Reports

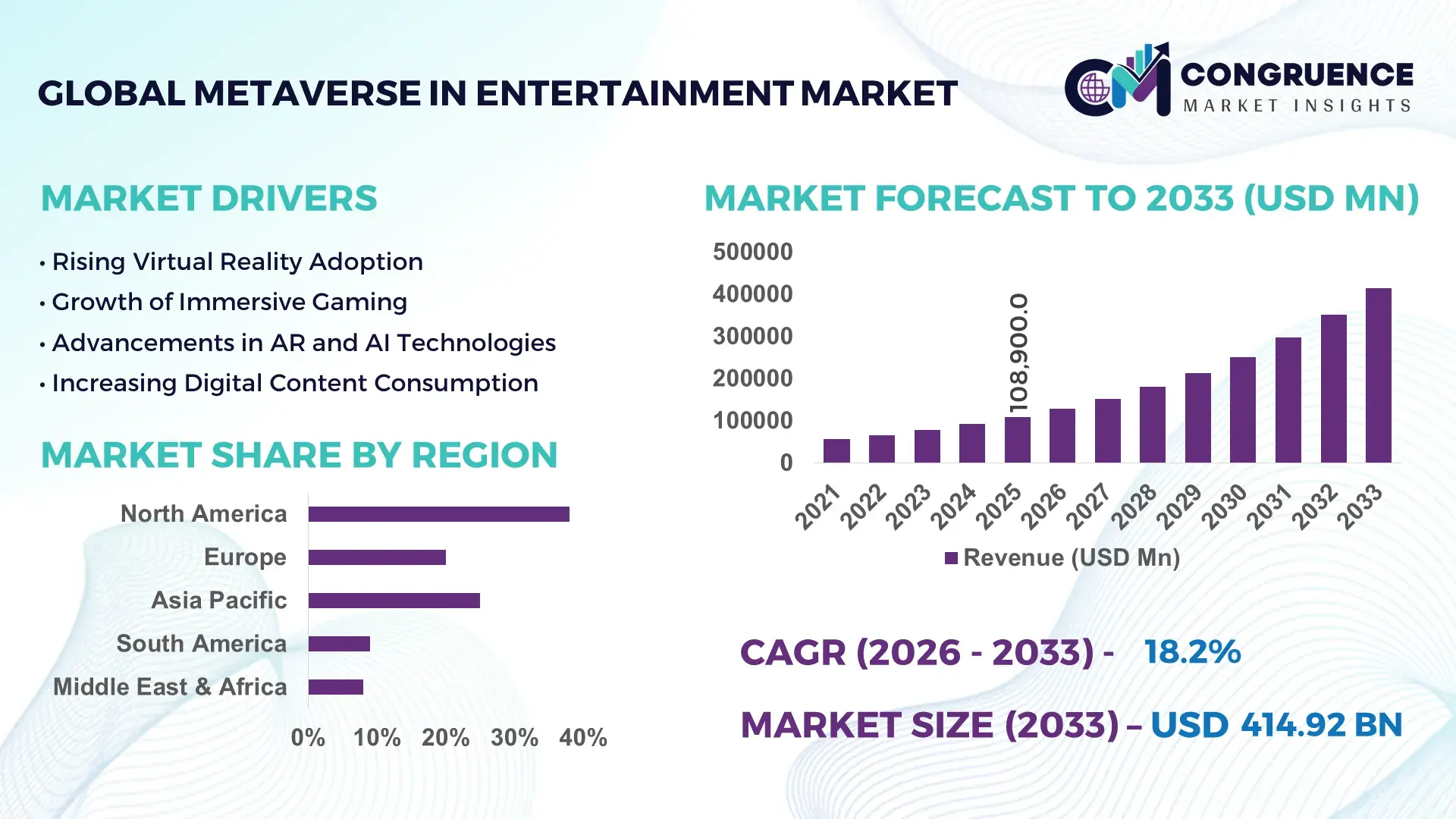

The Global Metaverse in Entertainment Market was valued at USD 108900 Million in 2025 and is anticipated to reach a value of USD 414923.17 Million by 2033 expanding at a CAGR of 18.2% between 2026 and 2033. Growth is being accelerated by large-scale integration of immersive virtual concerts, AI-powered fan engagement platforms, interoperable gaming ecosystems, and enterprise-backed spatial computing investments across streaming, sports, and digital media industries.

The United States dominated the global metaverse in entertainment market with approximately 38% share in 2025, supported by over USD 24 billion in immersive content and XR infrastructure investments from gaming studios, media conglomerates, and cloud providers. China followed with nearly 21% market participation, driven by state-backed virtual ecosystem programs and 5G-enabled entertainment adoption across mobile-first consumers. Following post-2025 semiconductor supply normalization and AI hardware expansion, U.S. entertainment platforms reported over 32% higher user retention in immersive digital events compared to conventional streaming environments.

Companies expanding interoperable content ecosystems, real-time rendering capacity, and AI-driven monetization frameworks are positioned to secure long-term audience ownership and premium digital engagement advantages.

Market Size & Growth: USD 108900 Million in 2025 reaching USD 414923.17 Million by 2033 at 18.2% CAGR, fueled by immersive gaming, virtual live events, and AI-generated entertainment experiences.

Top Growth Drivers: Virtual concert attendance increased 41%, VR gaming subscriptions rose 36%, and branded metaverse advertising spending expanded 33% globally in 2025.

Short-Term Forecast: By 2027, cloud-rendering optimization is projected to reduce immersive content delivery costs by 22% while improving real-time interaction efficiency by 31%.

Emerging Technologies: Generative AI avatars, spatial computing, and blockchain-based digital ownership accelerated platform engagement by over 28% across advanced entertainment ecosystems.

Regional Leaders: North America exceeded USD 41 billion through premium gaming ecosystems, Asia-Pacific crossed USD 35 billion via mobile metaverse adoption, while Europe surpassed USD 22 billion through virtual sports and music integrations.

Consumer/End-User Trends: Nearly 47% of Gen Z users participated in interactive virtual entertainment environments weekly during 2025.

Pilot/Case Example: In 2026, a global music platform deployed AI-driven immersive concerts, increasing paid audience engagement rates by 34% and reducing churn by 19%.

Competitive Landscape: Meta Platforms controlled approximately 17% market share alongside major participants including Tencent, Roblox, Epic Games, and Microsoft.

Regulatory & ESG Impact: Regional digital governance policies improved user data transparency compliance by 26% following tighter virtual asset regulations across North America and Europe.

Investment & Funding: Global investments surpassed USD 29 billion in 2025, led by strategic partnerships, AI infrastructure expansion, and spatial computing acquisitions.

Innovation & Future Outlook: Persistent virtual worlds, hyper-realistic avatars, and cross-platform digital commerce are reshaping high-growth entertainment monetization strategies globally.

The metaverse in entertainment market is witnessing rapid expansion across interactive gaming, virtual concerts, digital cinemas, and AI-powered creator economies. Advanced spatial computing platforms improved immersive user engagement by nearly 29% during 2025, while real-time rendering engines accelerated content deployment cycles for major entertainment operators. Asia-Pacific emerged as a high-activity expansion zone due to rising mobile XR adoption and localized digital content ecosystems, creating strong momentum for strategic partnerships and scalable audience monetization initiatives.

The metaverse in entertainment market has become strategically critical as media companies, gaming publishers, sports franchises, and streaming platforms compete for persistent digital audience ownership and higher engagement monetization. Following accelerated AI infrastructure expansion and post-2025 cloud supply-chain stabilization, entertainment operators are restructuring content delivery models toward immersive ecosystems with integrated commerce, digital assets, and real-time interaction layers. More than 44% of leading global entertainment firms increased spatial computing and immersive platform budgets during 2025 to strengthen user retention and diversify subscription-based revenue streams.

Modern cloud-rendered metaverse platforms reduce content deployment time by nearly 37% compared with legacy on-premise gaming and streaming architectures while lowering large-scale event latency by approximately 29%. The United States leads in enterprise-scale deployment through advanced GPU infrastructure and AI-enabled virtual production pipelines, whereas South Korea is accelerating consumer-focused adoption through nationwide 5G optimization and interoperable digital identity frameworks. In 2026, a major sports entertainment operator deployed immersive fan arenas integrated with AI avatars, increasing average user session duration by 31%.

Over the next two to three years, companies are expected to prioritize cross-platform interoperability, creator monetization ecosystems, and strategic telecom partnerships to improve scalability and audience conversion efficiency. Organizations capable of combining immersive engagement, AI personalization, and scalable infrastructure will secure stronger competitive positioning across the evolving digital entertainment economy.

Gaming publishers, streaming companies, and live entertainment operators are accelerating metaverse integration to increase engagement duration and digital monetization efficiency. During 2025, virtual event participation rose by 39%, while AI-powered interactive entertainment deployments improved premium user retention by nearly 27%. The expansion of low-latency cloud infrastructure across the United States and Japan enabled large-scale concurrent immersive experiences with reduced rendering delays and stronger transaction stability. This operational shift is driving companies toward ecosystem-based business models integrating digital merchandise, virtual ticketing, and creator-led economies. Entertainment firms are responding through acquisitions of XR studios, partnerships with telecom operators, and investment in spatial computing infrastructure. A notable strategic shift involves studios prioritizing interoperable digital assets to extend user lifetime value across multiple entertainment environments rather than isolated platform ecosystems.

High-performance computing dependency and fragmented platform standards continue to restrict scalable metaverse deployment across entertainment ecosystems. Advanced XR content environments require nearly 32% higher infrastructure spending compared with traditional streaming operations, while interoperability inconsistencies increase integration costs by approximately 24% for multi-platform developers. In 2025, semiconductor component supply fluctuations in Taiwan and South Korea extended hardware deployment timelines for immersive entertainment providers. These constraints directly affect scalability, device accessibility, and operational profitability, particularly for mid-sized content studios. Companies are mitigating risks through localized cloud partnerships, hybrid rendering architectures, and strategic GPU procurement contracts. A critical operational insight is that firms adopting open-engine development frameworks are reducing cross-platform deployment complexity faster than competitors relying on proprietary infrastructure ecosystems.

AI-enhanced avatars, real-time procedural content generation, and blockchain-enabled digital ownership systems are creating high-value expansion opportunities across entertainment platforms. Consumer interaction within personalized immersive environments increased by 34% during 2025, while automated virtual production workflows reduced digital asset creation time by nearly 28%. India and the United Arab Emirates are emerging as strategic deployment hubs due to expanding 5G penetration, creator economy growth, and government-backed digital infrastructure initiatives. Companies are investing heavily in AI-integrated creator tools and immersive commerce ecosystems to capture younger digital-native audiences. A significant opportunity is developing lightweight mobile-first metaverse environments that reduce hardware dependency while expanding audience reach. Entertainment operators establishing interoperable partnerships with telecom providers and payment technology firms are positioning themselves for stronger ecosystem scalability and recurring digital engagement models.

Long-term expansion of metaverse entertainment ecosystems is constrained by cybersecurity exposure, infrastructure synchronization complexity, and high-volume rendering demands. In 2025, immersive entertainment platforms experienced approximately 26% higher cybersecurity incident exposure compared with conventional digital media environments due to decentralized asset transactions and persistent virtual identity systems. Simultaneously, large-scale virtual events require up to 40% greater processing intensity, creating operational pressure on cloud infrastructure providers and content delivery systems. Regulatory evolution across the European Union and China is also increasing compliance obligations around digital identity protection and virtual asset governance. Companies must strengthen encryption frameworks, edge-computing investments, and identity verification systems to maintain deployment consistency and user trust. Organizations that integrate scalable security architecture early will gain a measurable operational advantage as immersive entertainment ecosystems become increasingly interconnected and transaction-intensive.

• AI-Powered Immersive Personalization Entertainment platforms are integrating generative AI engines into metaverse ecosystems to improve audience retention, automate avatar behavior, and accelerate virtual content production. During 2025, AI-assisted asset generation reduced development timelines by 33%, while personalized recommendation layers improved session duration by 26%. U.S.-based streaming operators increasingly shifted toward automated real-time rendering workflows following GPU supply normalization, enabling lower operational latency and faster multi-event deployment capacity.

• Mobile-First Virtual Ecosystems Expansion Smartphone-optimized metaverse environments are reshaping user acquisition strategies across India, Southeast Asia, and Brazil, where mobile immersive traffic exceeded desktop participation by 48% during 2025. Entertainment companies are restructuring deployment models toward lightweight XR experiences requiring lower processing intensity and reduced bandwidth consumption. Telecom partnerships and edge-computing integration improved concurrent user handling efficiency by nearly 24%, allowing broader audience scalability without relying heavily on premium VR hardware penetration.

• Enterprise-Backed Virtual Event Scaling Sports leagues, music labels, and event operators accelerated investment in persistent virtual venues following rising physical event operating costs and venue scheduling pressure. In 2026, hybrid immersive events lowered audience acquisition expenses by approximately 21% while increasing cross-border attendance participation by 29%. Companies are responding through cloud infrastructure partnerships, AI moderation deployment, and integrated digital merchandise ecosystems designed to improve recurring engagement monetization beyond traditional ticket-based models.

• Interoperable Digital Asset Integration Entertainment providers are prioritizing cross-platform digital ownership frameworks as consumers demand transferable virtual identities and persistent digital collectibles. NFT-enabled entertainment interactions increased by 31% during 2025, particularly across gaming and live music ecosystems in South Korea and Japan. Regulatory tightening around virtual asset transparency pushed companies toward standardized identity verification systems and blockchain interoperability alliances, creating stronger operational trust while reducing duplicate content management and fragmented marketplace inefficiencies.

Virtual Reality Platforms remained the dominant segment in the metaverse in entertainment market due to superior immersion capability, mature gaming integration, and stronger monetization efficiency across digital entertainment ecosystems. In 2025, nearly 43% of immersive entertainment deployments were linked to VR-enabled environments, particularly across multiplayer gaming, virtual sports arenas, and live entertainment simulations. Major entertainment operators prioritized VR ecosystem expansion through cloud rendering optimization and AI-enhanced interaction layers to improve session engagement and reduce latency-related churn. Virtual Event Platforms also maintained strong strategic relevance as hybrid entertainment delivery gained momentum among music labels and sports broadcasters seeking scalable audience participation models.

Mixed Reality Platforms emerged as the fastest-growing segment, supported by increasing enterprise adoption of spatial computing and lightweight wearable interfaces. MR-based engagement deployments improved collaborative interaction efficiency by approximately 28% compared with standalone VR systems. Augmented Reality Platforms gained traction through mobile-first entertainment integration, particularly in Japan and India where smartphone-based immersive engagement accelerated rapidly. NFT Platforms continued evolving beyond speculative trading into utility-focused digital ownership ecosystems supporting interoperable entertainment assets and creator monetization frameworks. Companies are expanding investment toward cross-platform compatibility and AI-integrated immersive environments to strengthen ecosystem scalability and long-term audience retention.

Gaming remained the leading application segment due to persistent user engagement, advanced monetization structures, and large-scale virtual ecosystem deployment. During 2025, gaming accounted for nearly 46% of immersive entertainment activity, supported by rising multiplayer interaction demand and AI-driven digital economies. Game publishers increasingly integrated interoperable avatars, digital assets, and creator-led ecosystems to extend user retention cycles and improve transaction frequency. Digital Content Streaming also strengthened operational relevance as immersive viewing formats and AI-powered recommendation systems improved engagement duration by approximately 23%, particularly among younger mobile-first audiences.

Virtual Concerts emerged as the fastest-growing application as entertainment companies sought scalable alternatives to venue-constrained physical events. In 2026, immersive concert participation increased by 34%, while hybrid live event integration reduced international audience acquisition costs by nearly 19%. Live Events continued expanding through sports and fan-engagement deployments, particularly across the United States and South Korea where 5G-enabled virtual attendance models accelerated. Social Media Experiences evolved toward avatar-based interaction environments with integrated commerce and creator monetization systems. Companies are prioritizing cloud scalability, AI moderation, and telecom partnerships to strengthen operational reliability and expand concurrent participation capacity.

Media and Entertainment Companies represented the dominant end-user segment due to extensive infrastructure dependency, high-volume content distribution requirements, and aggressive investment in immersive audience engagement ecosystems. In 2025, approximately 39% of metaverse entertainment deployments were driven by large streaming operators, film studios, and digital media networks integrating AI-enhanced virtual production and immersive advertising systems. These organizations prioritized scalable cloud rendering architectures and interoperable content ecosystems to strengthen viewer retention and cross-platform monetization. Gaming Companies also maintained strong operational intensity through persistent virtual worlds and integrated digital commerce frameworks supporting high-frequency user interaction.

Sports Organizations emerged as the fastest-growing end-user group as leagues and franchises accelerated investment in virtual fan arenas, immersive merchandise ecosystems, and AI-powered engagement analytics. Virtual sports participation environments improved fan interaction duration by nearly 27% during 2026. Event Organizers expanded hybrid immersive experiences to reduce venue dependency and improve international audience accessibility, while Advertising Agencies increasingly deployed branded virtual campaigns and interactive placements. Content Creators gained strategic relevance through decentralized monetization ecosystems and AI-assisted production tools. Companies are tailoring platform customization, subscription models, and partnership strategies to secure long-term ecosystem loyalty and diversified digital engagement channels.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 20.4% between 2026 and 2033.

AI-Led Immersive Entertainment Scaling

North America maintained the leading position due to strong cloud infrastructure, advanced GPU availability, and large-scale enterprise deployment across gaming, streaming, and virtual sports ecosystems. The region contributed nearly 38% of global immersive entertainment deployments during 2025, with the United States driving the majority of XR-enabled entertainment activity. Major entertainment operators accelerated partnerships with telecom providers and AI infrastructure firms to improve rendering efficiency and concurrent audience capacity. During 2026, multiple streaming and gaming enterprises reduced immersive content latency by approximately 27% through edge-computing deployment and cloud-rendering optimization. Companies are increasingly prioritizing interoperable virtual ecosystems and AI-personalized engagement frameworks to strengthen long-term monetization and audience retention efficiency.

United States Market Outlook: The United States dominates the regional market through advanced spatial computing infrastructure, strong gaming ecosystem concentration, and large-scale investment in immersive media technologies. More than 62% of major entertainment enterprises integrated AI-assisted virtual engagement systems during 2025, particularly across sports broadcasting, gaming, and virtual concerts. Entertainment studios and streaming operators are expanding virtual production capabilities and cloud-rendered event platforms to improve audience scalability and accelerate premium immersive content deployment across highly connected digital ecosystems.

Regulated Virtual Ecosystem Modernization

Europe is strengthening its metaverse entertainment position through privacy-focused infrastructure upgrades, digital identity governance, and immersive cultural content deployment. The region accounted for approximately 24% of global immersive entertainment activity in 2025, supported by growing investment in virtual sports broadcasting, digital exhibitions, and AI-assisted interactive media environments. Germany, France, and the United Kingdom accelerated deployment of secure virtual transaction systems and interoperable entertainment platforms following tighter digital governance policies. During 2026, cloud-based immersive event systems improved operational scalability by nearly 22% through 5G-enabled streaming optimization and AI-driven moderation tools. Companies are focusing on compliance-oriented infrastructure modernization and energy-efficient rendering systems to improve long-term deployment reliability.

Germany Market Outlook: Germany is emerging as a strategic immersive entertainment technology hub due to advanced telecommunications infrastructure, strong enterprise XR capabilities, and increasing deployment of immersive media environments. Nearly 46% of German media technology firms expanded mixed-reality initiatives during 2025, particularly across interactive sports, gaming, and digital exhibition platforms. German enterprises are prioritizing secure cloud architecture and edge-computing integration to improve immersive engagement consistency and strengthen compliance with evolving virtual identity and data governance frameworks.

Mobile-First Immersive Deployment Expansion

Asia-Pacific is witnessing the fastest operational expansion due to rising mobile gaming penetration, expanding 5G infrastructure, and large-scale adoption of digital entertainment ecosystems. The region contributed nearly 31% of global immersive entertainment activity in 2025, led by China, South Korea, Japan, and India. Entertainment companies accelerated deployment of lightweight XR platforms and AI-powered engagement systems optimized for smartphone-based participation. During 2026, telecom-supported immersive streaming systems improved concurrent user management efficiency by approximately 34%, enabling scalable audience expansion with lower hardware dependency. Companies are increasingly restructuring regional operations around creator economies, localized virtual content production, and interoperable digital asset ecosystems.

China Market Outlook: China maintains a dominant operational position through advanced gaming infrastructure, strong mobile entertainment adoption, and state-supported digital ecosystem development. More than 58% of major domestic entertainment technology firms expanded AI-integrated immersive engagement systems during 2025. Chinese gaming publishers and virtual entertainment providers are increasing investment in cloud-rendering architecture, digital avatar ecosystems, and virtual commerce integration to strengthen audience retention and improve large-scale immersive event deployment across highly connected urban markets.

Affordable Digital Entertainment Adoption

South America is experiencing increasing metaverse entertainment adoption driven by mobile-first consumer behavior, improving broadband infrastructure, and growing demand for low-cost immersive engagement environments. Brazil and Argentina represented the majority of regional deployment activity during 2025, particularly across gaming and virtual social entertainment ecosystems. Entertainment providers expanded cloud-based streaming partnerships to reduce latency constraints and improve accessibility for smartphone users. During 2026, mobile-optimized immersive entertainment deployments improved user participation rates by approximately 23% across major urban markets. Despite infrastructure inconsistency and limited high-performance device penetration, companies are scaling localized creator ecosystems and telecom-integrated entertainment platforms to strengthen audience accessibility and operational reach.

Brazil Market Outlook: Brazil leads the regional market through strong gaming participation, expanding creator economies, and rising enterprise investment in immersive digital entertainment services. Nearly 49% of immersive entertainment traffic originated from mobile-based platforms during 2025, encouraging operators to prioritize lightweight XR deployment models. Brazilian entertainment companies are increasingly collaborating with telecom providers and payment technology firms to improve monetization efficiency, audience scalability, and cross-platform engagement consistency across rapidly expanding digital consumer segments.

Government-Backed Immersive Infrastructure Investment

The Middle East & Africa region is advancing through government-supported digital modernization initiatives, smart city expansion, and increasing investment in immersive tourism and entertainment ecosystems. The United Arab Emirates and Saudi Arabia accounted for the largest deployment concentration during 2025, supported by advanced 5G rollout and enterprise-backed virtual engagement projects. Entertainment operators integrated AI-driven immersive experiences across tourism, sports, and cultural event ecosystems to strengthen international audience participation. During 2026, infrastructure partnerships across Gulf countries improved immersive event processing efficiency by approximately 25% through cloud optimization and edge-computing deployment initiatives. Regional expansion remains partially constrained by uneven broadband accessibility across parts of Africa, although investment momentum continues improving deployment scalability.

United Arab Emirates Market Outlook: The United Arab Emirates is positioning itself as a regional immersive entertainment innovation hub through aggressive smart infrastructure investment and enterprise-focused metaverse deployment strategies. More than 41% of large digital entertainment operators in the country expanded immersive audience engagement initiatives during 2025, particularly across tourism-linked entertainment and virtual live events. UAE-based technology ecosystems are accelerating commercialization of AI-powered avatar systems, blockchain-enabled digital experiences, and cloud-rendered virtual environments designed for large-scale international audience participation.

Meta Platforms, Tencent, Microsoft, Roblox, and Epic Games compete aggressively through proprietary XR infrastructure, AI-powered engagement systems, and scalable virtual ecosystem deployment. The top five players collectively controlled nearly 54% of global market activity during 2025, with competition centered on rendering efficiency, interoperability, immersive engagement depth, and digital asset monetization. AI-assisted content generation reduced production timelines by approximately 31%, while cloud-optimized immersive delivery improved concurrent event handling efficiency by nearly 26%. U.S.-based platform operators are competing through studio acquisitions, infrastructure expansion, and vertical ecosystem integration, whereas Asian firms prioritize mobile-first scalability and localized creator economies. Telecom-backed entertainment partnerships are strengthening infrastructure control and reducing latency dependency across immersive streaming ecosystems. Rising GPU procurement costs, cybersecurity compliance requirements, and interoperability complexity remain major entry barriers. Companies capable of combining scalable cloud architecture, AI-driven personalization, and interoperable virtual commerce ecosystems are securing sustainable competitive advantage.

Meta Platforms Inc.

Tencent Holdings Ltd.

Microsoft Corporation

Roblox Corporation

Epic Games Inc.

NVIDIA Corporation

Unity Software Inc.

ByteDance Ltd.

Sony Group Corporation

NetEase Inc.

HTC Corporation

Animoca Brands Corporation Ltd.

Decentraland Foundation

The Sandbox

Cloud-rendered XR platforms, AI-driven avatars, and real-time spatial engines currently dominate metaverse entertainment deployment across gaming, virtual concerts, and streaming ecosystems. During 2025, AI-assisted content generation reduced virtual asset production timelines by nearly 33%, while edge-computing integration improved immersive event latency performance by approximately 27%. More than 58% of major entertainment platforms deployed cloud-based rendering systems to support large-scale concurrent user participation. Compared with legacy standalone rendering architectures, modern GPU-optimized cloud environments improved scalability efficiency by nearly 35%, enabling faster deployment cycles and lower infrastructure dependency for global entertainment operators.

Emerging technologies including mixed reality wearables, blockchain-enabled digital ownership, and interoperable identity systems are accelerating operational transformation between 2026 and 2028. Mobile-first XR ecosystems increased immersive engagement participation by approximately 29% across Asia-Pacific markets due to lightweight processing frameworks and telecom-integrated streaming models. Companies integrating AI-driven personalization engines reported nearly 24% higher audience retention compared with conventional digital entertainment interfaces. Gaming publishers and streaming operators are increasingly partnering with telecom firms and AI infrastructure providers to strengthen scalable audience engagement and improve cross-platform interoperability.

Disruptive technologies such as generative virtual production, decentralized digital commerce ecosystems, and AI-powered immersive advertising frameworks are reshaping competitive positioning. Enterprise operators deploying automated immersive production workflows reduced content deployment costs by approximately 21% during 2026. Companies capable of integrating AI personalization, interoperable digital assets, and scalable cloud infrastructure will secure stronger operational efficiency and long-term audience monetization advantages.

April 2025 – Roblox Corporation expanded immersive advertising capabilities through a strategic partnership with Google, enabling scalable rewarded video ad deployment across metaverse gaming environments. Early campaign testing achieved over 80% ad completion rates, strengthening monetization efficiency and creator revenue opportunities across interactive entertainment ecosystems. Source: domain: corp.roblox.com

May 2024 – Roblox Corporation opened immersive video advertising access to all eligible advertisers, targeting more than 71.5 million daily active users across virtual entertainment environments. The rollout accelerated brand participation and strengthened commercial adoption of metaverse-native advertising models for gaming-focused digital engagement strategies. Source: corp.roblox.com

August 2025 – Meta Platforms partnered with Midjourney to integrate AI image and video generation technologies into future immersive ecosystem development. The initiative strengthened AI-powered avatar realism and virtual content scalability while accelerating advanced metaverse production workflows across entertainment and social interaction environments. Source: techcrunch.com

January 2026 – Meta Platforms restructured Reality Labs operations by reducing approximately 10% of division workforce and closing three VR studios to prioritize AI wearables and mobile-integrated immersive systems. The shift improved operational focus toward scalable AI-enabled engagement technologies and streamlined infrastructure allocation strategies. Source: pcgamer.com

The report provides comprehensive analysis of the metaverse in entertainment market across platform types, applications, end-user industries, technology ecosystems, and regional deployment dynamics between 2026 and 2033. Coverage includes Virtual Reality Platforms, Augmented Reality Platforms, Mixed Reality Platforms, NFT Platforms, and Virtual Event Platforms, alongside application analysis across gaming, virtual concerts, live events, social media experiences, and digital content streaming. The study evaluates deployment concentration, infrastructure modernization, AI integration trends, and immersive engagement adoption patterns across North America, Europe, Asia-Pacific, South America, and Middle East & Africa.

The report assesses operational strategies of leading entertainment technology providers, gaming companies, streaming operators, sports organizations, and immersive infrastructure developers. More than 60% of analyzed enterprise participants are actively prioritizing AI-enabled immersive engagement, cloud-rendering optimization, and interoperable digital asset ecosystems. Strategic insights support competitive positioning, expansion planning, investment prioritization, partnership evaluation, and long-term deployment decision-making across evolving immersive entertainment and virtual engagement environments.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 108900 Million |

|

Market Revenue in 2033 |

USD 414923.17 Million |

|

CAGR (2026 - 2033) |

18.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Meta Platforms Inc., Tencent Holdings Ltd., Microsoft Corporation, Roblox Corporation, Epic Games Inc., NVIDIA Corporation, Unity Software Inc., ByteDance Ltd., Sony Group Corporation, NetEase Inc., HTC Corporation, Animoca Brands Corporation Ltd., Decentraland Foundation, The Sandbox |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |