Reports

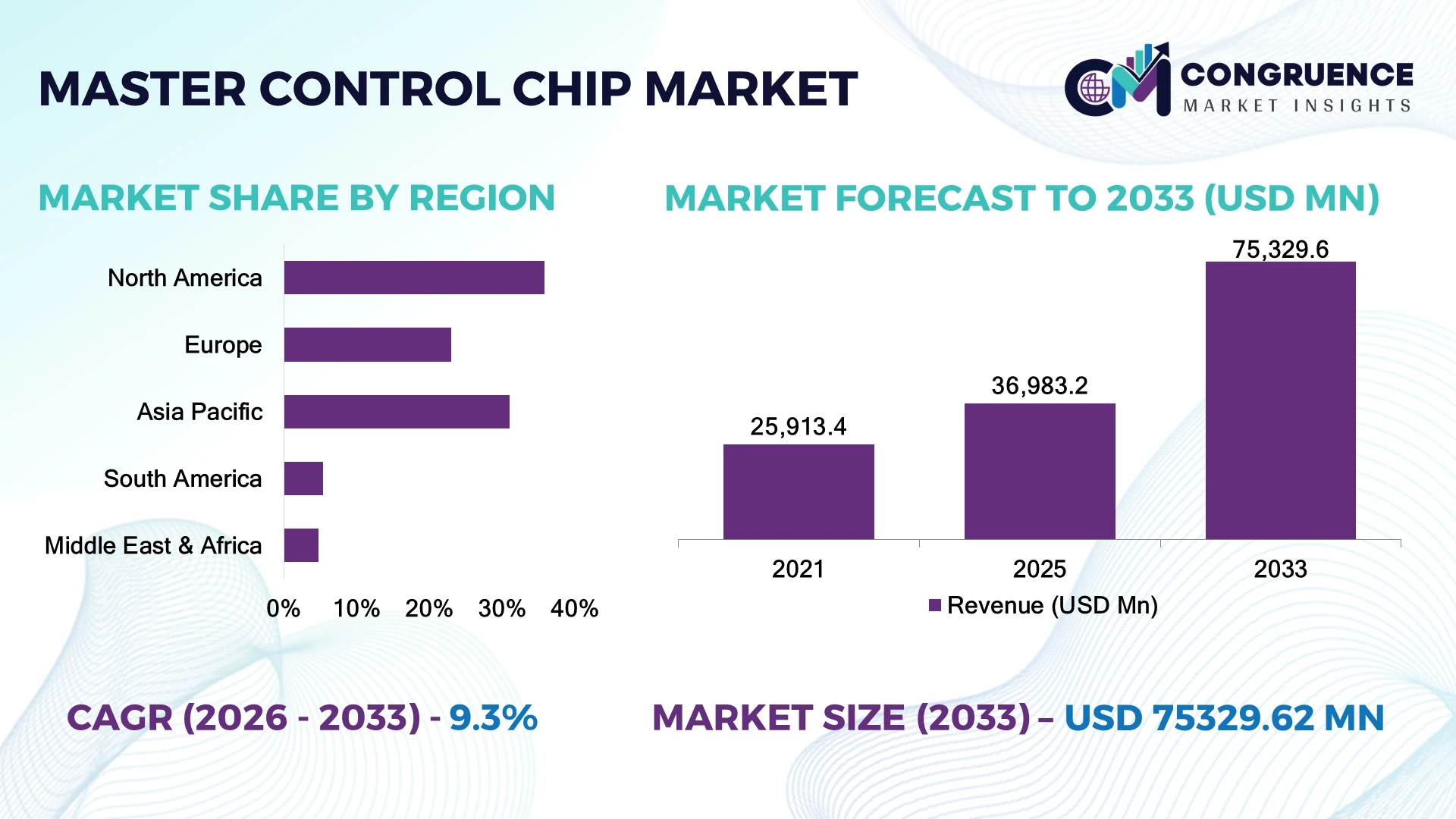

The Global Master Control Chip Market was valued at USD 36,983.2 Million in 2025 and is anticipated to reach a value of USD 75,329.6 Million by 2033 expanding at a CAGR of 9.3% between 2026 and 2033. Growing AI-enabled edge computing, automotive electronics, industrial automation, and high-performance consumer devices are accelerating demand for advanced master control chips with higher processing efficiency and integrated connectivity.

China dominates global master control chip manufacturing with approximately 36% semiconductor packaging and electronics production capacity, supported by multi-billion-dollar investments in domestic chip fabrication and smart manufacturing. In comparison, the United States leads high-performance chip architecture and advanced design, accounting for nearly 48% of global fabless semiconductor R&D activity. Amid ongoing geopolitical semiconductor supply-chain diversification, leading manufacturers continue expanding advanced-node production and backend assembly across multiple countries to strengthen supply resilience.

Strategic investment increasingly favors companies combining advanced chip design capabilities with geographically diversified manufacturing and packaging ecosystems.

Market Size & Growth: USD 36,983.2 million in 2025, projected to reach USD 75,329.6 million by 2033, expanding at a CAGR of 9.3%, driven by AI-enabled computing and advanced semiconductor integration.

Top Growth Drivers: AI processors contribute 31% of demand expansion, automotive electronics 24%, and industrial automation 19%.

Short-Term Forecast: By 2028, chip power efficiency improves by nearly 22% while controller latency declines approximately 18%.

Emerging Technologies: AI accelerators, chiplet architectures, and advanced 3D packaging are improving processing density and thermal performance.

Regional Leaders: North America, Asia-Pacific, and Europe remain the leading markets, supported by advanced semiconductor investments and manufacturing expansion.

Consumer/End-User Trends: Nearly 68% of newly designed intelligent electronic devices integrate advanced multi-function master control chips.

Pilot/Case Example: A 2026 industrial automation deployment improved machine response speed by approximately 27% through AI-enabled controller integration.

Competitive Landscape: Leading semiconductor suppliers collectively account for nearly 55% market participation through advanced processor portfolios and diversified manufacturing.

Regulatory & ESG Impact: Energy-efficient semiconductor initiatives reduce controller power consumption by approximately 16% while supporting sustainability objectives.

Investment & Funding: More than USD 120 billion is being invested globally in semiconductor fabrication, advanced packaging, and strategic manufacturing expansion.

Innovation & Future Outlook: Next-generation heterogeneous integration, edge AI processing, and advanced chip packaging are redefining long-term semiconductor competitiveness.

The Master Control Chip Market is increasingly driven by AI-enabled industrial equipment, smart vehicles, intelligent consumer electronics, and advanced communication infrastructure. Nearly 42% of newly designed embedded systems now integrate AI-capable controllers, while advanced packaging technologies improve thermal performance and computing density. Ongoing semiconductor supply-chain diversification is encouraging manufacturers to regionalize production, creating new strategic opportunities and setting the stage for evolving competitive dynamics.

Master control chips have become strategic assets as industries accelerate intelligent automation, connected devices, and real-time computing. Competition increasingly depends on processing performance, energy efficiency, and secure integration rather than component cost alone. Supply-chain diversification and domestic semiconductor manufacturing programs are reshaping sourcing decisions while reducing dependence on concentrated fabrication hubs.

Advanced SoC architectures integrated with AI acceleration deliver approximately 35% higher processing efficiency than conventional controller designs while reducing power consumption by nearly 20%. North America continues leading high-performance semiconductor design, whereas Asia-Pacific dominates manufacturing scale, packaging capacity, and electronics integration. More than 60% of newly introduced industrial controllers now incorporate embedded AI or advanced connectivity functions, with deployment expected to expand further over the next two to three years.

Industrial automation providers increasingly deploy master control chips supporting predictive maintenance, machine vision, and edge analytics within a single platform, reducing hardware complexity and shortening deployment cycles. Semiconductor manufacturers are expanding advanced-node production, strengthening foundry partnerships, and investing in heterogeneous integration technologies. Companies combining superior architecture, resilient manufacturing networks, and software-enabled ecosystems will secure durable competitive advantages as intelligent electronics become foundational across automotive, industrial, communication, and consumer markets.

Rapid deployment of AI-enabled industrial automation, connected vehicles, and intelligent consumer electronics is significantly increasing demand for high-performance master control chips. Nearly 64% of newly designed industrial embedded systems now integrate multi-core controllers, while AI-enabled edge processors improve real-time computing efficiency by approximately 28%. Automotive electronic control units account for almost 22% of advanced controller demand. Semiconductor localization programs in the United States and Japan are encouraging advanced chip production and packaging investments. This structural shift enables faster product development, higher computing density, and improved supply resilience. Leading chip vendors are expanding advanced-node manufacturing, investing in heterogeneous integration, and forming foundry partnerships to secure production capacity. Companies combining hardware innovation with software ecosystem support are achieving stronger long-term design wins.

Master control chip production remains constrained by advanced wafer fabrication costs, backend packaging limitations, and dependence on specialized manufacturing ecosystems. Approximately 72% of leading-edge semiconductor production remains concentrated within a limited number of fabrication hubs, increasing supply exposure. Advanced packaging expenses have risen nearly 18% over recent years, while qualification cycles frequently extend beyond 12 months for complex industrial applications. Export-control policies affecting semiconductor equipment continue influencing technology access and production planning. These constraints increase inventory costs, delay product launches, and reduce manufacturing flexibility. Chip developers are addressing these pressures through dual-source procurement, regional manufacturing diversification, long-term foundry agreements, and greater investment in mature-node optimization for industrial and automotive applications.

Next-generation edge intelligence creates significant opportunities for master control chip suppliers as AI processing, industrial robotics, and connected infrastructure increasingly require localized computing. More than 58% of new industrial automation platforms are expected to support embedded AI acceleration, while advanced chiplet integration improves computing density by approximately 24%. India and Southeast Asia continue attracting semiconductor assembly and electronics manufacturing investments, creating new downstream demand. Companies are accelerating R&D in low-power AI processors, integrated security modules, and high-speed connectivity architectures while expanding strategic partnerships with OEMs. A notable opportunity lies in combining edge AI with real-time functional safety, enabling single-chip solutions that reduce hardware complexity and lower total system costs across industrial and automotive platforms.

Long-term competitiveness increasingly depends on seamless integration between master control chips, embedded software, cybersecurity frameworks, and application-specific architectures. Nearly 46% of industrial OEMs identify software optimization as a greater deployment challenge than hardware availability, while system validation can consume over 30% of total development schedules. Increasing cybersecurity regulations require secure boot, hardware encryption, and lifecycle protection across connected devices. Failure to achieve software compatibility reduces deployment consistency and delays commercial adoption. Semiconductor companies are strengthening software development kits, investing in developer ecosystems, expanding validation laboratories, and collaborating with industrial automation partners. Future leadership will depend on delivering complete hardware-software platforms rather than standalone semiconductor components.

AI Edge Integration Expands AI-enabled master control chips are becoming standard across industrial automation and intelligent devices, with embedded AI adoption increasing by approximately 34% and edge processing workloads rising nearly 27%. Manufacturers are integrating dedicated neural processing units and expanding software optimization partnerships, enabling faster local decision-making while reducing cloud dependency and operational latency.

Advanced Packaging Gains Momentum Chiplet architectures and 3D advanced packaging are improving computing density by nearly 26% while reducing board space by approximately 18%. Semiconductor companies are restructuring manufacturing around heterogeneous integration and advanced substrate technologies. Continued investment in advanced packaging addresses performance limitations while improving thermal efficiency for automotive and industrial controller applications.

Automotive Controller Consolidation Vehicle manufacturers are replacing multiple distributed electronic controllers with centralized domain architectures, reducing controller count by nearly 30% while improving computing capability by approximately 25%. Semiconductor suppliers are responding through scalable automotive-grade platforms, functional safety certification, and long-term partnerships with automotive OEMs developing software-defined vehicle ecosystems.

Regional Supply Diversification Semiconductor manufacturers are expanding fabrication, testing, and packaging outside traditional production hubs, with nearly 21% of announced manufacturing investments targeting new geographic locations. Industrial policy incentives and supply-chain resilience initiatives continue reshaping production strategies. Companies are strengthening localized manufacturing, strategic inventory planning, and multi-foundry partnerships to improve delivery reliability and reduce geopolitical exposure.

Microcontrollers (MCUs) remain the dominant master control chip segment, accounting for approximately 39% of global demand because of their low power consumption, integrated peripherals, cost efficiency, and broad deployment across consumer electronics, automotive electronics, and industrial control systems. Their scalable architecture and mature software ecosystems allow rapid integration into high-volume embedded applications. Microprocessors (MPUs) continue serving computing-intensive systems, while Digital Signal Processors (DSPs) retain importance for audio, imaging, and communication workloads requiring dedicated signal-processing performance.

FPGA-based master control chips represent the fastest-growing segment as industries demand reconfigurable hardware for AI acceleration, 5G infrastructure, and advanced automotive electronics. FPGA adoption has increased by nearly 21% across new industrial computing platforms, while AI-enabled controllers account for approximately 33% of recent high-performance embedded designs. Semiconductor manufacturers are expanding programmable chip portfolios, strengthening foundry partnerships, and investing in heterogeneous architectures combining MCU, FPGA, and AI accelerators. Investment priorities continue shifting toward flexible computing platforms that balance performance, upgradeability, and long-term deployment efficiency.

A 2025 embedded systems developer survey found that ARM-based microcontrollers remained the most widely deployed embedded processors globally, while FPGA adoption accelerated in industrial automation and edge AI applications requiring hardware reconfigurability.

Consumer electronics remain the leading application, contributing approximately 36% of master control chip demand due to continuous production of smartphones, wearables, smart home devices, and computing equipment. High shipment volumes, rapid product refresh cycles, and increasing device intelligence continue supporting sustained controller demand. Industrial automation maintains stable adoption through robotics, programmable machinery, and factory automation, while healthcare applications increasingly require secure embedded processing for connected diagnostic and monitoring equipment.

Automotive electronics represent the fastest-growing application as electric vehicles, ADAS, and software-defined vehicle architectures require substantially higher semiconductor content. Automotive controller integration has increased by nearly 24% in next-generation vehicle platforms, while industrial automation deployments incorporating AI-enabled controllers have expanded approximately 18%. Semiconductor suppliers are scaling automotive-qualified product portfolios, strengthening OEM partnerships, and expanding functional safety certification. Business demand increasingly favors highly integrated controllers capable of supporting real-time processing, cybersecurity, and high-speed connectivity within a unified semiconductor architecture.

A 2026 enterprise semiconductor adoption assessment reported that automotive and industrial automation represented the fastest-growing embedded processing deployments as manufacturers increased investment in intelligent edge control and software-defined systems.

Manufacturing remains the largest end-user segment, accounting for nearly 29% of market demand because of extensive deployment across factory automation, robotics, CNC machinery, and process control systems. Large-scale industrial infrastructure depends on reliable, low-latency master control chips for continuous production and predictive maintenance. Consumer electronics manufacturers remain significant buyers due to high-volume device production, while IT and telecommunications organizations continue expanding advanced network infrastructure requiring high-performance embedded processing.

Automotive manufacturers represent the fastest-growing end-user group as electrification, intelligent mobility, and centralized vehicle computing accelerate semiconductor integration. Automotive demand for advanced control chips has increased by approximately 26%, while industrial digitalization initiatives have expanded embedded controller deployment by nearly 19%. Semiconductor companies are developing customized automotive platforms, expanding long-term OEM agreements, and strengthening ecosystem partnerships around AI-enabled embedded software. Future competitive advantage increasingly depends on delivering scalable semiconductor platforms tailored to industry-specific operational requirements.

A 2026 enterprise manufacturing technology assessment reported that intelligent factory projects increasingly standardized advanced embedded controllers to support AI-driven automation, machine connectivity, and predictive maintenance across production operations.

North America accounted for the largest market share at 35.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.4% between 2026 and 2033.

Advanced Semiconductor Design Leadership Strengthens Enterprise Adoption

North America remains the largest regional market due to its leadership in semiconductor design, AI computing, cloud infrastructure, and automotive electronics. The region accounts for nearly 36% of global demand, supported by major fabless chip companies, hyperscale data centers, and strong enterprise digitalization. Industrial automation, aerospace, and defense continue deploying advanced master control chips requiring high processing performance and security. During 2025, multiple semiconductor manufacturers expanded advanced packaging and R&D capacity, increasing domestic advanced semiconductor production capability by approximately 15%. Companies are strengthening long-term foundry partnerships, investing in AI-specific controller architectures, and expanding software ecosystems to improve product differentiation and reduce supply-chain dependence.

United States Market Outlook: The United States dominates regional demand through leadership in semiconductor architecture, AI processor development, and advanced electronics manufacturing. More than 48% of global fabless semiconductor research activity originates from U.S.-based companies, supported by significant domestic semiconductor investments and advanced design ecosystems. Major technology firms continue strengthening chip design capabilities, AI accelerator development, and advanced packaging infrastructure to improve long-term semiconductor competitiveness.

Automotive Electronics and Industrial Automation Drive Structural Demand

Europe maintains a strong position through advanced automotive manufacturing, industrial automation, and embedded electronics innovation. The region contributes approximately 23% of global market demand, with increasing deployment of intelligent controllers across smart factories, robotics, and connected mobility solutions. Semiconductor policy initiatives continue encouraging local manufacturing resilience and advanced packaging investment. In 2025, several European semiconductor expansion projects increased regional wafer processing and packaging capability by nearly 12%, strengthening supply security. Manufacturers continue emphasizing automotive-grade chip certification, industrial reliability, and energy-efficient embedded platforms to serve highly regulated industries.

Germany Market Outlook: Germany leads the European market through its globally competitive automotive sector, industrial machinery manufacturing, and Industry 4.0 deployment. Advanced manufacturing facilities continue integrating AI-enabled controllers into robotics, factory automation, and precision engineering systems. Semiconductor suppliers increasingly collaborate with automotive OEMs and industrial equipment manufacturers to develop application-specific master control chip platforms supporting high-reliability industrial operations.

Manufacturing Scale and Electronics Ecosystems Accelerate Expansion

Asia-Pacific is the fastest-growing regional market, supported by its unmatched semiconductor manufacturing ecosystem, electronics exports, and expanding domestic chip demand. The region accounts for approximately 31% of global market activity while hosting leading wafer fabrication, packaging, and electronics assembly operations. Investments in semiconductor fabrication, AI infrastructure, and automotive electronics continue strengthening production capabilities. During 2025, advanced packaging capacity across major manufacturing hubs increased by approximately 20%, improving supply flexibility for high-performance controllers. Companies continue expanding regional fabrication, testing, and OSAT partnerships while strengthening local semiconductor supply chains.

China Market Outlook: China leads the regional market through its extensive electronics manufacturing base, semiconductor packaging capacity, and expanding domestic chip ecosystem. Large investments in semiconductor self-sufficiency continue supporting advanced manufacturing facilities and intelligent electronics production. Domestic manufacturers are increasing controller integration across industrial equipment, consumer electronics, and electric vehicles while expanding collaboration with local foundries and packaging providers.

Industrial Digitalization Creates Emerging Semiconductor Demand

South America continues expanding master control chip adoption through industrial modernization, consumer electronics assembly, and automotive manufacturing investments. Brazil and neighboring economies are increasing deployment of embedded controllers across manufacturing, energy, and transportation infrastructure. Although semiconductor fabrication remains limited, growing electronics production continues supporting controller demand. Industrial automation projects implemented during 2025 increased embedded controller deployment by approximately 14% within selected manufacturing sectors. Global semiconductor companies are responding through stronger regional distribution networks, localized technical support, and strategic partnerships with electronics manufacturers to improve market penetration.

Brazil Market Outlook: Brazil remains the region's largest semiconductor consumption market because of its automotive manufacturing base, industrial automation initiatives, and expanding electronics assembly sector. Increasing investment in digital manufacturing and connected industrial infrastructure continues driving demand for embedded processing platforms. Technology suppliers are strengthening engineering support, distribution partnerships, and localized product customization for industrial and automotive customers.

Digital Infrastructure Investment Expands Embedded Intelligence

The Middle East & Africa market is advancing through investments in smart infrastructure, industrial digitalization, telecommunications, and intelligent energy systems. Demand for master control chips is increasing across data centers, utilities, industrial automation, and connected public infrastructure. Government-led digital transformation initiatives continue supporting deployment of advanced embedded systems throughout the region. In 2025, multiple smart infrastructure projects increased demand for intelligent controllers by approximately 16% across transportation and utility applications. Semiconductor vendors continue expanding regional technology partnerships, engineering services, and distribution capabilities to support long-term deployment growth.

Saudi Arabia Market Outlook: Saudi Arabia represents the region's most strategic market because of large-scale smart city initiatives, industrial diversification programs, and advanced digital infrastructure investment. Expanding automation across energy, manufacturing, and transportation sectors is accelerating adoption of intelligent control platforms. Technology providers continue partnering with industrial enterprises and government programs to deploy secure, high-performance embedded semiconductor solutions supporting long-term digital transformation objectives.

The Master Control Chip Market is led by NVIDIA, Qualcomm, MediaTek, Intel, AMD, NXP Semiconductors, Renesas Electronics, and Texas Instruments, with global semiconductor leaders competing against specialized embedded controller suppliers, while fabless innovators challenge integrated device manufacturers through faster architecture development. The top five participants collectively control approximately 56% of global market activity. Competition centers on computing performance, AI acceleration, power efficiency, software compatibility, and supply-chain resilience, with advanced node migration improving performance by nearly 30% while reducing energy consumption by around 22%. Companies are strengthening competitive positions through foundry partnerships, advanced packaging, custom silicon development, vertical integration, and AI ecosystem expansion. The competitive shift increasingly favors heterogeneous computing, chiplet architectures, and software-defined platforms over standalone processor performance. High development costs, advanced process-node access, and long design qualification cycles remain major entry barriers. Winning requires sustained R&D leadership, scalable manufacturing partnerships, robust software ecosystems, and application-specific chip optimization across automotive, industrial, AI, and edge computing markets.

NVIDIA Corporation

Qualcomm Incorporated

Intel Corporation

Advanced Micro Devices (AMD)

MediaTek Inc.

NXP Semiconductors

Renesas Electronics Corporation

Texas Instruments Incorporated

STMicroelectronics N.V.

Infineon Technologies AG

Broadcom Inc.

Microchip Technology Inc.

Synaptics Incorporated

UNISOC

Master control chip technology is rapidly evolving toward heterogeneous computing architectures integrating CPUs, GPUs, NPUs, DSPs, and dedicated security engines on a single package. AI-enabled controllers improve edge inference efficiency by approximately 28% while reducing latency by nearly 20% compared with conventional multicore processors. More than 58% of newly designed high-performance controllers now incorporate dedicated AI acceleration or neural processing capabilities. Automotive, industrial automation, networking, and edge computing manufacturers benefit through faster decision-making, lower energy consumption, and improved system responsiveness.

Chiplet architectures, 3D packaging, advanced FinFET nodes, embedded MRAM, and high-bandwidth interconnects are replacing monolithic chip designs. Compared with legacy architectures, advanced chiplet-based controllers deliver nearly 35% higher computing performance while lowering package development costs by approximately 18%. Around 46% of enterprise semiconductor development programs now evaluate chiplet integration to improve scalability and shorten product development cycles. Companies investing in advanced packaging and AI software ecosystems gain competitive advantages through faster customization and reduced product qualification timelines.

Between 2026 and 2028, AI-native controller platforms, software-defined hardware, RISC-V expansion, silicon photonics integration, and advanced edge processing will redefine semiconductor competitiveness. Manufacturers capable of combining leading-edge process technologies, secure architectures, software optimization, and flexible heterogeneous computing platforms will strengthen long-term leadership across automotive electronics, industrial automation, communications infrastructure, and intelligent computing applications.

November 2024: NXP Semiconductors introduced the i.MX 94 applications processor family integrating a built-in TSN switch and post-quantum cryptography, improving industrial edge connectivity and enabling safer real-time control applications. Source: NXP

March 2025: NXP Semiconductors launched the S32K5 automotive microcontroller family built on 16nm FinFET technology with embedded MRAM, enabling higher processing performance and supporting ECU consolidation for software-defined vehicles. Source: NXP

May 2025: NVIDIA unveiled NVLink Fusion, allowing partners including MediaTek, Marvell, Fujitsu, and Qualcomm to integrate custom CPUs with NVIDIA AI infrastructure, expanding scalable heterogeneous computing for enterprise AI deployments. Source: Nvidia

May 2025: Qualcomm announced its return to the data center processor market with custom CPUs designed to interoperate with NVIDIA GPUs, strengthening high-performance AI infrastructure capabilities. Source: Reuters

The report provides comprehensive analysis of the global Master Control Chip Market across processor architectures, integration levels, computing platforms, applications, end-user industries, and major geographic markets. It evaluates adoption across automotive electronics, consumer devices, industrial automation, networking equipment, AI infrastructure, communications systems, and intelligent edge computing. The assessment covers advanced semiconductor technologies including AI accelerators, chiplet architectures, heterogeneous computing, advanced packaging, embedded security, and high-performance interconnects. More than 25 application scenarios and multiple deployment models are evaluated to identify evolving demand patterns and technology priorities.

The study delivers detailed competitive benchmarking, regional manufacturing analysis, technology roadmaps, and strategic market positioning between 2026 and 2033. It highlights deployment trends, enterprise adoption patterns, semiconductor ecosystem developments, and innovation priorities supporting investment planning, product strategy, manufacturing expansion, supply-chain optimization, and long-term competitive positioning across mature semiconductor markets and emerging intelligent computing applications.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 36,983.2 Million |

|

Market Revenue in 2033 |

USD 75,329.6 Million |

|

CAGR (2026 - 2033) |

9.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

NVIDIA Corporation, Qualcomm Incorporated, Intel Corporation, Advanced Micro Devices (AMD), MediaTek Inc., NXP Semiconductors, Renesas Electronics Corporation, Texas Instruments Incorporated, STMicroelectronics N.V., Infineon Technologies AG, Broadcom Inc., Microchip Technology Inc., Synaptics Incorporated, UNISOC |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |