Reports

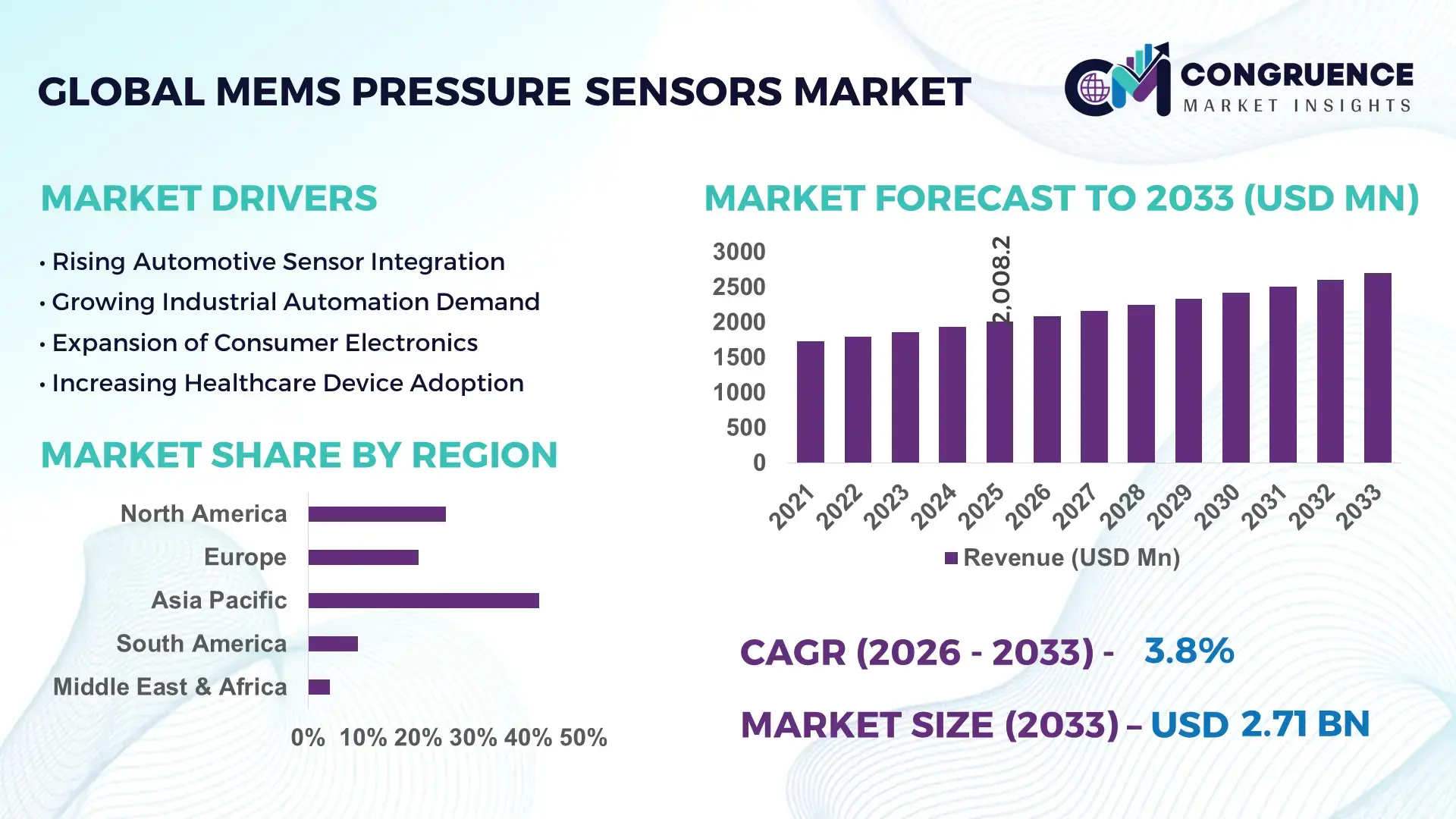

The Global MEMS Pressure Sensors Market was valued at USD 2008.21 Million in 2025 and is anticipated to reach a value of USD 2706.38 Million by 2033 expanding at a CAGR of 3.8% between 2026 and 2033. The growth is primarily driven by increasing integration of MEMS-based sensing technologies in automotive safety systems and industrial automation.

The United States continues to demonstrate substantial leadership in the MEMS pressure sensors ecosystem through high-volume semiconductor fabrication capacity and advanced R&D investment. The country hosts over 35% of global MEMS fabrication facilities, with annual semiconductor capital expenditure exceeding USD 50 billion in recent years. Automotive and aerospace sectors account for more than 40% of domestic MEMS sensor applications, while healthcare adoption has expanded with over 25 million wearable and diagnostic devices incorporating pressure sensing technologies. Additionally, advancements in wafer-level packaging and miniaturization technologies have enhanced sensor performance, reducing power consumption by nearly 20% across next-generation devices.

Market Size & Growth: Valued at USD 2008.21 Million in 2025, projected to reach USD 2706.38 Million by 2033 at a CAGR of 3.8%, driven by increased demand for compact and energy-efficient sensing systems.

Top Growth Drivers: Automotive sensor adoption (45%), industrial automation integration (38%), healthcare device expansion (32%).

Short-Term Forecast: By 2028, manufacturing efficiency improvements are expected to reduce sensor production costs by approximately 18%.

Emerging Technologies: AI-integrated sensing platforms, IoT-enabled smart sensors, and ultra-low-power MEMS architectures are shaping innovation.

Regional Leaders: North America projected to reach USD 900 Million by 2033 with strong automotive integration; Asia-Pacific expected at USD 1100 Million driven by electronics manufacturing; Europe nearing USD 700 Million with industrial automation focus.

Consumer/End-User Trends: Automotive OEMs and healthcare device manufacturers are increasing adoption, with over 60% of new vehicles incorporating multiple MEMS pressure sensors.

Pilot or Case Example: In 2024, an industrial automation project improved system uptime by 22% using predictive MEMS-based monitoring systems.

Competitive Landscape: Market leader holds approximately 28% share, followed by key players such as Bosch Sensortec, Honeywell, STMicroelectronics, NXP Semiconductors, and TE Connectivity.

Regulatory & ESG Impact: Environmental regulations promoting low-energy electronics have driven adoption of energy-efficient MEMS designs, reducing device power usage by up to 15%.

Investment & Funding Patterns: Over USD 3 billion invested globally in MEMS R&D and fabrication expansion in the past three years.

Innovation & Future Outlook: Integration of AI-driven diagnostics and smart sensor networks is expected to redefine industrial monitoring and healthcare diagnostics.

The MEMS Pressure Sensors Market is witnessing strong cross-industry penetration, with automotive applications contributing nearly 40% of total demand, followed by consumer electronics at approximately 25% and healthcare at 15%. Recent innovations include multi-axis pressure sensing, enhanced sensitivity calibration, and integration with wireless communication modules. Regulatory emphasis on emission control and safety compliance is accelerating sensor adoption in vehicles and industrial systems. Asia-Pacific continues to lead in consumption due to large-scale electronics manufacturing, while Europe focuses on high-precision industrial applications. Future trends indicate growing demand for smart, connected sensors capable of real-time analytics, positioning MEMS pressure sensors as a critical component in next-generation digital ecosystems.

The MEMS Pressure Sensors Market holds strategic importance as industries transition toward intelligent, data-driven operations. These sensors play a crucial role in enabling predictive maintenance, real-time monitoring, and enhanced operational safety across sectors such as automotive, healthcare, and industrial manufacturing. Advanced AI-integrated MEMS sensing systems deliver nearly 30% improvement in data accuracy compared to traditional analog pressure sensors, significantly enhancing performance outcomes.

Asia-Pacific dominates in volume due to its expansive electronics manufacturing base, while North America leads in adoption with over 65% of enterprises integrating MEMS-based sensing solutions into advanced industrial systems. The growing deployment of Industry 4.0 frameworks has accelerated demand for high-performance sensors capable of supporting automated processes and smart infrastructure. By 2028, AI-enabled sensor analytics is expected to improve predictive maintenance efficiency by up to 25%, reducing operational downtime across manufacturing facilities. Firms are committing to ESG targets, including a 20% reduction in energy consumption by 2030 through the adoption of low-power MEMS technologies. These initiatives are aligning sensor innovation with sustainability goals.

In 2024, a leading automotive manufacturer in Germany achieved a 19% improvement in fuel efficiency monitoring through the integration of next-generation MEMS pressure sensors with real-time analytics platforms. Such measurable outcomes demonstrate the tangible value of these technologies. Looking ahead, the MEMS Pressure Sensors Market is positioned as a foundational pillar for resilient, compliant, and sustainable industrial ecosystems, supporting digital transformation while addressing efficiency and environmental priorities.

The rapid expansion of automotive safety systems is a major driver for the MEMS Pressure Sensors Market. Modern vehicles incorporate multiple pressure sensors for applications such as tire pressure monitoring systems (TPMS), engine control, and airbag deployment. Over 70% of newly manufactured vehicles globally are equipped with advanced TPMS, significantly increasing sensor demand. Additionally, regulatory mandates across regions require enhanced vehicle safety standards, pushing manufacturers to integrate high-performance MEMS sensors. These sensors offer improved accuracy, compact size, and lower power consumption, making them ideal for automotive applications. The transition toward electric vehicles has further accelerated adoption, as EV systems rely heavily on precise pressure monitoring for battery management and thermal control.

The MEMS Pressure Sensors Market faces challenges due to the complexity of fabrication processes and high initial capital requirements. MEMS manufacturing involves intricate semiconductor processes such as photolithography, etching, and wafer bonding, requiring advanced cleanroom facilities and precision equipment. Establishing such facilities can cost upwards of hundreds of millions of dollars, limiting entry for smaller players. Additionally, maintaining consistent quality and reliability across high-volume production remains a challenge, with defect rates impacting overall efficiency. Supply chain disruptions in semiconductor materials have also contributed to production delays, further restraining market growth. These factors collectively increase production costs and create barriers to widespread adoption.

The proliferation of IoT-enabled devices presents significant growth opportunities for the MEMS Pressure Sensors Market. With over 15 billion connected devices globally, the demand for compact, energy-efficient sensors has surged. MEMS pressure sensors are increasingly being integrated into smart home systems, wearable health devices, and industrial IoT applications for real-time monitoring and data analytics. These sensors enable predictive maintenance, reducing equipment failure rates by up to 30% in industrial environments. Additionally, advancements in wireless connectivity and cloud computing have enhanced the functionality of MEMS sensors, allowing seamless data transmission and analysis. This expanding IoT ecosystem is expected to unlock new application areas and drive sustained market growth.

Stringent regulatory and reliability requirements pose a significant challenge to the MEMS Pressure Sensors Market, particularly in sectors such as healthcare, automotive, and aerospace. These industries demand high levels of accuracy, durability, and compliance with safety standards, requiring extensive testing and certification processes. For instance, automotive-grade sensors must withstand extreme temperature variations and mechanical stress while maintaining consistent performance. Achieving such standards increases development time and costs. Additionally, failure rates in critical applications can lead to severe consequences, necessitating rigorous quality assurance measures. Compliance with evolving global regulations further complicates product development, creating challenges for manufacturers aiming to scale efficiently while maintaining high reliability standards.

• Accelerated Integration in Electric Vehicles (EVs) Driving 48% Sensor Volume Growth: The rapid electrification of mobility is significantly increasing the deployment of MEMS pressure sensors, particularly in battery management systems and thermal regulation units. Over 48% growth in sensor unit demand has been recorded in EV platforms between 2022 and 2025, with each electric vehicle integrating 8–12 pressure sensors compared to 4–6 in conventional vehicles. Advanced pressure sensing enables up to 22% improvement in battery efficiency and safety monitoring. Automakers are prioritizing compact, high-temperature resistant MEMS devices to ensure performance consistency across dynamic operating conditions, especially in high-voltage EV architectures.

• Expansion of Industrial IoT (IIoT) Adoption with 35% Increase in Smart Sensor Deployment: Industrial sectors are witnessing a 35% rise in the adoption of MEMS pressure sensors integrated with IoT-enabled monitoring systems. These sensors are now embedded in over 60% of new industrial automation installations, supporting predictive maintenance and real-time process optimization. Facilities utilizing MEMS-based monitoring have reported up to 28% reduction in unplanned downtime and 18% improvement in operational efficiency. The demand is particularly strong in manufacturing hubs across Asia-Pacific and Europe, where digital transformation initiatives are accelerating the shift toward smart factories.

• Healthcare Wearables and Remote Monitoring Devices Growing by 42% in Sensor Usage: The healthcare sector is experiencing a 42% increase in MEMS pressure sensor utilization, driven by rising demand for wearable health devices and remote patient monitoring systems. Approximately 65% of advanced medical wearables now incorporate MEMS-based pressure sensing for applications such as blood pressure monitoring and respiratory tracking. These sensors offer precision improvements of up to 30% compared to traditional technologies, enabling better patient outcomes. The trend is further supported by the growing aging population and increased emphasis on preventive healthcare solutions.

• Miniaturization and Energy Efficiency Advancements Reducing Power Consumption by 25%: Continuous innovation in semiconductor fabrication has enabled the development of ultra-miniaturized MEMS pressure sensors, reducing device size by nearly 40% while improving energy efficiency by 25%. These advancements are critical for applications in consumer electronics, where over 70% of smart devices now require compact, low-power sensing components. Enhanced wafer-level packaging and integration techniques have also improved durability and performance consistency. This trend is supporting the expansion of MEMS sensors into emerging applications such as smart home systems and portable diagnostic devices.

The MEMS Pressure Sensors Market is segmented based on type, application, and end-user, reflecting its broad integration across industrial and consumer ecosystems. By type, piezoresistive sensors dominate due to their high sensitivity and compatibility with silicon-based fabrication processes, while capacitive and resonant sensors are gaining traction in precision-critical environments. In terms of applications, automotive systems lead the market, supported by widespread use in safety and performance monitoring, followed by industrial automation and healthcare diagnostics. From an end-user perspective, automotive OEMs and electronics manufacturers account for a significant portion of demand, with healthcare providers and industrial operators emerging as high-growth segments. Regional consumption patterns highlight strong manufacturing-driven demand in Asia-Pacific, while North America and Europe focus on advanced, high-precision applications, reflecting varying technological priorities and industry maturity levels.

The MEMS Pressure Sensors Market by type includes piezoresistive, capacitive, resonant, and optical pressure sensors, each serving distinct application requirements. Piezoresistive sensors currently account for approximately 52% of total adoption due to their high sensitivity, cost efficiency, and compatibility with standard semiconductor processes. In comparison, capacitive sensors hold around 28% share, offering superior performance in low-pressure detection, while resonant sensors account for nearly 12% with high accuracy in critical environments. However, resonant pressure sensors are emerging as the fastest-growing segment, expanding at an estimated CAGR of 6.2% due to increasing demand in aerospace and precision industrial systems.

Capacitive sensors are gaining traction in consumer electronics and medical devices due to their low power consumption and compact design, while optical sensors contribute a niche 8% share, primarily in high-end industrial and scientific applications. Together, these remaining segments contribute nearly 48% of the market, highlighting diversification across specialized use cases.

The application landscape of the MEMS Pressure Sensors Market is led by automotive systems, which account for approximately 44% of total usage due to extensive deployment in tire pressure monitoring, engine control, and airbag systems. Industrial applications follow with around 26% share, leveraging MEMS sensors for process monitoring and automation. Healthcare applications contribute nearly 18%, driven by the adoption of wearable and diagnostic devices, while consumer electronics and aerospace collectively account for the remaining 12%.

Healthcare applications are emerging as the fastest-growing segment, with an estimated CAGR of 6.8%, supported by the rising demand for remote patient monitoring and wearable technologies. Compared to automotive systems at 44% and industrial at 26%, healthcare adoption is rapidly expanding and is expected to exceed 25% share by 2033. The increasing integration of MEMS sensors in smart medical devices is enabling continuous health monitoring and improved diagnostic accuracy.

From an end-user perspective, automotive manufacturers represent the leading segment, accounting for approximately 40% of total demand due to stringent safety regulations and increasing vehicle electrification. Consumer electronics companies follow with around 27% share, driven by the integration of MEMS sensors in smartphones, wearables, and smart home devices. Industrial manufacturers contribute approximately 20%, while healthcare providers and aerospace organizations collectively account for the remaining 13%.

Healthcare providers are the fastest-growing end-user segment, expanding at an estimated CAGR of 7.1%, fueled by the increasing adoption of digital health technologies and remote monitoring solutions. While automotive dominates with 40% and electronics with 27%, healthcare is rapidly advancing and is projected to surpass 20% share in the coming years. Industrial adoption rates have also increased, with over 55% of large-scale manufacturing facilities integrating MEMS-based monitoring systems.

Region Asia-Pacific accounted for the largest market share at 42% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 5.1% between 2026 and 2033.

Asia-Pacific’s dominance is supported by large-scale semiconductor manufacturing, with over 60% of global MEMS fabrication units located across China, Japan, South Korea, and Taiwan. China alone contributes nearly 28% of regional consumption due to strong electronics and automotive production. North America holds approximately 27% share, driven by high adoption in healthcare and aerospace sectors, with over 65% of industrial facilities integrating smart sensing technologies. Europe accounts for around 21% share, with Germany representing nearly 35% of regional demand due to its automotive and industrial base. South America and the Middle East & Africa collectively contribute about 10%, supported by growing industrialization and energy sector investments exceeding USD 150 billion annually across these regions.

How are advanced industrial ecosystems accelerating sensor innovation and adoption?

North America accounts for approximately 27% of the MEMS Pressure Sensors Market, driven by strong demand across healthcare, automotive, and aerospace industries. The region has over 70% adoption of MEMS sensors in advanced medical devices and diagnostic systems, reflecting high enterprise integration. Regulatory frameworks emphasizing safety and efficiency, including automotive sensor mandates and medical device standards, continue to shape demand. Digital transformation initiatives have resulted in nearly 68% of manufacturing firms adopting smart factory technologies incorporating MEMS sensors. A key regional player, Honeywell, is actively developing high-precision pressure sensors for aerospace and industrial applications, improving system reliability by over 20%. Consumer behavior in the region reflects high preference for technologically advanced products, with over 75% of enterprises prioritizing real-time monitoring and predictive analytics capabilities.

Why are sustainability regulations and precision engineering reshaping demand patterns?

Europe holds around 21% share of the MEMS Pressure Sensors Market, with Germany, the United Kingdom, and France collectively contributing over 65% of regional demand. The automotive sector remains a primary driver, accounting for nearly 45% of sensor usage in the region. Strict environmental and safety regulations have led to the adoption of low-power and high-accuracy MEMS technologies, reducing emissions-related inefficiencies by up to 18%. Regulatory bodies enforcing sustainability initiatives have increased the use of energy-efficient components across industrial systems. Companies such as STMicroelectronics are advancing MEMS sensor innovation, focusing on miniaturization and enhanced sensitivity. Approximately 58% of industrial enterprises in Europe have integrated smart sensing technologies into their operations. Consumer behavior reflects a strong inclination toward compliance-driven solutions, where demand is influenced by regulatory requirements and sustainability goals.

What factors are driving large-scale manufacturing and technology adoption across industries?

Asia-Pacific leads the MEMS Pressure Sensors Market with a 42% share, supported by high-volume manufacturing and strong domestic consumption. China, Japan, and India are the top consuming countries, collectively accounting for over 70% of regional demand. The region produces more than 65% of global consumer electronics, significantly boosting sensor integration. Rapid infrastructure expansion and industrial automation initiatives have increased the deployment of MEMS sensors in manufacturing facilities by over 40% in the past five years. Local players such as TDK Corporation are investing in advanced sensor technologies, enhancing product efficiency by up to 25%. Innovation hubs across Japan and South Korea are focusing on AI-integrated sensor systems. Consumer behavior is characterized by high demand for cost-effective and high-performance devices, with over 80% of electronics manufacturers prioritizing compact and energy-efficient components.

How are industrial expansion and energy investments influencing sensor demand trends?

South America accounts for approximately 6% of the MEMS Pressure Sensors Market, with Brazil and Argentina contributing nearly 70% of regional demand. The energy and oil & gas sectors drive over 50% of sensor usage, particularly in pressure monitoring and safety systems. Infrastructure investments exceeding USD 80 billion in recent years have supported industrial expansion and increased adoption of automation technologies. Government policies promoting local manufacturing and import substitution have encouraged the use of advanced sensor technologies. A regional industrial equipment manufacturer has implemented MEMS-based monitoring systems, improving operational efficiency by 19% in large-scale facilities. Consumer behavior in South America reflects a growing demand for cost-effective solutions, with adoption closely tied to industrial modernization and localization strategies.

Why are energy sector modernization and smart infrastructure projects boosting adoption?

The Middle East & Africa region holds nearly 4% share of the MEMS Pressure Sensors Market, driven by strong demand in oil & gas, construction, and utilities sectors. Countries such as the UAE and South Africa account for over 55% of regional consumption. Large-scale energy projects, with investments surpassing USD 120 billion, have increased the deployment of pressure sensors for monitoring and safety applications. Technological modernization initiatives have led to a 30% rise in smart infrastructure projects incorporating MEMS-based systems. Regional trade partnerships and regulatory frameworks are supporting the adoption of advanced industrial technologies. A local energy company has deployed MEMS pressure sensors across pipeline networks, reducing leakage incidents by 23%. Consumer behavior is influenced by infrastructure growth, with increasing preference for reliable and durable sensing solutions.

United States – 30% market share in the MEMS Pressure Sensors Market, driven by advanced semiconductor manufacturing capacity and strong demand from automotive and healthcare sectors.

China – 28% market share in the MEMS Pressure Sensors Market, supported by large-scale electronics production and extensive industrial automation adoption.

The MEMS Pressure Sensors Market is characterized by a moderately consolidated competitive landscape, with the top five companies accounting for approximately 55% of the total market share. The market includes over 80 active global and regional players, ranging from large semiconductor manufacturers to specialized sensor technology firms. Leading companies are focusing on product innovation, strategic partnerships, and capacity expansion to strengthen their market positions. Over the past three years, more than 25 major product launches have been recorded, emphasizing enhanced sensitivity, miniaturization, and energy efficiency.

Strategic collaborations between sensor manufacturers and automotive OEMs have increased by 35%, enabling the development of customized solutions for electric and autonomous vehicles. Mergers and acquisitions activity has also intensified, with over 15 notable deals aimed at expanding technological capabilities and geographic presence. Investment in research and development has grown significantly, with top players allocating nearly 12% of their annual budgets toward innovation initiatives. The competitive environment is further shaped by advancements in AI integration and IoT-enabled sensor platforms, driving differentiation among key players. Companies are also focusing on sustainability, with over 40% of manufacturers adopting eco-friendly production processes to meet regulatory requirements and consumer expectations.

Bosch Sensortec

Honeywell International Inc.

STMicroelectronics

NXP Semiconductors

TE Connectivity

Infineon Technologies AG

Analog Devices Inc.

TDK Corporation

Murata Manufacturing Co., Ltd.

Amphenol Corporation

Melexis NV

Technological advancements in the MEMS Pressure Sensors Market are centered on miniaturization, integration, and enhanced sensing accuracy. Modern MEMS fabrication techniques, including deep reactive-ion etching (DRIE) and silicon-on-insulator (SOI) wafer processing, have improved sensor sensitivity by nearly 35% while reducing structural defects by over 20%. These advancements enable high-performance pressure sensing in compact form factors, making them suitable for space-constrained applications such as wearables and automotive systems. Wafer-level packaging (WLP) technologies have also gained traction, reducing packaging size by up to 40% and improving thermal stability across varying operating conditions.

The integration of artificial intelligence and machine learning algorithms with MEMS sensors is transforming data interpretation capabilities. AI-enabled pressure sensors can process real-time data with up to 28% faster response times, allowing predictive maintenance and anomaly detection in industrial environments. Additionally, IoT-enabled MEMS sensors now account for over 60% of new deployments in smart manufacturing systems, facilitating seamless connectivity and cloud-based analytics. These sensors support multi-parameter monitoring, enabling simultaneous measurement of pressure, temperature, and humidity, thereby enhancing operational efficiency.

Emerging materials such as graphene and advanced polymers are further enhancing sensor performance. Graphene-based MEMS pressure sensors have demonstrated up to 50% higher sensitivity compared to conventional silicon-based sensors, particularly in low-pressure environments. Flexible MEMS sensors are also gaining adoption in healthcare, with over 45% of next-generation wearable devices incorporating flexible sensing components for improved comfort and accuracy. Additionally, advancements in low-power design have reduced energy consumption by approximately 30%, extending battery life in portable and remote devices. The adoption of digital calibration techniques and self-diagnostic capabilities has improved reliability, reducing sensor failure rates by nearly 18%. These innovations are particularly critical in aerospace and automotive applications, where precision and durability are essential. Overall, continuous technological evolution is enabling MEMS pressure sensors to deliver higher performance, greater integration, and broader application scope across industries.

• In March 2025, Bosch Sensortec expanded its MEMS sensor portfolio with a new generation of high-precision pressure sensors designed for wearable and IoT applications, achieving up to 20% improved measurement accuracy and 15% lower power consumption. Source: www.bosch-sensortec.com

• In September 2024, STMicroelectronics introduced an advanced MEMS pressure sensor platform integrating AI-based calibration, enabling real-time environmental compensation and improving sensor reliability by approximately 25% in industrial automation systems. Source: www.st.com

• In January 2025, Infineon Technologies AG announced enhancements to its XENSIV™ sensor family, incorporating pressure sensing capabilities with enhanced thermal stability, reducing performance drift by nearly 18% in automotive and industrial applications. Source: www.infineon.com

• In November 2024, TDK Corporation launched a compact MEMS pressure sensor module optimized for consumer electronics, reducing device footprint by 30% while maintaining high sensitivity, supporting integration into next-generation smartphones and wearable devices. Source: www.tdk.com

The MEMS Pressure Sensors Market Report provides a comprehensive evaluation of key industry segments, technological advancements, and regional dynamics shaping the market landscape. The report covers a wide range of product types, including piezoresistive, capacitive, resonant, and optical sensors, which collectively address diverse application requirements across industries. These sensor types are analyzed based on performance characteristics such as sensitivity, durability, and energy efficiency, with piezoresistive sensors accounting for over 50% of total adoption and capacitive sensors contributing nearly 30%.

The scope extends to detailed application analysis, encompassing automotive, industrial, healthcare, consumer electronics, and aerospace sectors. Automotive applications alone represent approximately 40% of total demand, driven by safety systems and electric vehicle integration. Industrial automation and healthcare sectors together contribute over 40%, highlighting the growing importance of real-time monitoring and diagnostic capabilities. The report also examines emerging application areas such as smart infrastructure and wearable health technologies, which are experiencing adoption increases exceeding 35%.

Geographically, the report includes in-depth coverage of major regions, including Asia-Pacific, North America, Europe, South America, and the Middle East & Africa. Asia-Pacific leads with over 40% of global consumption, supported by strong manufacturing capabilities, while North America and Europe focus on high-value, precision-driven applications. The report further explores regional production capacities, trade dynamics, and regulatory frameworks influencing market development.

Additionally, the report evaluates technological trends such as AI integration, IoT connectivity, and advanced materials, which are driving innovation and expanding application possibilities. It also highlights niche segments such as flexible and ultra-low-power sensors, which are gaining traction in wearable and portable devices. Overall, the scope provides a holistic view of the MEMS Pressure Sensors Market, enabling informed decision-making for industry stakeholders.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

3.8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Bosch Sensortec, Honeywell International Inc., STMicroelectronics, NXP Semiconductors, TE Connectivity, Infineon Technologies AG, Analog Devices Inc., TDK Corporation, Murata Manufacturing Co., Ltd., Amphenol Corporation, Melexis NV |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |