Reports

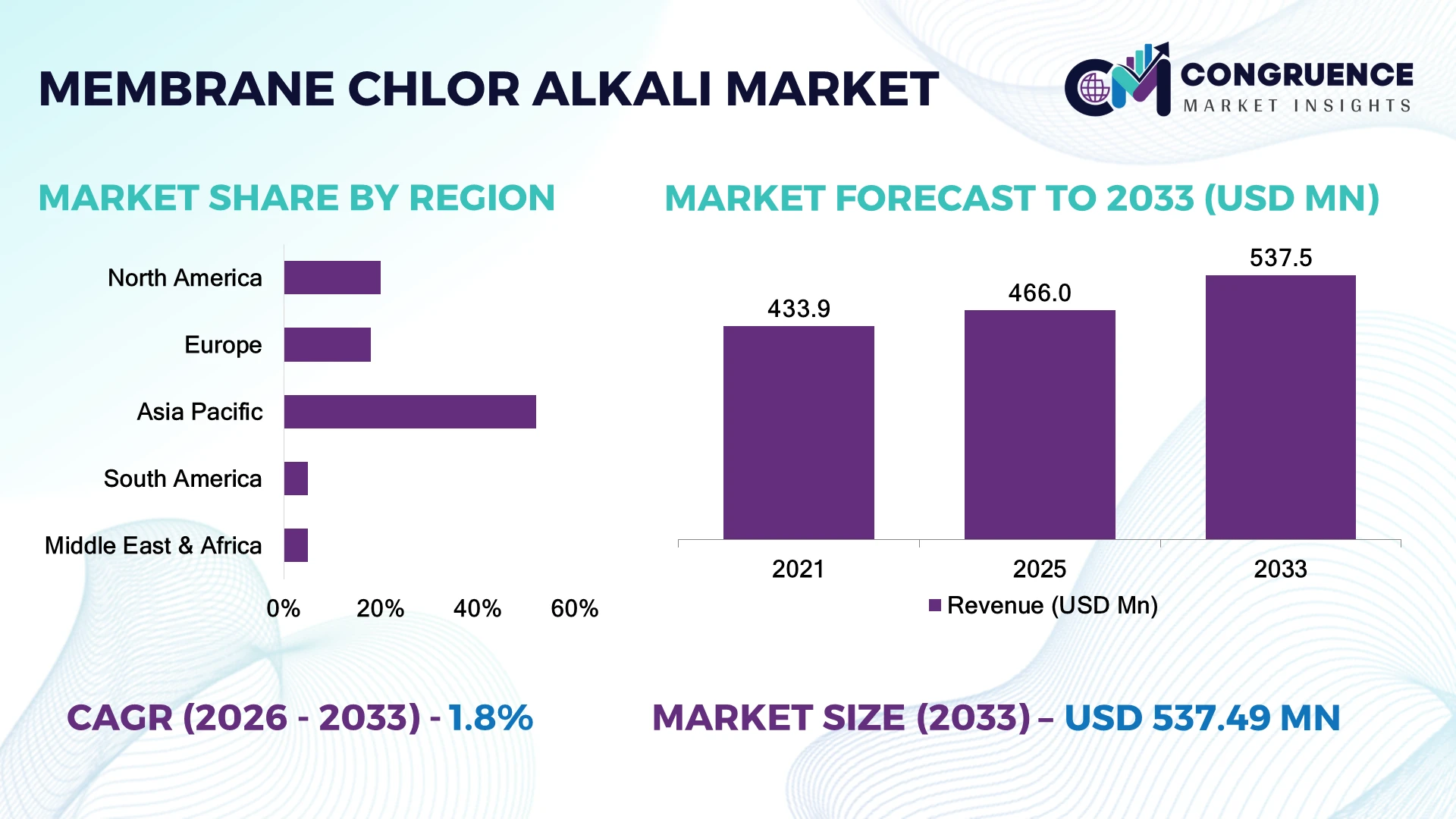

The Global Membrane Chlor-alkali Market was valued at USD 466 Million in 2025 and is anticipated to reach a value of USD 537.5 Million by 2033 expanding at a CAGR of 1.8% between 2026 and 2033. Growth is driven by replacement of mercury and diaphragm cells with energy-efficient membrane electrolysis systems, stricter environmental regulations, and modernization of chemical production facilities.

