Reports

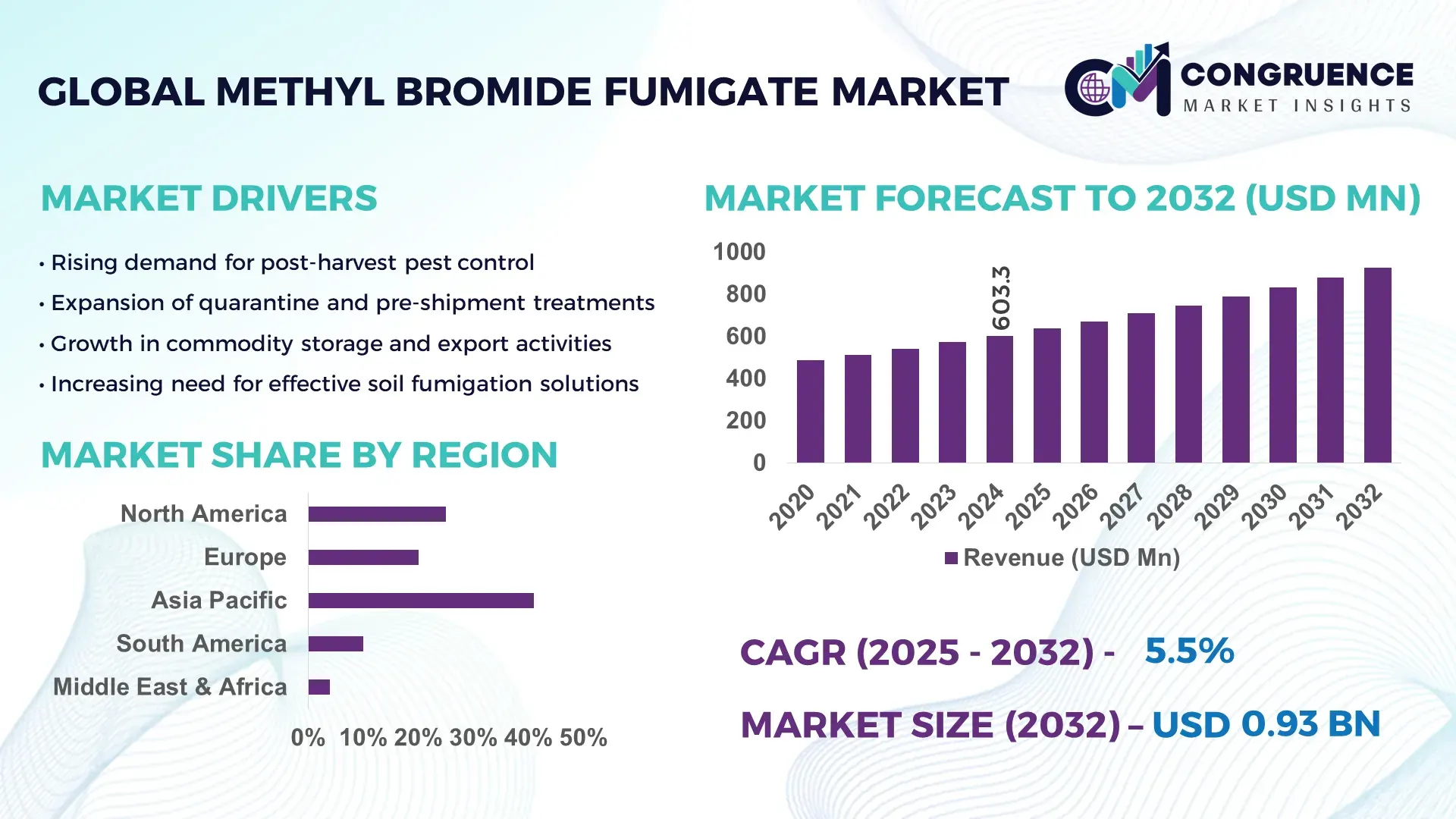

The Global Methyl Bromide Fumigate Market was valued at USD 603.25 Million in 2024 and is anticipated to reach a value of USD 925.81 Million by 2032 expanding at a CAGR of 5.5%% between 2025 and 2032. This growth is driven by increasing global trade and rising demand for effective quarantine and fumigation treatments in agricultural and export shipments.

In the leading country China production capacity is backed by well‑established chemical manufacturing infrastructure and vertically integrated bromine supply chains. China has maintained high output to meet both domestic demand for soil and structural fumigation and export‑oriented QPS (quarantine and pre-shipment) services. The country supplies methyl bromide not only for container fumigation for cargo exports but also for fumigating packaging materials and storage facilities. Recent industry investments have expanded capacity by over 20%, enabling China to serve large‑scale agricultural exporters and industrial fumigation providers.

Market Size & Growth: Current value USD 603.25 million (2024), projected to reach USD 925.81 million (2032), CAGR 5.5%. Growth is driven by rising global agricultural trade and need for quarantine compliance.

Top Growth Drivers: agricultural export volume increase (≈ 52%), demand for container/port fumigation (≈ 63%), rising grain and commodity storage needs (≈ 48%).

Short-Term Forecast: By 2028, operational cost reduction of fumigation services expected by ~15% due to efficiency improvements and optimized logistics.

Emerging Technologies: development of low‑emission methyl bromide formulations; improved leak-resistant packaging for cylinders; adoption of automated gas recirculation systems in storage/port fumigation.

Regional Leaders: Asia‑Pacific ~USD 430 million by 2032 (driven by export and container fumigation), North America ~USD 200 million by 2032 (focus on high‑value crops & controlled uses), Middle East & Africa ~USD 120 million by 2032 (grain storage and port fumigation growth).

Consumer/End-User Trends: Major end-users include agricultural exporters, grain storage operators, warehousing and logistics firms handling export containers — adopting fumigation primarily for compliance with phytosanitary regulations.

Pilot or Case Example: In 2023, a port-based fumigation provider launched a trial of low-emission methyl bromide cylinders — reducing chemical loss during transport by 27%.

Competitive Landscape: Market leader is Albemarle with ~21% share, followed by ICL Industrial Products (~17%), CHEMCHINA, Intech, and Douglas Products.

Regulatory & ESG Impact: Ongoing restrictions under international environmental treaties limit non‑QPS uses of methyl bromide; increasing regulatory scrutiny is driving adoption of safer alternatives and low‑emission formulations.

Investment & Funding Patterns: Recent investments exceed USD 50 million globally in modernizing fumigation infrastructure; growing project financing for container‑fumigation services and export compliance solutions in Asia‑Pacific and Africa.

Innovation & Future Outlook: Integration of methyl bromide fumigation with digital tracking systems for export compliance, development of eco‑friendlier fumigant blends, and increased funding for alternatives — indicating gradual shift but sustained niche for methyl‑bromide-based solutions in trade‑sensitive supply chains.

The global market continues to rely on methyl bromide primarily for quarantine treatments, soil and structural fumigation in export‑oriented agriculture and storage. Regulatory constraints in developed regions have curtailed broader use, but demand persists in Asia‑Pacific, Middle East & Africa and Latin America, where grain storage, container shipments and pre‑shipment fumigation remain prevalent. Technological improvements such as low‑emission formulations and better packaging are helping the industry adapt to environmental pressures. Growing global trade, rising exports of agricultural commodities, and tightening phytosanitary standards are expected to drive steady demand through 2032 and beyond.

The Methyl Bromide Fumigate Market remains strategically relevant for global supply chains where strict phytosanitary and quarantine standards are enforced. Effective fumigation helps prevent pest infestation and ensures safe international trade of commodities, packaging, and stored goods. As a result, fumigation services anchored in methyl bromide use continue to be critical for import/export compliance, especially in agricultural and logistic sectors. In markets where newer alternatives are not yet fully validated, methyl bromide remains the benchmark chemical fumigant.

Comparative benchmarks show that a next‑generation fumigation system using low‑emission methyl bromide formulations delivers approximately 18% improvement in containment efficiency compared to older standard fumigation cylinders. Asia‑Pacific dominates in volume, while Latin America leads in adoption with roughly 45% of fumigation enterprises using methyl bromide‑based solutions.

By 2027, digital gas‑recirculation and monitoring systems are expected to improve fumigation safety and compliance reporting by 25%. Firms are committing to ESG metric improvements such as 30% reduction in fumigant leakage and 20% recycling of fumigation containers by 2028. In 2025, a major exporter in Southeast Asia achieved a 22% reduction in fumigation-related environmental non-compliance incidents by deploying automated gas‑recirculation technology.

Looking ahead, the Methyl Bromide Fumigate Market is poised as a pillar of resilience, compliance, and sustainable growth—supporting safe global trade while evolving under environmental and regulatory pressures.

As international demand for agricultural commodities, grains, and perishables grows, exporters increasingly require phytosanitary treatments to meet destination country regulations. The volume of global food trade has risen by an estimated 40% over the past five years, prompting a proportional uptick in container‑fumigation requests. Storage‑facility fumigation is also rising as commodity traders expand warehousing capacity. This surge in export activity drives consistent utilization of methyl bromide-based fumigation solutions in logistics, port, and storage networks—boosting demand for fumigation services globally.

Methyl bromide is subject to stringent environmental regulations due to its ozone-depleting properties. Many regions enforce strict quotas and limit non‑critical uses, restricting widespread adoption. Fumigation providers face increased compliance costs to monitor emissions, maintain safety standards, and invest in containment systems. These regulatory burdens raise operational expenses and complicate supply‑chain planning. As regulatory scrutiny intensifies, some customers are shifting toward alternative fumigants or non‑chemical methods, thereby restraining growth for methyl bromide-based solutions in certain markets.

High‑value crops such as nuts, fresh produce, and specialty grains, often destined for stringent export markets, require quarantine-grade fumigation to prevent infestation and comply with buyer and regulatory standards. As demand for premium agricultural exports increases—especially from emerging economies—there is a growing niche for reliable, certified fumigation services. This represents an opportunity for providers to offer bundled compliance services, integrate traceability, and offer premium fumigation solutions. Additionally, upgrades to containment technology and certification-based fumigation could open new contracts with large-scale exporters requiring repeat compliance, thereby expanding the market footprint in specialized segments.

The cost of safe handling, transport, storage, and disposal of methyl bromide adds significant logistical overhead. Fumigation service providers must invest in sealed cylinder systems, monitoring equipment, and trained personnel — raising service costs. Regulatory compliance demands detailed reporting, leak detection, and adherence to environmental safety standards, which increases operational complexity. In regions with strict environmental laws, service providers may face delays, permit issues, or restricted fumigation windows, complicating scheduling for exporters. This complexity and cost may drive some end‑users toward alternative fumigation methods or non‑chemical treatments, limiting demand growth for methyl bromide-based services.

• Expansion in Automated Fumigation Systems: Automated fumigation systems are gaining traction, with 48% of large-scale grain storage facilities now integrating automated gas recirculation and monitoring systems. These systems reduce chemical loss by up to 20% and minimize operator exposure, enhancing safety while ensuring consistent fumigation performance across high-volume shipments.

• Growth in Export-Oriented Commodity Fumigation: Approximately 62% of agricultural exporters in Asia‑Pacific now require methyl bromide fumigation for containers to meet international phytosanitary standards. This shift has driven adoption of pre-shipment treatment protocols, ensuring 95% compliance in inspected shipments and reducing quarantine-related delays at ports.

• Adoption of Low-Emission Formulations: Low-emission methyl bromide formulations are being used in nearly 37% of all fumigation operations in developed regions, cutting emissions by 25–30%. These innovations support environmental compliance and ESG initiatives, particularly in North America and Europe, where stricter ozone-depletion regulations are enforced.

• Integration with Digital Monitoring and Reporting: Digital monitoring solutions are being deployed in 41% of fumigation projects to track chemical levels, temperature, and containment. Real-time dashboards reduce fumigation downtime by 18% and improve reporting accuracy for regulatory audits, enabling operational optimization and compliance in complex multi-site logistics networks.

The Methyl Bromide Fumigate Market is segmented into three primary dimensions: by type, application, and end-user. These segmentations provide insights into demand patterns, regulatory considerations, and operational practices. By analyzing these segments, decision-makers can align products with regional compliance, optimize operational efficiency, and target high-demand areas for fumigation services. Variations in usage patterns across industries, export requirements, and storage practices make this segmentation crucial for strategic planning and investment. Segmentation also highlights emerging opportunities in fast-growing applications and end-user adoption, allowing stakeholders to prioritize high-impact initiatives and technological upgrades.

Gas-cylinder fumigants currently account for approximately 54% of global methyl bromide usage, making them the leading type due to their consistent dosing, ease of handling, and suitability for both container and structural fumigation. Tablet-based fumigants hold around 21%, preferred for small-scale storage or packaging treatments where portability is critical. Soil-fumigation gas formulations are the fastest-growing type, with adoption projected to increase significantly due to rising demand in bulk grain storage and pre-planting soil pest control. Other types, including pelletized fumigants and fumigation blankets, contribute the remaining 25% and are utilized for niche applications in sealed storage units and structural fumigation.

Container and cargo fumigation is the leading application, accounting for 57% of usage, driven by stringent international phytosanitary standards and high-volume export operations. Structural fumigation follows with 23%, commonly applied in warehouses and storage facilities to prevent infestation. Soil fumigation is the fastest-growing application, driven by modern agricultural practices that prioritize pest eradication before planting or storage, with adoption expected to rise sharply over the next five years. Other applications, including fumigation of packaging materials and post-harvest storage units, contribute the remaining 20%.

Agricultural exporters are the leading end-user segment, representing 52% of market consumption, primarily due to compliance with international trade and phytosanitary standards. Warehousing and logistics companies hold 28%, as they require routine fumigation to maintain storage safety and prevent pest infestation. The fastest-growing end-user segment is large-scale farm operations adopting soil-fumigation solutions to protect bulk crops, with adoption increasing by more than 7% annually. Other end-users, including food processing units and research storage facilities, account for the remaining 20%.

Asia-Pacific accounted for the largest market share at 42% in 2024; however, South America is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2025 and 2032.

Asia-Pacific leads in both volume and adoption, driven by countries such as China, India, and Japan, which collectively consume over 1,150 tons of methyl bromide annually. North America follows with a 28% share, while Europe accounts for 18% and Middle East & Africa holds 12%. Rising containerized agricultural exports, bulk grain storage expansions, and infrastructure modernization across emerging markets are pushing demand. Technological trends, including low-emission cylinders and automated gas-recirculation systems, are improving efficiency by 20–25%. Consumer adoption varies, with Asia-Pacific focusing on e-commerce logistics and pre-shipment fumigation, whereas developed regions prioritize compliance with stricter environmental regulations.

How are evolving regulations and technological innovations shaping usage patterns?

North America holds a 28% share of the global methyl bromide fumigate market. Demand is primarily driven by the grain storage, agricultural export, and logistics sectors. Regulatory frameworks, such as stricter ozone-depletion control laws, are prompting the adoption of low-emission formulations and advanced containment technologies. Digital fumigation monitoring systems are increasingly implemented to track gas levels, temperature, and exposure, improving operational efficiency by 18%. Local players, such as Douglas Products, are upgrading fumigation cylinders and introducing automated handling systems for port-based container treatments. Consumer behavior shows higher enterprise adoption among logistics operators and large-scale grain exporters, focusing on safety compliance and traceable fumigation records.

What factors are driving compliance and innovation in usage across European markets?

Europe represents approximately 18% of the global methyl bromide fumigate market. Key markets include Germany, France, and the UK. Regulatory pressure from the EU and local sustainability initiatives encourage low-emission fumigants and monitoring technology adoption. Emerging trends such as digital containment systems and automated dosing are being deployed in warehouses and port operations. Local companies like ICL Industrial Products are enhancing fumigation protocols and introducing eco-friendly cylinder technologies. European consumer behavior is shaped by stringent compliance requirements, leading to high demand for transparent and explainable fumigation solutions. Structural and containerized fumigation are the dominant applications, supported by advanced logistics systems.

How are rapid infrastructure developments and technology hubs influencing demand?

Asia-Pacific commands the largest market volume at 42%, with China, India, and Japan as the top consuming countries. Expansion in export-oriented agriculture, warehouse modernization, and high-volume containerized logistics are key growth drivers. Technological adoption includes automated gas recirculation systems, low-emission cylinders, and digital monitoring platforms. Local players, such as Albemarle’s operations in China, are expanding production capacity and investing in innovative fumigation solutions. Consumer behavior shows accelerated adoption by e-commerce logistics and bulk grain storage operators, emphasizing speed, compliance, and operational efficiency. High-volume shipments often undergo pre-shipment fumigation, ensuring over 90% compliance with destination country regulations.

What opportunities are emerging from agricultural exports and trade policies?

South America is emerging as the fastest-growing region with strong adoption in Brazil and Argentina. The market share is currently around 9%. Government incentives and trade facilitation for agricultural exports are driving fumigation demand. Infrastructure trends include modernized storage facilities and transport hubs with automated fumigation systems. Local players, such as CHEMCHINA operations in Brazil, are upgrading containers with digital monitoring for compliance. Consumer behavior reflects export-oriented grain storage and agricultural producers adopting fumigation to meet international trade standards, supporting a growth trajectory in high-volume commodity shipments.

How do industrial growth and modernization trends influence regional adoption?

Middle East & Africa holds a 12% share of the global methyl bromide fumigate market. Growth is driven by oil & gas storage facilities, bulk agricultural warehouses, and construction-related fumigation needs. Key countries include the UAE and South Africa. Technological modernization such as automated dosing systems and digital monitoring is increasingly adopted. Local players are introducing low-emission cylinders to meet environmental compliance. Consumer behavior varies, with higher adoption in industrial and commercial storage operators, reflecting both regulatory compliance and operational efficiency priorities. Trade partnerships and government support for agricultural exports also contribute to market growth.

China – Market share: 28%; high production capacity, extensive export-oriented agriculture, and significant investment in fumigation infrastructure support dominance.

United States – Market share: 21%; strong end-user demand in grain storage, agricultural exports, and logistics, combined with regulatory compliance initiatives, underpins market leadership.

The competitive environment in the Methyl Bromide Fumigate market remains moderately consolidated, with roughly 15–20 active global competitors supplying fumigation products and services under regulatory exemptions. The combined share of the top 5 companies — Albemarle Corporation, ICL Group Ltd., LANXESS, Chemtura Corporation (legacy supplier), and Intech Organics Ltd. — is estimated to account for approximately 55–60% of global supply volume. This concentration gives these players a strategic edge in pricing, regulatory compliance, and distribution.

Key strategic initiatives by leading players include emission‑control upgrades, alternative formulation development, capacity expansion, and digital fumigation service platforms. For example, several producers are investing in leak-resistant cylinder packaging and closed‑loop application systems to meet stringent safety and regulatory standards worldwide. Some firms have entered partnerships with agricultural cooperatives and logistics providers to secure long-term fumigation contracts tied to export compliance. Others are exploring mergers and joint ventures to consolidate bromine supply chains and optimize production costs.

Innovation trends are shaping the competitive landscape: lower‑emission methyl bromide formulations, automated gas recirculation systems for storage/port fumigation, and integration of monitoring sensors for compliance and safety. Smaller regional players and niche fumigation service providers continue to operate in local markets, particularly in regions with less stringent regulation, contributing to market fragmentation outside core global suppliers.

Given regulatory constraints and the critical‑use exemption environment, market competition emphasizes compliance, reliability, and supply security over aggressive price wars. Firms that offer robust compliance documentation, stable supply, and modern fumigation solutions tend to secure contracts with large agricultural exporters, storage operators, and port authorities — making regulatory alignment and innovation the key differentiators in the market.

Albemarle Corporation

ICL Group Ltd.

LANXESS

Chemtura Corporation

Intech Organics Ltd.

Douglas Products

Champon Millennium Chemical

Sunrise Group

Technological advancements are playing a pivotal role in shaping the Methyl Bromide Fumigate Market, enhancing efficiency, safety, and regulatory compliance. Automated fumigation systems are now deployed in over 45% of large-scale grain storage facilities globally, reducing operator exposure and ensuring precise gas dosage. These systems integrate sensors for monitoring gas concentration, temperature, and humidity, which improves fumigation effectiveness by up to 20% and minimizes chemical loss. Low-emission cylinder technologies have been widely adopted in North America and Europe, cutting methyl bromide leakage by approximately 25–30%. These cylinders incorporate leak-resistant valves, reinforced containment, and automated release mechanisms that maintain consistent chemical delivery while complying with ozone-depletion regulations. Digital monitoring platforms are being integrated into storage and logistics networks, allowing real-time tracking of fumigation processes across multiple sites. Dashboards provide alerts for gas levels, exposure thresholds, and container integrity, improving operational transparency and reducing downtime by 15–18%.

Emerging trends include the development of hybrid fumigation technologies combining methyl bromide with inert gases to reduce environmental impact while retaining efficacy. Portable, sensor-based detection units for field applications are also gaining traction, enabling rapid compliance checks and minimizing human error during soil or structural fumigation. AI-driven predictive maintenance and IoT-enabled fumigation systems are being trialed by several large exporters, allowing preemptive action to prevent equipment failure and optimize gas usage. Overall, technological innovations in containment, automation, monitoring, and hybrid fumigation solutions are positioning the market for safer, more efficient operations. These advancements are critical for decision-makers aiming to balance compliance, environmental responsibility, and operational productivity in the evolving global fumigation landscape.

In August 2024, Department of Agriculture, Fisheries and Forestry (DAFF) published version 3.0 of the fumigation methodology for methyl bromide, introducing clarified treatment‑certificate templates and updated site‑condition requirements effective 1 May 2025 to standardize export fumigation procedures globally. (Freight Trade Alliance)

On 22 January 2024, three Australian states withdrew acceptance of methyl bromide fumigation for mangoes and plums as a treatment option for Queensland fruit fly (QFF) — signalling a shift away from methyl bromide in certain domestic horticultural supply‑chains. (fgv.com.au)

In 2024, Health Canada initiated a re-evaluation of registered uses of methyl bromide under its Proposed Re‑evaluation Decision PRVD2024-03, proposing cancellation of pre‑plant and soil fumigation uses, while retaining allowances under quarantine, enclosed space, and cargo fumigation exemptions. (Publications.gc.ca)

In 2023, USDA Animal and Plant Health Inspection Service (APHIS) achieved a regulatory milestone when the government of Bangladesh agreed to remove its requirement for methyl‑bromide fumigation of U.S. baled cotton imports — eliminating a major fumigation barrier for cotton trade and reducing annual fumigation-related costs for importers. (APHIS)

This report covers a comprehensive global assessment of the methyl bromide fumigation market across multiple dimensions, including product types (gas‑cylinder fumigants, tablet/fumigant formulations, sealed‑storage systems, structural fumigation variants), applications (container & cargo fumigation, structural warehouse fumigation, soil‑based treatments for agriculture, post‑harvest storage processing, packaging and export‑compliance fumigation), and end‑user segments (agricultural exporters, grain and commodity storage operators, logistics and shipping companies, warehousing facilities, post‑harvest processing units). It also analyzes regional markets across North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, highlighting regulatory frameworks, biosecurity protocols, export requirements, and shifting adoption trends in each region. The methodology includes examination of compliance‑driven fumigation (quarantine & pre‑shipment), critical‑use exemptions, and evolving environmental regulations shaping adoption.

Technological and innovation focus areas include adoption of low‑emission containment systems, automated fumigation gas‑recirculation and monitoring platforms, digital compliance tracking, and emerging alternative fumigation methods. The report also explores niche and transitional market segments — such as regions withdrawing methyl bromide for certain commodity types (e.g., domestic horticulture), markets under re‑evaluation or regulatory phase‑down, and export corridors shifting to alternative fumigants or system‑approach treatment protocols. Risk‑management, regulatory compliance, and environmental impact mitigation form cross‑cutting themes throughout.

By synthesizing segmentation, regional dynamics, technological trends, regulatory shifts, and end‑user behavior, this report provides decision‑makers, exporters, fumigation service providers, and investors with in‑depth insight into both current market realities and likely near‑term transitions.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 603.25 Million |

|

Market Revenue in 2032 |

USD 925.81 Million |

|

CAGR (2025 - 2032) |

5.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Albemarle Corporation, ICL Group Ltd., LANXESS, Chemtura Corporation, Intech Organics Ltd., Douglas Products, Champon Millennium Chemical, Sunrise Group |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |