Reports

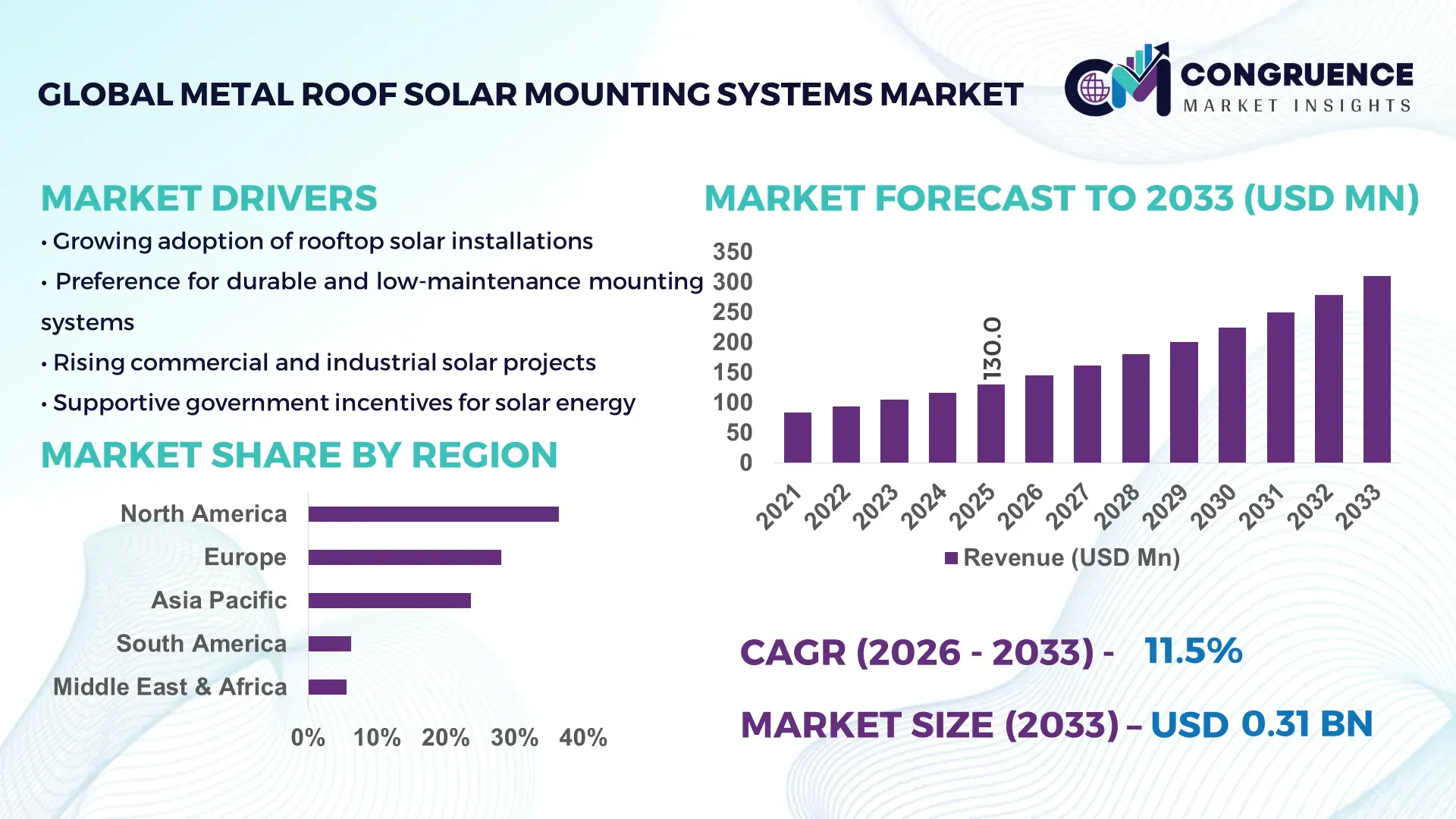

The Global Metal Roof Solar Mounting Systems Market was valued at USD 130.0 Million in 2025 and is anticipated to reach a value of USD 310.6 Million by 2033 expanding at a CAGR of 11.5% between 2026 and 2033, according to an analysis by Congruence Market Insights. The market is expanding due to the rising installation of rooftop solar photovoltaic systems across commercial, industrial, and residential infrastructures.

The United States represents one of the most significant production and technology hubs for metal roof solar mounting systems. The country installed more than 32 GW of new solar capacity in 2023, with rooftop and distributed solar accounting for nearly 28% of installations across commercial and industrial facilities. Over 2.6 million rooftop solar systems are currently operational in the U.S., many of which utilize metal roof mounting solutions for warehouses, logistics centers, and manufacturing facilities. The country also hosts more than 350 solar component manufacturing facilities, including mounting and racking system plants across states such as Texas, Ohio, and California. Industrial adoption is particularly strong in sectors like retail distribution and cold storage, where metal roofs dominate construction structures. In addition, U.S. companies are investing in automated mounting technologies and aluminum alloy mounting rails capable of supporting 30% higher load tolerance, improving durability and reducing installation time by nearly 25% compared with earlier mounting designs.

Market Size & Growth: The market reached USD 130.0 Million in 2025 and is projected to reach USD 310.6 Million by 2033, expanding at a CAGR of 11.5%, driven by increasing adoption of rooftop solar systems across industrial facilities and logistics warehouses.

Top Growth Drivers: Rooftop solar adoption across industrial buildings exceeds 45% penetration in new commercial facilities, improvements in mounting system durability reaching 30% higher load-bearing capacity, and installation efficiency improvements of nearly 25% through pre-assembled mounting structures.

Short-Term Forecast: By 2028, automated installation and pre-engineered mounting structures are expected to reduce installation labor costs by 20% while improving system deployment speed by 18%.

Emerging Technologies: Key innovations include rail-less mounting architectures, aerodynamic clamp-based mounting systems, and AI-assisted structural design software enabling optimized load distribution and faster engineering validation.

Regional Leaders: North America is projected to reach approximately USD 95 Million by 2033 driven by industrial rooftop adoption, Europe around USD 82 Million supported by commercial solar retrofits, and Asia-Pacific about USD 105 Million due to large-scale manufacturing facility solarization.

Consumer/End-User Trends: Commercial buildings, logistics warehouses, and manufacturing plants collectively represent more than 65% of installations, with facility operators prioritizing long-term roof-integrated energy generation and reduced operational energy costs.

Pilot or Case Example: In 2024, a large U.S. distribution warehouse project implemented aerodynamic metal roof mounting systems that improved installation speed by 27% and increased panel density by 15%, improving onsite energy production capacity.

Competitive Landscape: The market leader holds roughly 16% share, followed by major players including Unirac, S-5!, IronRidge, Schletter Group, and K2 Systems, all focusing on lightweight aluminum mounting innovations.

Regulatory & ESG Impact: Government rooftop solar incentives and ESG commitments are accelerating installations, with more than 70% of Fortune 500 companies implementing renewable energy procurement targets tied to rooftop solar expansion.

Investment & Funding Patterns: Global solar infrastructure investments exceeded USD 250 Billion in 2024, with mounting system manufacturing expansion accounting for nearly 8% of equipment investment across supply chains.

Innovation & Future Outlook: Advances in corrosion-resistant alloys, integrated cable management systems, and prefabricated clamp technologies are expected to reduce installation complexity by 20–25%, enabling wider rooftop solar adoption across industrial buildings.

Metal roof solar mounting systems are widely adopted across industrial facilities (around 40% demand), commercial buildings (about 35%), and residential installations (roughly 25%). Product innovations include lightweight aluminum clamps, rail-less mounting solutions, and corrosion-resistant fastening systems designed for extreme weather conditions. Regulatory incentives supporting rooftop solar deployment and corporate renewable energy commitments are accelerating installations, particularly across North America and Asia-Pacific manufacturing sectors, while automation in mounting design and installation continues to improve project efficiency and scalability.

The Metal Roof Solar Mounting Systems Market is becoming strategically important as organizations shift toward distributed renewable energy generation integrated directly into building infrastructure. Metal roofing is widely used in commercial and industrial buildings due to its durability and structural strength, creating an ideal foundation for rooftop solar installations. Globally, nearly 60% of industrial warehouses and logistics centers utilize metal roofing, creating a substantial installed base for mounting system integration.

Technological innovation is playing a key role in shaping the market’s future. Rail-less mounting systems deliver nearly 20% faster installation compared to traditional rail-based mounting standards, while advanced aluminum clamp technologies provide 30% higher structural load resistance in high-wind environments. These performance improvements reduce installation time, lower engineering complexity, and improve long-term structural reliability.

Regional adoption patterns show distinct strategic differences. Asia-Pacific dominates in installation volume, particularly across China and India where large manufacturing facilities deploy rooftop solar across factory campuses. Meanwhile, North America leads in technology adoption, with nearly 48% of large commercial rooftop solar projects integrating advanced aerodynamic mounting systems designed to reduce structural roof load.

Over the next few years, digital engineering technologies are expected to reshape installation processes. By 2028, AI-assisted structural simulation tools are projected to reduce system design errors by 22%, enabling faster permitting and engineering approvals for rooftop solar systems.

Environmental commitments are also accelerating adoption. Corporations are committing to renewable energy usage targets exceeding 50% by 2030, while solar installations using metal roof mounting systems enable companies to reduce building-related carbon emissions by up to 35%.

A micro-scenario highlighting technological impact emerged in 2024, when a U.S. industrial logistics operator deployed advanced clamp-based mounting systems across multiple distribution centers, achieving a 26% reduction in installation time and a 19% improvement in structural stability under high wind loads.

As rooftop solar continues expanding across industrial and commercial infrastructure, the Metal Roof Solar Mounting Systems Market is positioned to become a critical pillar supporting energy resilience, sustainability commitments, and decentralized power generation strategies worldwide.

The Metal Roof Solar Mounting Systems Market is evolving rapidly as rooftop solar photovoltaic installations expand across commercial, industrial, and residential buildings. Metal roofs offer structural durability, lightweight properties, and long operational lifespans exceeding 40 years, making them highly compatible with solar mounting infrastructure. Increasing electrification of industrial facilities and rising electricity costs are encouraging companies to integrate onsite renewable energy systems. Additionally, the expansion of distributed energy resources and net-metering policies across many countries has strengthened demand for rooftop solar installations supported by advanced mounting technologies. Manufacturers are introducing lightweight aluminum and stainless-steel mounting components designed to withstand wind speeds exceeding 150 km/h, improving system reliability. Automation in mounting system manufacturing has also improved production efficiency by nearly 20% over the past decade. At the same time, integration of prefabricated mounting kits is enabling faster solar panel deployment across large commercial buildings such as warehouses, shopping centers, and production plants. These developments collectively contribute to increasing demand for specialized mounting systems optimized for metal roofing structures.

The rapid global expansion of rooftop solar installations is one of the most significant drivers for the Metal Roof Solar Mounting Systems Market. Industrial and commercial buildings frequently use metal roofs because of their durability and structural capacity to support additional equipment such as photovoltaic panels. Globally, more than 30% of commercial buildings constructed after 2015 incorporate metal roofing structures, providing a large installation base for mounting systems. Large logistics facilities, which often exceed 50,000 square meters of roof area, are increasingly integrating rooftop solar arrays to offset energy consumption. For example, distribution warehouses and retail chains are installing solar systems capable of producing 2–5 MW of electricity per facility. Metal roof mounting systems are preferred in such projects because clamp-based designs eliminate the need for roof penetration, reducing maintenance requirements and installation risks. Additionally, installation efficiency has improved significantly. Modern rail-less mounting systems reduce installation components by nearly 40%, allowing installers to complete projects faster. Industrial rooftop solar adoption is particularly strong in sectors such as automotive manufacturing, cold storage, and e-commerce logistics where energy consumption levels are high. These factors collectively strengthen demand for specialized mounting systems designed specifically for metal roofing structures.

Despite strong adoption trends, structural and compatibility limitations represent a significant restraint for the Metal Roof Solar Mounting Systems Market. Not all metal roofing systems are designed to support solar panel installations without reinforcement. Older buildings constructed before modern building standards often lack the structural strength required to support solar arrays weighing 12–20 kilograms per square meter. Roof slope and panel orientation also present challenges. In facilities with steep roof angles exceeding 30 degrees, mounting systems require additional safety structures and specialized clamps, increasing installation complexity. Furthermore, metal roofs may vary in design types such as corrugated panels, standing seam roofs, and trapezoidal profiles, each requiring different mounting hardware configurations. Maintenance considerations also affect adoption. Industrial buildings often host HVAC equipment, ventilation systems, and safety pathways on rooftops, limiting the available installation area for solar panels. In some cases, rooftop solar coverage may be restricted to less than 50% of usable roof space due to structural constraints. These structural limitations create additional engineering requirements and may slow adoption in certain building categories.

Industrial decarbonization initiatives are creating major opportunities for the Metal Roof Solar Mounting Systems Market. Manufacturing companies and logistics operators are increasingly investing in onsite renewable energy systems to reduce operational carbon emissions and electricity costs. Industrial facilities typically have large rooftop areas exceeding 10,000 square meters, enabling installation of solar systems generating 1–3 MW of electricity per building. Many multinational corporations have committed to renewable energy targets exceeding 50% clean energy usage by 2030, driving adoption of rooftop solar installations. Metal roof mounting systems allow companies to deploy solar panels without extensive structural modifications, making them a preferred installation method. Advances in mounting technology are also unlocking new opportunities. Lightweight aluminum mounting rails and clamp-based systems have reduced installation time by nearly 25%, enabling faster solar deployment across multiple facilities. In addition, governments in several regions are introducing building regulations that encourage or require rooftop solar integration in new commercial buildings. Such policy measures significantly expand the addressable market for mounting systems specifically designed for metal roofs.

Supply chain disruptions and rising raw material costs represent key challenges for the Metal Roof Solar Mounting Systems Market. Aluminum and stainless steel are primary materials used in mounting structures, and fluctuations in metal prices significantly affect manufacturing costs. Over the past few years, global aluminum prices have experienced volatility of 15–25% annually, affecting component manufacturing expenses. Transportation logistics also influence supply chains because mounting systems are bulky structural components that require specialized packaging and shipping methods. Delays in international shipping routes and container shortages have increased delivery timelines for solar project components in several regions. In addition, manufacturing mounting components requires precision engineering and specialized extrusion processes. Limited availability of extrusion capacity in some regions can create production bottlenecks, particularly during periods of strong solar installation demand. These supply chain complexities and material cost fluctuations create operational challenges for manufacturers and project developers, potentially delaying rooftop solar installation timelines.

Rapid adoption of rail-less mounting systems: Rail-less mounting architectures are transforming rooftop solar installations by reducing component requirements by nearly 35% compared with traditional rail-based systems. Installation time has improved by approximately 22%, allowing installers to complete projects faster. In North America and Europe, more than 40% of new commercial rooftop solar installations are adopting rail-less mounting technologies due to their simplified design and reduced material consumption.

Growing demand from industrial warehouses: Industrial warehouse rooftops are becoming one of the fastest-growing installation environments for solar mounting systems. Logistics facilities typically feature roof areas exceeding 30,000–60,000 square meters, enabling large solar arrays. Approximately 52% of newly constructed logistics facilities globally now incorporate rooftop solar infrastructure as part of energy efficiency initiatives.

Increased use of lightweight aluminum mounting materials: Manufacturers are shifting toward high-strength aluminum alloys capable of reducing mounting system weight by 20–25% while maintaining structural durability. These materials also provide corrosion resistance for installations in coastal and high-humidity environments. Aluminum mounting components currently represent nearly 70% of structural materials used in rooftop solar mounting systems.

Integration of prefabricated installation kits: Prefabricated mounting kits are becoming widely used in commercial rooftop solar projects. Pre-assembled mounting components reduce onsite labor requirements by approximately 18% and allow installers to complete system assembly faster. Nearly 45% of solar installers now use pre-configured mounting kits for large commercial installations to improve efficiency and reduce installation errors.

The Metal Roof Solar Mounting Systems Market is segmented based on type, application, and end-user industries, reflecting the diverse installation environments where rooftop solar systems are deployed. Mounting system types vary according to roof structure and installation requirements, including rail-based systems, rail-less systems, and clamp-based mounting solutions designed specifically for standing seam metal roofs. Application segmentation includes residential rooftops, commercial buildings, and industrial facilities, each with different system sizes and structural considerations. Commercial and industrial sectors collectively account for the majority of installations because these buildings often feature expansive metal roof structures suitable for solar deployment. End-user segmentation highlights adoption across manufacturing plants, logistics warehouses, retail complexes, and residential properties. Increasing electrification of buildings and corporate sustainability initiatives are encouraging rooftop solar installations across these sectors, creating sustained demand for specialized mounting systems designed to integrate safely and efficiently with metal roof structures.

Metal roof solar mounting systems are commonly categorized into rail-based mounting systems, rail-less mounting systems, and clamp-based mounting systems designed for standing seam metal roofs. Rail-based mounting systems currently represent the leading segment with approximately 46% of total installations. These systems are widely used in commercial projects due to their structural stability and ability to support large solar arrays across wide rooftop surfaces. Rail-based systems also allow flexible panel positioning, making them suitable for industrial rooftops with varying structural layouts. Rail-less mounting systems are emerging as the fastest-growing type, expanding at an estimated 14% annual growth rate as installers prioritize simplified installation designs. These systems eliminate long metal rails and instead use direct panel attachments to mounting brackets, reducing material usage and improving installation speed. Clamp-based mounting systems designed specifically for standing seam metal roofs represent approximately 32% of installations, particularly in industrial and warehouse facilities where non-penetrative mounting is required to maintain roof integrity.

• A 2024 engineering assessment conducted on large commercial rooftop solar projects found that rail-less mounting systems reduced installation component counts by nearly 38%, significantly improving installation efficiency.

The Metal Roof Solar Mounting Systems Market serves residential, commercial, and industrial applications, each representing different installation scales and system requirements. Commercial buildings represent the largest application segment with approximately 41% adoption, driven by solar installations on office buildings, shopping centers, and logistics warehouses. Commercial facilities often possess large metal roofing structures capable of supporting solar systems ranging from 100 kW to 2 MW. Industrial facilities are the fastest-growing application segment, expanding at roughly 13% annual adoption growth as manufacturing companies deploy rooftop solar arrays to reduce electricity costs. Industrial facilities frequently install solar systems exceeding 1 MW capacity, making them major users of heavy-duty mounting systems. Residential installations account for roughly 27% of the market, particularly in regions where metal roofing is widely used in suburban housing developments. In 2025, approximately 37% of commercial property owners globally reported plans to expand rooftop solar installations, while nearly 44% of industrial facility managers identified onsite solar generation as a key energy cost-reduction strategy.

• A large commercial logistics park project implemented rooftop solar systems across multiple warehouses, generating over 18 MW of combined electricity capacity and significantly reducing facility energy consumption.

End-users in the Metal Roof Solar Mounting Systems Market include manufacturing industries, logistics and warehousing companies, commercial real estate operators, and residential homeowners. Manufacturing facilities represent the largest end-user segment with nearly 38% adoption, as factories typically operate energy-intensive machinery and benefit from onsite renewable energy generation. These facilities often install solar arrays across expansive rooftops exceeding 20,000 square meters, making them ideal for mounting system deployment. Logistics and warehousing operators are the fastest-growing end-user segment, experiencing approximately 15% annual adoption growth as e-commerce companies expand distribution networks. Warehouses frequently integrate rooftop solar to power automated sorting systems and refrigeration units. Commercial real estate operators account for roughly 29% of installations, particularly across shopping centers and office complexes seeking to reduce operational energy costs. In 2025, nearly 40% of logistics facility developers incorporated rooftop solar systems into new warehouse designs, while approximately 35% of manufacturing companies reported active solar installation programs across production sites.

• A multi-facility industrial solar deployment across distribution centers reduced grid electricity consumption by over 30%, demonstrating the economic viability of rooftop solar mounting systems in logistics operations.

North America accounted for the largest market share at 36.4% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12.8% between 2026 and 2033.

The regional distribution of the Metal Roof Solar Mounting Systems Market reflects differences in rooftop solar penetration, industrial infrastructure, and renewable energy policies. North America installed more than 9.5 GW of commercial rooftop solar capacity in 2025, with metal-roof warehouses representing nearly 48% of rooftop solar installations in the United States and Canada. Europe followed with approximately 28.1% market share, supported by strong solar adoption in Germany, France, and the United Kingdom where rooftop solar capacity exceeded 75 GW combined installations. Asia-Pacific represented about 23.7% of global demand in 2025, driven by expanding manufacturing facilities and industrial rooftops across China, India, and Japan. Meanwhile, South America accounted for nearly 6.2% share, supported by distributed solar expansion in Brazil and Argentina. The Middle East & Africa region represented around 5.6% share, with rising solar adoption in countries such as the UAE and South Africa where commercial rooftop installations increased by more than 18% year-over-year in 2025. Regional growth dynamics are strongly influenced by industrial building construction, renewable energy incentives, and increasing corporate sustainability commitments, particularly in sectors like logistics, automotive manufacturing, and retail infrastructure.

North America held approximately 36.4% share of the global Metal Roof Solar Mounting Systems Market in 2025, making it the largest regional market. The United States accounted for nearly 79% of regional installations, while Canada contributed around 14%. Commercial and industrial sectors represent the primary drivers of demand, with logistics warehouses, retail distribution centers, and manufacturing facilities accounting for more than 61% of rooftop solar installations across the region. In 2025, North America deployed more than 3.8 GW of rooftop solar capacity on commercial buildings, many of which utilize metal roof mounting systems due to their non-penetrative clamp technology. Regulatory support plays a major role in market expansion. Federal tax credits covering 30% of solar project costs, along with state-level renewable portfolio standards across 29 U.S. states, have accelerated rooftop solar adoption. Technological innovation is also transforming installation processes, including rail-less mounting architectures that reduce installation components by 35% and improve installation speed by nearly 20%. One notable player, Unirac, has expanded its mounting technology portfolio by introducing lightweight aluminum rail systems capable of supporting higher wind load resistance exceeding 160 km/h, improving structural reliability for large rooftop installations. Regional consumer behavior shows distinct characteristics. North American enterprises increasingly deploy rooftop solar to achieve ESG targets and energy cost reductions, with corporate facilities aiming to reduce building electricity costs by 15–25% through onsite renewable generation.

Europe accounted for approximately 28.1% of the global Metal Roof Solar Mounting Systems Market in 2025, supported by widespread rooftop solar deployment across commercial and industrial buildings. Germany, the United Kingdom, and France represent the largest national markets, collectively contributing nearly 63% of regional demand. Germany alone installed more than 2.4 GW of new commercial rooftop solar capacity in 2025, with metal-roof industrial buildings representing approximately 45% of installations. Regulatory initiatives strongly influence adoption across the region. The European Green Deal and national energy transition programs have encouraged solar deployment on commercial rooftops, while new building codes in countries like France require solar installations on commercial buildings larger than 500 square meters. These policies have significantly expanded the addressable market for metal roof mounting systems. Technological innovation is also shaping the regional market. European installers are adopting modular mounting kits and rail-less installation designs capable of reducing installation time by nearly 22%. Digital engineering tools used in system planning have improved installation accuracy and reduced structural load analysis time by approximately 18%. One example of regional innovation is Schletter Group, which has introduced high-strength aluminum mounting structures designed for extreme wind resistance exceeding 150 km/h, particularly suitable for large industrial rooftops. Regional consumer behavior reflects regulatory influence. Across Europe, organizations increasingly prioritize compliance with sustainability regulations, leading to higher demand for energy-efficient infrastructure integrated directly into building design.

Asia-Pacific represents one of the fastest expanding markets for metal roof solar mounting systems, accounting for approximately 23.7% of global demand in 2025. China dominates regional consumption with nearly 54% share of installations, followed by India at 16% and Japan at approximately 12%. Rapid industrialization and large-scale manufacturing facilities are driving the installation of rooftop solar systems across factory complexes and logistics hubs. In 2025, more than 6.5 GW of rooftop solar capacity was installed across industrial buildings in Asia-Pacific, many of which utilize metal roofing structures common in manufacturing plants and warehouse facilities. China alone operates more than 1.4 million industrial buildings with metal roofs, representing a massive potential market for solar mounting systems. Infrastructure development is another major driver. Governments across Asia-Pacific have introduced solar incentives encouraging rooftop installations in industrial parks and export manufacturing zones. India’s rooftop solar program targets more than 40 GW of distributed solar capacity, with a large portion installed on industrial rooftops. Regional innovation hubs are also contributing to market growth. Japan and South Korea are developing high-strength lightweight aluminum mounting components designed to withstand seismic activity and typhoon-level winds. A regional example includes K2 Systems, which has expanded production capacity in Asia to supply modular mounting kits optimized for industrial rooftop solar installations. Consumer behavior in Asia-Pacific is strongly influenced by cost efficiency and industrial energy independence, with manufacturing companies increasingly installing rooftop solar to reduce electricity expenses by 20–30%.

South America accounted for approximately 6.2% share of the global Metal Roof Solar Mounting Systems Market in 2025, driven primarily by the rapid expansion of distributed solar programs in Brazil and Argentina. Brazil alone represented nearly 58% of regional installations, while Argentina accounted for approximately 17%. The expansion of rooftop solar across industrial warehouses, agricultural facilities, and retail infrastructure has significantly increased demand for metal roof mounting systems. The energy sector is undergoing transformation as countries diversify electricity generation away from fossil fuels. Brazil’s distributed solar program has supported the installation of more than 25 GW of small-scale solar capacity, with commercial rooftops representing a substantial portion of installations. Industrial facilities in Brazil frequently feature large metal roofs exceeding 15,000 square meters, making them ideal environments for solar deployment. Government incentives such as tax exemptions for distributed solar equipment and simplified grid interconnection policies have accelerated rooftop solar adoption across the region. Additionally, trade policies supporting solar component imports have reduced installation costs by nearly 12% over the past five years. Regional companies are expanding installation capabilities. For instance, Solar Group Brazil has developed large-scale rooftop solar projects across logistics warehouses capable of generating 1–3 MW of electricity per facility. Consumer behavior in South America is closely linked to energy cost volatility, encouraging businesses to adopt rooftop solar as a long-term strategy to stabilize electricity expenses.

The Middle East & Africa region accounted for approximately 5.6% share of the global Metal Roof Solar Mounting Systems Market in 2025, with demand largely concentrated in the United Arab Emirates, Saudi Arabia, and South Africa. Rapid expansion of commercial infrastructure and industrial zones is supporting rooftop solar adoption across the region. In 2025, the UAE installed more than 350 MW of rooftop solar capacity, much of which was deployed on metal-roof commercial buildings and logistics centers. Energy diversification initiatives in oil-producing economies are accelerating renewable energy adoption. Countries such as Saudi Arabia have announced renewable energy targets exceeding 50% clean electricity generation by 2030, creating demand for distributed solar installations. Industrial construction across logistics parks and free economic zones is also expanding the available rooftop infrastructure for solar installations. Technological modernization is playing a role in regional adoption. Advanced mounting systems designed to withstand extreme temperatures exceeding 50°C and high wind conditions are increasingly deployed in desert environments. A regional example includes Al Shirawi Solar, which has implemented large-scale rooftop solar installations across manufacturing facilities in Dubai industrial zones, deploying systems capable of producing more than 5 MW of electricity per facility. Regional consumer behavior reflects energy diversification strategies and rising electricity demand, encouraging commercial enterprises to integrate rooftop solar systems as part of sustainability and cost-reduction initiatives.

United States – 31.2% Market Share: Dominance driven by strong commercial rooftop solar deployment, large warehouse infrastructure exceeding 1.2 billion square feet, and supportive federal renewable energy incentives.

China – 24.6% Market Share: Leadership supported by massive industrial manufacturing infrastructure, over 1.4 million metal-roof industrial buildings, and aggressive distributed solar installation programs.

The Metal Roof Solar Mounting Systems Market features a moderately fragmented competitive structure, with more than 70 active global and regional manufacturers producing specialized rooftop solar mounting components. The top five companies collectively account for approximately 38–42% of global market share, indicating strong competition among both established engineering companies and specialized solar infrastructure manufacturers.

Leading companies compete primarily through product innovation, lightweight structural design, and installation efficiency improvements. Rail-less mounting architectures, corrosion-resistant aluminum alloys, and modular installation kits are becoming major competitive differentiators. Manufacturers are also focusing on wind-resistant structural engineering, with modern mounting systems capable of supporting solar arrays under wind speeds exceeding 160 km/h.

Strategic partnerships between solar developers, engineering firms, and mounting system manufacturers are increasing. Over the past three years, more than 25 strategic collaborations have been formed globally to integrate mounting technologies with large commercial solar installations. Product launches are another important strategy; nearly 18 new mounting system designs were introduced between 2024 and 2025 featuring improved load tolerance and simplified installation structures.

Digital engineering tools are also transforming competition. Companies increasingly deploy AI-assisted structural modeling and automated design software, reducing installation planning time by nearly 20% and improving project deployment efficiency.

Regional expansion is another competitive strategy. Several mounting system manufacturers have expanded production capacity across Asia and Europe to meet rising demand from industrial rooftop solar installations. These strategies collectively intensify competition while accelerating innovation across the Metal Roof Solar Mounting Systems Market.

Schletter Group

K2 Systems

IronRidge

Mounting Systems GmbH

Clenergy

SunModo Corp.

Van der Valk Solar Systems

EcoFasten Solar

SolarRoofHook

Renusol

Xiamen Grace Solar Technology Co., Ltd.

Tata Power Solar Systems Ltd.

Technological innovation is significantly reshaping the Metal Roof Solar Mounting Systems Market as manufacturers focus on improving structural durability, installation efficiency, and compatibility with diverse roof designs. One of the most significant advancements involves rail-less mounting technologies, which eliminate long aluminum rails traditionally used to support solar panels. Rail-less systems reduce component counts by nearly 35–40%, simplifying installation and reducing labor time by approximately 20%.

Another major technological trend involves clamp-based mounting systems designed specifically for standing seam metal roofs. These systems allow installers to attach solar panels without penetrating the roof surface, preserving roof integrity and minimizing maintenance requirements. Modern clamp designs can support loads exceeding 5400 Pa, enabling installations in high-wind and heavy-snow regions.

Materials innovation is also transforming the market. High-strength aluminum alloys and stainless steel components now dominate mounting system production, accounting for more than 70% of structural materials used in rooftop mounting infrastructure. These materials provide corrosion resistance and reduce system weight by nearly 25% compared with earlier steel mounting structures.

Digital engineering technologies are becoming increasingly important. AI-driven structural simulation software allows installers to evaluate load distribution, wind resistance, and panel orientation before installation. These tools reduce design errors by nearly 22% and accelerate permitting processes for commercial rooftop solar installations.

Prefabricated mounting kits represent another emerging technology trend. Pre-assembled components simplify installation workflows and reduce on-site assembly time by approximately 18%. These kits are particularly useful for large commercial rooftop solar installations exceeding 500 kW capacity, where installation efficiency significantly impacts project timelines.

In addition, integrated cable management systems and grounding technologies are being incorporated directly into mounting structures. These integrated solutions reduce wiring complexity and improve system safety. As rooftop solar installations continue expanding globally, advanced mounting technologies will play a crucial role in improving installation efficiency, structural reliability, and long-term system performance.

• In February 2025, Unirac integrated its U-Builder plan-set platform with Scanifly’s drone-based solar design software, enabling automatic transfer of roof measurements, structural data, and CAD files directly into mounting system design workflows. Installers reported 1–3 hours reduction in design time and 2–4 hours reduction in installation preparation per project. Source: www.unirac.com

• In January 2024, Unirac expanded its strategic partnership with S-5!, a leading manufacturer of metal roof solar attachment solutions. The collaboration extended UL 2703 certifications for S-5! clamps and brackets so they are officially approved for use with Unirac NXT UMOUNT® and SolarMount® systems, improving regulatory compliance and simplifying permitting for rooftop solar installations.

• In July 2024, Unirac introduced domestic-content solar mounting systems manufactured in the United States, enabling installers to qualify for the 10% Domestic Content Bonus Credit under the Inflation Reduction Act (IRA). The product lineup includes U.S.-manufactured rails, attachments, and clamps designed for residential and commercial rooftop solar installations.

• In April 2025, Unirac announced pricing adjustments across its solar mounting product portfolio, reflecting increases in aluminum and steel costs. The company implemented product-specific price changes ranging from 5% to 18%, while maintaining supply commitments and manufacturing of domestically produced mounting components.

The Metal Roof Solar Mounting Systems Market Report provides a comprehensive analysis of the global industry covering key market segments, technology developments, and regional demand dynamics. The report evaluates market activity across five major geographic regions, including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting differences in rooftop solar adoption and industrial infrastructure development.

The scope of the report includes segmentation by mounting system type, application, and end-user industry. Key product categories covered include rail-based mounting systems, rail-less mounting systems, and clamp-based solutions designed for standing seam metal roofs. These technologies support solar installations across a wide range of building structures including commercial warehouses, manufacturing facilities, retail complexes, agricultural buildings, and residential homes. The report also analyzes installation environments and project scales. Commercial rooftop solar installations typically range between 100 kW and 2 MW, while industrial rooftop installations frequently exceed 1 MW capacity due to larger roof surface areas. Industrial buildings with metal roofing structures often exceed 20,000–50,000 square meters, creating large opportunities for mounting system deployment. In addition to structural components, the report evaluates technological integration trends including AI-assisted structural design software, prefabricated mounting kits, and advanced clamp technologies. These innovations reduce installation complexity and improve project efficiency across large solar installations.

The report also examines demand trends across multiple industries including manufacturing, logistics, retail infrastructure, energy utilities, and residential construction. Industrial facilities and logistics warehouses represent a significant portion of installations due to their expansive metal rooftop infrastructure. Furthermore, the report provides insights into regulatory frameworks, renewable energy incentives, and corporate sustainability initiatives influencing rooftop solar deployment globally. It also explores emerging opportunities in distributed solar energy systems, smart building integration, and energy-efficient infrastructure development.

Overall, the Metal Roof Solar Mounting Systems Market Report provides a comprehensive view of technological advancements, installation trends, and industrial adoption patterns shaping the global rooftop solar mounting systems industry.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 130.0 Million |

| Market Revenue (2033) | USD 310.6 Million |

| CAGR (2026–2033) | 11.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Unirac Inc.; Schletter Group; K2 Systems; IronRidge; Mounting Systems GmbH; Clenergy; SunModo Corp.; Van der Valk Solar Systems; EcoFasten Solar; SolarRoofHook; Renusol; Xiamen Grace Solar Technology Co., Ltd.; Tata Power Solar Systems Ltd. |

| Customization & Pricing | Available on Request (10% Customization Free) |