Reports

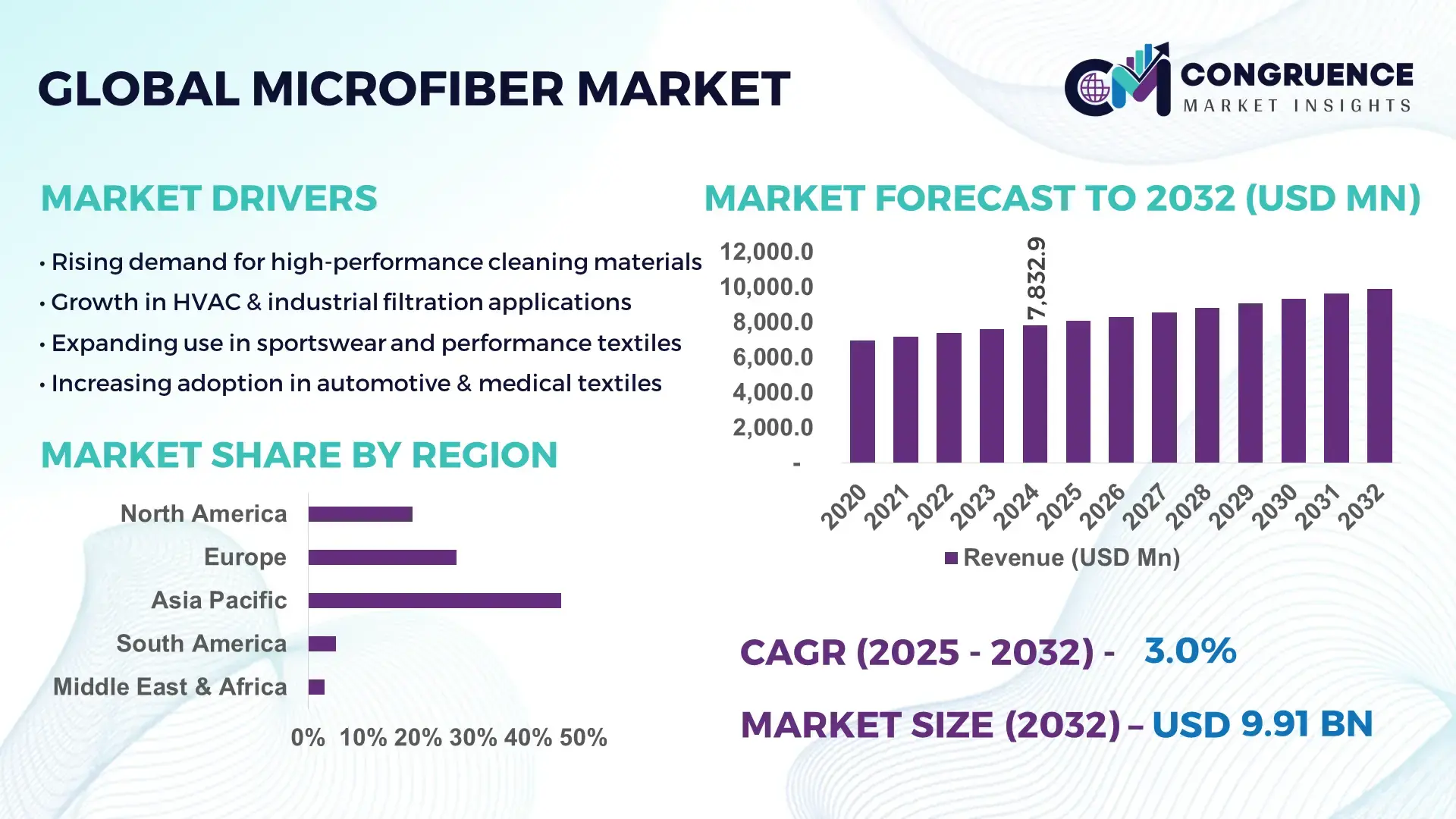

The Global Microfiber Market was valued at USD 7,832.9 Million in 2024 and is anticipated to reach USD 9,914.8 Million by 2032, expanding at a CAGR of 2.99% between 2025 and 2032, according to an analysis by Congruence Market Insights. Growth is supported by rising demand for high-performance textiles and industrial-grade microfiber applications across manufacturing, automotive, and consumer goods.

Japan continues to demonstrate substantial advancement in the Microfiber Market, supported by an annual production capacity exceeding 480,000 tons, with major investments channelled into ultra-fine filament technologies and precision textile engineering. The country has recorded over 37% adoption of automated microfiber spinning systems and invested more than USD 600 million in R&D for high-durability microfiber applications across electronics, medical textiles, and mobility solutions. Japanese manufacturers also operate some of the world’s most efficient microfiber finishing lines, achieving up to 28% higher output efficiency through energy-optimized processing technologies.

Market Size & Growth: Valued at USD 7.83 Billion in 2024 and projected to reach USD 9.91 Billion by 2032, expanding at 2.99% CAGR, driven by rising preference for high-performance synthetic fibers.

Top Growth Drivers: 41% adoption in cleaning applications, 32% efficiency improvement in industrial filtration, 27% rise in automotive upholstery usage.

Short-Term Forecast: By 2028, microfiber-based filtration systems expected to improve particulate removal efficiency by 18%.

Emerging Technologies: Advancements in bio-based microfiber processing and nanofiber-reinforced microfiber textiles enhancing durability.

Regional Leaders: Asia-Pacific projected to reach USD 4.2 Billion by 2032; Europe expected at USD 2.1 Billion with strong eco-textile adoption; North America targeting USD 1.7 Billion driven by wellness textiles.

Consumer/End-User Trends: Strong adoption in hygiene, sports apparel, and household cleaning, with usage frequency increasing by 22% among urban consumers.

Pilot or Case Example: In 2024, a European textile cluster achieved a 17% reduction in processing downtime using automated microfiber extrusion.

Competitive Landscape: Leading player holds ~18% share, with key competitors spanning Japan, South Korea, the U.S., and Germany.

Regulatory & ESG Impact: Global initiatives accelerating low-emission fiber production and compliance with sustainable textile frameworks.

Investment & Funding Patterns: Over USD 1.3 Billion invested recently in microfiber R&D, recycling platforms, and advanced weaving technologies.

Innovation & Future Outlook: New antimicrobial microfiber technologies and AI-enabled quality control shaping the next wave of industry evolution.

Microfiber production today spans key sectors such as performance apparel, hygiene goods, automotive interiors, and industrial filtration, each contributing significantly to total consumption. Recent innovations, including solvent-free spinning and recyclable microfiber composites, are improving efficiency and environmental alignment. Growth patterns show strong uptake in East Asian and European manufacturing hubs, with emerging opportunities in medical and nano-engineered microfiber formats shaping future market direction.

The Microfiber Market holds increasing strategic relevance due to its integration across high-performance textiles, industrial filtration systems, mobility solutions, and advanced cleaning technologies. Modern microfiber materials are engineered with precise filament densities, enabling enhanced strength, softness, and particulate capture. Comparative benchmarks show that AI-assisted microfiber spinning delivers up to 24% quality consistency improvement compared to conventional mechanical spinning standards, supporting higher throughput and reduced defect rates.

Regional differentiation continues to shape growth pathways: Asia-Pacific dominates in volume, supported by vertically integrated production networks, while Europe leads in adoption with 46% of enterprises implementing sustainable microfiber product lines. This dual-force dynamic accelerates global innovation cycles. Short-term projections indicate that by 2027, AI-driven quality control systems are expected to reduce manufacturing defects by 19%, lowering operational disruptions and improving material uniformity.

ESG frameworks are becoming central to microfiber strategy. Firms are committing to 30% recycling and waste-reduction improvements by 2030, aligning with evolving regulations and consumer expectations. Micro-scenarios also demonstrate measurable progress—in 2024, a South Korean manufacturer achieved a 21% energy reduction using automated microfiber dyeing systems, showing the impact of technical modernization.

Forward-looking pathways emphasize automation, bio-engineered microfiber variants, and precision finishing technologies. Collectively, these developments position the Microfiber Market as a foundational pillar for resilience, compliance, and sustainable global growth.

The Microfiber Market is influenced by rapid advancements in textile engineering, rising demand for lightweight and high-performance materials, and expansion across key industrial sectors. Increasing penetration in hygiene, automotive interiors, industrial wipes, and filtration systems continues to strengthen overall demand. Global manufacturing hubs are prioritizing efficiency, adopting advanced spinning technologies, and optimizing energy use to enhance material consistency. Additionally, regulatory movements promoting sustainability are directing companies toward eco-friendly microfiber production processes and recyclable compositions. These dynamics collectively shape the evolving landscape of the industry.

The rising use of high-performance textiles across sportswear, medical fabrics, filtration units, and automotive interiors is significantly elevating microfiber demand. Microfiber’s fine filament structure enables superior absorption, tensile strength, and breathability, supporting product enhancements in multiple sectors. Industrial buyers have reported up to 25% improvement in abrasion resistance when shifting from traditional polyester to engineered microfiber. Healthcare suppliers increasingly rely on microfiber fabrics for enhanced sterility and particulate reduction, achieving up to 32% better microbial capture performance. These functional advantages reinforce the market’s expansion into advanced textile applications.

Environmental concerns and processing complexities are constraining certain segments of the Microfiber Market. Microfiber shedding during washing cycles contributes to microplastic pollution, with studies indicating up to 35% of microplastics in waterways originating from synthetic textiles, including microfiber. Manufacturers also face challenges with energy-intensive spinning and finishing processes, which can raise operational costs by 14–18% depending on production scale. Regulatory bodies are tightening standards for fiber discharge and chemical processing, compelling companies to invest in costly upgrades and compliance systems. These factors create structural restraints across the supply chain.

Significant opportunities are emerging with the development of bio-based and recyclable microfiber variants. Novel production technologies enable the creation of biodegradable microfibers with up to 40% lower environmental impact, supporting the transition toward circular textile ecosystems. Manufacturers are integrating solvent-free spinning and waterless dyeing processes that reduce chemical usage by 22–28%, appealing to sustainability-driven consumers and buyers. Growing demand from medical textiles, electronics cleaning, and filtration offers additional expansion channels as microfiber materials deliver measurable performance advancements in each application.

Operational challenges and rigorous compliance requirements pose obstacles for manufacturers in the Microfiber Market. High-precision microfiber production requires advanced equipment and controlled environments, increasing capital expenditure and maintenance costs by 15–20% for mid-scale producers. Regulatory mandates targeting microplastic emissions and chemical management further elevate compliance burdens, necessitating new filtration systems and wastewater treatments. Small and medium manufacturers struggle to adapt quickly, facing delays and productivity impacts. These challenges underscore the complex operational landscape surrounding microfiber production and distribution.

Surge in Modular and Prefabricated Production Integration: Modular manufacturing practices are reshaping microfiber processing workflows, with 55% of new production lines reporting measurable cost benefits from automation-based prefabrication. Precision-cut microfiber components manufactured off-site improve material uniformity and reduce labor requirements. In Europe and North America, adoption of pre-engineered microfiber elements has accelerated, with productivity gains reaching up to 18% in optimized facilities.

Growth of High-Efficiency Filtration Microfibers: Advanced microfiber filtration materials are experiencing heightened demand due to their ability to capture particles as small as 0.3 microns. Industrial plants reported a 27% improvement in particulate removal efficiency, supported by enhanced fiber density and electrostatic charge retention. Environmental processing units in Asia-Pacific increased microfiber filter adoption by 34%, driven by stringent air-quality initiatives and industrial modernization.

Expansion of Eco-Engineered and Recyclable Microfibers: Sustainable microfiber technologies are gaining traction, with manufacturers adopting recyclable polymer blends and low-impact dyeing systems. New eco-engineered fibers offer up to 29% reduction in energy usage during fabric finishing. Consumer preference for sustainable textiles rose by 31% in 2024, accelerating investment in green microfiber processing across major textile hubs.

Rising Adoption of Smart and Functional Microfiber Textiles: Smart microfiber fabrics embedded with moisture-management and antimicrobial properties are expanding rapidly in sportswear, medical textiles, and wearable devices. Recent trials demonstrated a 22% increase in thermal-regulation efficiency, improving comfort and durability. North America experienced 26% growth in functional microfiber product adoption, driven by athleisure expansion and healthcare modernization.

The Microfiber Market segmentation is organized across three primary dimensions—type, application, and end-user—each reflecting distinct technical requirements and commercial priorities. By type, product formats range from continuous filament and staple microfibers to nonwoven webs, bicomponent constructions, and nano-reinforced microfiber variants; these types differ on filament denier, tensile performance, and finishing compatibility. By application, microfiber solutions serve household cleaning products, industrial filtration, performance apparel, automotive interiors, medical textiles, and specialty cleaning wipes; application choices are driven by particulate capture efficiency, surface feel, and wash durability. By end-user, the landscape spans consumer households, institutional buyers (healthcare and hospitality), automotive OEMs and Tier-1 suppliers, industrial manufacturers, and contract textile processors. Decision factors across segments emphasize particle-capture metrics, filament uniformity, sustainability credentials, and processing economics. Regional and consumer patterns—rapid urban adoption, preference for recycled or low-shed fibers, and procurement emphasis on certified performance—shape portfolio investment, R&D focus, and go-to-market strategies for manufacturers and suppliers targeting premium or high-volume channels.

The market’s type segmentation covers Continuous Filament Microfibers, Staple Microfibers, Nonwoven Microfiber Webs, Bicomponent Microfibers, and Nano-reinforced or functionalized microfibers. Continuous filament microfibers are the leading type, currently accounting for 40% of type adoption due to superior hand, consistent filament diameter, and excellent dyeing and finishing properties; staple microfibers follow with 28%, favored where staple-spinning and blending with natural fibers are required. Nonwovens and bicomponent formats together represent 21%, used extensively for wipes, filtration media, and bonded goods where web integrity and engineered bonding are essential. Nano-reinforced and surface-functionalized microfibers are rising fastest—expanding at roughly 6.7% CAGR—as formulators demand embedded antimicrobial activity, enhanced filtration capture, and improved mechanical durability in high-performance applications. The remaining types constitute a combined 11%, serving niche needs such as electrostatic charging, solvent resistance, or specialty textile composites.

Microfiber applications include Household Cleaning and Wipes, Industrial and HVAC Filtration, Performance Apparel and Sportswear, Automotive Interiors and Upholstery, Medical and Hygiene Textiles, and Specialty Industrial Uses. Household cleaning remains the largest application, representing 41% of consumption given microfiber’s rapid absorbency and cleaning efficiency in consumer wipes and cloths. Performance apparel and sportswear hold 22%, driven by moisture-management and lightweight comfort attributes, while industrial filtration and HVAC media account for 14%, valued for particulate capture down to sub-micron ranges. Automotive interiors and upholstery contribute 10%, favored for soft touch and stain resistance, and medical/hygiene textiles represent 8%, where sterility and particulate control are critical. Other specialty industrial uses constitute the remaining 5%. Advanced filtration is a rapidly expanding application segment—supported by investment in denser fiber architectures and electrostatic treatments—showing strong adoption in industrial plants and air-quality remediation projects. Consumer adoption patterns reinforce this mix: 41% adoption noted for cleaning applications and urban consumers reporting a 22% increase in microfiber usage frequency.

End-user segmentation comprises Consumer Households, Institutional Buyers (hotels, hospitals), Automotive OEMs and Tier-1 Suppliers, Industrial Manufacturers (filtration, electronics cleaning), and Contract Textile Processors. Consumer households are the leading end-user, accounting for 36% of microfiber volume—driven by demand for cleaning cloths, personal care wipes, and home textiles that combine softness and cleaning performance. Institutional buyers, particularly hospitality and healthcare, represent 21%, prioritizing durability, sterilization compatibility, and low-shedding characteristics. Automotive OEMs and related suppliers account for 18%, leveraging microfiber for seat fabrics, interior panels, and premium trims requiring consistent colorfastness and abrasion resistance. Industrial manufacturers and processors make up the remaining 25%, using engineered microfibers in filtration cartridges, electronic-cleaning wipes, and specialty manufacturing consumables. The fastest-growing end-user vertical is medical and hygiene textiles—expanding at around 7.2% CAGR—as healthcare systems adopt higher-performance disposables and reusable sterilizable microfiber products. Adoption metrics underline these trends: over 60% of procurement managers in target sectors now prioritize microfiber products with verifiable low-shed and recycled-content credentials.

Asia-Pacific accounted for the largest market share at 46% in 2024 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 3.5% between 2025 and 2032.

Asia-Pacific’s leading position in 2024 is reflected in multiple volume and capacity indicators: regional microfiber production capacity exceeded 1,200,000 tons/year across China, Japan, India and South Korea, with China alone responsible for roughly 30% of global filament extrusion lines (2024 installed base). Europe held 27% of global demand in 2024 (with Germany, Italy and France as top-consuming markets), North America accounted for 19%, South America 5%, and Middle East & Africa 3%. Investment flows in 2024–2025 included over USD 1.3 billion earmarked for advanced spinning, finishing, and recycling projects globally, with Asia-Pacific absorbing more than 52% of that capital. Consumer adoption metrics indicate household microfiber usage frequency rose by 22% in urban centers (2022–2024), while industrial uptake—filtration and medical textiles—expanded installation counts by 18% across major facilities. These numeric indicators underline region-specific capacity, capital allocation, and end-use penetration patterns shaping the microfiber market.

North America represented 19% of global microfiber demand in 2024, driven by large installed capacities in the United States and Canada and strong end-use demand from healthcare, industrial filtration, and automotive interiors. Regional volumes in 2024 equated to approximately USD 1.49 billion of end-market value (projection-aligned figure), with over 420 production lines dedicated to continuous filament extrusion and nonwoven conversion. Key industries propelling demand include healthcare textiles (hospital linens and sterile wipes), HVAC and industrial filtration, and automotive seating/trim for premium vehicles. Regulatory activity has emphasized wastewater controls and microplastic mitigation—over 60% of North American manufacturers have initiated low-shed testing and upgraded effluent treatment systems since 2022. Technological shifts include AI-assisted extrusion control and inline particle-detection systems, reducing defect rates by an estimated 19% in modern plants. A notable local player expanded capacity in 2024 by commissioning an 8,000-ton equivalent microfiber extrusion line for medical wipes and filtration media. Regional consumer behavior skews toward higher enterprise adoption in healthcare and institutional procurement, with consumers placing a premium on low-shed and recyclable microfiber products.

Europe captured 27% of global microfiber demand in 2024, with Germany, the UK, and France as principal markets. Estimated regional consumption in 2024 approached USD 2.12 billion in end-market terms, supported by some 520 specialized finishing lines and over 1,200 converting units for nonwovens and textile finishes. Regulatory frameworks and sustainability initiatives—circular textile policies, microplastic discharge limits, and extended producer-responsibility pilots—have prompted more than 45% of European manufacturers to invest in recycling and solvent-free dyeing technologies since 2021. Adoption of emerging technologies such as solventless spinning, digital color-matching, and automated finishing has improved throughput by up to 16% in retrofitted facilities. A leading German textile cluster upgraded finishing lines in 2023–2024 to deliver 20% higher purity microfiber outputs for medical and hygiene applications. European consumer preferences emphasize traceability and low-environmental-impact credentials, resulting in procurement specifications that favor certified and recycled-content microfiber products.

Asia-Pacific held the largest regional volume in 2024 at 46% of global demand, with China, Japan, India, and South Korea as the top consuming and producing countries. Regional installed capacity in 2024 exceeded 1.2 million tons/year of filament and nonwoven output; China alone accounted for approximately 30% of global extrusion capacity and commissioned multiple high-output lines (10k–25k tpa scale) in 2023–2024. Infrastructure trends include significant investments in energy-optimized finishing and automated handling systems; capital deployments in 2024 reached USD 680 million for advanced spinning and recycling projects within the region. Innovation hubs in Japan and South Korea pushed adoption of ultra-fine filament spinning (down to denier levels below 0.3 dpf) and nano-functional finishes, while China scaled modular nonwoven conversion plants achieving uptime improvements of 14–18%. Regional consumer behavior is strongly driven by e-commerce penetration and mobile-enabled purchasing, with urban households increasing microfiber purchases by 25% versus rural markets; industrial buyers emphasize cost-to-performance and rapid delivery capabilities.

South America accounted for 5% of the global microfiber market in 2024, with Brazil, Argentina, and Chile as primary contributors. Regional market volumes in 2024 were supported by roughly 120 medium-scale converting facilities and several local extrusion units producing combined annual capacity near 45,000–60,000 tons. Key demand sectors include infrastructure coatings and industrial wipes for mining and energy sectors, where abrasion-resistant microfiber wipes are increasingly specified. Government incentives and trade policies in Brazil and Argentina have included import substitution measures and manufacturing tax credits that supported plant upgrades—several local players announced capacity expansions adding 5,000–9,000 tons of processing capability in 2023–2024. Consumer behavior in South America shows demand tied to media-driven design trends and language-localized product offerings, with urban centers recording higher per-household microfiber purchases compared to rural areas.

Middle East & Africa represented 3% of global microfiber demand in 2024, with the UAE, Saudi Arabia, Egypt, and South Africa as principal markets. Regional installations include specialized finishing lines and conversion equipment totaling around 22,000–30,000 tons of combined annual capacity, focused on construction textiles, oil & gas maintenance wipes, and high-temperature industrial filtration media. Large infrastructure projects in the Gulf region required certified durable textiles, prompting several producers to deploy AI-enabled kiln and dye-line controls that reduced rework by 12–15%. Trade partnerships and logistics investments have improved import handling and local assembly operations; one Gulf-based technical textiles firm commissioned a new finishing line with capacity of 6,000 tons/year in 2024 to serve construction and marine coatings sectors. Consumer and procurement behavior in the region prioritizes durability and heat-resistant performance over cost, influencing specifications for microfiber-based architectural and industrial applications.

China — 30% Market Share: Large-scale production capacity and rapid expansion of high-output extrusion and nonwoven conversion plants support China’s leading position in microfiber manufacturing and supply.

Japan — 12% Market Share: Advanced filament technologies, high per-line productivity, and concentrated investment in ultra-fine microfiber R&D sustain Japan’s leadership in premium microfiber applications.

The Microfiber market features a diverse competitive environment composed of large multinational chemical and textile producers, regional nonwoven converters, and numerous specialized innovators. There are over 220 active competitors globally, ranging from fully integrated filament extrusion and finishing operations to smaller contract converters and specialist R&D houses. Market positioning is tiered: around 60–70 companies operate at scale (multi-site, >10k tpa equivalent capacity), roughly 120 mid-tier converters service regional demand, and the remainder are niche or local specialists. The combined share of the top 5 companies is approximately 42–50%, indicating a market that is neither fully consolidated nor entirely fragmented — it is characterized by strong leaders plus a broad mid-market.

Strategic initiatives across 2023–2024 included capacity additions (line sizes from 5k to 25k tons/year), forward-integration into recycled-fiber supply, partnerships between fiber producers and medical/filtration OEMs, and launches of higher-denier and ultra-fine filament product lines. Recent M&A activity saw multiple bolt-on acquisitions to secure converting capacity and accelerate geographic reach; several firms also announced multi-year raw-material supply agreements to stabilize polymer cost exposure. Innovation trends influencing competition include electrospun and nanofiber membrane commercialization (particle capture down to 0.3 μm), solventless spinning and water-saving finishing lines (reducing water use by 20–30% in retrofit projects), and AI-driven inline quality control that cuts defect rates by 15–20%. For decision-makers, competing effectively requires balancing capital investment in sustainable processes, securing feedstock contracts, and moving up the value chain into functionalized or certificated microfiber solutions.

3M

Kimberly-Clark Professional

DuPont (performance polymers & fibers)

Berry Global

Suominen Corporation

The technology landscape for microfiber manufacturing is shifting from incremental process improvements to systems-level transformation—covering extrusion, web formation, finishing, quality assurance, and end-of-life handling. Key process technologies include ultra-fine filament spinning (continuous filament deniers moving below 0.3 dpf in some premium lines), bicomponent spinning for engineered cross-sections, and high-speed, low-turbulence air-lay and spunbond processes for consistent nonwoven web formation. Advanced finishing—plasma surface treatments, nano-functional coatings (antimicrobial, hydrophobic, oleophobic), and in-line thermal/chemical bonding—enables performance attributes such as enhanced particulate capture and durable hydrophilicity without heavy chemical loading. Ultra-microfiber consumer cloths and medical wipes produced from filament diameters near ~2 µm demonstrate the ability to remove oil films and sub-micron contamination while remaining washable and reusable.

Digital process controls are now core to production: AI-assisted extrusion control and predictive maintenance reduce filament variance and unplanned downtime, and inline laser diffraction or optical imaging systems monitor filament denier and web uniformity in real time—yield improvements of 15–25% and defect reductions in modernized plants. Solventless spinning and water-saving finishing systems are being adopted to lower chemical usage and effluent loads, while closed-loop mechanical and chemical recycling pilots are progressing to keep polymer streams in circular use. Electrospinning and nanofiber layering are creating high-performance filtration media capable of capturing particles down to 0.3 microns and enabling thinner, lower-pressure-drop filters for HVAC and medical respirators.

On the product side, integration of nano-functional additives (antimicrobial silver or permanently bound quaternary ammonium agents), hydrophobic silica treatments, and plasma activation allow microfiber textiles to meet stricter hygiene and durability specifications without sacrificing hand feel. Traceability tools—digital product passports and inline spectrophotometric color matching—help premium suppliers meet procurement specifications in healthcare and automotive OEM supply chains. Collectively, these technological advances increase capital intensity but materially raise product differentiation and reduce life-cycle environmental impacts when combined with recycling and low-chemical finishing flows.

In October 2023, Ahlstrom announced the launch of a new glass-fiber tissue line in Madisonville, U.S., intended for high-performance building and industrial materials; the expansion increased regional processing capability and complemented the company’s move into higher-value technical substrates. Source: www.ahlstrom.com

In March 2024, Freudenberg Performance Materials unveiled a new 100% synthetic wetlaid nonwoven product line manufactured in Germany that supports filtration and other industrial applications and can be produced using ultra-fine micro-fibers. Source: www.freudenberg-pm.com

In March 2024, Toray Group posted news of new product introductions in its water-treatment membrane and filter product lineup, highlighting developments in filtration materials and exhibiting these technologies at regional trade events in 2024. Source: www.toray.in

In April 2024, an industry restructuring event saw 3M complete strategic portfolio moves related to its filtration and healthcare businesses (spinoff and corporate streamlining reported across 2023–2024), affecting commercial positioning and channel approaches in filtration-related microfiber markets. Source: www.wsj.com

This report provides a comprehensive, decision-oriented analysis of the microfiber industry across product types, applications, technologies, and geographies. Coverage includes continuous filament and staple microfibers, nonwoven webs, bicomponent constructs, electrospun/nanofiber membranes, and functionalized/surface-treated microfiber variants. Application analysis spans household cleaning, industrial and HVAC filtration, performance apparel, automotive interiors, medical and hygiene textiles, and specialty industrial uses (electronics cleaning, precision wiping). End-user profiling addresses consumer households, institutional purchasers (healthcare, hospitality), OEMs (automotive and filtration equipment manufacturers), and contract textile processors.

Geographic scope is global with region-level granularity—Asia-Pacific, Europe, North America, South America, and Middle East & Africa—and includes major country profiles, installed capacity estimates (line counts and typical line capacities in tpa), and capital-expenditure trends for modernization and recycling projects. The report examines manufacturing process technologies (spinning, bicomponent extrusion, electrospinning, finishing), digital quality control implementations, and circular-economy approaches (mechanical and chemical recycling workflows). Competitive analysis maps active competitors, estimated scale tiers, and the combined share of leading players, while technology sections quantify improvements in throughput, energy and water savings from retrofits, and filtration performance metrics.

Deliverables include segmentation-level demand estimates, application use patterns, technology roadmaps, regulatory and compliance implications for microplastic and wastewater management, and investment guidance for capacity planning, R&D prioritization, and partnership strategies. The scope also highlights niche growth opportunities—medical-grade washable microfibers, microplastic-mitigating filter inserts, and smart/functional microfibers—providing actionable insight for executives, product managers, and investors evaluating entry, expansion, or upgrade strategies in the microfiber market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 7,832.9 Million |

| Market Revenue (2032) | USD 9,914.8 Million |

| CAGR (2025–2032) | 2.99% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, End-User Behavior Analysis, Regulatory & ESG Overview, Recent Developments, Innovation & Material Science Insights |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Toray Industries, Inc., Freudenberg Performance Materials, Ahlstrom (Ahlstrom-Munksjö), 3M, Kimberly-Clark Professional, DuPont (performance polymers & fibers), Berry Global, Suominen Corporation |

| Customization & Pricing | Available on Request (10% Customization Free) |