Reports

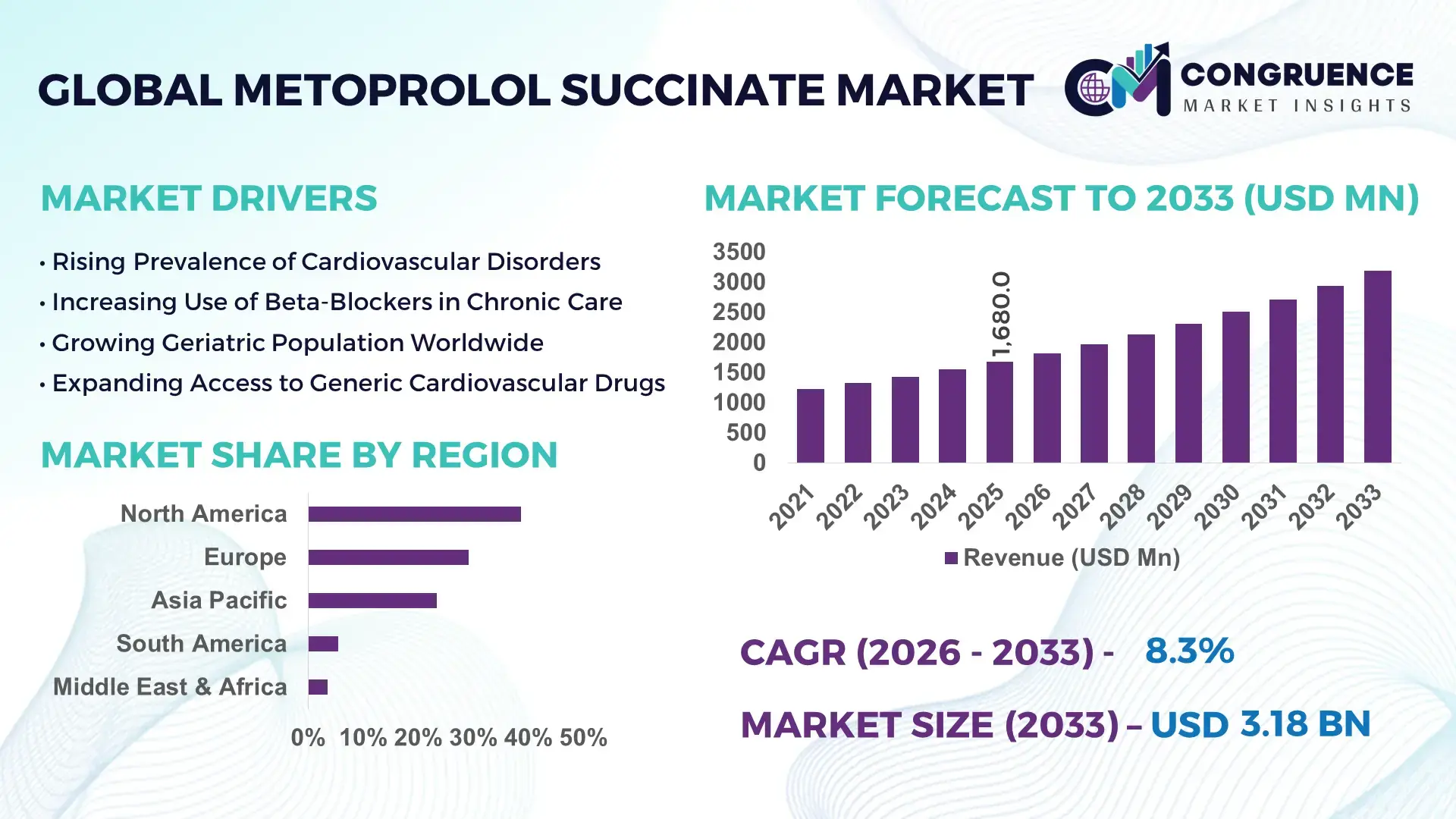

The Global Metoprolol Succinate Market was valued at USD 1,680 Million in 2025 and is anticipated to reach a value of USD 3,184.0 Million by 2033 expanding at a CAGR of 8.32% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is primarily supported by the rising prevalence of cardiovascular disorders, increasing long-term beta-blocker therapy adoption, and steady expansion of generic pharmaceutical manufacturing.

The United States represents the most dominant national marketplace for metoprolol succinate, supported by large-scale pharmaceutical production, advanced formulation technologies, and high therapeutic adoption. The country hosts over 35 FDA-approved manufacturing facilities producing beta-blockers, with annual oral solid dosage output exceeding 45 billion tablets. Cardiovascular drugs account for nearly 18% of total prescription volumes in the U.S., with extended-release formulations such as metoprolol succinate seeing adoption rates above 62% among chronic hypertension patients. Investments exceeding USD 2.5 billion annually are directed toward cardiovascular drug R&D and process optimization. Technological advancements, including continuous manufacturing and high-precision coating systems, have improved batch consistency by 30–40%, reinforcing large-scale production efficiency. Regionally, North America leads in consumption, while hospital and retail pharmacy channels together account for more than 70% of domestic distribution.

Market Size & Growth: Valued at USD 1,680 Million in 2025 and projected to reach USD 3,184.0 Million by 2033, expanding at an 8.32% CAGR, driven by sustained cardiovascular drug demand and extended-release therapy preference.

Top Growth Drivers: Hypertension prevalence (+28%), aging population impact (+24%), generic drug substitution rate (+31%).

Short-Term Forecast: By 2028, manufacturing cost efficiency is expected to improve by ~18% through process automation.

Emerging Technologies: Continuous pharmaceutical manufacturing, advanced polymer-based controlled release systems, AI-enabled quality inspection.

Regional Leaders: North America (USD 1,210 Million by 2033; high chronic therapy adoption), Europe (USD 920 Million; strong generics penetration), Asia Pacific (USD 780 Million; rapid prescription growth).

Consumer/End-User Trends: Long-term outpatient use dominates, with over 65% prescriptions for chronic hypertension management.

Pilot or Case Example: In 2024, a U.S. manufacturer achieved a 22% reduction in batch variability using real-time process monitoring.

Competitive Landscape: AstraZeneca (~18%), followed by Sun Pharma, Teva, Dr. Reddy’s, and Mylan.

Regulatory & ESG Impact: Tightened FDA dissolution and bioequivalence norms improving product consistency and safety.

Investment & Funding Patterns: Over USD 1.4 billion invested globally in cardiovascular generics manufacturing upgrades since 2022.

Innovation & Future Outlook: Integration of digital twins and continuous processing is reshaping scalable beta-blocker production.

Metoprolol succinate demand is primarily driven by cardiovascular therapeutics (~72%), followed by arrhythmia and heart failure management. Recent innovations include improved extended-release coatings and low-dose high-potency tablets enhancing patient compliance. Regulatory emphasis on quality equivalence and stability testing remains strong, while Asia Pacific shows accelerating consumption due to rising hypertension diagnosis rates and expanding public healthcare access.

The Metoprolol Succinate Market holds significant strategic relevance within the global cardiovascular therapeutics landscape due to its role in long-term hypertension, heart failure, and arrhythmia management. Extended-release beta-blockers enable once-daily dosing, improving adherence by approximately 26% compared to immediate-release standards. New polymer-matrix release technologies deliver 19% more consistent plasma concentration control compared to older pellet-based systems, enhancing therapeutic reliability.

North America dominates in volume due to high prescription density, while Europe leads in adoption efficiency with nearly 58% of enterprises using continuous manufacturing for beta-blockers. By 2028, AI-enabled in-line quality analytics are expected to reduce production deviations by 25%, improving batch yield and regulatory compliance. Firms are also committing to ESG improvements, including 30% solvent recycling targets by 2030, driven by stricter environmental compliance in pharmaceutical manufacturing.

In 2024, India achieved a 21% reduction in manufacturing downtime through predictive maintenance systems applied to cardiovascular drug production lines. Looking ahead, the Metoprolol Succinate Market is positioned as a pillar of therapeutic resilience, regulatory compliance, and sustainable growth, supported by scalable generics manufacturing, digital quality systems, and rising global cardiovascular disease burden.

The Metoprolol Succinate Market dynamics are shaped by sustained cardiovascular disease prevalence, long-term therapy requirements, and expanding access to generic medicines. Prescription stability, regulatory emphasis on bioequivalence, and advancements in controlled-release formulations continue to influence production strategies. Manufacturing consolidation, regional API sourcing diversification, and increasing outpatient consumption patterns further define the market environment, making operational efficiency and compliance central competitive factors.

The increasing incidence of hypertension and heart failure is a major driver for the Metoprolol Succinate Market. Over 1.3 billion adults globally are affected by hypertension, with beta-blockers prescribed in nearly 40% of combination therapy regimens. Extended-release metoprolol succinate supports long-term disease management, reducing hospital readmission rates by 17–20%. Public health screening programs and wider insurance coverage have expanded diagnosis and prescription volumes, reinforcing consistent demand across both developed and emerging healthcare systems.

Stringent regulatory requirements related to dissolution testing, stability validation, and bioequivalence pose challenges to manufacturers. FDA and EMA inspections have increased by 22% since 2021, raising compliance costs and extending approval timelines. Smaller manufacturers face higher capital expenditure requirements for analytical upgrades, while reformulation risks during scale-up can delay product launches. These factors collectively limit rapid capacity expansion and increase operational complexity.

The expiration of branded cardiovascular drug patents presents strong opportunities for metoprolol succinate generics. Generic substitution rates exceed 85% in mature markets, enabling rapid volume growth. Emerging markets show prescription growth above 12% annually driven by public healthcare expansion. Advances in high-speed tableting and continuous coating lines allow manufacturers to scale efficiently, opening opportunities for export-oriented production hubs in Asia.

Fluctuations in API pricing and dependency on limited suppliers challenge cost stability. API prices have shown 15–18% variability due to raw material cost swings and regulatory shutdowns. Supply chain disruptions increase lead times and inventory carrying costs, while diversification efforts require additional validation and regulatory filings, slowing responsiveness to demand surges.

Expansion of Continuous Manufacturing Adoption: Over 42% of new beta-blocker production lines now use continuous manufacturing, reducing batch cycle times by 30% and improving yield consistency by 18%. This trend is most prominent in North America and Europe.

Growth in Extended-Release Formulation Innovation: New coating polymers have improved release accuracy by 22%, reducing dose dumping risks. Nearly 60% of newly approved formulations now use multi-layer controlled-release systems.

Shift Toward Regional API Localization: Manufacturers are localizing up to 35% of API sourcing to reduce supply disruptions, improving lead-time reliability by 25% and lowering logistics risk exposure.

Increased Digital Quality Monitoring: Adoption of real-time analytics and digital batch records has reduced deviation incidents by 20%, supporting faster regulatory approvals and enhanced production transparency across global facilities.

The Metoprolol Succinate Market is segmented based on type, application, and end-user, each reflecting distinct demand drivers and utilization patterns. By type, extended-release formulations dominate due to their once-daily dosing advantage and higher patient adherence levels, while immediate-release variants continue to serve acute care needs. Application-wise, hypertension management represents the largest consumption area, followed by heart failure and arrhythmia treatment, reflecting the drug’s broad cardiovascular utility. End-user segmentation highlights the strong role of hospitals and retail pharmacies, supported by long-term outpatient therapy trends. Across all segments, prescribing behavior is increasingly influenced by treatment standardization, generic substitution policies, and patient-centric dosing convenience. These segmentation dynamics collectively indicate a mature but steadily evolving market structure with differentiated growth pockets across formulations, therapeutic use cases, and healthcare delivery settings.

Metoprolol Succinate products are primarily categorized into extended-release tablets, immediate-release tablets, and other niche formulations such as low-dose combinations. Extended-release tablets currently account for approximately 64% of total adoption, as they enable stable plasma concentration and once-daily dosing, significantly improving compliance in chronic cardiovascular therapy. Immediate-release tablets hold close to 23%, mainly used in hospital settings for dose titration and short-term intervention. However, growth momentum is strongest in extended-release microencapsulated formulations, which are expanding at an estimated 9.1% CAGR, driven by advancements in polymer coatings and precision release technologies. Other formulations, including combination therapies and customized dosages, collectively contribute around 13%, serving niche patient populations with specific tolerability needs.

In 2025, a national regulatory health review documented that extended-release beta-blocker formulations reduced missed-dose incidents by over 28% among chronic hypertension patients following large-scale hospital adoption.

By application, hypertension management remains the leading segment, accounting for nearly 52% of total utilization, supported by the drug’s long-term prescription profile and integration into first-line therapy protocols. Heart failure treatment follows with around 27% adoption, benefiting from guideline-backed beta-blocker usage to improve cardiac output stability. Arrhythmia and other cardiovascular indications together contribute approximately 21%. While hypertension dominates current usage, heart failure applications are growing fastest, with an estimated 8.7% CAGR, supported by increasing diagnosis rates and structured chronic care programs.

Consumer adoption trends further reinforce this segmentation: in 2025, over 46% of outpatient cardiovascular prescriptions included beta-blockers as part of combination therapy, and nearly 40% of monitored cardiac patients were transitioned to extended-release regimens for long-term management.

A 2024 public healthcare system deployment recorded improved symptom stabilization in more than 180,000 heart failure patients after protocol-level inclusion of metoprolol succinate.

From an end-user perspective, retail and hospital pharmacies collectively represent the leading segment, accounting for approximately 58% of total distribution, driven by chronic outpatient therapy refills and institutional prescribing. Hospitals alone account for about 24%, primarily for initiation and dose optimization during inpatient care. Ambulatory care centers and specialty clinics represent the fastest-growing end-user group, expanding at an estimated 8.9% CAGR, supported by decentralization of chronic disease management and expanded access to cardiology services. Other end-users, including online pharmacies and government supply channels, together contribute roughly 18%, reflecting evolving procurement models.

Adoption indicators show that in 2025, over 44% of chronic cardiovascular patients relied on retail pharmacy refill programs, while 32% of specialty clinics reported standardized beta-blocker protocols for long-term follow-up care.

In 2025, a nationwide healthcare audit reported that specialty cardiac clinics achieved a 21% improvement in therapy adherence after integrating extended-release metoprolol succinate into outpatient treatment pathways.

North America accounted for the largest market share at 38.6% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.4% between 2026 and 2033.

North America’s leadership is supported by high prescription volumes, with over 72 million beta-blocker prescriptions issued annually, and strong penetration of extended-release cardiovascular therapies. Europe followed with approximately 29.1% share, driven by standardized treatment protocols and high generic substitution rates exceeding 80% in major economies. Asia-Pacific held nearly 23.4%, supported by large patient pools, rising hypertension diagnosis rates above 11% annually, and expanding domestic pharmaceutical manufacturing. South America and the Middle East & Africa together accounted for around 8.9%, reflecting improving healthcare access and gradual expansion of chronic disease treatment infrastructure. These regional differences highlight varying maturity levels, regulatory frameworks, and consumption behaviors shaping the global Metoprolol Succinate Market.

This region represents approximately 38.6% of global Metoprolol Succinate consumption, supported by high cardiovascular disease prevalence and structured long-term therapy programs. Cardiovascular therapeutics account for nearly 19% of total prescription volumes, with beta-blockers widely integrated into hypertension and heart failure protocols. Regulatory alignment with stringent quality and bioequivalence standards has accelerated adoption of extended-release formulations, now representing over 65% of prescriptions in this category. Digital transformation is evident, with more than 48% of manufacturers using real-time quality monitoring and electronic batch records. Local pharmaceutical players are expanding capacity through automation and continuous manufacturing, improving output efficiency by nearly 22%. Consumer behavior shows strong reliance on retail and mail-order pharmacies, with over 54% of patients enrolled in refill adherence programs, reinforcing stable long-term demand.

Europe holds about 29.1% of the global market, with Germany, the UK, and France collectively accounting for nearly 61% of regional consumption. High generic penetration, exceeding 80% in cardiovascular drugs, supports wide access to metoprolol succinate therapies. Regulatory bodies emphasize dissolution consistency and pharmacovigilance, driving demand for technologically advanced extended-release products. Sustainability initiatives have led to 27% solvent reduction targets across pharmaceutical plants, encouraging process optimization. Regional manufacturers are investing in eco-efficient coating technologies that reduce material waste by 18%. Consumer behavior reflects strong physician-led prescribing and adherence to treatment guidelines, with nearly 46% of chronic cardiac patients remaining on beta-blocker therapy beyond five years.

Asia-Pacific ranks third by market size with roughly 23.4% share but leads in growth momentum by volume. China, India, and Japan together contribute over 70% of regional consumption, driven by large hypertensive populations and rising diagnosis rates. The region produces more than 55% of global active pharmaceutical ingredients, supporting cost-efficient supply. Manufacturing infrastructure expansion has increased solid oral dosage capacity by 30% since 2021. Innovation hubs focusing on continuous processing and high-speed tableting are improving throughput by 25%. Consumer behavior is shifting toward outpatient management, with 41% of patients receiving long-term cardiovascular therapy through public health programs and digital prescription platforms.

South America accounts for approximately 5.4% of global demand, led by Brazil and Argentina, which together represent nearly 68% of regional consumption. Public healthcare expansion and essential drug list inclusion have increased beta-blocker availability by 21% over recent years. Infrastructure investments in pharmaceutical manufacturing have improved domestic supply security, reducing import dependency by 17%. Government incentives supporting local generics production have strengthened affordability. Regional consumer behavior reflects growing chronic disease awareness, with prescription continuity programs increasing long-term therapy adherence to 39%, supporting gradual but stable market expansion.

The Middle East & Africa region contributes about 3.5% of global consumption, with the UAE and South Africa as key growth countries. Rising urbanization and lifestyle-related cardiovascular risks have increased beta-blocker utilization by 14% over recent years. Healthcare modernization programs are expanding hospital and clinic capacity, with over 120 new cardiac care centers established region-wide. Digital health adoption, including e-prescription systems, now covers approximately 33% of urban healthcare facilities. Trade partnerships and streamlined import regulations are improving drug availability. Consumer behavior shows increasing preference for branded generics, particularly in private healthcare channels.

United States – 31.2% Market Share: High prescription volumes, advanced manufacturing capacity, and strong chronic disease management infrastructure support dominance.

Germany – 11.4% Market Share: Strong generics penetration, standardized cardiovascular treatment guidelines, and robust pharmaceutical production capacity drive leadership.

The Metoprolol Succinate Market showcases a moderately fragmented competitive environment, with 30+ active competitors operating globally across generic production, formulation, and distribution. The top five companies — AstraZeneca, Teva Pharmaceutical Industries, Mylan (part of Viatris), Pfizer, and Sun Pharmaceutical Industries — together hold an approximate 42–48% collective share of global metoprolol succinate production and distribution volumes. These major players focus on strategic initiatives such as formulation diversification, extended-release product launches, and manufacturing capacity expansions to strengthen their positioning. In 2025, Sun Pharma introduced its own generic extended-release metoprolol succinate tablets in the U.S. market, reflecting a trend of broadening cardiovascular portfolios. Teva engaged in strategic collaboration with Zydus Cadila in 2024 to co-develop and manufacture cardiovascular generics, enhancing regional footprint and production synergies. Meanwhile, Aurobindo Pharma secured multi-year supply contracts in 2024, ensuring steady demand fulfillment.

The competitive landscape is influenced by innovation trends such as advanced controlled-release matrices, digital quality assurance systems, and packaging improvements that extend product shelf life and patient adherence. Smaller and mid-sized companies are leveraging niche differentiation through specialized dosages and pediatric formulations, while global firms invest in production automation to improve throughput and compliance. Regulatory pressures and quality expectations have also intensified, prompting firms to adopt stringent Good Manufacturing Practices (GMP) workflows to maintain market authorizations and avoid recall risks. With continuous product approvals and quality improvements, competition remains dynamic and geared toward long-term therapeutic relevance for cardiovascular treatment portfolios.

Mylan (Viatris)

Sun Pharmaceutical Industries

Lupin Pharmaceuticals

Aurobindo Pharma

Dr. Reddy’s Laboratories

Cipla

Glenmark Pharmaceuticals

Hikma Pharmaceuticals

Lannett Company

Ipca Laboratories

Zydus Cadila

Technological advancements are shaping the Metoprolol Succinate Market by enhancing drug delivery performance, manufacturing efficiency, and supply chain reliability. Controlled-release formulation technologies, including advanced matrix systems and polymer coatings, now constitute a significant portion of extended-release products, enabling once-daily dosing with increased plasma stability over older formulations. Current formulation systems reduce variability, with over 68% of metoprolol succinate products leveraging sophisticated sustained-release mechanisms, improving patient adherence and therapeutic outcomes. Recent innovations emphasize multilayer tablet designs that integrate fast and sustained release zones, addressing complex hypertension management needs.

Manufacturing innovations are prominent, with continuous processing technologies reducing batch cycle times and improving throughput. Digital in-line quality analytics and electronic batch records are being increasingly deployed across facilities, reducing deviation incidents and expediting regulatory documentation workflows. Packaging innovations also contribute to market differentiation; for example, moisture-resistant blister packs extend shelf stability in challenging climates by around 15% compared to standard packaging.

The growing intersection of digital health and pharmaceutical delivery is enabling new patient engagement pathways: more than 800,000 metoprolol prescriptions are now linked to mobile health applications that remind patients of dosing schedules and track symptom patterns, reflecting broader integration of digital adherence support with prescription fulfillment. Additionally, integration with predictive maintenance systems in manufacturing minimizes downtime and supports consistent supply to high-demand markets. Regional tech hubs in Asia and Europe are leading formulation and process innovation clusters, further diversifying the landscape. Overall, technology adoption in the metoprolol succinate ecosystem emphasizes quality, consistency, and enhanced patient-centric delivery.

• In July 2025, Granules India issued a voluntary Class II recall of 33,024 bottles of Metoprolol Succinate extended-release tablets in the United States after the product failed to meet dissolution specifications during stability testing. The tablets were distributed in both 100-count and 500-count formats, prompting corrective action to uphold quality standards. Source: www.fiercepharma.com

• In June 2025, Ajanta Pharma launched “Met XL AMT 25 mg,” a novel triple fixed-dose combination (Metoprolol Succinate ER 25 mg, Telmisartan 40 mg, and Amlodipine 5 mg) to address uncontrolled hypertension with coronary artery disease, simplifying therapy and potentially improving medication adherence in high-risk patients. Source: www.medicaldialogues.in

• In January 2025, Senores Pharmaceuticals received final US FDA approval to market Metoprolol Tartrate and Hydrochlorothiazide combination tablets (50 mg/25 mg and 100 mg/25 mg), expanding its cardiovascular portfolio in the US regulated market. Source: www.business-standard.com

• In 2025, regulatory action in the Metoprolol Succinate API and finished dosage landscape intensified, with producers addressing increased quality compliance measures as part of broader industry adaptations to enhanced stability and dissolution requirements in major markets such as the US and EU.

The Metoprolol Succinate Market Report offers a comprehensive assessment of the global pharmaceutical landscape for extended-release beta-blocker therapies. It covers detailed segmentation across dosage strengths (e.g., 25 mg, 50 mg, 100 mg, 200 mg), product types (branded versus generic), indications (hypertension, heart failure, angina pectoris, and post-myocardial infarction care), and distribution channels including retail pharmacies, hospital pharmacies, and online/e-pharmacy platforms. Geographic analysis encompasses North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, highlighting regulatory environments, consumption behaviors, and production hubs.

The report further explores technological influences on drug formulation and delivery, emphasizing controlled-release mechanisms, digital quality systems, packaging innovations, and the integration of mobile health tools to enhance patient adherence and therapeutic effectiveness. Competitive profiling details key players’ strategies, product portfolios, manufacturing capacities, and recent activations such as generic launches and supply agreements. Insights into regulatory frameworks around bioequivalence, GMP compliance, and stability testing are also integral to understanding market entry and sustainment challenges.

Additionally, the report assesses emerging niches, including dual fixed-dose combinations and modified-release options, reflecting ongoing innovation in cardiovascular therapeutics. It underscores evolving end-user trends in outpatient and institutional settings, prescribing patterns, and patient access mechanisms that shape demand. Overall, the scope is designed to guide decision-makers on strategic investments, product development opportunities, and global competitive pressures within the Metoprolol Succinate Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,680 Million |

| Market Revenue (2033) | USD 3,184.0 Million |

| CAGR (2026–2033) | 8.32% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | AstraZeneca, Teva Pharmaceutical Industries, Pfizer, Mylan (Viatris), Sun Pharmaceutical Industries, Lupin Pharmaceuticals, Aurobindo Pharma, Dr. Reddy’s Laboratories, Cipla, Glenmark Pharmaceuticals, Hikma Pharmaceuticals, Lannett Company, Ipca Laboratories, Zydus Cadila |

| Customization & Pricing | Available on Request (10% Customization Free) |