China dominates the market with over 45% of global membrane chlor-alkali capacity, supported by large-scale PVC, alumina, and chemical manufacturing clusters and investments in cleaner electrolysis technologies. The country operates more than 70 million tons annually of chlor-alkali production capacity, while Europe focuses on low-carbon upgrades under EU industrial decarbonization policies. China’s installed capacity scale exceeds Europe’s by over 3 times, highlighting its manufacturing advantage and technology adoption pace.

Strategic implication on Companies prioritizing advanced membrane systems and regional capacity expansion gain stronger positioning in the evolving global chemical supply chain.

Market Size & Growth: USD 466 Million market in 2025 reaching USD 537.5 Million by 2033 at 1.8% CAGR, driven by membrane cell replacement and energy-saving chemical production upgrades.

Top Growth Drivers: Energy efficiency improvement (30%), environmental compliance adoption (25%), and industrial modernization demand (20%) are accelerating membrane technology deployment.

Short-Term Forecast: By 2028, advanced membrane systems reduce electricity consumption by up to 10–15% compared with older chlor-alkali technologies.

Emerging Technologies: Advanced ion-exchange membranes, AI-based process monitoring, and automated electrolysis control systems are transforming plant efficiency.

Regional Leaders: Asia-Pacific leads with over 50% adoption, Europe advances through low-carbon upgrades, and North America expands through chemical infrastructure renewal.

Consumer/End-User Trends: More than 60% of new chlor-alkali capacity additions prioritize membrane-based systems due to sustainability targets.

Pilot/Case Example: In 2023, European chemical plants using upgraded membrane cells achieved approximately 8–12% operational energy reductions.

Competitive Landscape: Leading suppliers include Asahi Kasei, AGC Inc., INEOS, Solvay, and ThyssenKrupp, with major players controlling a significant share of membrane technology supply.

Regulatory & ESG Impact: Global restrictions on mercury-based processes are driving nearly 100% transition toward safer membrane technologies in new installations.

Investment & Funding: More than USD 1 Billion has been directed toward chlor-alkali modernization projects, focusing on partnerships, automation, and cleaner production.

Innovation & Future Outlook: Next-generation membranes, renewable-powered electrolysis, and digital chemical plants are shaping the future competitive landscape.

The Membrane Chlor-alkali Market is gaining importance as chemical producers prioritize cleaner production methods, stable raw material supply, and efficient operations. Demand is expanding across PVC, pulp and paper, water treatment, and specialty chemicals, with membrane-based systems improving energy performance by around 10–15% compared with conventional technologies. Recent capacity upgrades in Asia and Europe reflect a global shift toward sustainable chemical infrastructure and supply-chain resilience, creating opportunities for technology providers and industrial operators.

The Membrane Chlor-alkali Market is becoming strategically important as chemical manufacturers shift toward safer, energy-efficient production systems while responding to stricter environmental standards. The global transition away from mercury-based chlor-alkali processes and increasing investment in industrial decarbonization are reshaping competitive priorities across major chemical-producing regions.

Modern membrane electrolysis technology delivers significant advantages over legacy diaphragm and mercury systems, reducing electricity consumption by approximately 20–30% while improving product purity and operational stability. Asia-Pacific remains the largest deployment hub due to extensive chemical manufacturing infrastructure, while Europe leads technology modernization through sustainability-focused investments and carbon reduction initiatives.

Operational examples include large chlor-alkali producers upgrading existing plants with advanced ion-exchange membranes, automated monitoring, and renewable energy integration to improve efficiency. Over the next 2–3 years, adoption of digital process controls and low-carbon production systems is expected to accelerate as companies strengthen partnerships and expand cleaner manufacturing capacity.

Strategically, companies that combine advanced membrane technology, efficient plant operations, and sustainable production models will secure stronger competitive advantages in the evolving global chemical industry.

The replacement of mercury and diaphragm-based chlor-alkali cells with membrane electrolysis systems is the primary growth driver, supported by stricter environmental standards and industrial decarbonization targets. Membrane technology reduces electricity consumption by approximately 20–30% and improves chlorine purity by more than 10% compared with older processes. China, India, and Germany are expanding cleaner chemical production infrastructure as regulations tighten around hazardous technologies. Companies such as major chlor-alkali producers are investing in plant modernization, advanced ion-exchange membranes, and automation platforms to improve operational efficiency. The strategic advantage lies in lowering energy exposure, as electricity accounts for nearly 50% of chlor-alkali production costs.

High installation costs and dependence on specialized membrane materials remain key restraints for market expansion. Advanced membrane-based chlor-alkali plants require significant upfront investment, with modernization projects often increasing capital expenditure by 15–25% compared with conventional upgrades. Supply constraints for fluoropolymer-based membranes and specialty coatings create procurement challenges, particularly during periods of global chemical supply-chain disruption. Countries such as Japan and South Korea maintain strong technology capabilities, but smaller producers face scalability barriers due to limited access to proprietary materials. Companies are reducing exposure through long-term supplier contracts, localized component sourcing, and partnerships with membrane technology providers to stabilize production costs and improve project feasibility.

The transition toward renewable-powered electrolysis and digitalized chemical operations creates new opportunities for membrane chlor-alkali technology providers. Renewable electricity integration can reduce operational emissions by more than 40% in suitable industrial locations, while advanced process controls improve plant efficiency by 5–10%. Countries including China, Saudi Arabia, and India are developing chemical hubs where sustainable chlorine and caustic soda production supports PVC, water treatment, and specialty chemical industries. Companies are strengthening their market position through research partnerships, next-generation membrane development, and integrated energy solutions. A major opportunity lies in combining membrane systems with hydrogen co-production models, enabling chemical producers to create additional value streams from existing electrolysis infrastructure.

Scaling membrane chlor-alkali systems requires overcoming operational complexity, skilled workforce shortages, and integration challenges across aging chemical facilities. Approximately 25–30% of existing chlor-alkali plants globally still require modernization to meet advanced efficiency and environmental benchmarks. In countries with older industrial infrastructure, upgrading electrical systems, control platforms, and chemical handling units creates deployment difficulties. Cybersecurity risks in digitally connected chemical plants are also increasing as automation adoption expands. Companies must address these barriers through workforce training, modular plant upgrades, technology partnerships, and improved industrial cybersecurity frameworks. Long-term competitiveness depends on maintaining reliable operations while balancing sustainability goals with production continuity.

Digital Plant Optimization: Chlor-alkali producers are accelerating digital transformation with AI-based monitoring, predictive maintenance, and automated process controls, improving plant efficiency by 5–10% and reducing unplanned downtime by nearly 15%. Companies in China and Germany are integrating smart manufacturing platforms to optimize membrane performance, energy usage, and chemical output consistency. The shift toward connected electrolysis operations is reducing operational variability and strengthening asset utilization.

Low-Carbon Electrolysis Integration: Chemical manufacturers are increasingly combining membrane chlor-alkali systems with renewable power sources, reducing production-related emissions by 30–40% in optimized facilities. Germany’s industrial decarbonization policies and China’s clean-energy expansion are encouraging companies to restructure energy procurement strategies. Producers are forming renewable energy partnerships and upgrading electrolysis infrastructure to improve sustainability performance while managing electricity cost volatility.

Advanced Membrane Engineering: Manufacturers are focusing on next-generation ion-exchange membranes with improved durability, conductivity, and chemical resistance. New membrane designs are extending operational lifecycles by 10–20% and reducing replacement frequency in large-scale plants. Japanese and U.S. technology suppliers are increasing R&D collaboration with chemical producers to improve process reliability and lower maintenance requirements.

Supply Chain Localization: Global chemical supply disruptions have accelerated regional sourcing strategies for membrane materials, coatings, and specialty components. Companies are increasing localized procurement by 20–30% to reduce dependency risks and improve production continuity. European and Asian producers are developing supplier networks closer to industrial hubs, creating more resilient chlor-alkali manufacturing ecosystems.

Membrane cell technology dominates the Membrane Chlor-alkali Market, accounting for approximately 85–90% of installed chlor-alkali capacity due to superior energy efficiency, lower environmental impact, and compliance advantages over mercury and diaphragm technologies. Its ability to deliver high-purity chlorine and caustic soda while reducing electricity consumption by nearly 20–30% has made it the preferred choice for large chemical producers. Mercury cells and diaphragm cells continue declining as regulatory pressure increases, although some legacy facilities maintain these systems during phased modernization programs. The fastest-growing shift is toward advanced ion-exchange membrane variants, which are gaining adoption through improved durability and lower maintenance requirements. New-generation membranes can extend operational life by 10–15% and support automated process optimization. Companies are prioritizing membrane innovation, strategic supplier partnerships, and plant retrofits to strengthen competitiveness. Investment priorities are shifting from basic capacity expansion toward efficiency-focused technology upgrades.

Chlorine production represents the leading application segment, contributing approximately 45–50% of membrane chlor-alkali system demand due to its essential role in PVC manufacturing, water treatment chemicals, and specialty chemical production. The application benefits from strong integration with downstream industries, particularly in China, India, and the United States, where chemical clusters rely on continuous chlorine supply. Caustic soda production and hydrogen co-production remain strategically important applications, supporting integrated chemical value chains. The fastest-growing application area is hydrogen co-production, driven by industrial interest in cleaner hydrogen sources and energy-efficient electrolysis systems. Adoption is increasing as companies integrate membrane chlor-alkali units with renewable electricity and low-carbon manufacturing models. Hydrogen-linked applications are expanding at approximately 8–10% adoption growth in new project planning. Companies are developing integrated chemical-energy platforms to maximize asset utilization and create additional revenue opportunities from electrolysis operations.

Chemical manufacturers represent the largest end-user segment, accounting for approximately 60–65% of membrane chlor-alkali technology adoption due to their extensive chlorine, caustic soda, and hydrogen requirements. Large producers in China, Germany, Japan, and the United States are upgrading existing facilities to improve energy efficiency and comply with environmental standards. The PVC, alumina, pulp and paper, and water treatment industries remain major demand centers due to their dependence on chlor-alkali derivatives. The fastest-growing end-user group is water treatment and specialty chemical producers, supported by rising infrastructure investment and stricter water quality regulations. These users are increasing adoption of reliable chlorine supply systems, with demand expansion concentrated in developing industrial markets. Companies are responding through customized membrane solutions, regional service networks, and technology partnerships that support smaller-scale deployment requirements. Future competition is shifting toward flexible systems capable of serving both large chemical complexes and emerging industrial applications.

Asia-Pacific accounted for the largest market share at 52% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 2.4% between 2026 and 2033.

North America holds approximately 20% of the global Membrane Chlor-alkali Market, supported by established chemical manufacturing networks, PVC production facilities, and replacement of aging chlor-alkali assets. The United States represents the largest contributor due to its extensive Gulf Coast chemical corridor, where membrane-based systems are being deployed to improve energy efficiency and environmental compliance. More than 70% of operating chlor-alkali facilities in the region have transitioned toward membrane technology. Companies are investing in plant automation, renewable power integration, and capacity optimization to strengthen operational reliability amid rising energy cost pressures.

United States Market Outlook: The United States maintains a strong market position through its large-scale chemical production infrastructure and advanced industrial technology adoption. The Gulf Coast region accounts for a significant share of national chemical output, with major producers upgrading electrolysis facilities to improve efficiency and reduce emissions. Increasing investment in clean manufacturing technologies is supporting membrane system adoption across chlorine and caustic soda production facilities.

Europe represents around 18% of the global Membrane Chlor-alkali Market, driven by strict environmental regulations, industrial decarbonization programs, and modernization of chemical facilities. Countries including Germany, Belgium, and the Netherlands are leading deployment due to concentrated chemical manufacturing clusters. European producers are replacing older electrolysis technologies with advanced membrane systems that reduce electricity consumption by approximately 20–30%. Industrial partnerships focused on renewable energy integration and low-carbon production are increasing as manufacturers align operations with European sustainability objectives. Companies are prioritizing efficiency upgrades, digital monitoring, and long-term energy management strategies.

Germany Market Outlook: Germany remains the leading European market due to its advanced chemical manufacturing base and strong engineering capabilities. The country’s chemical sector operates highly integrated production networks, with membrane technology adoption exceeding 80% in modern chlor-alkali installations. Investments in industrial electrification and sustainable chemical processes continue supporting technology upgrades across major production facilities.

Asia-Pacific dominates the Membrane Chlor-alkali Market with approximately 52% market share, supported by massive chemical production capacity, expanding PVC industries, and rapid industrial infrastructure development. China accounts for the majority of regional demand, supported by more than 70 million tons of chlor-alkali production capacity and extensive downstream chemical integration. India, Japan, and South Korea are also increasing adoption of advanced membrane systems to improve production efficiency and meet environmental requirements. Companies are expanding manufacturing capacity, forming technology partnerships, and upgrading existing plants with automated electrolysis solutions to improve competitiveness in global chemical supply chains.

China Market Outlook: China leads the global market due to its extensive chlor-alkali manufacturing ecosystem and strong downstream demand from PVC, alumina, and chemical industries. The country has accelerated membrane technology adoption across large industrial facilities, with new projects increasingly using energy-efficient electrolysis systems. Government emphasis on cleaner industrial production is encouraging chemical manufacturers to modernize existing plants.

South America accounts for approximately 5% of the global Membrane Chlor-alkali Market, with demand concentrated in Brazil and Argentina due to chemical processing, pulp and paper, and water treatment industries. Brazil represents the largest contributor as companies modernize chemical facilities and improve chlorine supply reliability. Adoption remains lower compared with developed markets due to infrastructure limitations and investment constraints, but membrane technology is gaining attention because of improved energy efficiency and lower environmental impact. Producers are focusing on selective upgrades, regional partnerships, and localized supply strategies to overcome equipment availability challenges.

Brazil Market Outlook: Brazil holds the strongest position in South America through its diversified industrial base and established chemical production sector. The country’s water treatment and pulp industries create steady chlorine demand, while chemical producers are gradually replacing older systems with membrane-based solutions. Infrastructure modernization projects are supporting long-term technology adoption.

Middle East & Africa represents approximately 5% of the global Membrane Chlor-alkali Market, supported by chemical diversification programs, infrastructure development, and investments in industrial manufacturing hubs. Gulf countries are increasing chlor-alkali capacity to support PVC, petrochemical, and water treatment industries. Saudi Arabia and the United Arab Emirates are developing integrated chemical complexes with advanced production technologies, including energy-efficient membrane systems. Companies are leveraging abundant energy resources, industrial partnerships, and new chemical investments to improve production competitiveness. However, technology adoption remains concentrated in large-scale industrial projects due to capital requirements and infrastructure availability.

Saudi Arabia Market Outlook: Saudi Arabia is the leading market in the region due to its expanding chemical manufacturing ecosystem and investment in integrated industrial complexes. The country’s petrochemical expansion strategy supports increased chlorine and caustic soda demand, while large industrial projects are incorporating advanced membrane technologies to improve efficiency and sustainability performance.

The Membrane Chlor-alkali Market features competition between global membrane technology leaders, chemical equipment suppliers, and regional chlor-alkali producers. Companies such as Asahi Kasei, AGC, ThyssenKrupp, and INEOS compete through advanced membrane solutions, while regional manufacturers compete on cost efficiency and localized supply chains. The top five players collectively account for approximately 55–60% of technology supply influence. Competition is based on membrane performance, energy savings, reliability, and customization, with advanced systems delivering 20–30% lower electricity consumption than legacy technologies. Leading players are expanding through plant modernization partnerships, technology licensing, and integrated chemical infrastructure investments. The market is shifting toward sustainable electrolysis, renewable-powered operations, and digital process control, increasing pressure on traditional suppliers. High technical expertise, intellectual property ownership, and manufacturing capabilities create strong entry barriers. Winning requires superior membrane innovation, reliable supply networks, and scalable solutions tailored to industrial producers.

AGC Inc.

ThyssenKrupp Uhde Chlorine Engineers

INEOS Group

Solvay S.A.

Occidental Petroleum Corporation

Tata Chemicals Limited

Olin Corporation

Westlake Corporation

Formosa Plastics Corporation

Nirma Limited

Xinjiang Zhongtai Chemical Co., Ltd.

Tosoh Corporation

Membrane chlor-alkali technology is advancing through high-performance ion-exchange membranes, automated electrolysis controls, and renewable energy integration. Modern membranes improve energy efficiency by 20–30% compared with mercury and diaphragm systems while increasing product purity. More than 80% of newly commissioned chlor-alkali plants prioritize membrane-based technology, driven by environmental compliance and operational savings.

Digital monitoring and AI-enabled process optimization are becoming important competitive tools, helping producers reduce downtime by 10–15% and improve production consistency. Compared with conventional manual operations, automated systems provide faster process adjustments and stronger asset utilization. Large chemical producers in China, Japan, Germany, and the United States are integrating these solutions into modernization programs.

Between 2026 and 2028, disruptive technologies will focus on renewable-powered electrolysis, advanced membrane materials, and hydrogen-linked chemical production models. Companies investing in next-generation membranes gain advantages through lower energy exposure, improved sustainability performance, and stronger regulatory positioning. Technology suppliers and integrated chemical manufacturers benefit most as the market shifts from capacity expansion toward efficiency-driven transformation.

April 2025 Asahi Kasei Corporation launched a joint demonstration with Nobian, Furuya Metal, and Mastermelt for recycling metals from chlor-alkali electrolyzer cells and electrodes. The project targets circular supply chains for valuable materials used in electrolysis components, strengthening sustainability practices. Source: www.asahi-kasei.com

May 2025 Asahi Kasei Corporation received the Imperial Invention Prize for nickel-based electrode technology that extends chlor-alkali electrolysis electrode life. The company reported its ion-exchange membrane process had been adopted at over 160 plants across more than 30 countries, improving long-term operational stability. Source: www.asahi-kasei.com

May 2025 INEOS Electrochemical Solutions appointed a commercial agent in South America to expand sales support for its BICHLOR™ membrane electrolyser technology and CHLORCOAT™ electrode coatings. The move strengthens regional customer engagement and supports wider deployment of advanced electrolysis systems. Source: www.ineos.com

October 2025 Asahi Kasei Corporation approved new Kawasaki Works facilities for manufacturing electrolysis system components, including cell frames and membranes for chlor-alkali and clean hydrogen applications. The expansion strengthens vertical integration and supply capacity for future industrial demand.

The Membrane Chlor-alkali Market Report provides comprehensive coverage of technology types, applications, end-user industries, regional markets, competitive dynamics, and strategic growth opportunities. The analysis evaluates membrane-based electrolysis systems across chlorine production, caustic soda manufacturing, hydrogen co-production, chemical processing, water treatment, and industrial applications. It covers major markets including North America, Europe, Asia-Pacific, South America, and Middle East & Africa.

The report examines adoption patterns, technology advancements, supplier positioning, modernization trends, and emerging opportunities in low-carbon chemical production. With more than 80% of new chlor-alkali installations adopting membrane technology, the study supports investment decisions, expansion planning, partnership evaluation, and competitive positioning. It provides insights into operational efficiency improvements, supply-chain strategies, and future technology pathways shaping the market through 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 466 Million |

| Market Revenue (2033) | USD 537.5 Million |

| CAGR (2026–2033) | 1.8% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Asahi Kasei Corporation; AGC Inc.; ThyssenKrupp Uhde Chlorine Engineers; INEOS Group; Solvay S.A.; Occidental Petroleum Corporation; Tata Chemicals Limited; Olin Corporation; Westlake Corporation; Formosa Plastics Corporation; Nirma Limited; Xinjiang Zhongtai Chemical Co., Ltd.; Tosoh Corporation |

| Customization & Pricing | Available on Request (10% Customization Free) |