Reports

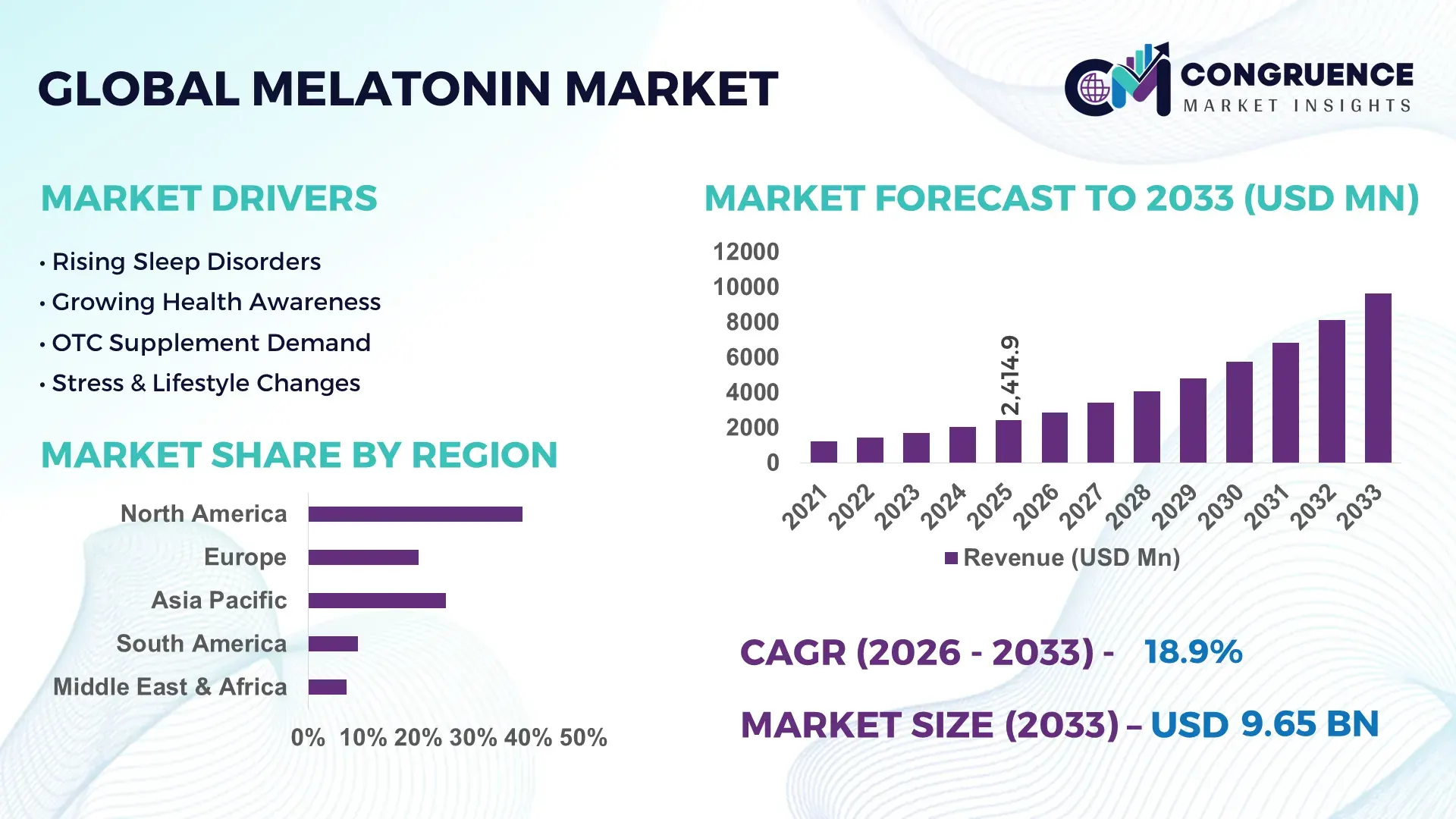

The Global Melatonin Market was valued at USD 2414.85 Million in 2025 and is anticipated to reach a value of USD 9645.98 Million by 2033 expanding at a CAGR of 18.9% between 2026 and 2033. Growth is being accelerated by rising clinical adoption of sleep-support supplements, expanding nutraceutical manufacturing capacity, increasing shift-work populations, and rapid innovation in sustained-release melatonin formulations.

The United States remains the dominant market, accounting for approximately 38% of global demand in 2026, supported by advanced nutraceutical production, strong retail penetration, and widespread consumer awareness. More than 65% of sleep-support supplement launches in North America now incorporate melatonin-based formulations. Compared with Germany, where regulatory oversight remains stricter, U.S. product availability is significantly broader. Continued supply-chain diversification following post-pandemic ingredient sourcing adjustments has strengthened manufacturing resilience and reduced procurement bottlenecks across major producers.

Companies prioritizing premium formulations, regulatory-compliant product portfolios, and scalable distribution networks are positioned to capture the strongest long-term market gains.

Market Size & Growth: USD 2414.85 Million in 2025, reaching USD 9645.98 Million by 2033 at 18.9% CAGR, driven by advanced sleep-health formulations and expanding nutraceutical distribution.

Top Growth Drivers: Sleep disorder prevalence (+22%), gummy-format adoption (+31%), and e-commerce supplement sales growth (+28%).

Short-Term Forecast: By 2028, manufacturing efficiency improves by 15% through automated dosing, encapsulation, and packaging systems.

Emerging Technologies: AI-assisted formulation design, controlled-release delivery systems, and precision microencapsulation improve product stability by up to 20%.

Regional Leaders: North America exceeds USD 3.8 Billion, Europe approaches USD 2.4 Billion, and Asia-Pacific surpasses USD 2.1 Billion, supported by expanding health-product adoption.

Consumer/End-User Trends: Nearly 45% of sleep-aid supplement consumers prefer non-prescription melatonin formats with convenient daily dosing.

Pilot/Case Example: In 2025, advanced encapsulation deployments improved ingredient stability by 18% and reduced product degradation rates by 12%.

Competitive Landscape: Leading manufacturers collectively control approximately 35% of global sales; competition centers on Natrol, NOW Foods, Life Extension, Puritan’s Pride, and Nature Made.

Regulatory & ESG Impact: Sustainable packaging initiatives reduced packaging material usage by 14%, supporting compliance and operational efficiency goals.

Investment & Funding: More than USD 700 Million in expansion, partnerships, and manufacturing upgrades supported regional supply-chain localization efforts.

Innovation & Future Outlook: Next-generation sustained-release products and personalized sleep-support solutions are expected to increase premium-product penetration above 30%.

Melatonin Market demand is increasingly concentrated across dietary supplements, sleep wellness products, pharmaceutical-grade formulations, and functional nutrition applications. Manufacturers are investing in advanced microencapsulation and extended-release technologies that improve ingredient stability by nearly 20% while enhancing user compliance. A notable trend is the expansion of localized production networks to strengthen supply-chain reliability and regulatory alignment, creating a more competitive environment and setting the stage for deeper strategic market positioning.

The melatonin market has evolved from a niche sleep-support category into a strategically important segment within preventive healthcare, nutraceuticals, and consumer wellness. Rising healthcare costs, growing workplace fatigue concerns, and increasing focus on sleep quality are strengthening competitive investment across product development and distribution. A notable market shift is the restructuring of ingredient sourcing networks, with manufacturers reducing dependence on single-country supply chains and expanding regional production capabilities to improve resilience and inventory stability.

Technology innovation is reshaping product performance and differentiation. Advanced microencapsulation and controlled-release formulations improve ingredient stability by nearly 20% and extend efficacy duration compared with conventional immediate-release products. The United States leads in product commercialization and retail penetration, while Japan and Germany emphasize precision formulations and quality-focused regulatory compliance. More than 40% of newly launched premium sleep-support products now incorporate enhanced delivery technologies, reflecting a clear transition toward science-backed formulations.

Operational deployment is increasingly focused on omnichannel distribution, personalized wellness offerings, and strategic partnerships between supplement brands and healthcare platforms. Several manufacturers have expanded localized packaging and fulfillment operations, reducing lead times by approximately 15%. Over the next two to three years, continued adoption of advanced formulations and digital wellness integration will strengthen competitive positioning, making innovation, supply-chain agility, and product differentiation critical determinants of long-term market leadership.

The primary growth driver is the integration of sleep health into preventive wellness strategies across consumer healthcare markets. More than 35% of adults in major developed economies report recurring sleep-related concerns, supporting sustained demand for melatonin-based products. Digital health applications tracking sleep quality have increased user engagement by over 25%, improving awareness and supplement adoption. In the United States, retailers and healthcare providers are expanding sleep-wellness portfolios as part of broader self-care initiatives. The result is higher product penetration, stronger repeat purchasing behavior, and accelerated innovation cycles. Companies are responding through sustained-release product launches, strategic retail partnerships, and investments in clinically supported formulations. A notable operational insight is that brands combining sleep tracking data with targeted supplement recommendations are achieving stronger consumer retention and premium product conversion.

Regulatory inconsistency remains a significant structural limitation across the melatonin market. Product classification varies considerably between countries, creating compliance complexity and extending market-entry timelines by as much as 20%. In several European markets, dosage restrictions limit product flexibility, while labeling and health-claim requirements increase development costs. Raw material procurement costs have also experienced periodic fluctuations exceeding 10% due to ingredient sourcing concentration and quality-control requirements. These factors directly affect profitability, product scalability, and portfolio harmonization. Manufacturers are mitigating exposure through localized regulatory teams, diversified supplier networks, and region-specific product formulations. A key strategic insight is that companies with multi-country compliance frameworks can commercialize products faster and reduce operational disruptions compared with competitors relying on centralized regulatory approaches.

Personalized wellness solutions represent a high-value opportunity for market participants. Consumer preference for targeted health products has increased by approximately 30%, while demand for premium nutraceutical formulations continues to expand. Advanced technologies such as precision microencapsulation, smart dosage systems, and AI-assisted formulation development can improve ingredient stability by nearly 20% and optimize user outcomes. In South Korea and the United States, companies are increasingly integrating sleep-support products into broader digital wellness ecosystems. Strategic investments are targeting subscription-based health models, personalized supplement recommendations, and direct-to-consumer channels. A less obvious opportunity lies in workplace wellness programs, where sleep-performance optimization is becoming a measurable productivity initiative. Companies establishing partnerships across healthcare, nutrition, and digital health ecosystems are positioned to capture differentiated value and strengthen long-term customer engagement.

Long-term competitiveness is increasingly challenged by product saturation and rising consumer expectations. More than 50% of new launches compete within similar dosage ranges and formulation categories, creating differentiation pressure. Product development cycles have shortened by nearly 15%, requiring continuous innovation to maintain visibility and pricing power. In the United States and Canada, intense competition from private-label offerings is compressing margins and increasing promotional spending. At the same time, maintaining consistent quality standards across expanding global supply networks remains operationally complex. Companies must invest in formulation science, clinical validation, and manufacturing modernization to sustain credibility and performance claims. A critical strategic insight is that future leaders will be defined less by product availability and more by scientific substantiation, brand trust, and the ability to integrate melatonin products into broader health-management ecosystems.

• Precision Release Formulations Expand Controlled-release and dual-phase melatonin products now represent more than 30% of new premium product launches, while consumer preference for extended-duration sleep support has increased by approximately 22%. Manufacturers are deploying advanced microencapsulation technologies that improve stability by nearly 18% and reduce dosage variability. Companies in the United States are expanding formulation partnerships and investing in specialized production lines to differentiate products through performance rather than dosage strength alone.

• Digital Sleep Ecosystems Converge Integration between sleep-tracking platforms and supplement recommendations has accelerated, with digital wellness engagement rising by over 25% and personalized health app usage increasing nearly 20%. The shift is being driven by broader adoption of connected health technologies and workplace wellness programs. Companies are forming partnerships with digital health providers, enabling data-informed product positioning and improving customer retention through subscription-based wellness models and automated replenishment programs.

• Supply Chain Localization Accelerates Ingredient sourcing diversification has become a key operational priority, with localized procurement programs reducing lead times by approximately 15% and inventory disruptions by nearly 12%. Ongoing geopolitical trade adjustments and stricter quality-control requirements have encouraged manufacturers to establish regional packaging and fulfillment hubs. The non-obvious outcome is improved regulatory responsiveness, allowing companies to adapt formulations more quickly to country-specific compliance requirements.

• Gummy Format Premiumization Advances Melatonin gummies account for more than 35% of retail product introductions, while demand for sugar-reduced and functional ingredient combinations has increased by approximately 28%. Companies are combining melatonin with botanicals, vitamins, and stress-management ingredients to create multifunctional wellness products. Automated manufacturing systems are improving production efficiency by nearly 14%, supporting larger-scale launches and faster commercialization across competitive consumer health channels.

Tablets remain the leading type segment due to their manufacturing scalability, dosage consistency, and cost-efficient production. They account for an estimated 34% of total market consumption, supported by strong pharmacy distribution and established consumer familiarity. Tablets offer operational advantages through high-volume manufacturing and longer shelf stability, making them the preferred format for mass-market deployment. Capsules continue to maintain relevance in premium supplement portfolios because of enhanced ingredient flexibility and cleaner-label positioning. Softgels support targeted premium applications where absorption performance and consumer convenience are prioritized.

Gummies represent the fastest-growing type, with annual product introductions increasing by more than 30% as consumers increasingly favor convenient and palatable delivery formats. Demand is particularly strong among younger adults and wellness-focused users seeking combination formulations. Liquid formulations are gaining traction in pediatric and customized dosage applications, although their market footprint remains smaller. Manufacturers are responding through capacity expansion, flavor innovation, and multifunctional product development. Investment priorities are shifting toward consumer-friendly formats, with companies allocating greater R&D resources to gummies and advanced delivery technologies while maintaining tablet-based production for scale efficiency.

Sleep Disorders represent the dominant application segment, accounting for an estimated 45% of overall melatonin utilization. Demand concentration is driven by increasing consumer focus on sleep quality, broader self-care adoption, and growing use of non-prescription sleep-support solutions. Companies continue expanding product portfolios specifically targeting sleep onset and sleep maintenance requirements. Circadian Rhythm Support maintains a strong position, particularly among shift workers and individuals exposed to irregular work schedules, where sleep-cycle management is becoming operationally important for workforce productivity.

Circadian Rhythm Support is also the fastest-growing application category, supported by rising deployment of digital sleep monitoring technologies and greater awareness of biological clock management. Adoption has increased by approximately 20% in populations using wearable sleep-tracking devices. Jet Lag Management remains strategically relevant for frequent travelers and aviation professionals, while Stress Relief and General Wellness applications are expanding through multifunctional formulations. Companies are scaling personalized wellness programs, integrating sleep analytics, and broadening distribution strategies. Demand is increasingly shifting from symptom-focused supplementation toward comprehensive sleep optimization and daily wellness management solutions.

Retail Pharmacies remain the leading end-user segment due to extensive distribution infrastructure, trusted consumer access, and broad product availability. They account for approximately 38% of market demand, benefiting from established purchasing behavior and immediate product accessibility. Hospitals and Specialty Clinics continue serving targeted patient populations where professional guidance supports usage decisions. Wellness Centers maintain a growing role by integrating sleep-support products into broader lifestyle and recovery programs, creating additional touchpoints for consumer engagement.

Online Pharmacies represent the fastest-growing end-user category, with digital supplement purchases increasing by more than 25% as consumers prioritize convenience, product comparison tools, and subscription fulfillment models. Home Care Users are also expanding rapidly as sleep management becomes increasingly self-directed. Companies are responding through direct-to-consumer strategies, digital marketing investments, and partnerships with online healthcare platforms. Customized product bundles, loyalty programs, and automated replenishment systems are becoming important competitive tools. Future demand is expected to shift toward digitally enabled purchasing ecosystems where convenience, personalization, and recurring engagement drive long-term customer value.

North America accounted for the largest market share at 39% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 20.8% between 2026 and 2033.

Premium Sleep Wellness Commercialization

North America maintains leadership through strong nutraceutical infrastructure, extensive retail distribution, and high consumer adoption of sleep-support supplements. The region accounts for approximately 39% of global market demand, supported by widespread deployment across retail pharmacies, online channels, and wellness platforms. More than 60% of newly launched sleep-support products incorporate advanced delivery technologies such as controlled-release formulations and microencapsulation. Manufacturers continue investing in localized production and digital health partnerships to improve consumer engagement and supply resilience. Enterprise focus has shifted toward premium formulations, subscription-based wellness programs, and direct-to-consumer strategies that enhance retention and product differentiation.

United States Market Outlook: The United States represents the largest concentration of melatonin consumption and product innovation globally. Strong retail penetration, advanced supplement manufacturing capabilities, and favorable consumer awareness support sustained deployment. More than 65% of North American sleep-support product launches originate from U.S.-based companies. Expansion of personalized wellness programs and integration with sleep-tracking technologies continue strengthening market positioning, while established quality-control systems support rapid commercialization of new formulations.

Regulatory Compliance Driving Product Differentiation

Europe remains a significant market driven by quality-focused product development, stringent regulatory oversight, and increasing consumer emphasis on preventive wellness. The region accounts for nearly 27% of global demand and demonstrates strong adoption of premium formulations with clinically supported positioning. Regulatory requirements are encouraging manufacturers to invest in product standardization, formulation consistency, and advanced packaging technologies. Several enterprises have expanded regional production and packaging operations, reducing cross-border supply complexity by approximately 12%. Companies increasingly compete through scientific validation, ingredient traceability, and regulatory compliance rather than volume-focused expansion.

Germany Market Outlook: Germany serves as the region's strategic center for high-quality nutraceutical production and regulatory-led product development. The country's advanced manufacturing infrastructure and strong consumer health market support broad deployment of premium melatonin formulations. More than 30% of sleep-support supplement innovation initiatives among major European manufacturers are linked to German research, formulation, or production activities. Strong quality standards continue attracting investment in advanced delivery systems and evidence-based product portfolios.

Manufacturing Scale and Consumer Expansion

Asia-Pacific is emerging as the fastest-expanding market due to increasing health awareness, rising disposable incomes, and expanding nutraceutical manufacturing capacity. The region accounts for approximately 24% of global demand, with production capabilities expanding rapidly across key industrial hubs. Manufacturing investments have increased by nearly 18% over the past two years as companies strengthen domestic supply chains and regional distribution networks. Adoption is being supported by growing utilization of digital commerce channels and broader acceptance of preventive wellness products. Companies are prioritizing local partnerships, production scaling, and product customization to address diverse consumer preferences.

China Market Outlook: China represents the most influential market within Asia-Pacific due to its manufacturing scale, extensive e-commerce ecosystem, and growing wellness consumer base. The country supports a substantial share of regional nutraceutical production and continues attracting investment in advanced supplement manufacturing facilities. Online health-product sales have increased by more than 20% annually, strengthening melatonin accessibility. Local manufacturers are expanding production capabilities while international brands pursue partnerships to improve market penetration and distribution efficiency.

Consumer Wellness Adoption Expands

South America is experiencing steady market development supported by growing awareness of sleep health and expanding access to nutraceutical products. The region contributes approximately 5% of global demand, with urban consumer populations driving adoption through retail and online channels. Product availability has improved through distributor partnerships and regional logistics investments, reducing delivery times by nearly 10% in key markets. However, regulatory complexity and varying market maturity levels continue influencing deployment speed. Companies are balancing expansion opportunities with localized product strategies and distribution network development.

Brazil Market Outlook: Brazil is the region's leading market due to its large consumer base, expanding supplement industry, and strengthening retail infrastructure. National wellness trends are increasing demand for sleep-support products across both traditional and digital sales channels. More than 40% of South American nutraceutical sales activity is concentrated within Brazil. Companies continue investing in local partnerships, marketing initiatives, and product portfolio diversification to strengthen competitive positioning and improve accessibility.

Healthcare Modernization Supporting Adoption

The Middle East & Africa market is benefiting from healthcare modernization initiatives, expanding wellness awareness, and growing investment in consumer health products. The region accounts for approximately 5% of global demand and is increasingly supported by digital retail expansion and premium wellness offerings. Investment in healthcare infrastructure and pharmacy modernization programs has improved product accessibility across major urban centers. Companies are utilizing distributor partnerships and targeted market-entry strategies to overcome fragmented market structures. Operational focus remains on education, awareness building, and supply-chain optimization.

United Arab Emirates Market Outlook: The United Arab Emirates serves as a strategic hub for premium consumer health products and regional distribution activities. Advanced retail infrastructure, strong purchasing power, and a growing wellness-focused population support market expansion. Digital pharmacy adoption has increased by approximately 15% in recent years, improving access to sleep-support products. The country's role as a logistics and trade center enables efficient product distribution, encouraging international brands to establish regional partnerships and strengthen market presence.

The melatonin market is characterized by competition between global supplement leaders such as Natrol, Nature Made, NOW Foods, Life Extension, and Puritan’s Pride, versus regional wellness brands and private-label manufacturers. The top five players collectively account for approximately 34% of market activity, creating a moderately consolidated structure. Competition is centered on formulation technology, brand trust, distribution reach, and supply-chain efficiency rather than price alone. Advanced delivery systems improve product differentiation by nearly 15%, while direct-to-consumer channels enhance customer retention by over 20%. Companies are expanding manufacturing capacity, pursuing retail partnerships, and introducing multifunctional sleep-support products combining melatonin with vitamins and botanicals. Vertical integration and ingredient sourcing control are becoming increasingly important as quality standards tighten. The competitive shift is moving toward personalized wellness ecosystems and science-backed formulations. The primary pressure point remains regulatory compliance across multiple markets. Winning requires formulation innovation, strong distribution networks, operational agility, and consistent product quality.

Natrol

Nature Made

NOW Foods

Life Extension

Puritan’s Pride

GNC Holdings

Swanson Health Products

Jamieson Wellness

Nature's Bounty

Solgar

Douglas Laboratories

Carlson Laboratories

Vitafusion

Pharmavite LLC

Melatonin manufacturing is increasingly leveraging precision microencapsulation, controlled-release delivery systems, and automated dosage management technologies. Controlled-release formulations improve ingredient stability by approximately 18% while reducing potency degradation during storage. More than 35% of newly introduced premium sleep-support products now utilize advanced release technologies. Automated encapsulation and packaging systems have reduced production errors by nearly 12%, improving manufacturing consistency and regulatory compliance. These technologies provide manufacturers with stronger quality control, higher operational efficiency, and improved product differentiation in competitive retail and digital health channels.

Emerging technologies are centered on AI-assisted formulation development, digital sleep analytics integration, and personalized wellness platforms. AI-enabled formulation screening reduces development timelines by approximately 15% compared with conventional trial-and-error methods. Adoption of connected sleep-monitoring applications has increased beyond 25% among active wellness consumers, creating new opportunities for personalized melatonin recommendations. Companies integrating sleep data with supplement programs gain stronger customer retention and improved product targeting, particularly in premium direct-to-consumer channels.

Disruptive innovation is shifting toward smart-release systems and precision-dose formulations. Compared with conventional immediate-release products, advanced dual-phase technologies improve sleep-duration support by approximately 20%. Between 2026 and 2028, brands investing in formulation science, digital health partnerships, and personalized delivery technologies will secure stronger competitive positioning. Market leaders benefit from superior efficacy, consumer engagement, and faster product innovation cycles, making technology adoption a critical operational priority rather than an optional enhancement.

February 2026 – Bonafide Health launched Noctera™, a hormone-free sleep-support supplement targeting menopausal sleep disturbances. The product addresses a demographic spanning women aged 40–64, expanding differentiated sleep-health offerings and strengthening portfolio diversification within the broader sleep wellness category. Source: pharmavite.com

June 2026 – ResMed completed the acquisition of Noctrix Health, adding FDA-classified TOMAC sleep therapy technology to its clinical sleep portfolio. The transaction expands access to treatment for Restless Legs Syndrome, the third most prevalent sleep disorder, strengthening integrated sleep-health capabilities.

May 2026 – Ultra introduced Sleep Pouches featuring six clinically backed ingredients and a smart-dose 1 mg melatonin formulation capable of delivering noticeable effects within 5–10 minutes. The launch expands alternative delivery formats and increases innovation within consumer sleep-support products. \

January 2026 – Therapeutic Goods Administration (Australia) intensified enforcement against counterfeit melatonin imports after laboratory testing identified products containing up to 417% more melatonin than labeled. The action increased regulatory scrutiny, quality-control requirements, and supply-chain compliance expectations across manufacturers. Source: news.com.au

This report provides comprehensive coverage of the global melatonin market across key product types including Tablets, Capsules, Gummies, Liquid Formulations, and Softgels. The analysis evaluates demand patterns across Sleep Disorders, Jet Lag Management, Stress Relief, Circadian Rhythm Support, and General Wellness applications while assessing adoption across Hospitals, Specialty Clinics, Retail Pharmacies, Online Pharmacies, Wellness Centers, and Home Care Users. The study also examines regional deployment trends across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, where more than 60% of product consumption is concentrated within organized retail and pharmacy networks.

The report assesses advanced technologies such as controlled-release formulations, microencapsulation systems, personalized wellness platforms, and digital sleep-health integration. Strategic insights include competitive positioning, supply-chain transformation, regulatory developments, investment priorities, and product innovation strategies. Coverage extends to emerging consumer segments, premium sleep-health solutions, digital distribution ecosystems, and evolving purchasing behaviors between 2026 and 2033, supporting expansion planning, portfolio optimization, partnership decisions, and long-term market positioning.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 2414.85 Million |

|

Market Revenue in 2033 |

USD 9645.98 Million |

|

CAGR (2026 - 2033) |

18.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Natrol, Nature Made, NOW Foods, Life Extension, Puritan’s Pride, GNC Holdings, Swanson Health Products, Jamieson Wellness, Nature's Bounty, Solgar, Douglas Laboratories, Carlson Laboratories, Vitafusion, Pharmavite LLC |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |