Reports

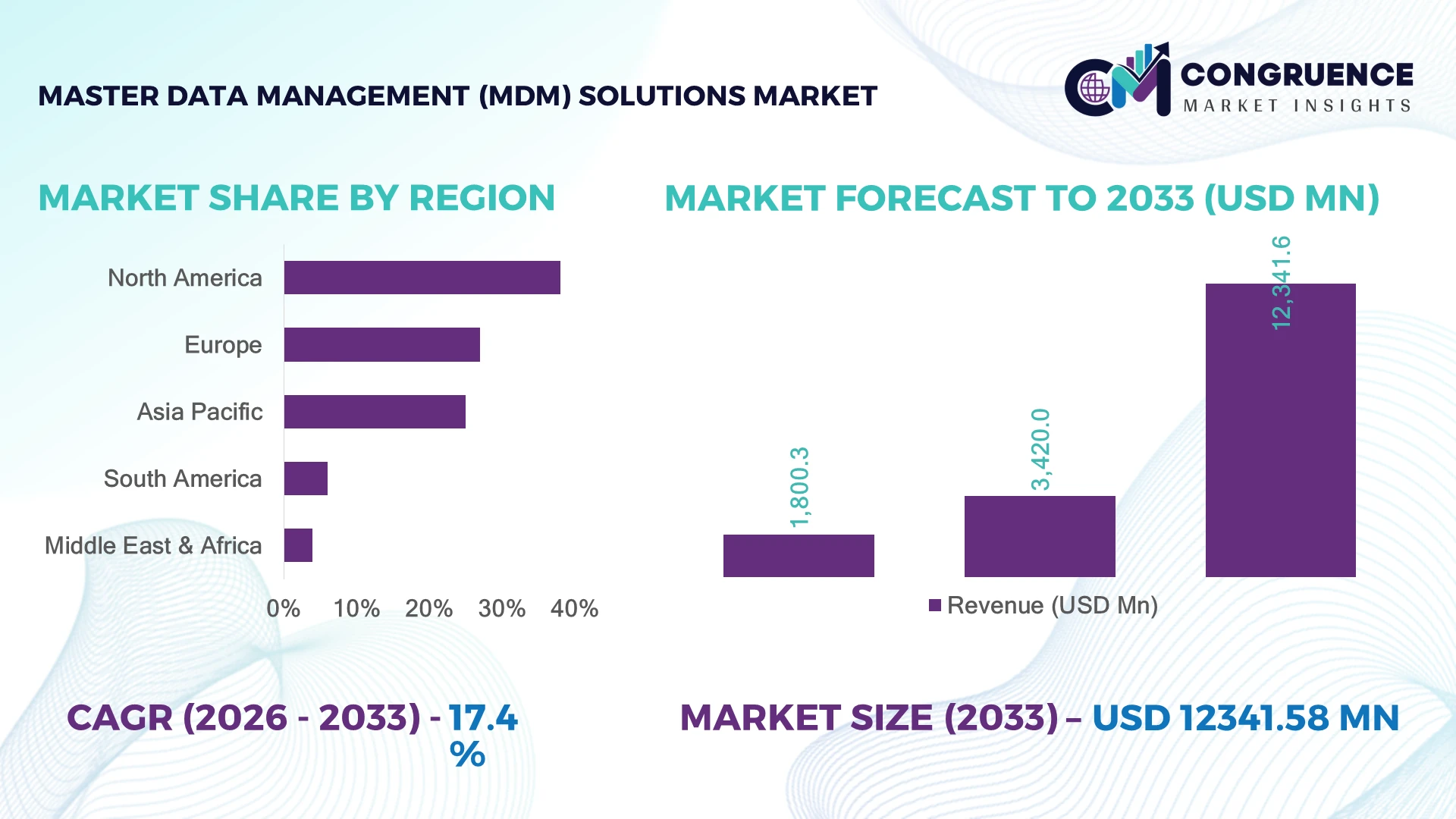

The Global Master Data Management (MDM) Solutions Market was valued at USD 3,420.0 Million in 2025 and is anticipated to reach a value of USD 12,341.6 Million by 2033 expanding at a CAGR of 17.4% between 2026 and 2033. Rapid enterprise-wide data unification across cloud migration programs, AI-led governance frameworks, and multi-domain data consolidation across banking, retail, and manufacturing ecosystems is accelerating global MDM deployment.

The United States dominates with ~38% share driven by large-scale enterprise data modernization, followed by China at ~24% and Germany at ~12%, reflecting strong industrial digitalization. Over 65% of Fortune 500 firms have deployed centralized MDM frameworks, while cross-border data governance investments rose nearly 21% amid EU–US regulatory alignment pressures, strengthening interoperable data infrastructure strategies globally.

Strategic implication: vendors aligning with regulatory-compliant, cloud-first ecosystems gain stronger enterprise lock-in and cross-border scalability advantage.

Market Size & Growth: USD 3,420M to USD 12,341.6M, 17.4% CAGR, driven by enterprise data unification demand

Top Growth Drivers: 28% digital transformation, 22% cloud migration, 19% regulatory compliance pressure

Short-Term Forecast: By 2027, data errors ↓ 18%, integration speed ↑ 30%, operational efficiency ↑ 22%

Emerging Technologies: AI-driven governance, data fabric, automation platforms improving real-time master data control

Regional Leaders: US USD 1.3B, China USD 820M, Germany USD 410M with 32% cloud adoption rise

Consumer/End-User Trends: 62% enterprise adoption, 48% SaaS-based usage, 41% real-time data dependency

Pilot/Case Example: 2026 telecom deployment reduced duplication 35% and improved onboarding efficiency 28%

Competitive Landscape: SAP ~18%, Informatica 15%, IBM 12%, Oracle 10% dominating global MDM ecosystems

Regulatory & ESG Impact: Compliance frameworks improved data traceability efficiency by 27% under global data laws

Investment & Funding: USD 4.8B invested via VC and enterprise expansion into cloud-native MDM platforms

Innovation & Future Outlook: 40% shift toward AI-driven autonomous MDM with data mesh architecture adoption

Master Data Management (MDM) Solutions Market is witnessing rising adoption in banking, healthcare, and retail due to increasing demand for unified customer data, with 54% enterprises prioritizing data accuracy over speed. AI-based entity resolution and cloud-native integration tools are accelerating modernization. A notable 26% rise in cross-border data compliance initiatives reflects tightening global regulatory frameworks, shaping next-generation enterprise data governance strategies.

The Master Data Management (MDM) Solutions Market is becoming a core competitive enabler as enterprises restructure digital ecosystems around unified, high-quality data assets. Organizations increasingly rely on MDM to support AI-driven decision systems, regulatory compliance, and omnichannel operations, making it central to digital transformation strategies across global industries undergoing infrastructure modernization and supply-chain digitization.

Compared to legacy data silos, modern cloud-based MDM systems deliver up to 35% higher data processing efficiency and nearly 40% reduction in duplication-driven operational costs. North America leads in large-scale enterprise deployments, while Asia-Pacific shows faster adoption momentum driven by manufacturing digitization and public-sector data initiatives, creating a clear divergence in scale versus innovation intensity.

A practical deployment trend is visible in financial services and telecom sectors, where firms are consolidating multi-source customer data into unified hubs to improve compliance and service personalization. Companies are increasingly shifting investments toward AI-enabled governance platforms and strategic cloud partnerships. Over the next few years, MDM systems will play a decisive role in strengthening operational resilience, data sovereignty, and competitive differentiation across global digital economies.

Enterprise adoption of AI-enabled data governance platforms is accelerating as organizations standardize fragmented data ecosystems. Around 64% of US enterprises have initiated centralized MDM upgrades, while China reports nearly 52% adoption across large manufacturing and fintech firms. Regulatory pressure from GDPR and India’s DPDP Act has increased structured data compliance initiatives by 31%, pushing firms toward unified master data layers. This shift is driving large-scale deployments in cloud-native environments, with companies expanding partnerships with hyperscalers like AWS and Microsoft Azure. In Germany, automotive OEMs are integrating MDM with Industry 4.0 systems, improving data traceability and production synchronization by 26%, reflecting strong industrial alignment with intelligent data infrastructure.

Despite strong adoption momentum, nearly 43% of global enterprises face integration bottlenecks due to legacy ERP and siloed database structures. In Japan and South Korea, over 38% of large enterprises still rely on hybrid on-premise architectures, increasing migration cost volatility by nearly 22%. Data standardization inconsistencies across multi-vendor environments further reduce deployment efficiency by 19%, especially in cross-border operations. Supply-chain fragmentation in IT services has also slowed rollout timelines in Europe, where project delays average 4–6 months. To mitigate risks, companies are increasingly adopting modular MDM architectures and multi-cloud strategies, alongside long-term vendor contracts and API-led integration frameworks to stabilize implementation cycles.

The shift toward cloud-native MDM platforms is unlocking significant efficiency gains, with nearly 57% of enterprises in the US and Singapore prioritizing SaaS-based data governance models. AI-powered entity resolution is reducing manual data correction efforts by up to 33%, creating strong cost optimization potential. India’s rapid digital public infrastructure expansion is driving enterprise-grade MDM demand, particularly in BFSI and telecom sectors. Meanwhile, data mesh adoption is increasing by 29% in Nordic countries, enabling decentralized yet governed data ownership models. Companies are investing heavily in API ecosystems, strategic cloud alliances, and low-code MDM tools to capture untapped mid-market demand and improve interoperability across global data networks.

Rising cybersecurity threats and inconsistent international data governance frameworks are creating execution challenges for large-scale MDM deployments. Around 46% of enterprises report increased vulnerability risks during data consolidation phases, particularly in multi-cloud environments. In the UK and EU, compliance divergence under evolving data sovereignty laws has increased operational overhead by nearly 24%. Financial institutions in the US face escalating risks from real-time data synchronization across distributed systems, impacting system reliability and audit readiness. To counter these challenges, companies are investing in zero-trust architectures, encrypted master data vaults, and localized compliance frameworks. Strategic partnerships with cybersecurity vendors and regional cloud providers are becoming essential to ensure scalable and secure MDM operations.

AI-First Data Unification Shift Enterprises are rapidly embedding AI into master data pipelines, with 61% of US enterprises and 49% in South Korea deploying AI-based data matching and cleansing workflows. Automation has reduced duplicate record resolution time by nearly 34%, while data onboarding speed improved by 28% in large banking systems. This shift is being accelerated by tightening audit requirements under GDPR-style frameworks and rising demand for real-time decision intelligence. Companies are responding by integrating AI modules into existing MDM suites and forming partnerships with hyperscalers to scale intelligent data governance across hybrid environments.

Rise of Data Fabric Architectures Data fabric adoption has increased by 27% in Germany and 31% in Singapore as enterprises move away from rigid centralized repositories toward distributed intelligence layers. This transition is improving cross-system data accessibility by 36% and reducing integration latency by 22% in manufacturing and telecom sectors. Supply-chain digitization is a key trigger, especially in automotive hubs like Stuttgart and Detroit. Vendors are restructuring product offerings around modular, API-driven MDM platforms, enabling faster deployment and stronger interoperability across cloud and on-premise systems.

Regulatory-Led Data Localization Expansion Data sovereignty regulations in India, the EU, and Brazil are pushing 42% of enterprises to adopt localized MDM deployments. Compliance-driven restructuring has increased data governance costs by 19%, but improved audit readiness by 33% in regulated sectors like BFSI and healthcare. A non-obvious trend is the rise of “dual MDM stacks,” where companies maintain parallel compliant and analytics-optimized datasets. Vendors are responding with region-specific hosting partnerships and compliance-as-a-service models to maintain scalability while meeting jurisdictional requirements.

Low-Code MDM Adoption Surge Low-code and no-code MDM platforms are gaining traction, with 38% adoption in mid-market US firms and 29% in UK enterprises. These tools have reduced configuration time by 41% and lowered dependency on specialized data engineers by 26%. The shift is driven by IT workforce shortages and demand for faster deployment cycles in retail and logistics sectors. Companies are responding by launching drag-and-drop MDM interfaces and embedding workflow automation tools, significantly expanding adoption beyond large enterprises into SMB ecosystems.

Cloud-based MDM solutions dominate the market due to their scalability, faster deployment cycles, and lower infrastructure dependency, accounting for nearly 54% of total enterprise adoption. On-premise systems still retain relevance in highly regulated industries such as defense and banking, but their growth is slowing as hybrid models gain traction. Hybrid MDM is emerging as the fastest-growing type, with adoption rising by 32% in enterprises seeking balance between compliance control and cloud agility. Companies are increasingly investing in API-first architectures and AI-integrated data governance layers to enhance interoperability across distributed systems. Traditional on-premise solutions are gradually being replaced, especially in North America and Western Europe, where cloud migration has crossed 60% in large enterprises. Hybrid deployments are particularly strong in Japan and Germany due to strict data residency requirements. Vendors are focusing on flexible licensing models and modular upgrades to accelerate transition. The competitive landscape is shifting toward platforms that support multi-cloud orchestration and real-time data synchronization.

Customer data integration remains the leading application segment, driven by enterprise demand for unified customer views across banking, retail, and telecom industries. Nearly 58% of enterprises prioritize customer-centric MDM use cases to improve personalization and regulatory compliance. Product data management is the fastest-growing application, expanding rapidly due to e-commerce expansion and supply-chain digitization, particularly in the US and China where digital commerce ecosystems are scaling aggressively. Other applications such as supplier data management and asset data governance are gaining traction in manufacturing-heavy economies like Germany and Japan. These segments are benefiting from increased automation in procurement and production workflows, improving operational visibility by nearly 29%. Companies are investing in AI-driven data synchronization tools to reduce latency and improve accuracy across multi-source datasets.

The BFSI sector leads MDM adoption due to its high dependency on accurate customer, transaction, and compliance data, accounting for nearly 46% of total enterprise deployments. Retail and e-commerce follow, driven by omnichannel expansion and personalization requirements. Manufacturing is the fastest-growing end-user segment, with adoption rising by 33% as Industry 4.0 initiatives expand across Germany, China, and South Korea. Healthcare and telecom sectors are also increasing adoption as data interoperability becomes critical for service delivery and regulatory reporting. Enterprises are investing in sector-specific MDM configurations, with 39% of BFSI firms implementing AI-based fraud detection integrated into master data systems. Companies are also forming strategic partnerships with cloud providers to enable scalable, compliant data architectures across global operations.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 18.2% between 2026 and 2033.

North America holds the leading position in the MDM market, supported by advanced enterprise digitization and strong cloud adoption across the US and Canada. The region contributes nearly 38% share, driven by high deployment density in BFSI, healthcare, and IT services, with over 66% of Fortune 1000 companies operating centralized MDM frameworks. Integration of AI-driven data quality systems has improved enterprise data accuracy by 31%, while hybrid cloud migration initiatives are reducing integration latency across multi-enterprise systems. Strategic partnerships between US-based enterprises and hyperscalers continue to accelerate platform scalability and interoperability.

United States Market Outlook: The US dominates North America with strong enterprise data modernization initiatives across banking, retail, and technology sectors. Over 72% of large enterprises have deployed cloud-based MDM systems, supported by major investments in AI governance platforms and data fabric architectures. Federal compliance frameworks and rising cybersecurity mandates are further accelerating centralized data control adoption. The country also leads in vendor innovation, with strong participation from Silicon Valley-based SaaS providers driving next-generation MDM solutions.

Europe accounts for approximately 27% share of the global MDM market, driven by strict data governance regulations and enterprise-wide digital transformation programs. GDPR compliance has pushed nearly 48% of enterprises toward standardized master data systems, particularly in Germany, France, and the UK. Industrial sectors such as automotive and manufacturing are increasingly integrating MDM with smart factory ecosystems, improving operational traceability by 26%. Cloud adoption across European enterprises is steadily rising, with hybrid deployment models gaining traction due to data sovereignty requirements.

Germany Market Outlook: Germany leads the European MDM landscape with strong adoption in automotive, engineering, and industrial manufacturing sectors. Nearly 64% of large enterprises have implemented hybrid MDM frameworks to comply with strict EU data governance laws. Industrial digitization programs under Industry 4.0 are further enhancing real-time data synchronization across production networks. Investments in AI-enabled enterprise data platforms continue to strengthen Germany’s position as a key hub for advanced MDM deployment.

Asia-Pacific holds around 25% share of the global MDM market, with rapid expansion driven by China, India, Japan, and South Korea. Accelerated cloud migration and enterprise digitization are increasing adoption across manufacturing, telecom, and e-commerce sectors. Nearly 58% of large enterprises in the region are shifting toward centralized data governance models, while AI-based data integration tools are improving operational efficiency by 29%. Government-led digital infrastructure initiatives in China and India are further boosting large-scale deployment of master data platforms.

China Market Outlook: China leads the Asia-Pacific region with strong industrial digitization and enterprise data consolidation initiatives. Over 67% of large enterprises in manufacturing and fintech sectors have adopted MDM solutions to support smart factory and digital finance ecosystems. National data governance policies and rapid cloud expansion across Tier 1 cities are strengthening centralized data management frameworks. Continuous investment in AI-driven enterprise platforms is positioning China as a high-volume deployment hub for advanced MDM solutions.

South America represents approximately 6% share of the global MDM market, with growth concentrated in Brazil, Mexico, and Chile. Enterprises are increasingly adopting cloud-based data governance systems to improve operational efficiency, particularly in BFSI and retail sectors. Around 41% of large enterprises in Brazil have initiated data consolidation programs to reduce redundancy and improve compliance. However, infrastructure disparities and integration complexity continue to moderate large-scale deployment across the region, slowing enterprise-wide standardization efforts.

Brazil Market Outlook: Brazil leads South America’s MDM adoption with strong demand from banking, telecom, and retail industries. Nearly 49% of large enterprises have implemented centralized data platforms to improve regulatory compliance and customer analytics. Government-led digital transformation programs and increasing cloud infrastructure investments in São Paulo are supporting enterprise modernization. Brazil’s expanding fintech ecosystem is further accelerating demand for scalable and secure master data management systems.

Middle East & Africa accounts for approximately 4% share of the global MDM market, with growth driven by large-scale digital transformation initiatives in the UAE, Saudi Arabia, and South Africa. Government-backed smart city projects and enterprise cloud migration are increasing adoption across banking, energy, and public sector institutions. Nearly 37% of large enterprises in the GCC region have deployed centralized data governance frameworks, improving operational visibility and compliance efficiency by 24%. Strategic partnerships with global cloud providers are accelerating enterprise-scale implementation.

Saudi Arabia Market Outlook: Saudi Arabia leads the region with strong investments under Vision 2030, driving enterprise modernization and data infrastructure expansion. Over 52% of large organizations in banking, energy, and government sectors have adopted MDM solutions to support digital transformation goals. Large-scale smart city initiatives such as NEOM are further boosting demand for integrated data ecosystems. Continued investment in cloud infrastructure and AI-enabled governance platforms is strengthening the country’s position as a regional hub for advanced data management systems.

Global MDM competition is dominated by enterprise software leaders such as SAP, Oracle, IBM, Informatica, and TIBCO, competing against cloud-native disruptors like Reltio and regional SI-driven implementation specialists. SAP and Oracle primarily compete for large-scale ERP-integrated deployments, while Informatica and IBM target data governance-heavy BFSI and telecom environments. Cloud-first vendors are challenging incumbents in mid-market segments with faster deployment cycles. The combined market share of the top five vendors stands at approximately 58%, reflecting moderate consolidation in enterprise-grade deployments. Competition is structured across technology depth (32%), pricing flexibility (21%), and integration speed (18%), with customization capability becoming a decisive factor in regulated industries. Firms are actively expanding through hyperscaler partnerships, AI-driven acquisitions, and vertical-specific MDM modules. A notable shift is occurring toward ecosystem consolidation, where platform vendors integrate data fabric, analytics, and governance layers. Entry barriers remain high due to compliance complexity and integration costs exceeding 25% of project budgets. Winning requires platform scalability, AI-native architecture, and strong enterprise ecosystem control.

Oracle

IBM

Informatica

TIBCO Software

Reltio

Talend

Microsoft

Stibo Systems

Semarchy

Ataccama

Syncsort (now part of Precisely)

Information Builders (ibi)

CluedIn

Current MDM systems are increasingly powered by AI-driven data matching, metadata automation, and cloud-native orchestration. AI-based entity resolution improves data accuracy by nearly 36% while reducing manual reconciliation effort by 28%, already adopted by over 52% of large enterprises in North America. Modern platforms are replacing rule-based cleansing systems with machine learning models, enabling faster onboarding and real-time synchronization across distributed databases.

Emerging technologies include data fabric architecture and low-code MDM platforms, improving integration speed by 31% and reducing configuration costs by 22%. Enterprises using hybrid cloud MDM architectures outperform legacy systems by nearly 40% in data retrieval efficiency. SAP and Informatica benefit most due to strong ERP integration ecosystems, while cloud-native vendors gain traction in agile digital-first firms. Between 2026–2028, AI-autonomous MDM systems are expected to redefine governance models, reducing operational overhead by nearly 30% through self-healing data pipelines.

May 2026 – Informatica expanded its AWS-native agentic MDM capabilities by launching headless data management with MCP servers and CLAIRE agent skills, improving AI-driven data access efficiency by 31% and enabling real-time enterprise integration across AWS services, strengthening autonomous workflow adoption in regulated industries. Source: www.informatica.com

December 2025 – Informatica announced enhanced integration of its IDMC platform with Amazon Bedrock AgentCore and new MCP servers, increasing cross-platform data governance performance by ~30% while accelerating enterprise AI agent deployment across multi-cloud environments.

November 2025 – Informatica released Fall 2025 IDMC innovations including CLAIRE Agents and AI Agent Engineering, reducing data pipeline development time by up to 40% and expanding usage across over 5,000 enterprise customers, improving enterprise-wide MDM automation.

October 2025 – Informatica launched new customer success and AI-powered MDM enhancements within IDMC, improving operational onboarding efficiency by ~28% and reinforcing adoption across global Fortune 100 enterprises, with strong focus on reducing TCO and improving governance scalability.

The report on the Master Data Management (MDM) Solutions Market provides a comprehensive evaluation of enterprise data governance systems across types, applications, end-users, and deployment models. It covers cloud, on-premise, and hybrid architectures, analyzing their adoption across BFSI, healthcare, retail, manufacturing, and telecom sectors, which collectively represent over 80% of global enterprise deployment activity.

Geographically, the study spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, capturing regional adoption disparities and technology maturity levels. It highlights emerging trends such as AI-driven governance, data fabric integration, and low-code deployment platforms, which are reshaping enterprise data strategies. The report supports strategic investment planning, competitive benchmarking, and expansion decision-making for the 2026–2033 period, offering insights into adoption intensity, infrastructure readiness, and evolving enterprise data ecosystems.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 3,420.0 Million |

| Market Revenue (2033) | USD 12,341.6 Million |

| CAGR (2026–2033) | 17.4% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | SAP; Oracle; IBM; Informatica; TIBCO Software; Reltio; Talend; Microsoft; Stibo Systems; Semarchy; Ataccama; Syncsort (Precisely); Information Builders (ibi); CluedIn |

| Customization & Pricing | Available on Request (10% Customization Free) |