Reports

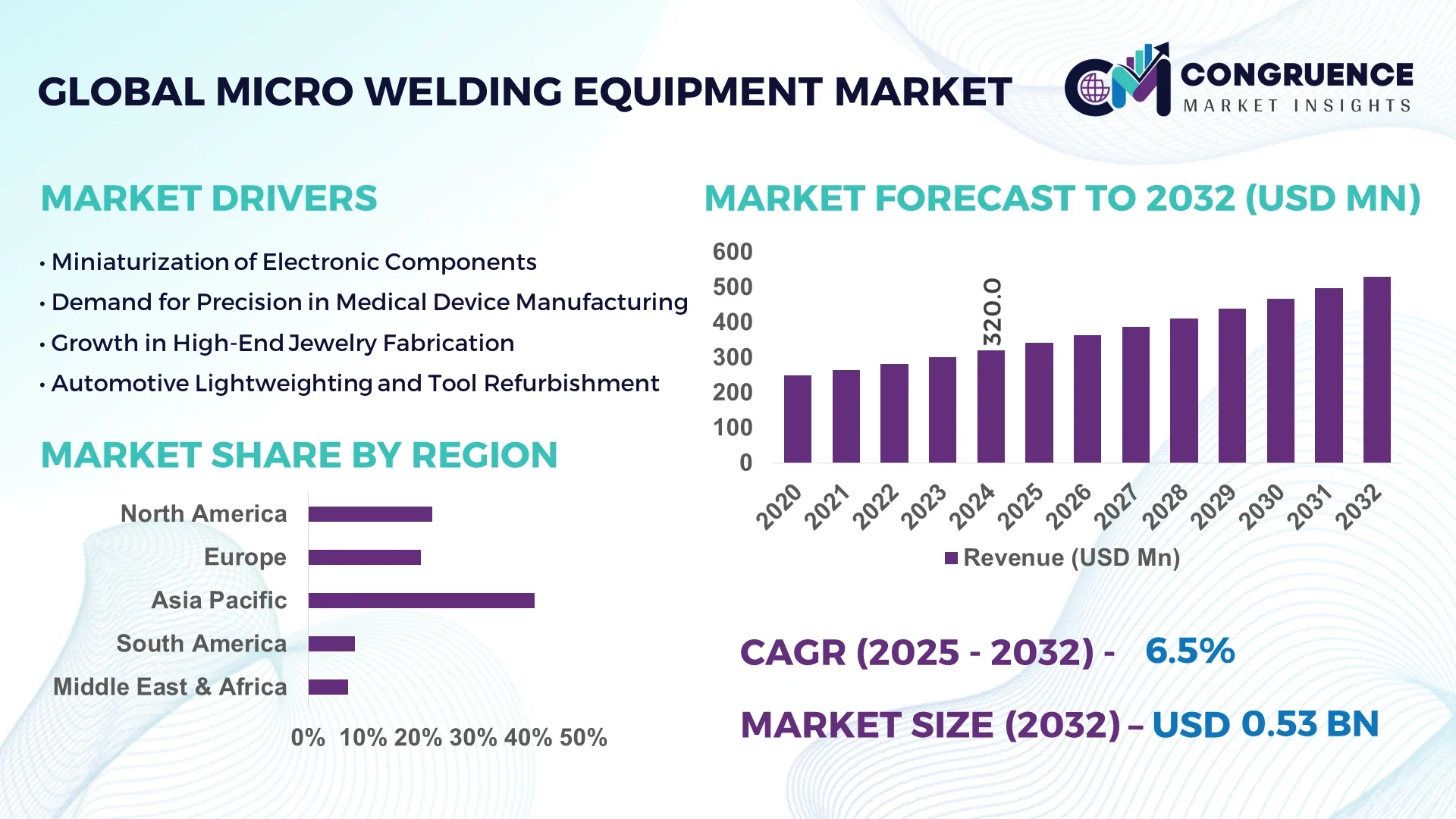

The Global Micro Welding Equipment Market was valued at USD 320.0 Million in 2024 and is anticipated to reach a value of USD 529.6 Million by 2032 expanding at a CAGR of 6.5% between 2025 and 2032.

China remains the dominant force in the Micro Welding Equipment Market, with robust annual production capacity exceeding 10,000 units. In 2024 alone, over USD 500 million was invested into state‑of‑the‑art micro welders and supporting automation systems. Its key applications span high‑precision electronics and medical device manufacturing, where micro‑scale weld integrity and repeatability are critical, and technological advancements feature integrated laser optics and AI‑driven calibration modules.

Micro Welding Equipment is integral across diverse sectors. In 2023, jewelry contributed approximately 40%, medical devices 25%, electronics 20%, and mold maintenance 15% of total volume. Major product innovations include fiber‑laser micro welders featuring sub‑10‑micron beam diameters, automated pulsed‑arc systems with servo‑controlled impedance, and turnkey robotic workcells for multi‑axis welding. Regulatory and environmental trends such as ISO 13485 for medical devices and RoHS‑compliant electronics drive material traceability and low‑heat methods. Regionally, North America leads in aerospace and defense applications, while Asia Pacific’s growth stems from rising consumer electronics. Trend indicators highlight an uptake of smart welding heads with embedded sensors and a rise in remote diagnostics. Looking ahead, adoption of Industry 4.0 practices—such as real‑time process monitoring and digital twins—will shape future market evolution.

Artificial intelligence is revolutionizing the Micro Welding Equipment Market by enhancing precision, throughput, and defect reduction. In modern production lines, AI‑driven controllers analyze real-time sensor data—such as arc voltage, weld pool imagery, and acoustic emissions—to dynamically adjust parameters like laser power, pulse frequency, and feed speed. As a result, manufacturers report up to 30% gains in welding repeatability and a 25% reduction in scrap rates for sensitive components. This integration enables continuous in‑situ quality assurance, eliminating bottlenecks and reducing reliance on post‑process inspection.

Enhanced process optimization software, leveraging machine learning models trained on millions of weld cycles, now enables predictive maintenance of welding heads and optics, extending component life by 15–20%. Such platforms also support adaptive weld scheduling, dynamically allocating production samples to optimal stations, improving line efficiency by approximately 18%. AI‑powered analytics dashboards present actionable metrics—cycle time variance, defect distribution, energy consumption—tailored to decision‑makers and process engineers.

Furthermore, AI‑guided multi‑axis robotic micro welding systems now coordinate synchronized movements with vision‑based joint tracking, enabling complex assemblies—such as medical micro‑stents or microfluidic substrates—to be welded with micron‑level accuracy. These systems can process high‑mix, low‑volume batches without custom fixturing, reducing setup time by nearly 40%. Overall, the convergence of AI and micro welding is delivering a transformative shift to smarter, leaner, and more resilient manufacturing architectures for high‑value, precision‑critical industries.

“In mid‑2024, a leading laser‑micro‑welding OEM introduced an AI‑calibration module that reduced beam alignment time by 60%, achieving consistent focal spot centering within ±2 µm across 500 validation cycles.”

The Micro Welding Equipment Market is shaped by several dynamic forces. Precision demand from industries such as electronics and medical devices is driving sustained investment in automated micro welders and fusion‑based technologies. Meanwhile, miniaturization trends in consumer and industrial products continue to pressure manufacturers to enhance weld accuracy and repeatability. The rise of smart manufacturing and digital transformation is pushing suppliers to embed connectivity protocols (e.g., OPC UA, MQTT) and predictive analytics directly into welding systems. Environmental and regulatory requirements are propelling low‑heat and low‑emission welding methods. Competitive pressures are increasing, with manufacturers differentiating through bundled solutions—training, service contracts, and remote support. Additionally, rising labor costs in key regions are incentivizing automation adoption. Taken together, these trends are reshaping the Micro Welding Equipment Market toward higher reliability, integration, and intelligent process control.

The explosion of compact electronic devices—including wearables, IoT sensor arrays, and advanced semiconductors—has created new demand for Micro Welding Equipment capable of sub‐100 µm weld widths. In 2024, production of micro‑welded assemblies in Asia surged by 28%, while manufacturers using pulsed‑arc systems reported 22% improvements in first‑pass yield. These precision welding capabilities enable reliable connection of ultra-thin wires, micro channels, and delicate components, underpinning the broader electronics device market.

Advanced Micro Welding Equipment featuring laser sources, vision systems, and AI controls often costs upwards of USD 150,000 per unit. Small and medium enterprises face budget constraints that delay adoption. Additionally, successful deployment requires specialized process engineers. A 2023 survey found only 32% of welding technicians had formal training in laser micro welding, resulting in under-utilization and extended ramp-up times of up to six months for new systems.

Embedding Micro Welding Equipment into digital twin ecosystems allows manufacturers to simulate and optimize weld cycles before actual production. By integrating sensor data and process models, companies achieved 15% cycle time reductions and accurate forecasting of maintenance intervals. With connected welding devices, cloud-based analytics can drive centralized quality control across global facilities, presenting a strong avenue for workflow standardization and efficiencies.

High-energy micro welding processes—especially lasers—can introduce localized heat-affected zones, impacting material integrity. Manufacturers report average energy consumption of 12 kW‑hrs per 100 welds, and inconsistent thermal profiles have led to 5% rework rates in critical components. Regulatory pressure to lower energy usage requires real-time thermal monitoring and optimized duty cycles, posing a technical and cost challenge for equipment makers.

Adoption of fiber‑laser handheld units: A growing number of manufacturers are deploying portable fiber-laser micro welders featuring ergonomic designs and instantaneous beam control. Since 2023, handheld sales grew by 15%, enabling on-site repair of electronics and rapid prototyping without dedicated OEM systems.

Smart realtime welding heads with embedded sensors: Advanced welding heads now embed optical, acoustic, and thermal sensors. These systems monitor weld parameters continuously; adoption rates climbed from 12% to 27% across leading factories, improving defect detection with less than 1% false positives.

Modular robotic micro welding cells: Turnkey robotic welding islands with quick‑replace end‑effectors became standard in 2024. These modular cells offer installation time under three days and facilitate rapid job changeovers, reducing line idle time by up to 20%.

Remote diagnostics and cloud‑based performance analytics: More manufacturers are using cloud platforms to monitor Micro Welding Equipment from remote locations. This shift enables field engineers to troubleshoot issues within hours, reducing mean-time-to-repair by about 30% and increasing uptime for global operations.

The Micro Welding Equipment Market is segmented comprehensively by type, application, and end-user, reflecting a diverse landscape shaped by technological innovation and sector-specific demands. In terms of type, laser micro welding, arc micro welding, and resistance micro welding are among the key categories offering varying levels of precision, material compatibility, and automation. Applications span across medical devices, electronics, jewelry, automotive, and mold repair—each requiring different technical specifications and throughput capacities. End-user segments include OEMs, contract manufacturers, R&D institutions, and service/repair centers, each leveraging micro welding systems based on operational scale, component complexity, and production frequency. This segmentation is crucial for industry players to align product development and marketing strategies with end-use requirements and emerging trends. The evolution of miniaturized electronics, medical implants, and intricate metal parts is continually redefining the demand matrix across all three segmentation axes.

Laser micro welding is the dominant type in the market due to its superior precision, ability to work with heat-sensitive materials, and minimal thermal distortion. It is widely deployed across medical, electronics, and aerospace sectors where micron-level accuracy and clean joints are critical. Recent integration with robotic automation and AI-enhanced control systems further strengthens its positioning in high-throughput manufacturing lines.

The fastest-growing type is pulsed-arc micro welding. Its rise is driven by increasing adoption in mold repair, fine jewelry, and prototyping environments. These systems are valued for their versatility, affordability, and reduced setup complexity, especially in operations that do not require ultra-fine precision but demand high reliability.

Resistance micro welding continues to maintain a steady niche presence, particularly in battery tab welding, wire connections, and contact welding. Despite lower growth, it offers cost-effective and robust solutions in high-volume applications where joint consistency is paramount. Other types such as ultrasonic and thermocompression welding also exist but are generally limited to specialized use cases.

The leading application for micro welding equipment is in medical devices, particularly for assembling pacemakers, surgical instruments, microcatheters, and implants. These products require extremely high-quality, contamination-free welds, and the industry’s stringent compliance environment mandates precision equipment.

The fastest-growing application segment is the electronics industry. Increased demand for compact and complex components like microprocessors, sensors, and circuit board assemblies is creating significant growth momentum. Manufacturers are investing in micro welding systems to ensure defect-free joins in ever-shrinking components and multilayer substrates.

Jewelry remains a steady and significant application area, especially in regions with strong demand for customized and high-end metal designs. Automotive applications, particularly in electric vehicles, are expanding due to the need for precision joining of miniature components in battery systems and electrical connectors. Mold and tool repair continues to rely on micro welding for extending tool life and reducing production downtime, contributing consistently to the application matrix.

Original Equipment Manufacturers (OEMs) are the leading end-users in the Micro Welding Equipment Market. These organizations invest heavily in advanced micro welding solutions to ensure quality, consistency, and efficiency in production environments. In sectors such as medical devices and electronics, OEMs demand high-speed automation, multi-axis capability, and data integration features for quality assurance and traceability.

Contract manufacturers are the fastest-growing end-user group. As OEMs increasingly outsource production to reduce cost and focus on core competencies, contract manufacturers are rapidly adopting advanced micro welding systems to meet client specifications. Their flexible business models and willingness to invest in high-mix, low-volume capabilities are driving equipment purchases across Asia and Eastern Europe.

Other end-users such as repair and refurbishment centers also contribute significantly, particularly in jewelry, tooling, and electronics repair. Research institutions and prototype developers leverage micro welding for R&D and small-batch applications, supporting innovation cycles across multiple industries. Their role, although smaller in volume, is crucial in pioneering new welding techniques and applications.

Asia-Pacific accounted for the largest market share at 41.2% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 7.1% between 2025 and 2032.

Asia-Pacific’s dominance is largely attributed to high-volume manufacturing hubs, an expansive electronics sector, and increasing investment in medical technology infrastructure, especially in China, Japan, and South Korea. Meanwhile, North America’s accelerated growth is supported by advanced automation, adoption of AI-integrated welding systems, and a growing emphasis on reshoring precision manufacturing capabilities. Additionally, regulatory modernization and workforce upskilling initiatives are enabling faster adoption of micro welding technologies across high-precision industries in both established and emerging economies.

North America held approximately 23.6% of the global Micro Welding Equipment Market in 2024, supported by its dominant position in aerospace, defense, and medical device manufacturing. The United States and Canada continue to invest heavily in precision production systems and high-mix, low-volume manufacturing models. Key drivers include the rise of implantable medical devices, micromachined aerospace parts, and miniaturized electronics. Regulatory reforms such as the U.S. CHIPS Act and FDA modernization are fueling demand for advanced welding capabilities. The integration of AI, real-time process monitoring, and machine learning-based optimization platforms is rapidly transforming legacy welding systems. Adoption of digital twin simulation and remote diagnostics is also enhancing operational resilience and scalability in the region.

Europe accounted for roughly 20.7% of the Micro Welding Equipment Market in 2024, with Germany, the UK, and France leading regional consumption. Germany’s automotive and engineering sectors, the UK’s aerospace manufacturing, and France’s strong medical device industry continue to drive demand for high-performance micro welding solutions. Regulatory bodies such as the European Chemicals Agency (ECHA) and growing ESG mandates are encouraging the adoption of eco-friendly, energy-efficient welding technologies. Europe is also pioneering the use of smart robotic welding arms and sensor-integrated welding heads that align with Industry 4.0 and sustainability goals. The European Green Deal and other regional decarbonization efforts are influencing welding process innovation and equipment upgrades across critical applications.

Asia-Pacific remained the largest regional market by volume in 2024, accounting for 41.2% of global demand. China, Japan, and India are the top consumers, driven by large-scale electronics production, rapid urbanization, and medical manufacturing expansions. China’s strong investment in micro welding automation and Japan’s precision engineering leadership continue to push boundaries in quality and output. India is rapidly emerging as a micro welding hub for mid-tier electronics and device assembly, supported by government-led manufacturing initiatives. Regional tech corridors in Shenzhen, Tokyo, and Bangalore are becoming innovation centers for next-generation welding technologies including fiber-laser integration, AI-guided systems, and real-time analytics. Demand for high-throughput, low-defect equipment is scaling rapidly across consumer electronics, EV batteries, and diagnostic device sectors.

South America represented an estimated 6.3% of the global Micro Welding Equipment Market in 2024, with Brazil and Argentina as key contributors. Brazil’s electronics assembly operations and energy infrastructure projects are driving adoption of advanced micro welding systems. In Argentina, increased activity in automotive electronics and tooling industries is creating opportunities for precision joining equipment. Regional growth is supported by infrastructure modernization and expanding local production of medical and electrical devices. Government-led incentives for industrial automation and trade reforms targeting manufacturing equipment are encouraging the adoption of smart welding platforms. Importantly, regional training and certification programs are enhancing technical capabilities and accelerating integration of micro welding technologies in smaller enterprises.

Middle East & Africa accounted for 4.1% of the global Micro Welding Equipment Market in 2024. Major growth drivers include oil & gas infrastructure, automotive assembly, and modular construction projects. The UAE and South Africa are leading adopters of micro welding systems, particularly in energy, medical diagnostics, and electrical manufacturing sectors. Government diversification strategies such as the UAE’s industrial transformation plan and South Africa’s localization of component production are supporting regional equipment investments. Technological modernization, including the adoption of portable fiber-laser micro welders and AI-enhanced quality control, is gaining traction in industrial parks. Local regulations now emphasize quality and safety compliance, encouraging higher standards in welding process accuracy and traceability.

China – 28.9% Market Share

High production capacity combined with rapid integration of micro welding automation in electronics and medical device sectors.

United States – 17.6% Market Share

Strong end-user demand from aerospace, defense, and surgical device manufacturers, coupled with high adoption of AI-powered welding systems.

The Micro Welding Equipment Market features a moderately fragmented competitive landscape with over 75 active global manufacturers and several regional technology integrators. Key players compete through continuous innovation, product performance, and integration with Industry 4.0 features. Leading companies have expanded their portfolios to include AI-enabled welding systems, modular robotic welding platforms, and cloud-connected monitoring solutions. Strategic partnerships between equipment manufacturers and automation providers have increased, focusing on co-developing intelligent welding workcells for medical and electronics sectors.

Product launches have emphasized faster weld cycle times, enhanced cooling systems, and greater energy efficiency. Companies are also investing in vertical integration to streamline component supply chains, particularly for laser modules and motion systems. Mergers and acquisitions are reshaping competitive dynamics, with several mid-size players consolidating to scale capabilities and expand market presence in North America and Asia-Pacific. Competitive differentiation is also driven by aftersales services, technician training programs, and software customization, especially among contract manufacturers and OEMs operating high-mix production lines.

AMADA WELD TECH

Emerson Electric Co.

IPG Photonics Corporation

OR Laser (Coherent Inc.)

Sunstone Engineering

Miyachi Unitek Corporation

Sisma S.p.A

LaserStar Technologies Corporation

Shenzhen Huagong Laser Engineering Co., Ltd.

Alpha Laser GmbH

MKS Instruments

TECHSONIC Industries

Technological advancements are reshaping the Micro Welding Equipment Market, particularly in the areas of laser technology, real-time control systems, and intelligent automation. One of the most significant breakthroughs is the integration of fiber lasers with sub-10 μm beam diameters, enabling ultra-precise welding for miniature components in electronics and medical implants. These lasers offer deeper penetration, lower thermal impact, and high beam quality, making them ideal for micro-scale joining tasks.

Artificial intelligence and machine learning are now embedded in process control modules, allowing for automatic parameter adjustments during live operations. These smart systems optimize arc stability, reduce defect rates by up to 25%, and provide predictive maintenance analytics based on sensor feedback. Additionally, robotic welding arms with multi-axis freedom and vision-guided joint tracking are being adopted for complex geometries and small-batch production.

Digital connectivity is another key area of focus, with manufacturers offering cloud-enabled dashboards that monitor energy usage, weld quality, and equipment health across multiple facilities. Pulse shaping and waveform modulation technologies are also enhancing weld consistency across different materials and thicknesses. These innovations are enabling a transition from manually tuned equipment to fully autonomous systems capable of real-time performance optimization and remote diagnostics, making micro welding smarter and more adaptive to industry-specific needs.

• In January 2024, Sunstone Engineering unveiled its new Orion mPulse 30i, a benchtop micro welder featuring pulse arc technology with digital touchscreen control, reducing electrode wear by 35% and improving weld cycle speed by 22% compared to earlier models.

• In March 2024, IPG Photonics launched a high-frequency fiber laser micro welder capable of producing welds as narrow as 8 microns, aimed at semiconductor and microelectronic packaging applications, delivering 18% better edge joint stability.

• In September 2023, Alpha Laser GmbH introduced an upgraded mobile laser welding system with onboard battery storage, allowing 6 hours of cordless operation in field service environments, targeting on-site tool and mold repair professionals.

• In November 2023, Emerson Electric Co. integrated its Branson micro-welding platform with IoT-ready diagnostics, enabling real-time alerts for electrode misalignment and predictive wear, leading to a 40% reduction in unplanned downtime at pilot facilities.

The Micro Welding Equipment Market Report provides an in-depth examination of the global market landscape, focusing on equipment types, application sectors, technological innovations, and regional performance across major economies. It covers detailed segmentation by laser welding, arc welding, resistance welding, and emerging technologies such as ultrasonic and hybrid welding systems. The report outlines key applications in medical devices, electronics, automotive, jewelry, and mold repair, offering insights into how each sector is adopting micro welding technologies based on product design complexity, material requirements, and compliance needs.

Geographically, the report analyzes North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting regional manufacturing strengths, infrastructure development, and government policies influencing adoption. It also profiles usage trends among key end-users such as OEMs, contract manufacturers, repair centers, and research institutions, detailing how demand varies by industrial focus and production volume.

Furthermore, the report emphasizes the role of AI integration, automation, smart diagnostics, and remote monitoring in shaping future equipment capabilities. It also identifies niche opportunities such as wearable electronics, implantable medical technology, and next-gen battery components, where micro welding systems are becoming essential for precision assembly. Overall, the scope is designed to inform stakeholders on investment decisions, product strategy, and competitive positioning in this fast-evolving manufacturing domain.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 320.0 Million |

| Market Revenue (2032) | USD 529.6 Million |

| CAGR (2025–2032) | 6.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | AMADA WELD TECH, Emerson Electric Co., IPG Photonics Corporation, OR Laser (Coherent Inc.), Sunstone Engineering, Miyachi Unitek Corporation, Sisma S.p.A, LaserStar Technologies Corporation, Shenzhen Huagong Laser Engineering Co., Ltd., Alpha Laser GmbH, MKS Instruments, TECHSONIC Industries |

| Customization & Pricing | Available on Request (10% Customization is Free) |