Reports

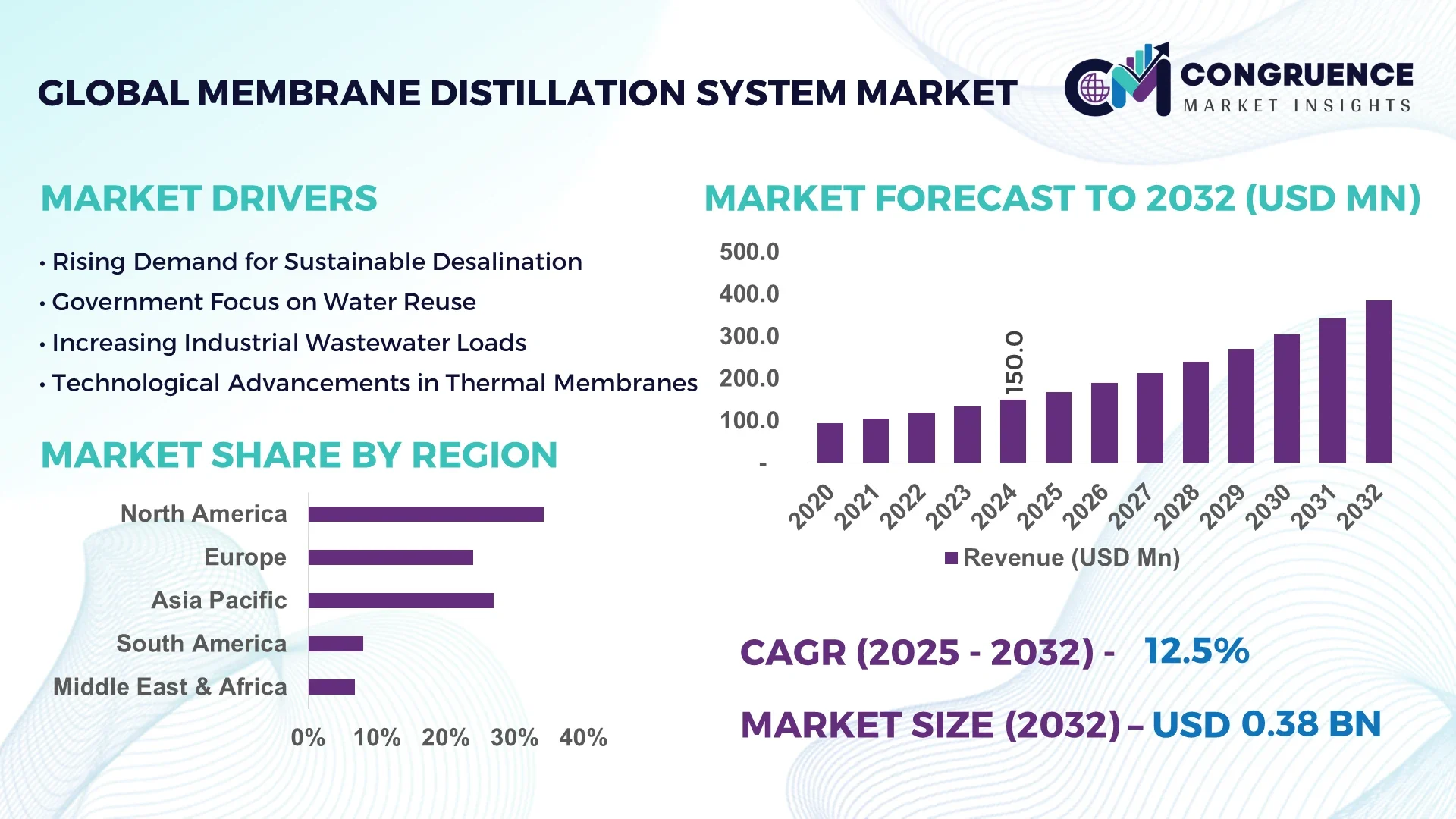

The Global Membrane Distillation Market was valued at USD 150 Million in 2024 and is anticipated to reach a value of USD 384.86 Million by 2032 expanding at a CAGR of 12.5% between 2025 and 2032.

Germany, a leader in advanced water treatment technologies, holds a prominent position in the Membrane Distillation Market with extensive production capacity, large-scale government-funded research initiatives, and significant adoption across pharmaceutical and chemical manufacturing industries.

The Membrane Distillation Market is witnessing rapid advancements as industries seek efficient and sustainable desalination and purification technologies. This process is gaining popularity across sectors such as food and beverage, pharmaceutical, textile, and power generation due to its ability to handle high-salinity feedwater with low energy requirements. Innovations in hydrophobic membrane materials and module designs are enhancing the efficiency and lifespan of membrane systems. Furthermore, regulatory policies focused on zero-liquid discharge and circular water use are accelerating adoption across industrial zones, particularly in the Asia-Pacific and European regions. Environmental concerns surrounding wastewater discharge and brine management are driving enterprises to integrate membrane distillation in hybrid treatment systems. Additionally, strong government incentives for clean water technologies and a growing demand for decentralized water treatment solutions are positioning membrane distillation as a key enabler of sustainable industrial practices. With increasing R&D investments and cross-industry collaborations, the market is poised for continual innovation and global expansion.

Artificial Intelligence (AI) is emerging as a game-changer in the Membrane Distillation Market, revolutionizing system operations, predictive maintenance, and process optimization. AI-driven algorithms are now capable of analyzing complex variables such as feedwater composition, membrane fouling patterns, and temperature gradients, allowing plant operators to make real-time decisions that minimize downtime and maximize output. These intelligent systems significantly reduce manual intervention and streamline performance monitoring across distillation units, especially in remote or decentralized installations.

In smart membrane distillation plants, AI-enabled digital twins are being utilized to simulate operational scenarios, forecast performance degradation, and suggest preventive actions. This approach has improved operational efficiency by up to 25% in industrial-scale facilities by reducing energy consumption and membrane replacement cycles. Machine learning tools are also being employed to identify early signs of membrane fouling through sensor data, enhancing longevity and throughput of filtration systems. Furthermore, AI-powered automated control systems ensure stable operation during fluctuating load conditions, helping companies meet stringent water quality standards without increasing operational costs.

Across the Membrane Distillation Market, AI integration is fostering innovation in both hardware and software components. From advanced fault detection systems to automated chemical dosing mechanisms, AI is reshaping the way industries approach water purification. As industries prioritize data-driven decision-making, AI technologies will continue to propel the Membrane Distillation Market toward more sustainable, responsive, and economically viable operations.

“In March 2024, a Netherlands-based water technology firm implemented an AI-powered membrane health monitoring system across its membrane distillation pilot plants, achieving a 30% reduction in downtime and extending membrane module lifespan by 18% within the first six months of deployment.”

Growing global concerns over industrial pollution and water scarcity are significantly boosting the adoption of membrane distillation systems in wastewater management. Industries in chemical processing, textiles, mining, and petroleum refining produce high volumes of saline and toxic effluents that conventional filtration systems struggle to treat efficiently. Membrane distillation offers a thermal separation process that is highly effective in treating these complex wastewater streams, especially in high TDS (Total Dissolved Solids) environments. With increasing regulatory mandates pushing industries to implement zero-liquid discharge (ZLD) protocols, membrane distillation is becoming a preferred solution. For instance, several industrial plants in China and India have begun deploying these systems to comply with national wastewater discharge standards. The technology’s ability to recover usable water while concentrating brine helps industries cut down on both environmental impact and operational costs, reinforcing its value across global wastewater treatment infrastructures.

Despite its advantages, the Membrane Distillation Market faces a restraint in the form of high energy requirements, especially when applied at a large industrial scale. The process relies on thermal gradients, typically requiring external heat sources, which leads to increased operational energy costs. In sectors with limited access to waste heat or renewable energy sources, this becomes a significant economic barrier. Moreover, the need for consistent temperature maintenance and membrane module integrity adds to the infrastructure and maintenance costs. Industrial players, particularly in developing regions, often find the return on investment slower compared to other membrane-based technologies like reverse osmosis. This cost-intensiveness hampers market penetration, especially for small and medium enterprises looking to upgrade their water treatment systems. Additionally, variability in feedwater composition can impact process efficiency, further limiting scalability without substantial capital expenditure on system customization and heat recovery technologies.

A key emerging opportunity in the Membrane Distillation Market is the integration of distillation units with renewable energy systems such as solar thermal collectors and geothermal heat sources. This alignment not only addresses the concern of high energy consumption but also supports global sustainability goals. In off-grid and remote locations, particularly across the Middle East, Africa, and rural parts of Asia, coupling membrane distillation with solar energy allows for decentralized water treatment solutions with minimal carbon footprint. Pilot projects in regions like the UAE and Morocco have successfully demonstrated the feasibility of solar-assisted membrane distillation units for potable water production. These developments are creating new market segments within environmentally conscious industries and water-stressed geographies. Moreover, government incentives supporting clean energy adoption can further accelerate the deployment of renewable-integrated systems, opening the door to broader commercial use and international collaborations focused on climate-resilient water purification strategies.

One of the persistent challenges in the Membrane Distillation Market is membrane fouling, which can lead to decreased performance, higher maintenance frequency, and increased operational costs. Fouling occurs due to the accumulation of organic materials, biofilms, and scaling on the membrane surface, especially when treating industrial effluents with complex chemical compositions. Over time, fouling reduces water flux and may necessitate chemical cleaning or module replacement, disrupting system continuity. These issues are further compounded in regions lacking robust technical expertise and maintenance infrastructure. While recent advancements in anti-fouling membrane coatings and pre-treatment techniques have shown promise, the lack of standardized protocols across applications continues to hinder performance optimization. End-users in harsh industrial environments often find it challenging to maintain consistent operating conditions, impacting overall system reliability and cost-effectiveness. Addressing these technical hurdles remains essential for achieving long-term scalability and trust in membrane distillation as a mainstream water purification solution.

Expansion of Zero-Liquid Discharge (ZLD) Systems in Manufacturing: Industrial manufacturers across the textile, pharmaceutical, and chemical sectors are increasingly integrating Membrane Distillation units within their ZLD systems to comply with wastewater disposal regulations. In 2024, over 35% of new ZLD systems installed in Asia-Pacific incorporated membrane distillation modules to efficiently handle high-salinity brine. This trend is especially notable in India and Southeast Asia, where industrial clusters are under pressure to reduce freshwater consumption and wastewater discharge.

Adoption of Solar-Assisted Membrane Distillation Technologies: Solar thermal energy is being used to reduce the operational cost of membrane distillation processes in water-stressed and off-grid regions. In 2024, more than 150 small-scale solar-driven membrane distillation plants were deployed across the Middle East and North Africa. These units provide decentralized water purification solutions with minimal environmental impact, attracting attention from both public sector initiatives and private eco-engineering firms.

Increase in Demand for Compact and Mobile Systems: There is a rising preference for containerized and mobile membrane distillation units, especially among military bases, disaster relief agencies, and mining operations. These compact systems enable on-site water purification in remote areas. In 2024, the demand for mobile units grew by 22%, driven by humanitarian and defense procurement programs in Europe and North America.

Integration of Smart Monitoring and Predictive Maintenance: Advanced digital tools using AI and IoT are now being embedded into membrane distillation plants for real-time monitoring of membrane performance and early fault detection. Over 40% of membrane distillation facilities commissioned in 2024 adopted smart control systems, leading to a 28% reduction in unscheduled maintenance events. This digital integration is improving operational uptime and reducing labor-intensive oversight.

The Membrane Distillation market is segmented into types, applications, and end-users, reflecting its diverse industrial relevance and technological adaptability. In terms of type, direct contact membrane distillation leads due to its simplicity and broad application scope, while air gap membrane distillation is emerging for energy-efficient applications. From an application standpoint, wastewater treatment dominates, especially in industries with high TDS waste streams, while food and beverage processing is showing rapid growth due to hygiene and purity requirements. On the end-user front, the industrial sector—particularly manufacturing and chemical processing—remains the largest adopter. However, the municipal segment is expanding as public utilities seek decentralized and cost-effective water purification methods. Each segment presents a distinct value proposition, shaping how suppliers and technology developers address market demands.

Direct Contact Membrane Distillation (DCMD) remains the most widely used type due to its design simplicity and compatibility with various heat sources. It is frequently employed in pilot plants and industrial wastewater treatment systems for its efficient separation and straightforward integration. Meanwhile, Air Gap Membrane Distillation (AGMD) is the fastest-growing type, driven by its higher thermal efficiency and reduced heat loss, making it suitable for integration with low-grade or solar thermal energy. Vacuum Membrane Distillation (VMD) is gaining niche popularity in the pharmaceutical and chemical industries for applications requiring high-purity output. Sweeping Gas Membrane Distillation (SGMD), though less common, is being explored in research setups for volatile compound recovery. These varying types highlight the market's adaptability across industries, each tailored to specific thermal and operational conditions.

Wastewater treatment leads all application areas within the Membrane Distillation Market due to increasing regulatory pressure and the need for ZLD compliance in industries like textiles, power, and chemicals. Its ability to handle high concentrations of dissolved solids makes it especially valuable in reclaiming process water. The food and beverage sector is the fastest-growing application segment, where membrane distillation is being used for juice concentration, dairy processing, and removal of contaminants without degrading product quality. Desalination remains a steady application area, particularly in off-grid and water-scarce regions, where conventional methods are too resource-intensive. Additionally, niche uses such as solvent recovery and production of ultrapure water in electronics manufacturing are also gaining momentum as the technology matures.

The industrial sector, encompassing chemical, textile, pharmaceutical, and oil & gas companies, remains the primary end-user of membrane distillation technologies. These industries generate complex wastewater streams requiring robust treatment solutions, making them ideal candidates for advanced thermal separation systems. Municipal utilities are emerging as the fastest-growing end-user group, spurred by the need for decentralized water treatment systems in peri-urban and rural areas. Government programs promoting water reuse and environmental sustainability are driving pilot implementations across Asia-Pacific and parts of Africa. Additionally, research institutions and universities are adopting membrane distillation systems for experimentation and process development, contributing modestly but steadily to the overall market demand. The diversity of end-users reflects the broad applicability and potential of membrane distillation technology in tackling both industrial and civic water challenges.

North America accounted for the largest market share at 34.2% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 15.8% between 2025 and 2032.

The North American region dominates the Membrane Distillation Market due to its robust industrial infrastructure, rapid adoption of advanced water treatment technologies, and stringent environmental regulations pushing industries toward sustainable solutions. Asia-Pacific, on the other hand, is witnessing accelerated growth driven by expanding manufacturing hubs in China and India, rising water scarcity concerns, and government initiatives promoting zero-liquid discharge technologies.

The Membrane Distillation Market is expanding as industries across wastewater treatment, pharmaceuticals, oil & gas, and food processing increasingly invest in thermal-based water purification systems. Key sectors such as chemical manufacturing and textiles are adopting this technology to comply with evolving discharge standards. Technological advancements, including solar-assisted systems and AI-integrated monitoring, are making operations more cost-effective and scalable. Globally, governments are pushing for reduced water footprints and industrial reuse of wastewater, aligning with the market’s core benefits. Additionally, innovation hubs in Asia-Pacific and Europe are focusing on next-gen membrane materials with enhanced anti-fouling capabilities, while modular and portable unit development is improving access in remote regions. These dynamics make the Membrane Distillation Market a priority for sustainable industrial operations.

Industrial Adoption Accelerates Wastewater Management Innovation

In 2024, the region held a commanding 34.2% share in the Membrane Distillation Market, primarily driven by strong demand from chemical, pharmaceutical, and oil & gas sectors. Regulatory frameworks established by the U.S. Environmental Protection Agency (EPA) and Canadian environmental authorities continue to push industrial facilities toward adopting advanced, eco-friendly water treatment systems. Government incentives under clean water infrastructure programs are further fueling adoption across multiple states. Digital transformation is a key enabler in this region, with membrane systems increasingly integrated with AI-powered predictive maintenance and IoT-based sensors. The result is increased operational efficiency, reduced maintenance downtimes, and improved membrane lifespan, making thermal distillation systems a preferred long-term investment across industrial zones.

Sustainability Mandates Fuel Membrane Technology Integration

Europe accounted for approximately 26.7% of the global Membrane Distillation Market in 2024, led by countries such as Germany, the United Kingdom, and France. Stringent wastewater discharge standards and sustainability initiatives under the EU Green Deal are compelling industrial users to incorporate advanced thermal separation technologies. European research bodies and private sector players are driving membrane innovation by developing low-energy, high-efficiency materials tailored for desalination and high-TDS effluents. Germany has emerged as a leader in deploying solar-assisted membrane distillation for municipal and agricultural reuse projects. The integration of smart automation and heat recovery systems is improving the ROI of distillation units across Europe’s industrial parks, especially in the food processing and chemical sectors.

Infrastructure Growth and Water Scarcity Boost Adoption

Asia-Pacific is the fastest-developing region in the Membrane Distillation Market, with countries like China, India, and Japan at the forefront of consumption and innovation. In 2024, the region ranked second globally by volume, and is expected to surpass others as large-scale manufacturing facilities implement membrane-based ZLD systems to address rising environmental regulations. China’s focus on sustainable industrial development and India’s expansion of textile and pharmaceutical sectors are key contributors to growth. Innovation hubs in Singapore, South Korea, and Japan are also developing energy-efficient membrane systems to reduce thermal loads. Additionally, increasing infrastructure investments in smart cities and industrial corridors are driving adoption of decentralized water treatment modules powered by renewable energy sources.

Renewable Integration and Infrastructure Drive Industrial Demand

South America is emerging as a promising market, with Brazil and Argentina leading demand for membrane distillation solutions in 2024. Brazil alone contributed to nearly 6.3% of the regional share, fueled by government-backed water reuse initiatives in the mining and agricultural sectors. In Argentina, distillation units are increasingly used in bioethanol production facilities and municipal water recycling programs. With rising interest in solar and geothermal energy integration, membrane distillation is finding support from regional infrastructure policies promoting energy-efficient water technologies. The emphasis on reducing freshwater withdrawals in energy and chemical sectors continues to create favorable conditions for advanced thermal separation technologies in the region.

Energy Sector Investments and Water Scarcity Shape Market Path

The Middle East & Africa held a regional share of 7.8% in 2024 within the global Membrane Distillation Market, with strong contributions from the UAE and South Africa. The oil & gas sector remains the biggest consumer of membrane distillation units, particularly for ZLD systems deployed in refinery operations. The UAE has piloted solar-assisted membrane distillation for remote and off-grid desalination, reflecting a regional shift toward integrating sustainable energy. South Africa’s growing construction and mining activities are also increasing the demand for compact, mobile distillation units. Trade agreements and regulatory shifts promoting water reuse and industrial water efficiency are creating a supportive landscape for new membrane technology investments across both industrial and municipal segments.

United States – 27.6% market share

High adoption of industrial wastewater reuse systems and government infrastructure support boost the U.S. position in the Membrane Distillation Market.

China – 18.3% market share

Strong manufacturing growth, rising industrial effluent treatment needs, and large-scale ZLD implementation make China a dominant force in the Membrane Distillation Market.

The Membrane Distillation market is characterized by a dynamic and moderately consolidated competitive environment, with over 40 active manufacturers and solution providers operating across regional and global scales. Leading players are aggressively investing in R&D to develop low-energy, anti-fouling membranes and hybrid systems that integrate solar or waste heat recovery to enhance system efficiency. Competition is intensifying in the Asia-Pacific and European regions, where regulatory pushes and industrial demand are prompting innovation in decentralized and modular distillation units.

Strategic partnerships between technology providers and industries in pharmaceuticals, oil & gas, and textile manufacturing are expanding commercial footprints. Notable market trends include the launch of AI-integrated process monitoring modules and containerized mobile distillation units for remote industrial applications. Mergers and acquisitions among mid-sized firms are increasing, aimed at consolidating membrane production capabilities and accessing emerging markets. Innovation-led competition, particularly in AI-augmented process optimization and energy-efficient modules, is shaping the current and future landscape of the Membrane Distillation market.

Memsys Clearwater Pte Ltd

Solar Water Solutions

Aquatech International LLC

Veolia Water Technologies

Xzero AB

Keppel Infrastructure Holdings Pte Ltd

Gore & Associates

Thermophase Energy

Aqualia Ingegneria

SUEZ WTS

The Membrane Distillation market is undergoing significant technological evolution, driven by rising demand for high-efficiency, low-energy water purification solutions. Advanced membrane materials such as polytetrafluoroethylene (PTFE), polypropylene (PP), and polyvinylidene fluoride (PVDF) are gaining traction for their superior hydrophobicity and thermal stability. New configurations including vacuum membrane distillation (VMD), direct contact membrane distillation (DCMD), air gap membrane distillation (AGMD), and sweeping gas membrane distillation (SGMD) are being implemented to optimize energy consumption across varying industrial applications.

Hybrid technologies are being introduced by integrating membrane distillation with solar thermal systems, adsorption chillers, or multi-effect distillation (MED) units to improve process sustainability. Smart sensor integration and AI-assisted membrane monitoring are now allowing real-time fouling detection and performance analytics, significantly reducing maintenance costs and downtime. Nanotechnology-infused membranes are also emerging, enabling higher flux rates and increased salt rejection for challenging wastewater streams.

Automation and modular designs are playing a crucial role in scaling up deployment across remote and decentralized settings. The rise of containerized and mobile membrane distillation units is expanding adoption across sectors such as disaster relief, mining, and offshore drilling. With enhanced material science and digitalization converging, membrane distillation is positioning itself as a leading desalination and purification solution for water-stressed regions globally.

• In March 2024, Aquatech International launched a modular membrane distillation unit with integrated solar heat exchangers designed to operate in off-grid rural environments, reducing external power dependency by 40% while maintaining high recovery rates for brackish water.

• In December 2023, Veolia unveiled a next-generation hydrophobic membrane with nanocomposite coatings that deliver up to 35% higher permeability and prolonged operational lifespan, specifically tailored for textile industry wastewater treatment.

• In July 2024, Xzero AB partnered with a Scandinavian pharmaceutical firm to install an AI-optimized membrane distillation system, enabling precise control of temperature gradients and improving water purity levels to meet stringent pharma-grade requirements.

• In May 2023, Memsys Clearwater integrated IoT-driven diagnostic modules into its membrane distillation systems, allowing remote performance tracking and predictive maintenance, which reduced unplanned downtime by 28% across pilot installations in Southeast Asia.

The Membrane Distillation Market Report provides an extensive analytical overview of the global landscape, covering technological, industrial, regional, and application-based dynamics. It evaluates four major configurations—DCMD, AGMD, VMD, and SGMD—based on their integration into industrial operations such as pharmaceuticals, food and beverage, desalination, and wastewater reuse. This report details key membrane materials including PTFE, PVDF, and PP, while also highlighting the emergence of nanocomposite and graphene-based variants designed to enhance durability and efficiency.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering quantitative insights into installation trends, demand volume, and infrastructure readiness. The report segments applications across various verticals, including municipal utilities, offshore platforms, biotech manufacturing, and mining industries, revealing distinct adoption behaviors and operational priorities within each.

It also includes an evaluation of end-user environments—industrial, commercial, and institutional—and how evolving compliance standards are driving technology upgrades. Notably, the scope addresses decentralized water treatment and portable distillation units as emerging niches. Decision-makers will benefit from targeted intelligence on R&D trends, product innovations, environmental regulations, and competitive benchmarks shaping the future of the membrane distillation sector.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 150 Million |

|

Market Revenue in 2032 |

USD 384.86 Million |

|

CAGR (2025 - 2032) |

12.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

ATG Access Ltd., FAAC Group, Calpipe Security Bollards, Came Urbaco, AUTOPA Limited, Macs Automated Bollard Systems Ltd., Rostek Oy, Bft S.p.A., PROEX Security, Heald Ltd., Nice S.p.A., Reliance Foundry Co. Ltd., Beijing ZhuoAoShiPeng Technology Co., Ltd., Doorking Inc., Pilomat Srl |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |