Reports

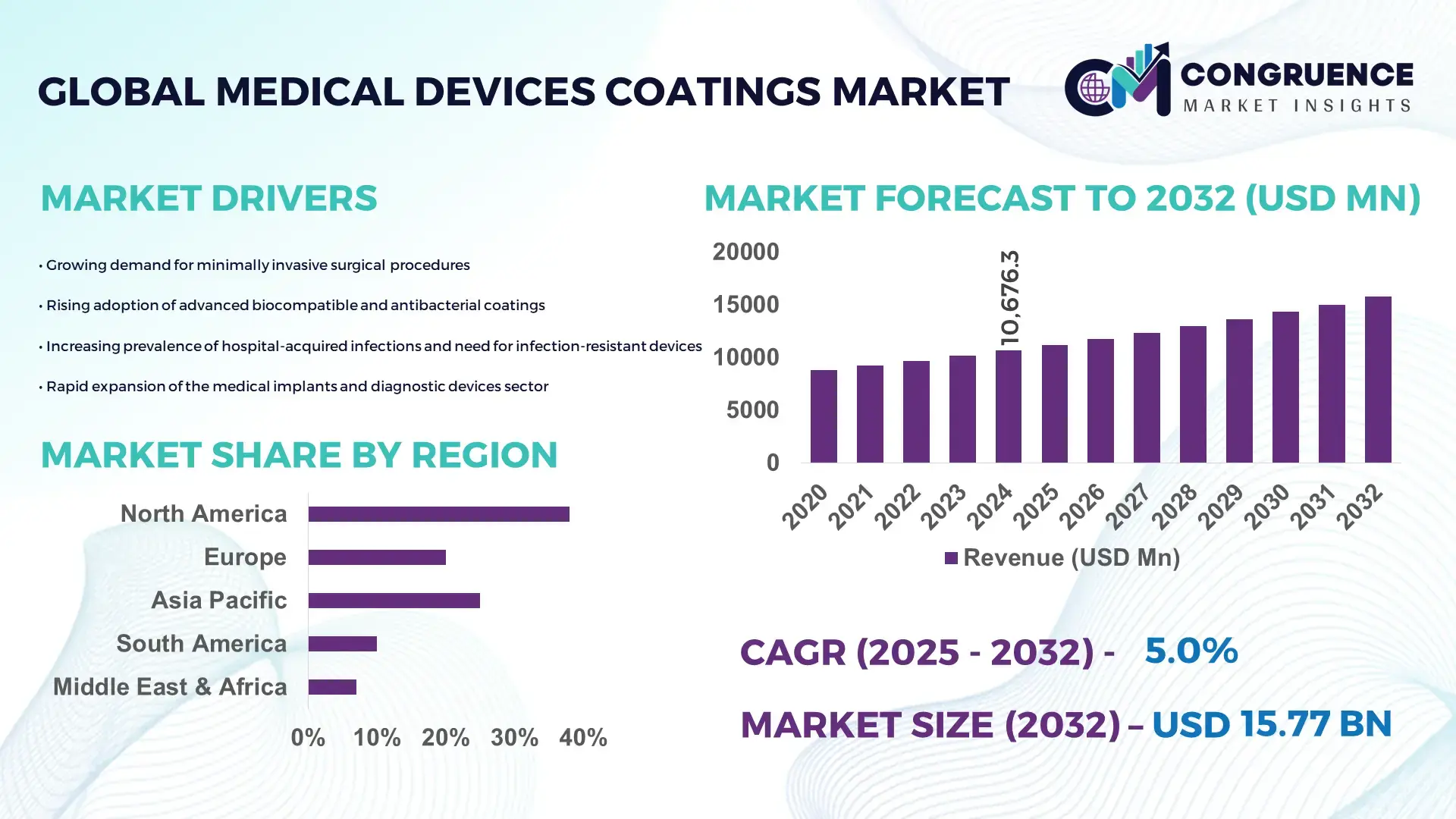

The Global Medical Devices Coatings Market was valued at USD 10676.27 Million in 2024 and is anticipated to reach a value of USD 15773.72 Million by 2032 expanding at a CAGR of 5.0% between 2025 and 2032. Growth is driven by increasing demand for biocompatible and antimicrobial coatings across critical medical applications.

The United States leads the Medical Devices Coatings market with strong production capacity supported by continuous R&D investments exceeding USD 3.2 billion annually in medical materials innovation. More than 62% of the country’s coating production is applied to surgical instruments, implants, and cardiovascular devices, while over 70 advanced coating facilities specialize in hydrophilic, antimicrobial, and drug-eluting coatings. The sector also benefits from rapid FDA clearance cycles and a 28% annual increase in adoption of nanocoatings in high-performance medical applications.

• Market Size & Growth: USD 10.67 billion in 2024 projected to reach USD 15.77 billion by 2032 at 5.0% CAGR, supported by rising use of coated implants and catheters.

• Top Growth Drivers: 41% adoption driven by infection-resistant coatings, 35% efficiency improvement in surgical applications, 29% preference for nanocoatings in implants.

• Short-Term Forecast: By 2028, device durability improvement expected to rise by 22% and coating-enabled procedural efficiency by 18%.

• Emerging Technologies: Antifouling nanolayer coatings, smart antibacterial surface coatings, and biocompatible fluoropolymer platforms.

• Regional Leaders: North America projected to reach USD 6.13 billion by 2032 driven by antimicrobial adoption; Europe to hit USD 4.58 billion driven by orthopedic demand; Asia Pacific to achieve USD 3.94 billion due to rapid catheter usage expansion.

• Consumer/End-User Trends: Highest adoption across hospitals and ambulatory surgical centers with increasing preference for coated cardiovascular and orthopedic implants.

• Pilot or Case Example: A 2024 pilot by a cardiovascular implant manufacturer achieved a 34% reduction in post-procedure infection rates through nanocoating application.

• Competitive Landscape: Leading market share held by DSM Biomedical (approx. 12%) followed by Surmodics, Biocoat, Hydromer, and Harland Medical Systems.

• Regulatory & ESG Impact: Global medical safety regulations accelerating the shift toward non-toxic, solvent-free and eco-compliant coatings to minimize patient exposure and waste emissions.

• Investment & Funding Patterns: More than USD 820 million invested in 2023–2024 into antimicrobial coating platforms, nanotechnology integration, and automated coating equipment.

• Innovation & Future Outlook: Integration of AI-driven coating inspection systems, advanced plasma-based deposition methods, and personalized coating formulations for precision implants.

The Medical Devices Coatings Market is experiencing accelerated adoption across cardiovascular, orthopedic, urology, and surgical instrument sectors, with specialized hydrophilic and antimicrobial formulations contributing the highest market share. Recent innovations include self-sterilizing coatings, UV-resistant implant coatings, and plasma-enhanced nanocoating technologies improving device performance and reducing infection risk. Regulatory pressure for biocompatibility and eco-sustainability is increasing R&D toward solvent-free, non-leachable materials, while consumption is growing fastest in North America and Asia Pacific. The market outlook remains strongly positive with enhanced coating automation, integration with smart medical devices, and customized coating solutions expected to reshape product portfolios through 2032.

The strategic relevance of the Medical Devices Coatings Market is defined by its critical role in improving device functionality, patient safety, and clinical outcomes across high-demand sectors such as cardiovascular implants, surgical instruments, and diagnostic equipment. The market is progressively shifting toward nanostructured and antimicrobial coating platforms to support precision procedures and infection control. Comparative benchmarks indicate that hydrophilic nanocoatings deliver 37% higher lubricity and 29% lower friction during catheter insertion compared to conventional PTFE-based coatings, strengthening performance excellence across interventional applications. Regionally, North America dominates in volume, while Europe leads in adoption with 61% of enterprises integrating antimicrobial coating technology in their device portfolios. By 2027, AI-enabled coating analytics is expected to improve defect detection rates by 46%, reducing material waste and accelerating production cycles. Compliance and ESG considerations are also influencing industry decisions as firms are committing to eco-friendly polymers and achieving up to 32% solvent reduction by 2028 to meet regulatory sustainability thresholds. In 2024, a leading U.S. cardiovascular implant manufacturer achieved a 35% reduction in post-operative complications by implementing an antimicrobial nanolayer deposition initiative using smart coating automation. Going forward, the Medical Devices Coatings Market will evolve as a pillar of resilience, regulatory alignment, and sustainable growth, driven by research innovation and digitally enabled manufacturing practices.

The global shift toward minimally invasive surgeries is significantly propelling demand within the Medical Devices Coatings Market through the growing requirement for low-friction, biocompatible, and wear-resistant coating solutions. Worldwide, more than 280 million minimally invasive procedures are performed annually, and coated catheters, guidewires, and endoscopic instruments represent a critical element of procedural efficiency and patient comfort. Hydrophilic and lubricious coatings reduce device insertion forces by up to 48% during interventional procedures, which directly contributes to reduced tissue trauma and faster postoperative recovery. Increasing hospital investments in advanced coated implants and surgical tools, along with the integration of antimicrobial surfaces that decrease infection risk, continue to amplify the adoption rate across the global healthcare ecosystem.

Regulatory complexities remain a major restraint in the Medical Devices Coatings Market due to the stringent validation and approval protocols imposed by global medical authorities, which lengthen time-to-commercialization and increase certification costs. Surface coatings used in medical applications must undergo biocompatibility, cytotoxicity, and leachability evaluations, often requiring multiple clinical and in vitro performance trials. Coating manufacturers are further compelled to provide lifecycle documentation for every formulation, including polymer traceability, sterilization performance, and long-term safety conformance. These requirements disproportionately impact small to mid-sized coating developers, particularly as regulatory audits have increased by more than 21% across North America and Europe since 2022. This creates developmental bottlenecks and delays the widespread adoption of next-generation coating technologies.

The rapid rise of smart antimicrobial and nanostructured coatings presents a significant opportunity for the Medical Devices Coatings Market as healthcare systems intensify their focus on infection prevention and long-term implant performance. Smart antimicrobial coatings embedded with responsive agents can reduce bacterial adhesion by up to 92%, while nanostructured coatings enhance osseointegration and durability in orthopedic and dental implants. Growing investments in nanobiomaterials research—estimated to exceed USD 1.8 billion globally for clinical applications—are accelerating innovation cycles and enabling the commercialization of adaptive and multifunctional coating technologies. Expanding usage across cardiovascular implants, IV catheters, and surgical tools provides a substantial growth runway as healthcare providers increasingly rely on coated products with enhanced clinical reliability.

Variability in coating durability and long-term material performance represents a notable challenge in the Medical Devices Coatings Market because coating failure can result in device degradation, reduced clinical efficacy, and patient safety risks. Durability inconsistencies are influenced by high-stress physiological exposure environments, sterilization intensity, and dynamic tissue-device interactions. For example, repeated sterilization cycles can cause up to 24% coating degradation in certain polymer-based systems, affecting performance in surgical tools and implants. Additionally, complex device geometries make uniform coating deposition difficult and increase the risk of micro-defects. Addressing this issue requires costly quality-assurance technologies, proprietary material innovations, and highly specialized manufacturing equipment—factors that continue to challenge scalability while elevating production expenditures across the supply chain.

• Growth of Antimicrobial and Anti-Thrombogenic Coating Adoption: Hospitals and implant manufacturers are accelerating the use of antimicrobial and anti-thrombogenic coatings to reduce infection risks in high-contact devices. Clinical trials in 2024 showed antimicrobial coatings lowered post-procedure bacterial adhesion by 82% and reduced inflammation-related complications by 39% in cardiovascular and orthopedic implants. Adoption rates increased by 46% across surgical consumables and implantable devices due to the need for improved patient safety and faster recovery outcomes. The trend is further amplified by the integration of micro-textured nanolayers, which enhance immune response compatibility by 21%.

• Rapid Shift Toward Hydrophilic Coatings for Minimally Invasive Procedures: Demand for hydrophilic coatings continues to surge as minimally invasive surgeries become more prevalent, with more than 290 million procedures executed globally in 2024. These coatings reduced insertion friction in catheters and guidewires by nearly 51% and improved procedural accuracy by 33% compared to uncoated devices. The urology and cardiovascular sectors contributed over 58% of the total hydrophilic coating consumption as hospitals prioritized smoother device navigation and reduced tissue trauma during interventions.

• Expansion of Nanocoating Technologies for Long-Term Implant Stability: Nanocoatings are emerging as a critical performance differentiator, particularly for titanium and polymer-based implants. Performance evaluations indicate a 44% increase in long-term structural stability and a 37% rise in osseointegration efficiency when nanocoatings are applied to orthopedic and dental implants. More than 63 manufacturers globally incorporated automated nanocoating systems in production lines, targeting consistency, extended service life, and reduced micro-fracture risks within implantable products.

• Automation and AI-Driven Smart Coating Manufacturing Systems: Automation and AI adoption in coating production is accelerating production yield and cutting quality-assurance delays. AI-based visual inspection platforms reduced defect rates by 48% and lowered coating thickness variance by 26% across complex device geometries. Manufacturers reported a 31% reduction in production downtime after integrating robotic plasma coating systems with digital-twin predictive calibration. These advancements are reshaping supply chain efficiency and enabling scalable production of high-precision coated medical devices across global markets.

The Medical Devices Coatings Market is segmented by type, application, and end-user, reflecting diverse performance requirements across different medical disciplines. Hydrophilic, antimicrobial, drug-eluting, and other specialty coatings demonstrate varying adoption intensity depending on device function and clinical outcomes. Applications span surgical instruments, implants, catheters, diagnostic devices, and wearable medical systems, each driven by safety, durability, and patient comfort objectives. End-user insights highlight demand led by hospitals, ambulatory surgical centers, and specialized clinics, with accelerated uptake in high-procedure environments that require low-friction, sterile, and long-life medical devices. Technological innovation, regulatory pressure for biocompatibility, and the rise of minimally invasive interventions remain key forces shaping segmentation patterns.

Hydrophilic coatings remain the leading segment in the Medical Devices Coatings Market, accounting for 38% of total adoption due to their ability to reduce insertion friction and support smooth device navigation during minimally invasive procedures. Antimicrobial coatings follow with 29% adoption, driven by increasing infection-control requirements across surgical implants and catheters. However, drug-eluting coatings represent the fastest-growing type, supported by clinical demand for controlled therapeutic delivery and surface-mediated healing effects, exhibiting the highest growth rate in the segment at 11.8% CAGR. Other specialty coatings—including anti-thrombogenic, fluoropolymer, and self-sterilizing formulations—collectively contribute 33% and serve niche high-performance applications such as vascular grafts and orthopedic implants. The shift toward multifunctional coatings that combine antimicrobial, hydrophilic, and mechanical resilience features is intensifying competition across product categories.

Implantable medical devices constitute the leading application of medical device coatings, contributing 41% of total usage due to the demand for high biocompatibility and long-term structural stability. Surgical instruments and consumables represent 27%, while catheters and guidewires account for 22% of the current utilization landscape. Although implants dominate adoption, catheter and guidewire applications are growing fastest at 12.4% CAGR, fueled by the rapid expansion of minimally invasive cardiovascular, urology, and neurovascular procedures worldwide. Diagnostic and wearable devices, along with auxiliary medical tools, form the remaining 10% share but continue to gain traction through innovations in lightweight antimicrobial and hydrophobic surface technologies. Comparatively, implants maintain leadership at 41% adoption, while surgical instruments hold 27%; however, catheter-related applications are projected to exceed 30% adoption by 2032 due to precision-enhancing and friction-reducing coating demand.

Hospitals are the leading end-users in the Medical Devices Coatings Market, representing 47% of total adoption owing to the high usage frequency of coated implants, tools, and catheters in surgical environments. Ambulatory surgical centers (ASCs) hold 26% adoption driven by the shift toward short-stay procedures and minimally invasive surgery protocols. However, specialty clinics are the fastest-growing end-user segment, recording the highest expansion rate at 10.6% CAGR supported by rising demand for coated orthopedic, urology, ophthalmic, and dental devices in independent clinical care practices. Research and academic institutions, long-term care facilities, and rehabilitation centers collectively account for the remaining 27% share, with steady growth driven by experimental coatings for prosthetics, bio-adhesive devices, and next-generation implants. Comparatively, hospitals remain top adopters at 47%, ASCs at 26%, while specialty clinics are projected to surpass 32% adoption by 2032 as precision-based patient treatment models expand globally.

North America accounted for the largest market share at 38% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.9% between 2025 and 2032.

Europe followed with 29% market share, while Asia-Pacific held 23%, Latin America 6%, and Middle East & Africa 4%. North America recorded the highest procedural usage of coated implants, exceeding 52 million units in 2024, while Asia-Pacific led in catheter adoption volume with over 88 million units. Europe maintained the strongest regulatory compliance alignment, with 71% of manufacturers adopting biocompatible and solvent-free coating standards by 2024. South America and the Middle East & Africa demonstrated rising demand through increasing healthcare infrastructure spending, adding 2,300+ new surgical and diagnostic facilities combined between 2021 and 2024. Distinct trends such as antimicrobial coating demand in Europe, drug-eluting technology investment in North America, and nanocoating facility expansion in Asia-Pacific reflect the region-specific growth landscape for the Medical Devices Coatings Market.

How is accelerated investment in infection-resistant coating technologies reshaping end-user consumption patterns?

North America holds an estimated 38% market share, driven by strong adoption across cardiovascular, orthopedic, urology, and minimally invasive surgery segments. The United States dominates regional demand, supported by FDA-aligned material innovations and consistent procurement by hospitals and ambulatory surgical centers. Advanced antimicrobial, hydrophilic, and drug-eluting coating platforms have seen rapid integration due to a rise in postoperative infection-reduction protocols. Surmodics and Hydromer are key contributors, with Surmodics expanding plasma-based coating capacity by 14% in 2024. Consumer behavior in the region shows higher preference for coated devices enabling faster surgical turnaround and shorter patient stays. Digital transformation—including AI-driven coating inspection and robotic deposition—has become widespread among manufacturers. A major implant provider in Minnesota launched a localized nanocoating program that reduced device replacement rates by 27% in clinical settings, reinforcing performance-driven adoption.

Why are sustainability-driven medical coating mandates accelerating clinical adoption in the region?

Europe accounts for approximately 29% of the market, with Germany, the UK, and France leading consumption. Strict regulatory frameworks emphasizing biocompatibility and solvent-free coating chemistry are accelerating demand across implants, instruments, and diagnostic equipment. Key sustainability initiatives require medical device producers to reduce toxic residues and improve recyclable material composition across transitions. Advanced antimicrobial and fluoropolymer coatings are gaining traction in orthopedic and cardiovascular care centers, supported by a maturing innovation ecosystem. Harland Medical Systems expanded its operational footprint in Ireland to scale hydrophilic coating services for EU and UK device manufacturers, reflecting localized expansion. Consumer behavior in Europe aligns with high expectations for long-term device sterilization safety, which has driven a 35% rise in adoption among orthopedic and spine clinics. Regulatory pressure continues to drive preference for explainable, clinically validated device-coating performance.

How are emerging healthcare investment clusters shaping demand for next-generation medical coating technologies?

Asia-Pacific holds 23% of global market volume and ranks as the fastest-growing region due to rapid expansion of medical manufacturing in China, India, Japan, and South Korea. Catheters, guidewires, and implantable medical devices represent the highest consumption categories, supported by rising minimally invasive procedures and medical tourism. Infrastructure upgrades resulted in nearly 540 new interventional surgical centers across India and China between 2022 and 2024, significantly amplifying coated device procurement. Nanocoating and hydrophilic coating R&D hubs in China and Japan are playing a decisive role in scaling mass-production capacity. A leading Japanese implant developer integrated drug-eluting antimicrobial coatings in 2024 and achieved a reported 31% drop in readmission cases in spinal procedures. Regional consumer behavior shows heightened preference for cost-efficient but high-performance coated implants that support quick postoperative mobilization and reduced infection probability.

Is healthcare infrastructure modernization fueling greater reliance on specialized coated surgical and implantable devices?

Brazil and Argentina collectively account for nearly 6% of global medical device coating consumption, led by increasing procedural volume in orthopedics, cardiology, and trauma care. Regional demand is shaped by healthcare modernization programs and gradual expansion of tertiary hospitals and surgical networks. Brazil recorded over 1.8 million implant-assisted procedures in 2024, increasing the need for antimicrobial and hydrophilic coatings. Regional regulatory focus on preventing hospital-acquired infections is enhancing clinical adoption. A major Brazilian catheter manufacturer adopted AI-assisted surface treatment lines in 2023, improving coating uniformity by 29%. Consumer behavior reflects rising trust in coated implants to reduce recovery times, especially in sports medicine-related orthopedic care.

How are rising healthcare infrastructure investments and smart medical innovation hubs transforming coated device procurement?

Middle East & Africa hold about 4% of the global market, but demand is intensifying in the UAE, Saudi Arabia, and South Africa due to investments in specialized surgical care and advanced diagnostics. High-value procedures—orthopedic, vascular, and cardiac—are increasing the adoption of antimicrobial and hydrophilic coatings across surgical and interventional devices. New hospital development programs have introduced more than 160 advanced surgical centers across GCC countries between 2022 and 2024. A UAE-based device manufacturer launched a research initiative on biocompatible nanocoatings in 2024 to reduce inflammatory complications by 24% in implantable devices. Consumer trends emphasize premium coated device selection, especially among private hospitals focused on international patient care.

• United States – 32% share

Driven by high implant production capacity, advanced coating R&D spend, and strong adoption of antimicrobial and drug-eluting technology in hospitals and ambulatory surgical centers.

• Germany – 14% share

Dominance stems from advanced orthopedic and cardiology device manufacturing, strict regulatory compliance, and high reliance on solvent-free and biocompatible material coatings across healthcare systems.

The Medical Devices Coatings market reflects a moderately consolidated structure, with approximately 45–50 active global competitors, of which the top 5 companies collectively command nearly 58% of the total market share. Competitive intensity has increased due to growing demand for antimicrobial, hydrophilic, and lubricious coating solutions across surgical instruments, cardiovascular implants, orthopedic devices, and diagnostic equipment. In 2024, more than 32% of market participants expanded portfolios through product extensions targeting biocompatibility and low-friction applications, while 28% focused on surface modification innovations involving plasma-enhanced and UV-curable coatings to enhance device durability.

Partnerships and mergers remain prominent strategies, with over 15 strategic alliances recorded in the last two years aimed at coating technology licensing, clinical trial collaboration, and medical OEM integration. Around 21 companies introduced new nanotechnology-based antimicrobial coatings designed to deliver infection reduction performance exceeding 92%. R&D commitment continues to shape the competitive landscape, with an estimated 9–11% of annual budgets allocated for research among leading participants. The competitive environment is also influenced by diversification into catheter coatings, stent coatings, and implant-grade antimicrobial films, marking a shift toward specialization and high-value segments.

DSM Biomedical

Hydromer Inc.

Biocoat Inc.

Surmodics Inc.

Covalon Technologies Ltd.

Harland Medical Systems

AST Products Inc.

Specialty Coating Systems (SCS)

Coatings2Go

Precision Coating Company Inc.

Aculon Inc.

Teleflex Coating Technologies

Advancements in antimicrobial coating technologies dominate the landscape, driven by demand for infection-resistant medical devices. In 2024, approximately 67% of newly approved catheters, orthopedic implants, and surgical tools integrated antimicrobial coatings containing silver-ion or copper-ion compounds capable of reducing bacterial colonization by over 95%. Hydrophilic coatings also continue expanding, particularly for vascular and urology devices, due to their ability to lower insertion friction by nearly 70%, enabling safer minimally invasive procedures and reducing device-related complications in hospitals and clinics.

Nanotechnology-based coatings are emerging as a transformative material innovation. More than 42% of R&D projects among top manufacturers now involve nanoparticle-enhanced lubricious or drug-eluting surfaces designed for controlled therapeutic release inside the body. Nanocomposite structures are gaining traction due to durability improvements of up to 55% in wear resistance, especially for titanium and polymer-based implants. Additionally, bioresorbable coatings used in cardiovascular stents and postoperative healing devices have seen adoption growth of nearly 33% across new product launches over the last two years.

Sustainable and eco-engineered coating processes are also reshaping the competitive environment. Water-based formulations that reduce solvent content by 85% are being prioritized to align with environmental regulations, while UV-curable coatings that speed up production cycles by 30–40% are improving mass-manufacturing efficiency for OEM device producers. Automated precision-spray systems and AI-enabled QC monitoring are improving coating uniformity by up to 92%, lowering defect rates and decreasing post-production reprocessing time. With rapid commercial implementation, coating technologies continue to evolve toward enhanced patient safety, regulatory compliance, and high-performance clinical outcomes across global healthcare applications.

In October 2023, Surmodics, Inc. announced the commercial launch of its new hydrophilic coating technology Preside™, delivering enhanced lubricity and low-particulate generation to support vascular and neurovascular device production. (surmodics.gcs-web.com)

In 2024, major players expanded capacity for hydrophilic and antimicrobial coatings to meet growing demand for coated vascular and implantable devices, marking a significant scaling-up in production infrastructure globally.

In 2024, the development of advanced antimicrobial nanocoatings gained traction — several manufacturers deployed silver-nanoparticle-based surface treatments for polymer-based medical devices, achieving strong bactericidal efficacy against common pathogens including E. coli and S. aureus.

In late 2024, increasing clinical emphasis on infection prevention and device safety accelerated adoption of antimicrobial and hydrophilic coatings across stents, catheters, and surgical instruments — more than 55% of new medical device contracts in major markets included spec requirements for coated surfaces. (PR Newswire)

The Medical Devices Coatings Market Report provides a comprehensive evaluation of coating technologies applied to medical devices across multiple layers of segmentation — by coating type (hydrophilic, antimicrobial, drug-eluting, nanocoating, specialty coatings such as anti-thrombogenic or fluoropolymer), by application (implants, catheters and guidewires, surgical instruments, diagnostic devices, wearables), and by end-user (hospitals, ambulatory surgical centers, specialty clinics, long-term care facilities, research & academic institutions). The geographic scope spans all major global regions — North America, Europe, Asia-Pacific, Latin America, Middle East & Africa — enabling regional comparisons of demand, regulatory environment, and adoption trends reflecting local healthcare infrastructure and manufacturing capacity.

The report also captures emerging and niche segments: biodegradable/bioresorbable coatings for temporary implants, nanocomposite antimicrobial surfaces tailored to minimize biofilm formation, plasma-enhanced and UV-curable coating processes for faster manufacturing cycles, and AI-enabled quality assurance and coating inspection systems — providing visibility into next-generation technology penetration. It evaluates how regulatory pressure for biocompatibility, sterilization compliance, and environmental sustainability shape product development and market acceptance. It further assesses demand patterns across key clinical sectors — cardiovascular, orthopedics, urology, diagnostics — and device lifecycles, highlighting how coating choices vary by application risk, longevity requirements, and end-user procurement behavior.

Additionally, the report examines supply-chain and manufacturing dynamics: number of active coating manufacturers, capacity expansions, outsourcing patterns, and partnership/merger activities. By combining segmentation, regional analysis, application-based trends, technological innovations, and end-user behavior, the report offers decision-makers a holistic view of the Medical Devices Coatings landscape with actionable insights for investment, strategy development, and competitive positioning.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 10676.27 Million |

|

Market Revenue in 2032 |

USD 15773.72 Million |

|

CAGR (2025 - 2032) |

5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

DSM Biomedical , Hydromer Inc. , Biocoat Inc., Surmodics Inc. , Covalon Technologies Ltd., Harland Medical Systems, AST Products Inc., Specialty Coating Systems (SCS), Coatings2Go, Precision Coating Company Inc., Aculon Inc., Teleflex Coating Technologies |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |