Reports

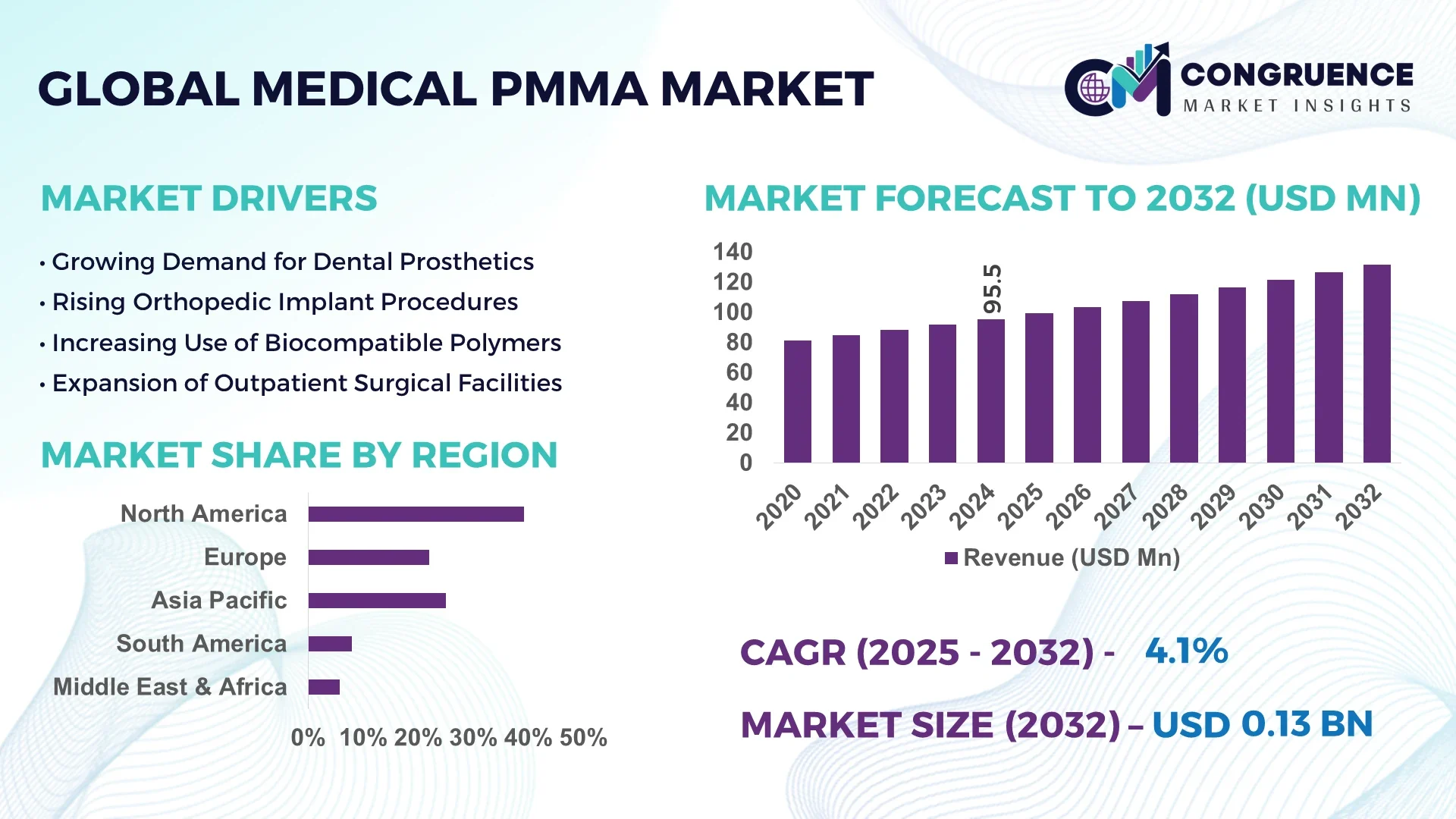

The Global Medical PMMA Market was valued at USD 95.45 Million in 2024 and is anticipated to reach a value of USD 131.63 Million by 2032 expanding at a CAGR of 4.1% between 2025 and 2032.

The United States dominates the global Medical PMMA market, accounting for a significant share in 2024. The country’s extensive use of PMMA in medical devices, dental applications, and bone cement is notable, supporting advanced healthcare infrastructure and continuous innovation in polymer technologies.

Globally, the Medical PMMA market is witnessing steady growth with rising usage in bone cement and intraocular lenses. Approximately 40% of PMMA applications are dedicated to orthopedic surgery, particularly for joint replacement and spinal fixation. Increasing demand for minimally invasive surgical procedures further fuels the adoption of PMMA-based biomaterials. The dental sector accounts for around 25% of market usage, with PMMA extensively utilized in dentures and dental prosthetics due to its aesthetic and physical properties. The ophthalmology segment continues to expand, with over 10 million intraocular lenses made from PMMA implanted annually worldwide. Furthermore, stringent regulatory approvals and advancements in PMMA polymerization techniques have improved product quality and safety, making Medical PMMA a preferred material in medical device manufacturing.Manufacturing facilities worldwide processed over 20,000 tons of medical-grade PMMA in 2024, reflecting robust production capacity to meet growing medical device demands.

Artificial Intelligence (AI) is revolutionizing the Medical PMMA market by enabling precision in design, manufacturing, and application processes. AI-powered 3D printing technologies now allow for customized PMMA implants tailored specifically to patient anatomy, improving surgical outcomes and reducing recovery times. Machine learning algorithms analyze vast clinical data to optimize PMMA formulations for enhanced biocompatibility and mechanical strength. AI-assisted imaging and diagnostic tools help clinicians select the most suitable PMMA products for treatments, thereby reducing failure rates and improving patient safety. In research and development, AI accelerates the discovery of new PMMA composites with added functionalities such as antimicrobial properties or enhanced flexibility.

In manufacturing, AI-driven automation increases production efficiency and reduces defects by monitoring critical parameters during polymerization and molding processes. Predictive maintenance of manufacturing equipment through AI minimizes downtime, ensuring continuous supply of Medical PMMA materials. Additionally, AI-based supply chain optimization enhances inventory management, reducing costs and ensuring timely delivery to medical facilities globally. Overall, the integration of AI in the Medical PMMA market supports innovation, enhances product performance, and contributes to better healthcare outcomes.

“In early 2024, a leading biomaterials company launched an AI-powered platform that designs patient-specific PMMA cranial implants, reducing surgical time by 30% and improving implant fit accuracy, marking a significant advancement in personalized medical devices.”

The rising demand for advanced medical implants is a key growth driver for the Medical PMMA market. With over 20 million joint replacement surgeries performed globally each year, PMMA bone cement is extensively used due to its excellent adhesion and stability. Increasing cases of osteoporosis and fractures in aging populations require durable and safe implant materials, boosting PMMA consumption. The dental sector also sees strong demand for PMMA in prosthetics and orthodontic appliances, driven by growing awareness of oral health and aesthetic needs. Innovations in PMMA formulations that improve longevity and patient comfort further contribute to market growth. The expanding use of PMMA in intraocular lenses for cataract surgeries also supports rising demand in ophthalmology.

Fluctuating raw material prices pose significant restraints to the Medical PMMA market. The production of medical-grade PMMA depends heavily on the availability and cost stability of monomers like methyl methacrylate, which are subject to volatility in the petrochemical industry. Price spikes increase manufacturing expenses, impacting product pricing and profit margins. Additionally, the complexity and costs associated with complying with stringent medical device regulations increase the overall expense of PMMA-based products. Limited availability of specialized medical-grade PMMA variants can lead to supply shortages, hindering market expansion. These financial pressures may delay product launches or limit adoption in price-sensitive regions, restricting the market’s growth potential.

The expansion of personalized and 3D-printed implants presents a significant opportunity in the Medical PMMA market. Customized PMMA implants designed using AI and advanced imaging allow precise anatomical matching, improving patient outcomes and reducing surgical risks. The rising adoption of additive manufacturing techniques enables rapid prototyping and cost-efficient production of complex implant geometries that were previously unattainable. This trend opens new avenues for PMMA applications in cranial, orthopedic, and dental surgeries. Furthermore, increasing investment in research for bioactive PMMA composites with enhanced properties such as antimicrobial effects offers promising growth potential. Emerging markets with growing healthcare infrastructure are also likely to benefit from these innovations.

Strict regulatory requirements and rigorous quality control present ongoing challenges for the Medical PMMA market. Medical-grade PMMA products must comply with high standards of biocompatibility, purity, and mechanical performance, requiring extensive testing and certification. These regulatory hurdles lead to prolonged development cycles and increased costs, potentially delaying market entry for new products. Ensuring consistent quality across large-scale manufacturing is complex, especially when incorporating innovative additives or composite materials. Furthermore, variations in regulatory frameworks across countries complicate global commercialization strategies. These challenges demand significant investment in compliance and quality assurance, impacting smaller manufacturers and limiting rapid expansion.

• Increasing Adoption of Customized Implants: Customized medical implants made from PMMA are gaining traction due to advancements in 3D printing and imaging technologies. Patient-specific cranial and orthopedic implants are increasingly manufactured with PMMA to enhance fit and reduce surgical complications. This trend is especially prominent in North America and Europe, where personalized healthcare solutions are prioritized. The demand for tailored PMMA products that offer superior biocompatibility and strength is reshaping implant manufacturing processes worldwide.

• Growth of Minimally Invasive Surgical Procedures: Minimally invasive surgeries are driving higher demand for Medical PMMA, particularly in orthopedics and ophthalmology. PMMA-based bone cement is favored for joint replacements and spinal surgeries due to its quick setting time and strong fixation properties. In cataract surgeries, PMMA intraocular lenses remain a preferred choice because of their excellent optical clarity and long-term stability. The increased adoption of such procedures is expanding the scope for PMMA applications across healthcare facilities globally.

• Emergence of Antimicrobial PMMA Composites: The integration of antimicrobial agents into PMMA materials is a notable trend addressing infection risks in implants. These advanced composites reduce post-surgical infections and promote faster healing, enhancing patient safety. The demand for such innovative PMMA materials is growing in both dental and orthopedic sectors, where infection prevention is critical. This innovation is expected to improve long-term implant success rates and broaden clinical usage of PMMA.

• Automation and AI in PMMA Manufacturing: Automation technologies and AI-driven quality control systems are increasingly utilized in Medical PMMA production to enhance consistency and reduce defects. Real-time monitoring of polymerization processes ensures optimal material properties and compliance with regulatory standards. AI algorithms also optimize supply chain management and forecast demand trends, improving manufacturing efficiency. These technological advancements are helping manufacturers meet growing market requirements while maintaining high product standards.

The Medical PMMA market is segmented by type, application, and end-user, each reflecting unique demand drivers and growth patterns. Key types include bone cement, intraocular lenses, and dental prosthetics, with bone cement leading due to its widespread use in orthopedic surgeries. Applications range from joint replacement and dental restoration to ophthalmology and cranial implants, where joint replacement holds a dominant share. End-users primarily include hospitals, ambulatory surgical centers, and dental clinics, with hospitals being the largest segment because of their extensive surgical infrastructure. The fastest growth is observed in personalized implant manufacturing driven by rising healthcare customization trends globally, signaling a shift toward more patient-centric medical solutions.

The Medical PMMA market by type comprises bone cement, intraocular lenses, dental prosthetics, and cranial implants. Bone cement remains the leading segment, accounting for over 45% of market volume, owing to its critical role in orthopedic surgeries such as hip and knee replacements. Intraocular lenses represent a significant portion, especially in aging populations with cataracts, driven by their high biocompatibility and optical clarity. Dental prosthetics, including dentures and orthodontic appliances made from PMMA, are expanding rapidly due to rising oral health awareness and cosmetic dentistry demand. Cranial implants, though smaller in volume, are the fastest growing segment because of technological advances in customized 3D printing and reconstructive surgery needs. This diversified product portfolio allows PMMA to penetrate multiple medical specialties efficiently.

Applications in the Medical PMMA market cover orthopedic surgery, dental restoration, ophthalmology, and cranial reconstruction. Orthopedic surgery dominates, accounting for more than half of the application share, propelled by increasing joint replacement surgeries globally. Dental restoration follows closely with high demand for prosthetics and orthodontics, especially in developed countries where cosmetic dentistry is popular. Ophthalmology applications are also significant, with PMMA used extensively in intraocular lenses for cataract treatment. Cranial reconstruction is a niche but rapidly expanding application, benefiting from the rise of personalized implants tailored via advanced imaging and 3D printing technologies. The growth in minimally invasive surgical techniques across these fields further accelerates demand for PMMA materials.

Hospitals represent the largest end-user segment in the Medical PMMA market, leveraging extensive surgical departments and specialized care units for orthopedic, dental, and ophthalmic procedures. This segment accounts for over 60% of market consumption, driven by rising surgical volumes and investments in advanced medical technologies. Ambulatory surgical centers are emerging as the fastest growing end-user segment due to increasing outpatient procedures and cost-effectiveness compared to hospital stays. Dental clinics also form a significant share, with rising demand for cosmetic and restorative dental treatments fueling PMMA use. Additionally, research institutes and specialized implant manufacturers contribute to market growth by developing innovative PMMA applications. This diverse end-user base ensures widespread adoption across healthcare sectors.

North America accounted for the largest market share at 39.2% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2025 and 2032.

North America leads due to advanced healthcare infrastructure and high adoption of innovative medical materials like PMMA for orthopedic and ophthalmic applications. Europe holds a significant share at 28%, driven by rising geriatric population and increasing surgical procedures requiring PMMA implants. Asia-Pacific’s rapid urbanization and growing healthcare investments contribute to its fast expansion. South America and the Middle East & Africa together hold smaller shares but are witnessing steady growth due to improving medical facilities and government support in healthcare sectors.

"Innovation and Precision Drive Market Growth"

The North American Medical PMMA market is witnessing steady demand driven by the U.S. and Canada, accounting for over 35% of the regional market. High prevalence of osteoarthritis and cataracts has increased the usage of PMMA-based bone cements and intraocular lenses. Research and development investments in biocompatible materials enhance product innovation. Hospitals and outpatient surgical centers are expanding their services, driving demand for PMMA implants and prosthetics. Moreover, regulatory approvals for new PMMA composites supporting antimicrobial properties are boosting market penetration. The region is also focusing on personalized medicine, with customized PMMA implants gaining traction for reconstructive surgeries.

"Sustainability and Regulatory Excellence Fuel Industry Expansion"

Europe holds around 28% of the global Medical PMMA market, with Germany, France, and the UK leading adoption. Increasing aging populations in these countries fuel demand for orthopedic implants and dental prosthetics made from PMMA. The region emphasizes high-quality standards and safety, leading to stringent regulations that enhance market reliability. Advancements in minimally invasive surgeries across European healthcare systems are boosting PMMA consumption. Additionally, the rise of dental tourism in countries like Spain and Hungary increases demand for dental prosthetics. Collaborations between research institutes and medical device manufacturers also foster innovation in PMMA applications.

"Rapid Industrial Expansion and Rising Healthcare Demand Boost Market Potential"

Asia-Pacific accounts for approximately 20% of the Medical PMMA market, led by countries such as China, Japan, and India. Rapid urbanization, increasing healthcare awareness, and expanding surgical infrastructure drive market growth. Rising incidence of lifestyle diseases requiring joint replacements and dental treatments contributes to higher PMMA usage. The growing middle class and increasing government healthcare expenditure support the expansion of hospitals and clinics equipped with advanced medical PMMA products. Additionally, the adoption of 3D printing technology in implant customization is accelerating market development. Regional manufacturers are focusing on affordable yet high-quality PMMA products to meet diverse market needs.

"Emerging Healthcare Infrastructure Spurs Market Development"

South America holds nearly 8% of the global Medical PMMA market, with Brazil and Argentina being the dominant players. Increasing investments in healthcare infrastructure and rising awareness about advanced medical treatments boost the demand for PMMA bone cements and dental prosthetics. Brazil accounts for the majority of regional consumption, supported by government initiatives to improve access to orthopedic and dental care. The growing elderly population and increasing incidence of trauma-related surgeries further propel market expansion. Additionally, growing private healthcare facilities and the rise of outpatient surgical centers in urban areas contribute to increasing PMMA adoption.

"Healthcare Modernization and Investment Power Market Growth"

The Middle East & Africa region represents about 6% of the Medical PMMA market, with Saudi Arabia and South Africa leading in adoption. Healthcare infrastructure developments and increasing medical tourism in these countries are key drivers of market growth. Saudi Arabia's investments in orthopedic and ophthalmic surgical centers support higher PMMA demand, especially for bone cement and intraocular lenses. South Africa's expanding private healthcare sector also contributes to growing PMMA usage in dental and reconstructive surgeries. Moreover, government initiatives aimed at improving healthcare access and quality are fostering steady market expansion across the region.

United States – 34% (2024): Leads the Medical PMMA market due to its advanced healthcare infrastructure and high adoption of innovative PMMA-based medical devices across orthopedic and ophthalmic sectors.

Germany – 15% (2024): Holds a significant share driven by a large aging population and stringent regulatory standards that ensure the quality and safety of PMMA medical products.

The Medical PMMA market is characterized by intense competition among key players focusing on innovation, product quality, and geographic expansion. Leading companies are investing heavily in research and development to introduce advanced PMMA materials with enhanced biocompatibility and mechanical properties tailored for medical applications such as orthopedic implants, dental prosthetics, and ophthalmic devices. Strategic collaborations and partnerships are common as companies aim to strengthen their market presence globally. Additionally, many market leaders are expanding their production capacities and distribution networks to meet growing demand in emerging regions. The focus on sustainability and regulatory compliance is pushing firms to develop eco-friendly PMMA products with lower environmental impact. Competitive pricing strategies and product differentiation also play a significant role in capturing market share. As a result, companies with strong innovation pipelines and robust supply chains continue to dominate, while smaller players strive to carve niche segments within the expanding medical PMMA market landscape.

Evonik Industries AG

Röhm GmbH

Mitsubishi Chemical Corporation

Arkema Group

Lucite International

Ensinger GmbH

Cyro Industries

Mitsubishi Gas Chemical Company

Evonik Degussa GmbH

Arkema Inc.

Technological advancements in the Medical PMMA market have significantly improved the performance and versatility of PMMA materials for medical applications. One key development is the enhancement of polymerization processes that produce ultra-pure PMMA with superior optical clarity, which is critical for applications such as intraocular lenses used in cataract surgery. Advanced copolymerization techniques have also enabled the creation of PMMA blends with improved flexibility and impact resistance, expanding their use in orthopedic devices and dental prosthetics. In recent years, surface modification technologies like plasma treatment and ion implantation have been adopted to enhance PMMA’s biocompatibility and reduce bacterial adhesion, thereby lowering the risk of post-surgical infections. These surface treatments improve the integration of implants with surrounding tissues, leading to better clinical outcomes.

Additive manufacturing, particularly 3D printing, is another transformative technology in the Medical PMMA sector. It allows for precise customization of implants and prosthetics tailored to individual patient anatomy, improving fit and comfort. PMMA-based filaments and resins compatible with 3D printing are gaining traction for rapid prototyping and final product manufacturing. Additionally, the integration of nanotechnology has led to the development of PMMA nanocomposites incorporating bioactive particles such as hydroxyapatite, which promote bone regeneration and enhance mechanical strength. Automation and AI-driven quality control systems have also been implemented in PMMA manufacturing plants, ensuring consistent product quality and reducing defects during production. These technological insights highlight how innovation continues to drive the Medical PMMA market forward, enabling safer, more effective, and patient-specific medical solutions.

In June 2024, LAPP introduced the ETHERLINE® FD bioP Cat.5e, its first bio-based Ethernet cable produced in series. This sustainable variant features a bio-based outer sheath composed of 43% renewable raw materials, reducing the carbon footprint by 24% compared to traditional fossil-based TPU sheaths.

In March 2024, Mitsubishi Chemical unveiled an advanced PMMA polymer with increased resistance to hydrolysis, targeting orthopedic implant manufacturers seeking longer implant lifespans under physiological conditions.

In July 2023, Arkema expanded its PMMA production capacity in Europe to meet rising demand for medical-grade materials, incorporating eco-efficient processes that reduce energy consumption during manufacturing.

In January 2024, Röhm GmbH introduced a bio-based PMMA variant suitable for ophthalmic lenses, emphasizing sustainability by utilizing renewable raw materials without compromising optical clarity and biocompatibility.

The scope of the Medical PMMA market report encompasses a comprehensive analysis of key market segments, including types, applications, and end-users within the healthcare and medical industries. The report details the production, consumption, and demand trends of polymethyl methacrylate (PMMA) specifically tailored for medical use, highlighting materials used in devices such as intraocular lenses, bone cement, dental prosthetics, and various implants. It covers innovations in bio-based and high-performance PMMA variants, emphasizing their role in improving patient outcomes and device longevity. Geographically, the report spans major regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, providing insights into regional market dynamics and growth potential. It also addresses the impact of regulatory frameworks and standards that govern medical-grade PMMA manufacturing, ensuring safety and compliance in critical applications.

The report highlights competitive analysis, profiling leading manufacturers, and their strategic initiatives such as capacity expansions, product launches, and sustainability efforts. Additionally, it explores technological advancements in PMMA polymerization processes and enhancements in material properties like transparency, biocompatibility, and mechanical strength. Overall, the report serves as a vital resource for stakeholders, offering data-driven insights into market size, demand drivers, challenges, and opportunities shaping the future of the Medical PMMA industry.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 95.45 Million |

|

Market Revenue in 2032 |

USD 131.63 Million |

|

CAGR (2025 - 2032) |

4.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Evonik Industries AG, Röhm GmbH, Mitsubishi Chemical Corporation, Arkema Group, Lucite International, Ensinger GmbH, Cyro Industries, Mitsubishi Gas Chemical Company, Evonik Degussa GmbH, Arkema Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |