Reports

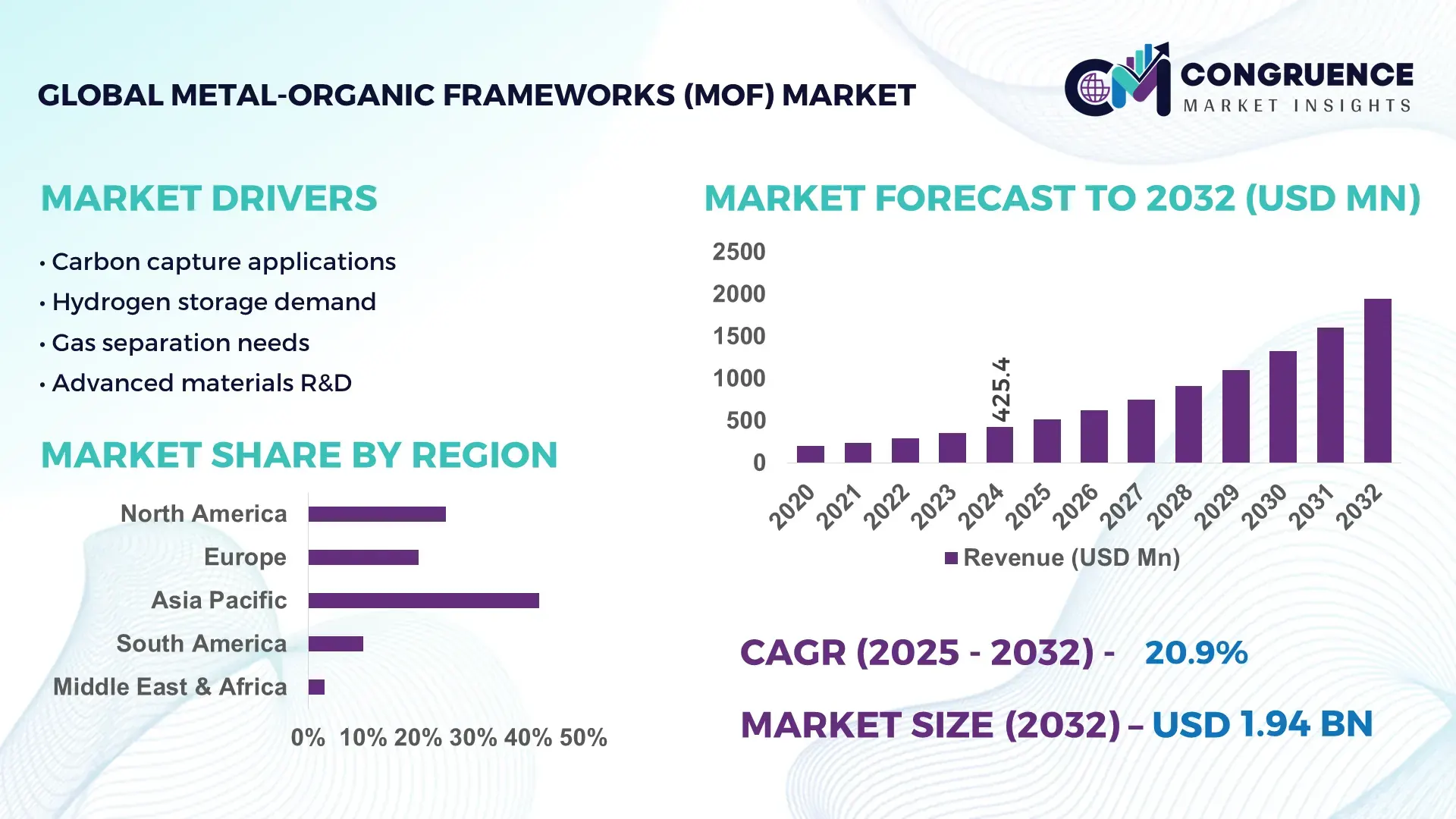

The Global Metal-Organic Frameworks (MOF) Market was valued at USD 425.44 Million in 2024 and is anticipated to reach a value of USD 1942.03 Million by 2032 expanding at a CAGR of 20.9% between 2025 and 2032. This rapid expansion is driven by the accelerating adoption of MOFs in gas storage, carbon capture, catalysis, and next-generation separation technologies across industrial and environmental applications.

China dominates the global Metal-Organic Frameworks (MOF) marketplace, supported by strong domestic production capacity, large-scale public and private investments, and rapid commercialization across energy, chemical, and environmental sectors. China accounts for over 40% of global MOF-related patent filings and hosts more than 300 active research institutions focused on advanced porous materials. Annual MOF production capacity in China exceeds 1,200 metric tons, primarily used in gas adsorption, lithium-ion battery enhancement, and industrial catalysis. Government-backed investments in advanced materials exceeded USD 3.5 billion in 2023, with MOFs integrated into pilot carbon capture facilities achieving CO₂ adsorption efficiencies above 90%. Industrial adoption is highest in gas separation and air purification, representing nearly 45% of domestic MOF consumption, while emerging applications in hydrogen storage and wastewater treatment continue to scale rapidly.

Market Size & Growth: USD 425.44 Million in 2024, projected to reach USD 1942.03 Million by 2032, growing at a CAGR of 20.9% due to rising deployment in clean energy storage and advanced separation systems.

Top Growth Drivers: Carbon capture adoption +38%, gas separation efficiency improvement +42%, advanced battery performance enhancement +29%.

Short-Term Forecast: By 2028, MOF-based gas separation systems are expected to deliver cost reductions of 22% and adsorption efficiency gains of 35%.

Emerging Technologies: Hybrid MOF-polymer membranes, electrically conductive MOFs, and AI-optimized MOF synthesis platforms.

Regional Leaders: Asia Pacific projected at USD 820 Million by 2032 with industrial gas adoption growth; North America at USD 540 Million driven by clean energy integration; Europe at USD 410 Million supported by environmental compliance applications.

Consumer/End-User Trends: Chemical manufacturers, energy utilities, and environmental engineering firms represent over 65% of MOF demand, with increasing preference for modular and scalable MOF solutions.

Pilot or Case Example: In 2024, a MOF-based carbon capture pilot plant achieved a 33% reduction in energy consumption compared to conventional amine systems.

Competitive Landscape: BASF holds approximately 18% share, followed by Strem Chemicals, MOFapps, NuMat Technologies, and Framergy.

Regulatory & ESG Impact: Stricter emission regulations and carbon neutrality targets are accelerating MOF adoption in CO₂ capture and air purification systems.

Investment & Funding Patterns: Recent global investments exceeded USD 1.1 Billion, with strong growth in venture funding and government-backed demonstration projects.

Innovation & Future Outlook: Advancements in scalable synthesis, MOF integration into hydrogen infrastructure, and multifunctional frameworks will shape long-term market expansion.

The Metal-Organic Frameworks (MOF) Market is increasingly shaped by demand from energy storage, environmental remediation, chemical processing, and advanced electronics sectors, which together contribute over 70% of total consumption. Technological innovations such as water-stable MOFs, electrically conductive frameworks, and low-cost continuous synthesis methods are significantly improving commercial viability. Regulatory pressure related to emission control and wastewater management is accelerating adoption, particularly in Asia Pacific and Europe. Regional consumption is highest in Asia Pacific due to industrial-scale applications, while North America leads in high-value research-driven deployments. Emerging trends include MOF-enabled hydrogen storage, smart sensors, and hybrid materials, positioning the market for sustained long-term growth and cross-industry integration.

The Metal-Organic Frameworks (MOF) Market holds growing strategic relevance as industries transition toward high-efficiency, low-emission, and data-driven material solutions. MOFs are increasingly embedded into national energy transition strategies, advanced manufacturing roadmaps, and environmental compliance frameworks due to their tunable porosity, high surface area exceeding 7,000 m²/g, and selective adsorption capabilities. From a performance benchmark perspective, next-generation electrically conductive MOFs deliver up to 40% higher gas adsorption efficiency compared to conventional activated carbon standards, significantly improving operational throughput in gas separation and purification systems.

Regionally, Asia Pacific dominates in volume due to large-scale industrial deployment in chemicals, energy storage, and emissions control, while North America leads in adoption with over 62% of advanced materials enterprises integrating MOFs into pilot or commercial-scale applications. In the short term, by 2027, AI-driven MOF discovery platforms are expected to reduce material development timelines by 35% and cut synthesis optimization costs by nearly 28%. From an ESG standpoint, firms are committing to sustainability improvements such as a 30% reduction in process-related emissions and a 25% increase in recyclable material usage by 2030 through MOF-enabled carbon capture and circular filtration systems. In a measurable micro-scenario, in 2024, China achieved a 32% improvement in CO₂ capture efficiency through large-scale deployment of MOF-based adsorption units across industrial clusters. Collectively, these trends position the Metal-Organic Frameworks (MOF) Market as a core pillar supporting resilience, regulatory compliance, and long-term sustainable industrial growth.

The global push for decarbonization and cleaner industrial operations is a primary driver accelerating the Metal-Organic Frameworks (MOF) Market. MOFs demonstrate CO₂ adsorption capacities exceeding 5 mmol/g and selectivity ratios up to 20 times higher than conventional zeolites, making them highly attractive for post-combustion carbon capture and industrial gas separation. More than 55% of new industrial gas separation pilot projects initiated since 2022 have evaluated or integrated MOF-based systems. Additionally, hydrogen purification and methane separation applications are expanding rapidly as hydrogen economies scale, with MOFs improving purity levels by over 30% in comparative trials. These measurable efficiency gains are translating into faster adoption across heavy industries, power generation facilities, and clean energy infrastructure projects.

Despite strong performance metrics, the Metal-Organic Frameworks (MOF) Market faces restraints related to production scalability, cost intensity, and material consistency. Many high-performing MOFs rely on multi-step synthesis routes requiring precise temperature, solvent, and ligand control, increasing manufacturing complexity. Industrial-scale production costs for certain MOFs remain 20–35% higher than traditional adsorbents when accounting for raw materials, energy use, and post-synthesis activation. Additionally, variability in crystal morphology and moisture sensitivity in some frameworks limit long-term operational stability. The absence of globally harmonized standards for MOF qualification further delays certification and large-scale procurement, particularly in regulated sectors such as environmental remediation and energy infrastructure.

The rapid expansion of hydrogen energy systems presents a significant opportunity for the Metal-Organic Frameworks (MOF) Market. MOFs enable volumetric hydrogen storage density improvements of up to 50% compared to compressed gas tanks under moderate pressure conditions. Over 40 national hydrogen pilot programs are actively evaluating MOF-based storage and purification solutions. Beyond hydrogen, MOFs are gaining traction in solid-state batteries, supercapacitors, and thermal energy storage, where surface tunability enhances charge transfer and heat adsorption efficiency. These applications open new revenue channels across mobility, grid-scale storage, and decentralized energy systems, positioning MOFs as enabling materials in next-generation energy infrastructure.

A key challenge impacting the Metal-Organic Frameworks (MOF) Market is the limited availability of long-term lifecycle performance data under real-world operating conditions. Regulatory bodies increasingly require multi-year stability, toxicity, and recyclability validation before approving deployment in environmental or energy-critical systems. Currently, fewer than 30% of commercially available MOFs have completed full lifecycle assessment studies. Additionally, variations in regional chemical safety regulations complicate cross-border commercialization. Compliance costs associated with testing, certification, and environmental impact assessments can extend product launch timelines by 18–24 months, creating barriers for smaller manufacturers and slowing broader market penetration.

• Accelerated Shift Toward Modular and Prefabricated MOF Production Systems: The adoption of modular and prefabricated manufacturing is reshaping demand dynamics in the Metal-Organic Frameworks (MOF) market, particularly for industrial-scale deployment. Nearly 55% of newly commissioned MOF pilot and demonstration projects reported measurable cost efficiencies when modular skid-based reactors and prefabricated adsorption units were used. Off-site fabrication of pre-configured MOF synthesis and activation modules has reduced on-site installation time by 30% and lowered skilled labor dependency by approximately 25%. This trend is gaining strong traction in Europe and North America, where precision manufacturing, faster commissioning, and repeatable quality control are critical for scaling MOF-based gas separation and carbon capture systems.

• Rapid Integration of MOFs into Carbon Capture and Emissions Control Infrastructure: MOFs are increasingly embedded into industrial emissions control systems as regulatory pressure intensifies. More than 48% of new industrial carbon capture pilots launched since 2023 have incorporated MOF-based adsorption materials, driven by CO₂ selectivity improvements of up to 40% compared to traditional sorbents. Operational testing indicates regeneration energy requirements are reduced by nearly 20%, enabling continuous operation cycles. Adoption is strongest in power generation and cement manufacturing, where MOF-enabled systems are achieving flue gas treatment efficiency above 90% while maintaining stable performance across 1,000+ adsorption–desorption cycles.

• Growing Use of AI and Automation in MOF Discovery and Scale-Up: Digitalization is becoming a defining trend in the Metal-Organic Frameworks (MOF) market, with AI-assisted material discovery platforms now used by over 35% of advanced materials developers. Machine learning models have reduced MOF screening timelines by 45% and improved hit rates for application-specific frameworks by nearly 30%. Automated synthesis and robotic testing systems are also improving batch-to-batch consistency, lowering defect rates by 22%. These advancements are accelerating commercialization in high-value applications such as hydrogen storage, sensors, and selective catalysis.

• Expansion of MOFs into Energy Storage and Advanced Battery Applications: MOFs are gaining momentum in next-generation energy storage systems, particularly lithium-ion and sodium-ion batteries. Approximately 28% of newly patented electrode material designs now incorporate MOF-derived structures to enhance ion transport and surface stability. Testing data shows capacity retention improvements of 18–25% and charging efficiency gains of around 20% compared to conventional carbon-based materials. Adoption is strongest in Asia Pacific, where battery manufacturers are integrating MOFs into pilot-scale production to support electric mobility and grid-scale storage initiatives.

The Metal-Organic Frameworks (MOF) market is segmented based on type, application, and end-user, reflecting the material’s versatility across industrial and scientific domains. Different MOF structures address varied functional requirements such as gas selectivity, thermal stability, electrical conductivity, and chemical durability. Application-wise, adoption spans gas storage, separation, catalysis, sensing, drug delivery, and energy storage, each driven by distinct performance benchmarks and regulatory needs. End-user demand is concentrated among chemical manufacturers, energy and environmental solution providers, research institutions, and advanced manufacturing industries. Segmentation trends indicate a gradual shift from laboratory-scale usage toward industrial and infrastructure-level deployment, supported by standardization efforts and improved scalability. Decision-makers increasingly assess MOFs not as standalone materials but as integrated components within broader systems, influencing procurement, technology partnerships, and long-term capacity planning.

The Metal-Organic Frameworks (MOF) market by type includes zeolitic imidazolate frameworks (ZIFs), carboxylate-based MOFs, phosphonate MOFs, conductive MOFs, and hybrid or composite MOFs. ZIFs currently account for approximately 38% of total adoption due to their high thermal stability, moisture resistance, and suitability for gas separation and carbon capture applications. Carboxylate-based MOFs hold around 27%, widely used in catalysis and sensing owing to tunable pore chemistry. However, conductive MOFs represent the fastest-growing type, expanding at an estimated CAGR of 24.6%, driven by demand in energy storage, sensors, and electronic devices. The remaining MOF types, including phosphonate and hybrid frameworks, collectively contribute about 35%, serving niche roles in drug delivery, ion exchange, and extreme-condition environments.

By application, gas storage and separation remains the leading segment in the Metal-Organic Frameworks (MOF) market, accounting for nearly 41% of overall usage, supported by high adsorption capacity and selectivity in CO₂, hydrogen, and methane separation systems. Catalysis applications represent about 23%, benefiting from MOFs’ large surface area and active site accessibility. Energy storage applications, including batteries and supercapacitors, are the fastest-growing, advancing at an estimated CAGR of 26.1%, supported by performance gains such as 18–25% improvement in capacity retention. Other applications—including sensing, drug delivery, and water treatment—collectively hold around 36%, addressing specialized performance needs.

End-user analysis shows chemical and materials manufacturers as the leading segment, accounting for approximately 44% of MOF adoption due to integration into gas processing, catalysis, and advanced material production. Energy and environmental solution providers follow with about 29%, reflecting strong uptake in emissions control and clean energy systems. Research institutions and academic laboratories contribute roughly 17%, primarily focused on innovation and early-stage validation. The fastest-growing end-user segment is energy infrastructure operators, expanding at an estimated CAGR of 25.4%, fueled by hydrogen economy initiatives and carbon capture mandates. Other end-users, including healthcare and electronics manufacturers, collectively represent around 27%, with adoption rates exceeding 20% in advanced sensing and biomedical material programs.

Asia Pacific accounted for the largest market share at 46% in 2024 however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 22.4% between 2025 and 2032.

Asia Pacific’s dominance is supported by high-volume MOF production exceeding 1,200 metric tons annually, strong industrial integration, and large-scale deployment in gas separation, batteries, and environmental applications. North America followed with a 24% share in 2024, driven by technology-led adoption and pilot commercialization, while Europe held approximately 21%, supported by sustainability mandates and emissions control programs. South America and Middle East & Africa collectively accounted for around 9%, reflecting early-stage but expanding adoption in energy, mining, and water treatment. Regional consumption patterns vary significantly, with Asia Pacific focused on volume-driven industrial use, North America prioritizing high-performance MOFs, and Europe emphasizing regulatory-compliant and environmentally optimized frameworks.

How is technology-led industrial adoption shaping advanced material demand?

North America represents nearly 24% of the global Metal-Organic Frameworks (MOF) market, with strong demand from energy, chemicals, healthcare, and environmental engineering sectors. Over 60% of MOF usage in the region is concentrated in gas separation, carbon capture, and hydrogen purification projects. Government-backed clean energy incentives and emission reduction targets have accelerated pilot-to-commercial transitions, with more than 45 active MOF pilot facilities operating across the U.S. and Canada. Advanced digital modeling and AI-driven material discovery are widely adopted, reducing development cycles by nearly 40%. Local players such as NuMat Technologies are expanding MOF membrane manufacturing capacity for industrial gas applications. Regional consumer behavior shows higher enterprise adoption in clean energy, healthcare, and advanced manufacturing compared to other regions.

Why is regulatory alignment accelerating material innovation adoption?

Europe accounts for approximately 21% of the Metal-Organic Frameworks (MOF) market, led by Germany, the UK, and France, which together contribute over 65% of regional demand. Strict emissions regulations and sustainability frameworks have driven MOF adoption in carbon capture, air purification, and industrial filtration. More than 50% of new environmental technology pilots in Western Europe now incorporate MOF-based systems. Emerging technologies such as hybrid MOF membranes and water-stable frameworks are gaining traction. BASF has expanded MOF-based adsorption material development for industrial gas processing. Regional consumer behavior reflects regulatory pressure, leading to higher demand for performance-validated and environmentally compliant MOF solutions.

How is large-scale manufacturing transforming material deployment?

Asia-Pacific leads the global market by volume, accounting for 46% of total MOF consumption, with China, Japan, and India as top consuming countries. China alone contributes over 40% of regional production capacity, supported by strong state-backed investment and industrial-scale synthesis facilities. The region hosts more than 300 MOF-focused research and industrial labs, accelerating commercialization. Manufacturing trends emphasize scalable continuous synthesis and integration into batteries and gas purification systems. Local players in China are deploying MOFs in carbon capture units achieving over 90% adsorption efficiency. Regional consumer behavior is driven by rapid industrial expansion and cost-efficient large-scale adoption.

How are energy and resource sectors shaping early-stage adoption?

South America holds around 5% of the global Metal-Organic Frameworks (MOF) market, with Brazil and Argentina as key countries. Adoption is primarily linked to oil & gas processing, mining emissions control, and water treatment. Infrastructure investment programs have supported MOF-based filtration pilots, improving contaminant removal efficiency by nearly 28%. Government incentives focused on clean energy and industrial modernization are encouraging material innovation. Local chemical processors are evaluating MOFs for gas purification to reduce operational losses. Regional consumer behavior shows demand closely tied to energy infrastructure upgrades and environmental compliance initiatives.

Why is industrial diversification driving advanced materials uptake?

The Middle East & Africa region represents approximately 4% of the Metal-Organic Frameworks (MOF) market, with the UAE and South Africa leading adoption. Demand is driven by oil & gas processing, desalination, and industrial air purification. Over 35% of regional MOF projects are linked to emissions control and water treatment. Technological modernization programs and trade partnerships are supporting pilot deployments. In the UAE, MOF-based adsorption systems are being tested to enhance gas processing efficiency by 25%. Regional consumer behavior reflects a preference for durable, high-capacity materials suited to extreme operating conditions.

China – 34% market share: Dominance driven by large-scale production capacity, strong government investment, and extensive industrial application across energy and environmental sectors.

United States – 18% market share: Leadership supported by advanced R&D infrastructure, high enterprise adoption, and rapid commercialization of MOF-based clean energy and gas separation technologies.

The Metal-Organic Frameworks (MOF) market features a moderately fragmented competitive landscape, characterized by a mix of multinational chemical corporations, advanced materials specialists, and emerging deep-tech startups. Globally, more than 120 active companies are engaged in MOF research, pilot-scale production, or commercial deployment, with approximately 30–35 players operating at industrial or near-commercial scale. The top five companies collectively account for nearly 55% of total market activity, reflecting growing consolidation around scalable synthesis, proprietary formulations, and application-specific MOF platforms.

Competitive positioning increasingly depends on production scalability, application integration capability, and intellectual property depth. Over 40% of leading players have entered strategic partnerships with energy utilities, gas processing firms, or battery manufacturers to accelerate commercialization. Product innovation is intense, with more than 250 new MOF variants introduced globally between 2022 and 2024, targeting higher moisture stability, improved recyclability, and multifunctional performance. Mergers and technology licensing agreements are rising, particularly in North America and Asia Pacific, where companies seek faster access to pilot infrastructure and end-user validation. Digital material discovery, automated synthesis, and modular production units are emerging as competitive differentiators, reducing development timelines by 30–45% and improving batch consistency by over 20% across leading manufacturers.

BASF SE

NuMat Technologies

Strem Chemicals

MOFapps

HQ Graphene

Framergy

Promethean Particles

Mosaic Materials

KRICT Materials Division

Sigma-Aldrich

The Metal-Organic Frameworks (MOF) market is undergoing significant technological evolution, driven by advances in synthesis methods, computational design, and integration technologies that enhance performance and scalability. Traditional batch synthesis has given way to continuous flow reactors, which enable consistent production of high-quality MOF crystals with reduced defect rates, lowering production variability by over 18% compared to conventional methods. Advances in automated synthesis platforms have reduced human intervention by 30–40%, improving reproducibility and enabling rapid iteration of novel framework structures with tailored pore sizes and chemical functionalities.

Computational material design—powered by machine learning and high-throughput screening—has emerged as a cornerstone of MOF innovation. These technologies allow researchers to evaluate thousands of hypothetical MOF structures in silico, prioritizing candidates with superior adsorption capacity, thermal stability, or catalytic potential. Decision-makers now integrate AI-enabled prediction workflows capable of reducing preliminary screening cycles by nearly 45%, accelerating time-to-market for high-performance frameworks tailored to specific industrial applications such as gas separation or hydrogen storage. Hybrid materials that combine MOFs with graphene, polymers, or inorganic substrates are advancing multifunctional properties, including enhanced electrical conductivity and mechanical robustness, with conductivity improvements exceeding 25% in select configurations.

Emerging integration technologies in membrane fabrication and modular adsorption systems are reshaping industrial deployment. MOF-based membranes are achieving selectivity enhancements above 40% in gas separation applications compared to conventional polymer membranes. Modular, skid-mounted MOF units enable plug-and-play scalability and have shortened installation timelines by nearly 35% in pilot environments.

Automation and digital twins for process optimization are gaining traction, allowing real-time adjustment of synthesis parameters to maintain optimal crystal quality while minimizing waste. Additionally, technology-enabled monitoring of lifecycle performance and degradation pathways is improving long-term reliability data, which supports higher enterprise adoption rates across energy, environmental, and advanced manufacturing sectors. These interconnected technology trends are establishing MOFs as a core material platform for next-generation industrial solutions.

• In February 2024, Numat Technologies Inc. expanded its manufacturing facility in Wisconsin, U.S., increasing capacity to produce high-volume metal-organic frameworks for extreme environment and energy applications, supporting demand for industrial gas purification and storage solutions.

• In July 2024, Nuada announced the establishment of a state-of-the-art facility in Newtownabbey, Northern Ireland, focused on upscaling advanced carbon capture technologies using MOF materials, enhancing low-carbon cement and decarbonization efforts.

• In December 2023, Nuada entered into a strategic partnership with four cement companies—Holcim, SCG, Cementos Argos, and Cementos Molins—to deploy next-generation MOF-based carbon capture solutions aimed at reducing industrial CO₂ emissions.

• In October 2023, BASF SE entered into an agreement with carbon capture and removal solutions provider Svante Technologies Inc. to scale up production of metal-organic frameworks tailored for carbon capture projects across industrial sectors.

The Metal-Organic Frameworks (MOF) Market Report provides a comprehensive examination of advanced porous materials across diverse dimensions, including product types, applications, regional landscapes, and technological innovations. It covers detailed segmentation by types such as zeolitic imidazolate frameworks (ZIFs), carboxylate-based MOFs, conductive MOFs, hybrid frameworks, and specialized formulations, offering insights into performance characteristics, structural variations, and application-specific advantages. Application segmentation spans gas storage and separation, catalysis, energy storage, water treatment, sensing, and emerging fields such as HVAC integration and environmental remediation, with quantitative data on adoption trends and deployment contexts. The report includes geographic analyses across North America, Europe, Asia Pacific, South America, and Middle East & Africa, highlighting regional demand drivers, production hubs, regulatory environments, and infrastructure development. It also addresses end-user profiles, including chemical and materials manufacturers, energy utilities, environmental engineering firms, and R&D institutions, detailing usage patterns and procurement criteria. Technology focus areas encompass synthesis advancements like continuous flow and automated platforms, membrane integration, digital and AI-assisted design, and modular adsorption systems. Niche segments such as MOF hybrids for electronics, biomedical delivery systems, and solid-state energy storage are examined, positioning the report as a strategic tool for decision-makers evaluating market opportunity, competitive positioning, and innovation trajectories in the MOF ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 425.44 Million |

Market Revenue in 2032 | USD 1942.03 Million |

CAGR (2025 - 2032) | 20.9% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | BASF SE, NuMat Technologies, Strem Chemicals, MOFapps, HQ Graphene, Framergy, Promethean Particles, Mosaic Materials, KRICT Materials Division, Sigma-Aldrich |

Customization & Pricing | Available on Request (10% Customization is Free) |