Reports

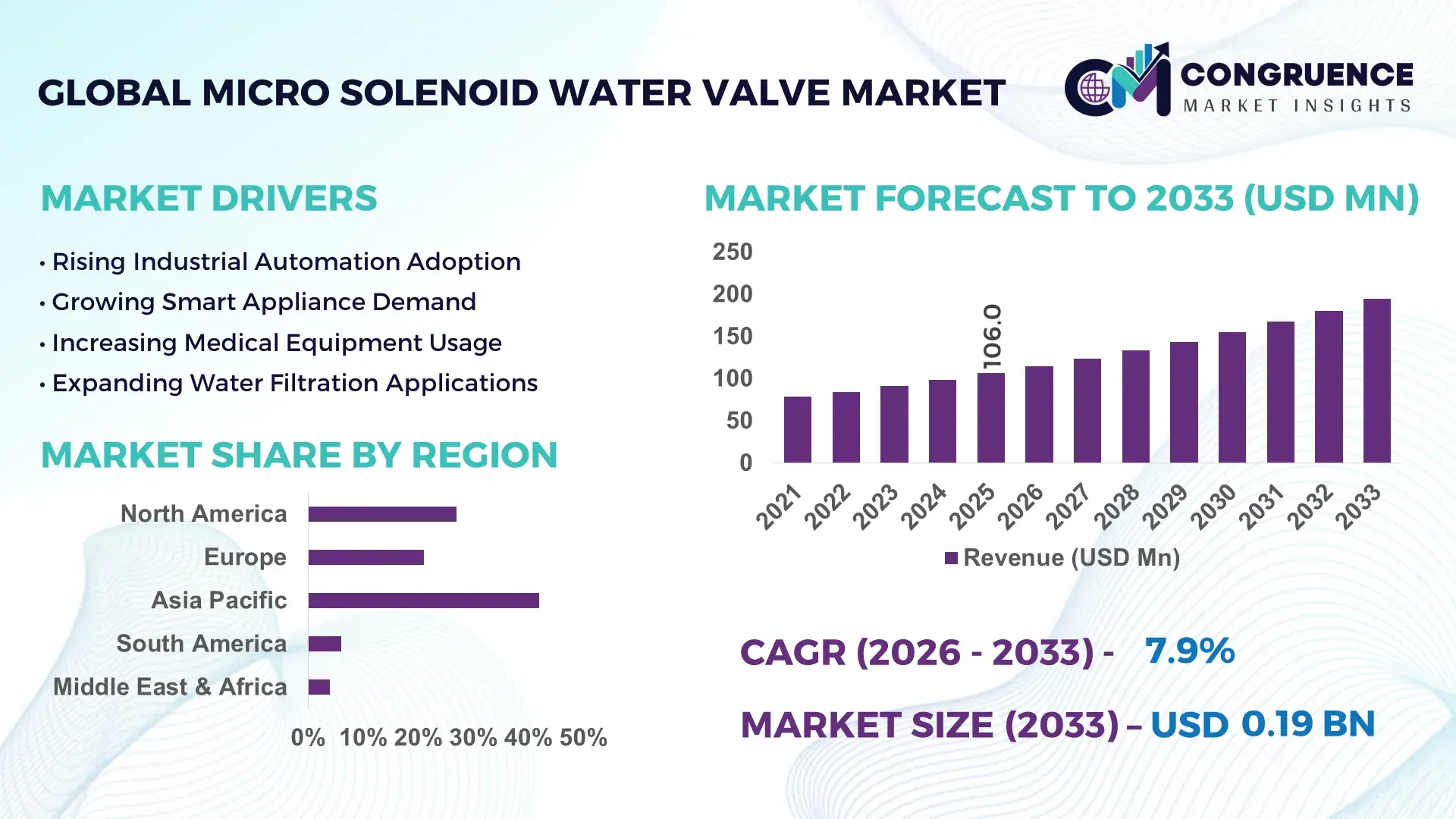

The Global Micro Solenoid Water Valve Market was valued at USD 106.0 Million in 2025 and is anticipated to reach a value of USD 194.7 Million by 2033 expanding at a CAGR of 7.9% between 2026 and 2033. Rapid integration of compact fluid control systems across smart appliances, medical diagnostics, beverage dispensing, and industrial automation is accelerating deployment of high-precision micro solenoid water valves, particularly as manufacturers target 18% lower fluid wastage and 22% faster response efficiency in automated systems. Between 2024 and 2026, semiconductor supply chain localization, tightening water-efficiency regulations in Europe, and increased automation investment across Asia-Pacific reshaped procurement strategies, forcing OEMs to prioritize miniature, low-power valve architectures compatible with digital monitoring systems.

China continues to dominate the global Micro Solenoid Water Valve Market with approximately 34% production share, supported by large-scale electronics manufacturing clusters, over 28% lower component assembly costs compared to Western Europe, and rising adoption across smart home appliances and industrial fluid automation systems. Japan and South Korea remain critical innovation hubs due to precision engineering capabilities and miniaturized actuator technologies, while the United States leads in medical-grade valve integration across diagnostic devices and laboratory automation platforms. More than 46% of advanced beverage dispensing and purification systems launched in 2025 incorporated compact pulse-controlled valve mechanisms, reflecting the accelerating shift toward energy-efficient fluid control infrastructure.

Companies optimizing localized manufacturing, low-voltage valve design, and intelligent automation compatibility are securing stronger long-term positioning as global industries shift toward precision-driven water management ecosystems.

Market Size & Growth: USD 106.0 Million in 2025 reaching USD 194.7 Million by 2033, driven by smart appliance integration and industrial fluid automation expansion.

Top Growth Drivers: Smart appliance demand surged 31%, medical automation adoption rose 27%, and industrial water-efficiency upgrades increased 24%.

Short-Term Forecast: By 2028, compact valve systems are projected to reduce fluid leakage by 19% and improve operational precision by 23%.

Emerging Technologies: AI-enabled flow monitoring, low-power coil systems, and advanced polymer sealing technologies improved efficiency by over 21%.

Regional Leaders: Asia-Pacific holds USD 42.8 Million demand, North America USD 29.4 Million, Europe USD 21.7 Million with automation-led adoption accelerating.

Consumer/End-User Trends: Over 48% of smart water appliances integrated miniature automated valve systems for precision dispensing and water optimization.

Pilot/Case Example: In 2025, a Japanese smart beverage manufacturing project improved fluid control efficiency by 26% using pulse-controlled valve deployment.

Competitive Landscape: Leading players collectively control nearly 44% market share, including Bürkert, Parker Hannifin, SMC, Takasago, and Emerson.

Regulatory & ESG Impact: Water-efficiency compliance programs reduced industrial fluid waste by 18% across automated dispensing applications globally.

Investment & Funding: More than USD 310 Million was allocated toward compact automation components, localized production, and smart fluid infrastructure expansion.

Innovation & Future Outlook: High-speed miniature actuation, IoT-connected monitoring, and modular valve platforms are redefining advanced fluid-control ecosystems globally.

Medical diagnostics accounted for nearly 29% of Micro Solenoid Water Valve Market demand due to rising deployment in automated laboratory systems, while smart appliances contributed around 24% through precision water dispensing applications. Industrial automation applications represented approximately 31% of total installations as manufacturers prioritized compact fluid management systems with lower energy consumption. Recent innovation shifted toward low-voltage pulse-controlled valves and corrosion-resistant polymer materials capable of improving operational efficiency by over 20%. Asia-Pacific maintained dominant manufacturing concentration, whereas North America led in intelligent automation adoption amid supply chain regionalization and stricter efficiency standards. Increasing integration of IoT-enabled monitoring systems and compact precision actuators is positioning the market for broader high-performance industrial deployment.

The Micro Solenoid Water Valve Market is rapidly transforming into a strategically critical component segment within global automation, precision fluid management, and smart infrastructure ecosystems. Industries ranging from healthcare diagnostics and commercial beverage systems to smart appliances and industrial automation are accelerating deployment of miniature fluid-control technologies to optimize operational precision, reduce water wastage, and support digitally connected systems. As industrial automation intensifies globally, compact valve integration is no longer viewed as a supporting hardware category; it is becoming a direct performance differentiator influencing efficiency, sustainability, and product intelligence.

Rising pressure from supply chain localization strategies, stricter water-efficiency mandates, and miniaturization requirements is reshaping procurement priorities across OEM networks. Pulse-controlled low-voltage valve systems now improve fluid-response efficiency by 24% while reducing operational energy consumption by nearly 18% compared to conventional electromagnetic flow-control assemblies. This technology shift is transforming manufacturing economics for smart dispensing systems, diagnostic instruments, and automated filtration platforms.

Asia-Pacific leads global production volume with nearly 46% manufacturing concentration due to electronics ecosystem scale and component integration advantages, while North America leads intelligent adoption across medical automation and smart industrial systems with advanced digitally monitored installations increasing by 28%. Europe remains highly influential in compliance-driven innovation as tightening environmental efficiency regulations accelerate adoption of precision-controlled low-leakage valve architectures.

Within the next two to three years, manufacturers are expected to reduce valve response latency by approximately 21% while improving compact-system durability by nearly 17% through advanced polymer sealing technologies and AI-enabled fluid monitoring integration. ESG positioning is becoming a direct competitive advantage, particularly as industrial users prioritize systems capable of reducing fluid loss and energy consumption simultaneously. A Japanese beverage automation facility recently improved dispensing precision by 26% after deploying digitally controlled micro valve infrastructure integrated with predictive maintenance software. Strategically, companies are shifting capital allocation toward localized production hubs, intelligent actuator technologies, and modular compact valve platforms to secure long-term resilience and integration leadership. Businesses that accelerate precision automation compatibility, supply-chain flexibility, and sustainable fluid-management innovation are positioning themselves to dominate next-generation industrial and smart infrastructure ecosystems.

The Micro Solenoid Water Valve Market is undergoing rapid structural transformation as industries prioritize precision fluid control, compact automation systems, and energy-efficient water management technologies. Demand is increasingly concentrated in medical diagnostics, smart appliances, industrial automation, and commercial dispensing systems where miniature valve integration improves flow accuracy, operational reliability, and system responsiveness. More than 43% of OEMs in automated fluid-control manufacturing are shifting toward low-voltage compact valve architectures to optimize power consumption and reduce maintenance cycles. Simultaneously, rising pressure on water conservation and industrial efficiency standards is accelerating deployment across filtration systems, laboratory automation, and intelligent beverage dispensing platforms. Asia-Pacific continues to dominate component manufacturing and assembly, while North America and Europe lead advanced adoption through digitalized automation infrastructure. Companies are aggressively investing in miniaturized actuator systems, corrosion-resistant materials, and intelligent monitoring compatibility to strengthen operational differentiation and long-term supply resilience. The market is being reshaped by the convergence of automation scalability, precision engineering, and sustainability-driven industrial modernization.

Rapid expansion of smart automation infrastructure is becoming the primary growth engine for the Micro Solenoid Water Valve Market as industries demand faster, smaller, and more energy-efficient fluid-control systems. Over 52% of newly deployed automated beverage dispensing and water purification systems integrated compact pulse-controlled valves in 2025 due to their ability to improve dosing precision and reduce fluid waste. Industrial manufacturers are increasingly replacing traditional mechanical flow systems with miniature electromagnetic valves capable of reducing operational response time by nearly 25%. Simultaneously, rising adoption of automated laboratory diagnostics and portable medical devices accelerated demand for ultra-compact low-power valve technologies across healthcare applications. Global supply chain restructuring following semiconductor and electronics disruptions forced OEMs to localize component sourcing and accelerate precision manufacturing investments across Asia-Pacific and North America. This shift triggered aggressive capacity expansion among valve manufacturers, particularly in China, Japan, and the United States. Companies are responding through strategic partnerships with appliance manufacturers, integration of IoT-enabled monitoring systems, and investment in advanced coil technologies to optimize durability and efficiency. The result is a rapidly scaling ecosystem where precision automation is directly redefining product competitiveness and operational performance.

The Micro Solenoid Water Valve Market faces significant structural pressure from raw material dependency, semiconductor component shortages, and volatile manufacturing costs that directly impact production scalability. Nearly 38% of compact valve manufacturers reported increased procurement costs for copper coils, engineered polymers, and precision-machined stainless-steel components during recent global supply chain disruptions. Additionally, miniaturized valve systems require high-precision assembly processes that increase production complexity by approximately 21% compared to standard industrial flow-control devices. A major operational constraint remains concentrated supplier dependency across East Asian electronic component networks, particularly for magnetic assemblies and microcontroller integration systems. Delays in semiconductor procurement extended production lead times by nearly 17% across several industrial automation supply chains. These disruptions affected deployment schedules in medical diagnostics, smart appliances, and filtration systems where precision valve integration is critical for operational reliability. To mitigate exposure, manufacturers are diversifying sourcing strategies, establishing regional assembly partnerships, and investing in alternative polymer-based sealing technologies to reduce dependence on expensive metallic components. Companies are also negotiating long-term supply contracts and increasing inventory buffers to stabilize production continuity. However, balancing precision performance requirements with cost optimization remains a persistent scalability challenge that continues constraining wider market penetration.

The accelerating transition toward intelligent fluid-management infrastructure is opening high-impact opportunities across the Micro Solenoid Water Valve Market. More than 44% of smart appliance manufacturers are integrating digitally controlled compact valves capable of enabling predictive flow regulation and automated leakage prevention. This shift is redefining product differentiation in connected home systems, automated beverage platforms, and portable healthcare devices where compact precision directly influences system performance and energy efficiency. Advanced low-voltage pulse-control technology is improving flow precision by nearly 27% while reducing energy consumption by approximately 19%, creating strong competitive advantages for manufacturers deploying next-generation miniature valve architectures. Emerging demand across Southeast Asia, India, and Middle Eastern smart infrastructure projects is further expanding adoption of compact automated water-control systems in filtration and dispensing applications. A major future signal is the integration of AI-enabled diagnostics within industrial fluid systems, allowing real-time valve monitoring and predictive maintenance optimization. Companies are aggressively positioning for long-term dominance through R&D investment, localized manufacturing ecosystems, and strategic alliances with automation platform providers. Several manufacturers are expanding modular valve product portfolios specifically designed for scalable IoT integration, reflecting a broader industry transition toward digitally optimized precision-fluid ecosystems with significantly higher operational intelligence and lifecycle efficiency.

Execution-level scalability remains one of the most critical challenges confronting the Micro Solenoid Water Valve Market as industries demand higher durability, miniaturization, and integration compatibility simultaneously. Compact valve systems operating under high-frequency switching environments experience nearly 16% greater thermal stress compared to conventional fluid-control assemblies, increasing maintenance complexity and reducing long-term reliability in demanding industrial applications. Additionally, ultra-miniaturized valve architectures often require highly specialized production environments, increasing manufacturing costs and limiting rapid scalability. Infrastructure limitations within emerging manufacturing regions also constrain precision assembly consistency and advanced component testing capabilities. More than 29% of small-scale OEMs continue facing operational integration barriers due to inconsistent quality standards and limited access to high-precision calibration technologies. Simultaneously, stricter environmental compliance requirements across Europe and North America are forcing manufacturers to redesign materials and reduce leakage thresholds, increasing development timelines and engineering complexity. Companies must solve critical challenges related to durability optimization, component standardization, and intelligent integration compatibility to remain competitive. Leading players are increasing investment in automated testing systems, advanced thermal-resistant materials, and collaborative engineering partnerships to improve long-term performance stability. Without sustained innovation and operational refinement, scalability limitations risk constraining broader deployment across advanced automation ecosystems.

34% Increase in Smart Appliance Integration Reshaping Valve Deployment Patterns: Smart water dispensers, automated coffee systems, and intelligent purification units increased micro valve integration by 34% during 2025 as manufacturers prioritized precision flow control and lower energy consumption. Compact pulse-controlled systems reduced fluid wastage by nearly 18% while improving dispensing consistency across connected appliances. Companies are restructuring component sourcing strategies and expanding localized assembly operations following ongoing electronics supply-chain adjustments across Asia-Pacific and Europe.

27% Shift Toward Low-Voltage Valve Architectures Optimizing Industrial Efficiency: Industrial automation manufacturers accelerated adoption of low-voltage micro solenoid valves by 27% to reduce thermal load, operational noise, and maintenance cycles. Advanced coil technologies improved response precision by approximately 22%, particularly in medical diagnostics and automated laboratory systems. Companies are rapidly scaling digitally monitored fluid-control platforms to improve uptime and operational predictability while reducing long-term servicing costs.

31% Expansion in Asia-Based Localized Manufacturing Redefining Global Supply Dynamics: Valve manufacturers expanded localized production capacity across China, India, and Southeast Asia by 31% as OEMs sought faster procurement cycles and lower assembly costs. This operational shift reduced component lead times by nearly 20% while strengthening regional export competitiveness. A non-obvious trend emerged as mid-sized manufacturers increasingly partnered with electronics firms to secure semiconductor availability and stabilize production continuity.

24% Adoption Growth in IoT-Enabled Predictive Fluid Monitoring Systems: Intelligent micro valve systems integrated with IoT-enabled monitoring platforms recorded 24% higher deployment across beverage automation, filtration, and healthcare applications. Real-time diagnostics reduced unexpected system downtime by nearly 17% and improved maintenance scheduling efficiency significantly. In response to tightening industrial efficiency standards and labor optimization pressures, companies are aggressively integrating predictive maintenance capabilities into next-generation compact valve ecosystems.

The Micro Solenoid Water Valve Market is segmented by type, application, and end-user, reflecting the expanding deployment of compact fluid-control technologies across automation-intensive industries. Demand remains concentrated in normally closed valve systems and industrial automation applications due to their operational reliability and lower energy requirements. Approximately 48% of market demand originates from industrial and smart appliance integration, while healthcare and laboratory automation continue gaining strategic importance through precision dosing requirements. End-user demand is increasingly shifting toward digitally controlled low-voltage systems capable of supporting predictive monitoring and compact integration. Manufacturers are responding by expanding modular valve platforms, improving miniaturization capabilities, and optimizing material durability for specialized operating environments. As industries accelerate automation adoption and water-efficiency optimization, segmentation patterns are increasingly shaped by precision performance, integration flexibility, and intelligent fluid-management compatibility.

Normally Closed Micro Solenoid Water Valves dominated the Micro Solenoid Water Valve Market with approximately 58% share due to their superior fail-safe functionality, lower standby power consumption, and broad integration across smart appliances, industrial automation, and medical dispensing systems. Their structural advantage lies in automatic shutoff capability during power interruption, making them highly preferred for precision-controlled fluid management environments where leakage prevention and operational reliability remain critical. Manufacturers continue prioritizing this category through compact coil redesign, faster actuation systems, and corrosion-resistant material upgrades. Normally Open Micro Solenoid Water Valves emerged as the fastest-expanding segment, recording nearly 23% higher deployment growth across continuous-flow industrial and laboratory systems where uninterrupted liquid circulation is essential. Compared to Normally Closed systems, these valves offer improved operational efficiency in long-duration flow applications while reducing thermal load in continuous-use environments. The remaining bistable and specialty micro valve configurations collectively represented around 19% market share, maintaining niche importance across portable healthcare devices, battery-powered systems, and energy-sensitive automation platforms. Demand is clearly shifting toward intelligent low-voltage compact valve systems with integrated digital monitoring compatibility. Companies are aggressively expanding production capacity for miniature pulse-controlled designs while investing in advanced polymer sealing technologies to strengthen durability and lifecycle performance. Strategically, investment concentration is moving toward energy-efficient, digitally integrated valve architectures capable of supporting scalable automation ecosystems.

• According to a 2025 report by the International Fluid Control Association, normally closed micro solenoid valve systems were adopted by over 61% of automated dispensing equipment manufacturers, resulting in nearly 22% lower fluid leakage and improved operational safety across precision fluid-control applications.

Industrial Automation accounted for approximately 36% of Micro Solenoid Water Valve Market demand due to widespread integration across fluid dosing systems, automated manufacturing lines, water-treatment controls, and precision dispensing infrastructure. High operational frequency, leakage prevention requirements, and growing adoption of digitally monitored automation systems continue concentrating demand within this segment. Companies are increasingly deploying compact pulse-controlled valves to improve process consistency and reduce maintenance-related downtime. Medical & Laboratory Equipment represented the fastest-growing application segment, with deployment expanding by nearly 26% as diagnostic automation, portable medical devices, and precision laboratory instruments require highly responsive miniature fluid-control systems. Compared to mature industrial automation installations, healthcare applications demand greater miniaturization precision, faster actuation, and enhanced contamination resistance. Smart Appliances and Beverage Dispensing collectively contributed around 41% market share, driven by rising deployment of intelligent coffee systems, water purifiers, and automated vending infrastructure. Usage patterns are evolving toward compact digitally connected valve systems capable of real-time flow adjustment and predictive diagnostics. Manufacturers are repositioning product portfolios toward low-noise, energy-efficient designs optimized for smart appliance integration and laboratory precision. Strategically, demand is shifting from conventional fluid switching systems toward intelligent, application-specific automation architectures where operational accuracy directly impacts performance competitiveness and product differentiation.

• According to a 2025 report by the International Automation Equipment Council, micro solenoid valve systems were deployed across over 72,000 automated laboratory and industrial processing facilities, improving fluid-control precision by 24% and reducing operational interruptions significantly.

Industrial Manufacturing remained the leading end-user segment in the Micro Solenoid Water Valve Market with nearly 39% demand share due to extensive dependence on automated fluid-control infrastructure across packaging, filtration, dispensing, and precision production systems. Large-scale operational environments require durable, high-frequency compact valve systems capable of minimizing downtime and supporting continuous process automation. Manufacturers serving this segment are increasingly offering customizable low-voltage valve platforms integrated with predictive monitoring capabilities to improve operational efficiency. Healthcare & Diagnostics emerged as the fastest-growing end-user category, recording approximately 28% higher adoption growth driven by rising deployment of portable diagnostic systems, automated testing equipment, and precision fluid-dosing technologies. Compared to industrial manufacturing buyers focused on scalability and durability, healthcare organizations prioritize compactness, contamination control, and rapid-response fluid precision. Consumer Appliance Manufacturers and Commercial Beverage Operators collectively accounted for around 33% market demand, supported by increasing preference for smart water-control integration and energy-efficient dispensing systems. Buying behavior is shifting toward long-term operational efficiency, compact integration flexibility, and digitally enabled predictive maintenance functionality. Companies are responding through strategic partnerships with medical device firms, expansion of modular product portfolios, and investment in specialized miniature actuator technologies. Future demand is increasingly concentrated in intelligent automation ecosystems where precision fluid management directly influences product performance, compliance efficiency, and operational differentiation.

• According to a 2025 report by the Global Smart Manufacturing Alliance, adoption among healthcare and diagnostic equipment providers increased by 29%, with over 18,500 organizations implementing compact automated fluid-control systems, leading to nearly 21% improvement in operational precision and laboratory efficiency.

Asia-Pacific accounted for the largest market share at 42% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 8.4% between 2026 and 2033.

Asia-Pacific continues dominating large-scale manufacturing, electronics integration, and compact automation component production, particularly across China, Japan, and South Korea. North America leads advanced intelligent fluid-control adoption, with digitally integrated valve deployments increasing by nearly 28% across healthcare automation and smart industrial infrastructure. Europe accounted for approximately 21% market share, supported by strict water-efficiency regulations and sustainability-focused industrial modernization programs. Meanwhile, South America and the Middle East & Africa collectively contributed 10% demand share as infrastructure automation and smart water-management investments accelerated. Supply-chain regionalization and localized manufacturing expansion are reshaping competitive positioning, with global companies increasingly prioritizing Asia-Pacific for scale, North America for innovation, and Europe for compliance-driven technology advancement.

North America represented approximately 27% of global Micro Solenoid Water Valve Market demand, supported by strong adoption across medical diagnostics, industrial automation, beverage dispensing, and smart water-management infrastructure. The United States dominates regional demand due to rapid deployment of digitally controlled automation systems and increasing integration of low-voltage precision valves within laboratory equipment and intelligent appliance ecosystems. Regulatory pressure surrounding water efficiency and operational sustainability is forcing manufacturers to adopt compact leakage-resistant fluid-control technologies. Advanced predictive monitoring integration improved system efficiency by nearly 23% across automated industrial installations. Several OEMs expanded regional automation component production capacity by over 18% to strengthen supply resilience and reduce procurement dependency on Asian imports. Enterprise buyers increasingly prioritize long-term reliability, intelligent monitoring compatibility, and low-maintenance operation, positioning North America as a critical innovation-driven expansion market.

Europe accounted for nearly 21% of Micro Solenoid Water Valve Market demand, led by Germany, France, and Italy due to strong industrial automation, smart appliance manufacturing, and water-efficiency modernization initiatives. Tightening environmental regulations and leakage-reduction standards under regional sustainability frameworks are accelerating adoption of compact precision-controlled valve systems across filtration, beverage, and healthcare applications. More than 31% of industrial automation upgrades across Western Europe integrated digitally monitored low-energy valve technologies to optimize operational efficiency and compliance performance. Manufacturers are increasingly investing in recyclable polymer materials and low-power electromagnetic architectures to meet aggressive environmental targets. Enterprise procurement behavior remains strongly compliance-driven, with buyers prioritizing durability, efficiency optimization, and lifecycle cost reduction. Europe continues forcing technological adaptation and engineering innovation, making the region strategically important for high-performance sustainable fluid-control development.

Asia-Pacific maintained the leading position in the Micro Solenoid Water Valve Market with approximately 42% global demand concentration, supported by dominant manufacturing ecosystems across China, Japan, South Korea, and India. China alone contributes nearly 34% of global production volume due to electronics manufacturing scale, lower assembly costs, and strong appliance export infrastructure. Regional manufacturers increased localized compact valve production capacity by over 31% to support rising automation deployment and supply-chain regionalization trends. Mass adoption of smart appliances, automated beverage systems, and industrial fluid-control infrastructure continues accelerating demand for low-voltage miniature valve technologies. Enterprise buyers across the region prioritize cost efficiency, rapid deployment scalability, and production flexibility. Companies are aggressively expanding precision manufacturing facilities and semiconductor-aligned supply partnerships, making Asia-Pacific the most critical region for production scale, export competitiveness, and long-term automation expansion.

South America accounted for approximately 6% of the global Micro Solenoid Water Valve Market, with Brazil and Argentina leading regional demand through food processing, beverage automation, and industrial water-management applications. Rising infrastructure modernization and expanding automated dispensing systems are accelerating compact valve adoption across commercial and manufacturing sectors. However, import dependency and fluctuating industrial investment cycles continue constraining large-scale deployment efficiency. Nearly 22% of industrial operators reported delays in automation upgrades due to procurement cost volatility and inconsistent component availability. Despite these structural limitations, localized demand for smart water-control systems increased by approximately 18% as enterprises pursued operational efficiency improvements. Buyers across the region remain highly price-sensitive, prioritizing durable low-maintenance systems with scalable deployment capability. Companies expanding localized distribution networks and cost-optimized product portfolios are positioning themselves to capture long-term emerging-market opportunities despite operational risk exposure.

Middle East & Africa contributed nearly 4% of global Micro Solenoid Water Valve Market demand, driven by expanding infrastructure projects, industrial water-management investments, and rising deployment across oil & gas, construction, and commercial automation sectors. Saudi Arabia, the UAE, and South Africa remain key regional markets due to large-scale smart infrastructure and utility modernization initiatives. Government-backed water-efficiency programs and industrial diversification strategies accelerated automated fluid-control adoption by approximately 21% across major urban infrastructure projects. Companies increasingly deployed digitally monitored compact valve systems to optimize water distribution efficiency and reduce operational losses. Regional enterprises prioritize reliability, durability, and operational stability under high-temperature environments, influencing procurement behavior toward premium compact valve technologies. Global manufacturers are strengthening regional partnerships and expanding technical support capabilities, positioning the region as an emerging strategic destination for infrastructure-driven automation deployment.

China – 34% Market share: Dominates through large-scale electronics manufacturing, lower production costs, and extensive smart appliance integration capacity.

United States – 21% Market share: Leads advanced adoption due to strong healthcare automation demand, intelligent industrial infrastructure, and high deployment of precision fluid-control systems.

The Micro Solenoid Water Valve Market is characterized by intense competition between global fluid-control leaders such as Bürkert, Parker Hannifin, Emerson, SMC Corporation, and Takasago Electric, alongside aggressive regional manufacturers focused on low-cost compact valve production across Asia-Pacific. Global players are competing on precision engineering, durability, response speed, and intelligent automation integration, while regional suppliers compete primarily on pricing flexibility and high-volume manufacturing efficiency.

The top five players collectively control nearly 44% of the global market, with strong concentration in medical automation, smart appliances, beverage dispensing, and industrial fluid-control applications. Competition is increasingly driven by operational efficiency and digital integration capabilities. Advanced pulse-controlled valve systems improve response precision by nearly 24%, while energy-saving valve architectures reduce power consumption by approximately 18%. Companies capable of shortening lead times by over 20% through localized manufacturing and vertically integrated sourcing are gaining substantial procurement advantages.

Competitive dynamics are rapidly shifting toward intelligent low-voltage systems, predictive maintenance compatibility, and compact modular architectures. Players are aggressively expanding production facilities, forming OEM partnerships, and investing in advanced polymer sealing technologies to strengthen lifecycle performance. High precision manufacturing requirements, semiconductor dependency, and certification complexity remain major entry barriers. Winning in this market now requires scale-efficient manufacturing, rapid customization capability, automation-ready engineering, and resilient supply-chain control.

Parker Hannifin Corporation

SMC Corporation

Emerson Electric Co.

Takasago Electric Industry Co., Ltd.

IMI plc

Danfoss

The Lee Company

CKD Corporation

Festo SE & Co. KG

ODE S.r.l.

GSR Ventiltechnik GmbH & Co. KG

CEME S.p.A.

Kendrion N.V.

The Micro Solenoid Water Valve Market is being reshaped by rapid advancements in low-voltage actuation systems, intelligent fluid-control architectures, and miniaturized precision engineering technologies. Current deployment trends strongly favor pulse-controlled electromagnetic valves capable of reducing energy consumption by nearly 18% while improving response precision by approximately 24%. More than 46% of newly integrated smart appliance and laboratory automation systems now use digitally controlled compact valve platforms optimized for predictive monitoring and low-noise operation.

Emerging technologies are increasingly centered around IoT-enabled diagnostics, AI-assisted flow optimization, and advanced polymer sealing systems designed for high-frequency switching environments. Intelligent monitoring integration reduced unplanned maintenance interruptions by nearly 17% across industrial fluid-control installations. Compared to legacy mechanical flow-control systems, next-generation digitally monitored valve platforms improve operational efficiency by approximately 28% while reducing leakage-related fluid loss significantly.

A major disruptive shift involves the integration of ultra-compact modular valve architectures within portable healthcare devices, beverage automation systems, and decentralized filtration platforms. Companies specializing in semiconductor-aligned automation ecosystems and predictive maintenance software integration are securing substantial competitive advantages through faster system interoperability and lifecycle optimization. Manufacturers with advanced miniaturization and smart diagnostics capabilities are increasingly capturing premium industrial and healthcare demand segments.

Between 2026 and 2028, high-speed intelligent actuation systems and self-monitoring valve platforms are expected to redefine operational automation standards across smart infrastructure ecosystems. Companies acting early on digitally integrated compact valve technologies will secure stronger positioning as industries accelerate toward intelligent, low-maintenance, and highly efficient fluid-management environments.

February 2025 – Parker Hannifin introduced the upgraded DFplus Generation IV pilot valve platform with up to 30% faster response times, improving process stability and reducing industrial scrap rates across automated fluid-control systems. The launch strengthened Parker’s position in high-speed precision valve applications. [Response-Speed Upgrade] Source: www.valveuser.com

April 2025 – Parker Hannifin launched its new Parker Legris axial valve integrating actuation and control into a compact single-unit architecture for water-treatment and pneumatic systems. The redesign improved space efficiency and operational durability while simplifying automation integration across industrial applications. [Integrated Valve Design]

October 2025 – Bürkert unveiled a new generation of compact solenoid valves for automatic coffee machines at HOST Milan 2025, featuring tool-free maintenance architecture and optimized lifecycle performance for high-frequency beverage dispensing environments. The system targeted reduced downtime and faster servicing efficiency. [Tool-Free Maintenance]

October 2025 – Parker Hannifin announced the acquisition of Filtration Group Corporation in a USD 9.25 billion transaction to strengthen global filtration and fluid-control integration capabilities. The move expanded Parker’s industrial automation ecosystem and enhanced cross-platform flow-control infrastructure offerings globally. [Strategic Filtration Expansion]

The Micro Solenoid Water Valve Market Report provides comprehensive coverage across valve types, applications, end-user industries, regional demand structures, and emerging fluid-control technologies shaping next-generation automation ecosystems. The report analyzes key segments including normally closed, normally open, and specialty micro valve systems across industrial automation, medical diagnostics, smart appliances, beverage dispensing, and water-treatment applications. Geographic assessment spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with detailed evaluation of production concentration, adoption behavior, and infrastructure-driven deployment patterns.

The study delivers deep analytical coverage through demand distribution analysis, technology benchmarking, competitive positioning assessment, and operational adoption trends. More than 42% of market demand concentration, 46% manufacturing distribution patterns, and over 28% intelligent automation deployment shifts are evaluated to identify structural market transformation signals. The report also profiles leading manufacturers, innovation strategies, supply-chain positioning, and expansion activities influencing competitive intensity across precision fluid-control systems.

Special focus is placed on emerging technologies including IoT-enabled monitoring, low-voltage pulse-control systems, predictive maintenance integration, and advanced polymer sealing architectures expected to influence market evolution between 2026 and 2033. The report supports strategic decision-making for investment prioritization, product expansion, partnership development, regional manufacturing allocation, and competitive positioning within rapidly transforming intelligent fluid-management ecosystems.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 106.0 Million |

| Market Revenue (2033) | USD 194.7 Million |

| CAGR (2026–2033) | 7.9% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Bürkert Fluid Control Systems; Parker Hannifin Corporation; SMC Corporation; Emerson Electric Co.; Takasago Electric Industry Co., Ltd.; IMI plc; Danfoss; The Lee Company; CKD Corporation; Festo SE & Co. KG; ODE S.r.l.; GSR Ventiltechnik GmbH & Co. KG; CEME S.p.A.; Kendrion N.V. |

| Customization & Pricing | Available on Request (10% Customization Free) |