irrigation systems. Additionally, companies are increasingly focusing on sustainable solutions, with more than 40% of new product launches incorporating water-saving and energy-efficient features.

Regional players continue to compete by offering cost-effective solutions tailored to local agricultural needs, while global players leverage advanced technologies and strong distribution networks to maintain market leadership. The competitive environment is further shaped by increasing demand for precision agriculture, driving continuous innovation and strategic collaboration across the industry.

Jain Irrigation Systems Ltd.

Netafim Ltd.

The Toro Company

Rain Bird Corporation

Hunter Industries

Lindsay Corporation

Valmont Industries, Inc.

Rivulis Irrigation Ltd.

T-L Irrigation Co.

Nelson Irrigation Corporation

Technological advancements are playing a pivotal role in transforming the microirrigation systems market into a data-driven and highly efficient agricultural ecosystem. One of the most significant innovations is the integration of Internet of Things (IoT) sensors, which are now deployed in over 35% of advanced irrigation systems globally. These sensors continuously monitor soil moisture, temperature, and humidity levels, enabling real-time irrigation adjustments that improve water-use efficiency by up to 40%. Additionally, cloud-based irrigation platforms allow remote system control, with over 50% of large-scale farms adopting centralized dashboards for precision irrigation management.

Artificial intelligence and machine learning technologies are further enhancing irrigation accuracy. AI-powered predictive analytics can optimize irrigation schedules based on weather forecasts and crop requirements, reducing water consumption by nearly 25% while improving crop yields by up to 20%. Satellite imaging and geospatial analytics are also gaining traction, with more than 30% of commercial agricultural operations using remote sensing technologies to assess crop health and irrigation needs across large land areas exceeding 1,000 hectares.

Automation technologies such as smart valves, automated fertigation units, and pressure-regulated drip lines are improving system performance and reducing manual intervention by approximately 30%. Solar-powered irrigation systems are increasingly integrated with microirrigation setups, particularly in off-grid regions, lowering energy costs by up to 35% and ensuring uninterrupted water supply.

Emerging technologies such as blockchain-based water management systems and digital twin models for irrigation planning are beginning to gain attention among large agribusinesses. These innovations enable transparent resource allocation and predictive maintenance, reducing system downtime by nearly 20%. Collectively, these technologies are redefining irrigation efficiency, sustainability, and scalability, making microirrigation systems a cornerstone of modern precision agriculture.

• In March 2025, Netafim Ltd. expanded its precision irrigation portfolio by launching an advanced digital farming platform integrating AI-based irrigation scheduling and real-time soil monitoring, enabling up to 30% water savings and improved crop yield efficiency. Source: www.netafim.com

• In November 2024, The Toro Company introduced a next-generation automated irrigation controller equipped with IoT connectivity and cloud-based analytics, allowing commercial farms to reduce water usage by approximately 25% while improving operational efficiency. Source: www.toro.com

• In August 2024, Jain Irrigation Systems Ltd. announced the deployment of large-scale microirrigation projects covering over 200,000 hectares, incorporating solar-powered drip systems to enhance water efficiency by 35% and reduce energy consumption in rural farming regions. Source: www.jains.com

• In January 2025, Rivulis Irrigation Ltd. launched an upgraded drip irrigation solution featuring pressure-compensating emitters and advanced clog-resistant technology, improving irrigation uniformity by 20% and extending system lifespan in high-sediment water conditions. Source: www.rivulis.com

The Microirrigation Systems Market Report provides a comprehensive evaluation of key industry segments, technological advancements, and regional adoption patterns shaping the global irrigation landscape. The report covers a wide range of product types, including drip irrigation systems, sprinkler irrigation systems, subsurface irrigation technologies, and advanced fertigation solutions, collectively addressing over 90% of precision irrigation applications. It further analyzes application areas such as agriculture, horticulture, greenhouse cultivation, and landscaping, with agriculture alone accounting for nearly 70% of total system usage.

Geographically, the report spans major regions including Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, representing over 95% of global microirrigation deployments. It highlights country-level insights for key agricultural economies, focusing on infrastructure development, irrigation coverage exceeding 45 million hectares globally, and regional consumption patterns. The scope also includes analysis of end-user segments such as small and medium-scale farmers, large commercial farms, agribusiness enterprises, and institutional users, providing insights into adoption rates and technology penetration levels.

In addition to traditional irrigation systems, the report incorporates emerging technologies such as IoT-enabled irrigation platforms, AI-driven analytics, and solar-powered irrigation solutions, which are currently integrated into more than 30% of modern farming operations. It also examines regulatory frameworks, sustainability initiatives, and water conservation policies influencing market expansion. The report is designed to support strategic decision-making by offering a holistic view of market dynamics, innovation trends, competitive landscape, and evolving agricultural practices across global markets.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

17.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Jain Irrigation Systems Ltd., Netafim Ltd., The Toro Company, Rain Bird Corporation, Hunter Industries, Lindsay Corporation, Valmont Industries, Inc., Rivulis Irrigation Ltd., T-L Irrigation Co., Nelson Irrigation Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |