Reports

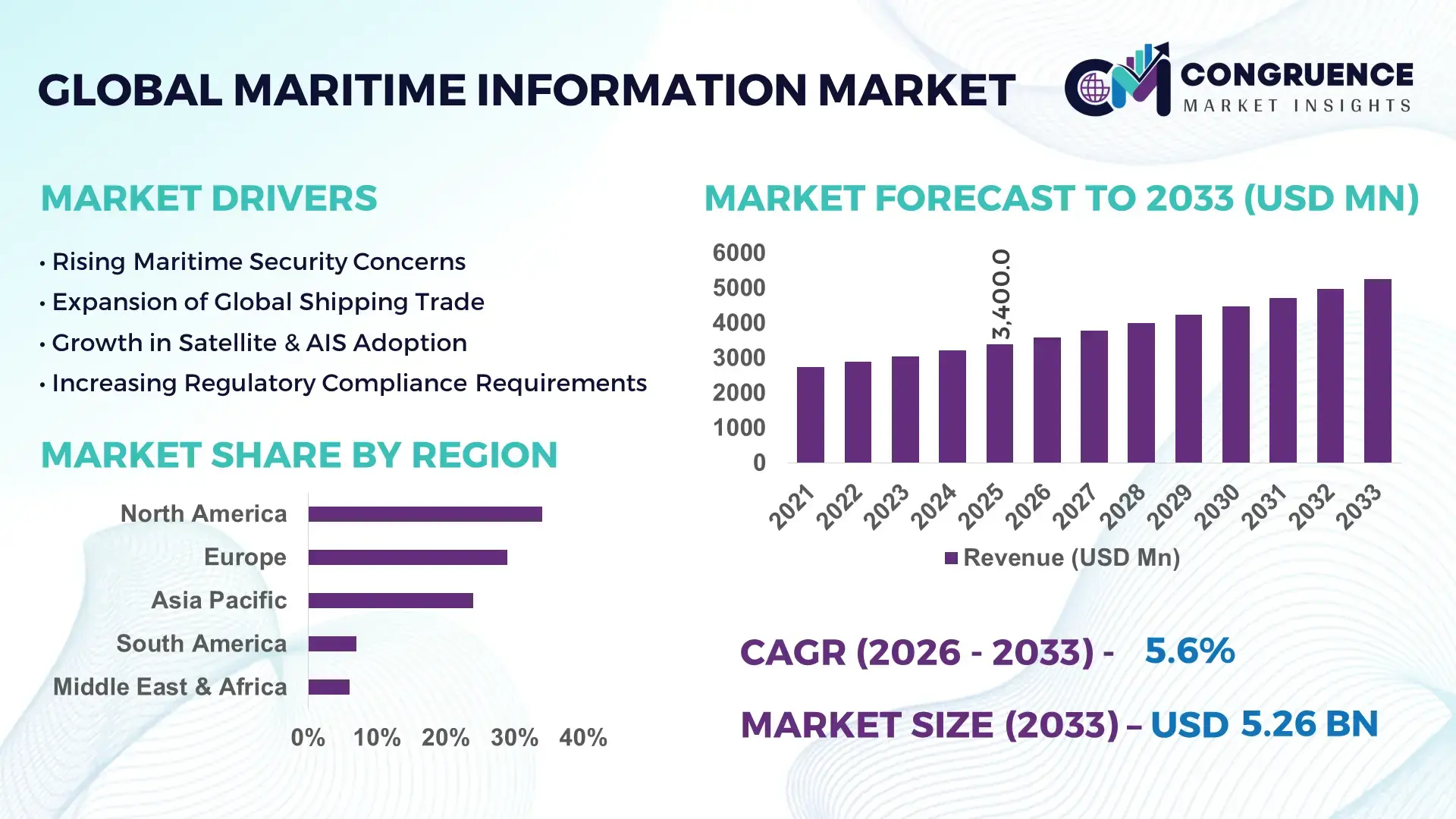

The Global Maritime Information Market was valued at USD 3,400.0 Million in 2025 and is anticipated to reach a value of USD 5,257.6 Million by 2033 expanding at a CAGR of 5.6% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is primarily driven by increasing digitization of fleet operations, mandatory maritime safety compliance frameworks, and expanding use of AI-based vessel tracking and predictive analytics platforms across global shipping networks.

The United States remains the dominant country in the Maritime Information Market, supported by its extensive commercial fleet operations and advanced maritime digital infrastructure. The U.S. manages over 25,000 vessels engaged in domestic and international trade, while more than 80% of major ports have integrated advanced AIS-based traffic management systems. Investments exceeding USD 1 billion in smart port modernization initiatives between 2022 and 2025 have accelerated adoption of satellite-enabled maritime analytics and cybersecurity platforms. Key industry applications include defense maritime intelligence, offshore energy logistics, and port optimization systems. Over 65% of U.S.-based shipping operators deploy predictive route optimization software, while maritime data integration across logistics networks has improved cargo visibility by over 30% in large-scale commercial operations.

Market Size & Growth: Valued at USD 3,400.0 Million in 2025, projected to reach USD 5,257.6 Million by 2033, expanding at 5.6% CAGR, driven by fleet digitization and regulatory compliance mandates.

Top Growth Drivers: AIS adoption at 78%, satellite-based monitoring penetration at 64%, predictive analytics integration improving efficiency by 28%.

Short-Term Forecast: By 2028, AI-driven route optimization is expected to reduce fuel consumption by 15% and cut vessel downtime by 12%.

Emerging Technologies: AI-powered maritime analytics, satellite IoT integration, blockchain-based cargo documentation systems.

Regional Leaders: North America projected above USD 1,900 Million by 2033 with strong defense applications; Europe exceeding USD 1,600 Million with smart port initiatives; Asia-Pacific surpassing USD 1,400 Million driven by large commercial fleets.

Consumer/End-User Trends: Over 60% of fleet operators prioritize real-time data integration; 48% deploy cloud-based maritime intelligence dashboards.

Pilot or Case Example: In 2024, a major Asian port implemented AI vessel scheduling, reducing turnaround time by 18%.

Competitive Landscape: Market leader holds approximately 22% share, followed by four major competitors maintaining strong global maritime analytics portfolios.

Regulatory & ESG Impact: IMO carbon intensity regulations encouraging 20% emission reduction targets by 2030 are accelerating digital monitoring adoption.

Investment & Funding Patterns: Over USD 2.5 Billion invested globally in smart port and maritime AI infrastructure projects between 2022–2025.

Innovation & Future Outlook: Integration of AI, satellite analytics, and predictive compliance monitoring is positioning maritime information platforms as critical digital infrastructure.

Commercial shipping accounts for approximately 45% of industry demand, followed by naval defense at 28% and offshore energy at 17%. AI-driven navigation systems and satellite-enabled IoT monitoring platforms are reshaping operational intelligence. Environmental compliance frameworks and carbon tracking mandates are accelerating adoption in Europe and North America, while Asia-Pacific demonstrates strong consumption growth through fleet expansion and port digitization initiatives, reinforcing long-term modernization strategies.

The Maritime Information Market holds strategic importance as global trade relies on over 80% of goods transported by sea. Maritime intelligence platforms enhance situational awareness, optimize fleet utilization, and ensure compliance with international maritime regulations. Advanced AI-driven predictive maintenance delivers 25% improvement in equipment reliability compared to traditional manual inspection systems. North America dominates in volume of maritime data deployments, while Europe leads in adoption with over 70% of major ports implementing digital traffic management platforms.

By 2028, AI-powered predictive routing systems are expected to improve fuel efficiency by 15%, directly supporting decarbonization goals. Firms are committing to ESG metrics including 20% carbon intensity reduction by 2030 through integrated emission tracking dashboards. In 2024, a Scandinavian shipping company achieved a 17% reduction in fuel consumption through AI-assisted voyage optimization technology, demonstrating measurable operational gains.

Satellite-enabled real-time vessel monitoring, blockchain-based documentation, and digital twin port modeling represent forward-looking pathways. Strategic investments in maritime cybersecurity frameworks are increasing by 30% annually as data protection becomes critical. As trade volumes expand and environmental compliance intensifies, the Maritime Information Market is positioned as a pillar of operational resilience, regulatory compliance, and sustainable maritime growth.

The Maritime Information Market is evolving under the influence of rapid digitization, global trade expansion, regulatory tightening, and integration of AI-driven analytics. Over 90% of internationally traded goods move through maritime routes, creating substantial demand for real-time vessel tracking and cargo intelligence systems. Increasing satellite coverage has improved maritime data transmission reliability by nearly 40% over the past five years. The adoption of automated identification systems across commercial fleets exceeds 75%, reflecting strong compliance alignment. Furthermore, port congestion management platforms have reduced vessel turnaround times by up to 20% in major global hubs. Defense modernization programs and offshore energy exploration activities are also increasing reliance on maritime surveillance technologies. However, cybersecurity risks, integration complexity, and high infrastructure deployment costs continue to influence investment strategies across emerging economies.

The digital transformation of shipping operations is a primary driver for the Maritime Information Market. Over 70% of large commercial fleets now utilize integrated maritime data platforms for navigation, compliance monitoring, and cargo tracking. Real-time vessel monitoring reduces operational uncertainty and enhances decision-making accuracy by approximately 30%. Automated port management systems have improved berth allocation efficiency by 18% in high-traffic ports. Additionally, the integration of AI-driven predictive maintenance reduces unexpected breakdowns by nearly 25%, ensuring higher fleet availability. Satellite-based AIS coverage has expanded global maritime visibility to above 95% of major shipping lanes. Regulatory frameworks mandating electronic documentation and emission reporting further accelerate system deployment, particularly in developed economies where compliance audits are increasingly data-driven.

Cybersecurity threats remain a significant restraint, with maritime cyber incidents increasing by nearly 35% over recent years. Ports and shipping companies face risks related to ransomware attacks and GPS spoofing, which can disrupt navigation systems. Integration complexity between legacy shipboard equipment and modern cloud-based platforms increases deployment timelines by up to 20%. Smaller fleet operators often struggle with interoperability standards and data harmonization requirements. Furthermore, initial system integration and staff training may require operational adjustments lasting 6–12 months. Concerns over data sovereignty and cross-border information sharing regulations also limit seamless global implementation, especially across multi-jurisdictional trade corridors.

AI-driven predictive analytics offers transformative opportunities in fuel optimization, route planning, and maintenance forecasting. Predictive route optimization can lower fuel consumption by 15%, significantly reducing operational costs and emissions. Digital twin technology adoption is expanding across 40% of newly modernized smart ports, enabling simulation-based infrastructure planning. Autonomous vessel trials have increased by 22% globally, supported by integrated maritime intelligence platforms. Furthermore, offshore wind installations require continuous maritime monitoring systems, expanding demand within renewable energy logistics. Real-time cargo visibility solutions improve supply chain transparency by 30%, enhancing customer trust and operational efficiency. Growing satellite bandwidth availability and cloud computing advancements are further enabling scalable deployment across mid-sized fleets.

Infrastructure investment requirements for maritime information systems can exceed multi-million-dollar budgets for large port installations. Approximately 45% of developing region ports lack advanced digital infrastructure, slowing adoption rates. Regulatory fragmentation across international maritime zones creates compliance complexity, requiring customized software configurations. Frequent updates to emission reporting standards increase operational adaptation costs. Skilled workforce shortages in maritime cybersecurity and AI analytics limit implementation capacity, with talent gaps estimated at 20% across specialized maritime IT roles. Additionally, integration of satellite data streams with terrestrial systems demands robust network reliability, which may be inconsistent in remote oceanic routes.

Expansion of AI-Based Route Optimization Platforms: Over 68% of global shipping operators are piloting AI-driven route optimization systems. These solutions have demonstrated fuel savings of 12–18% per voyage and reduced weather-related delays by 20%. AI-enabled navigation assistance is increasingly integrated with satellite AIS data, improving predictive accuracy by 30% compared to traditional routing software.

Growth in Smart Port Digitalization: More than 55% of Tier-1 global ports have deployed smart traffic management and automated docking systems. Digital berth scheduling has reduced vessel turnaround time by 15%, while automated cargo tracking platforms improved container traceability accuracy to 96%. Asia-Pacific leads with over 40 major ports integrating IoT-enabled monitoring systems.

Rising Maritime Cybersecurity Investments: Maritime cybersecurity spending has increased by approximately 30% over the past three years. Over 60% of large fleet operators have implemented multi-layered network security frameworks. Advanced threat detection systems reduce incident response time by 35%, safeguarding navigation and communication channels.

Integration of Satellite IoT and Emission Monitoring: Satellite IoT adoption in maritime operations exceeds 65% among large operators. Real-time emission tracking systems support 20% carbon intensity reduction targets by 2030. Digital emission dashboards improve reporting efficiency by 25%, ensuring regulatory compliance across international waters.

The Maritime Information Market is segmented by type, application, and end-user, reflecting diverse operational requirements across global shipping ecosystems. By type, software platforms dominate due to real-time analytics and compliance capabilities, while satellite communication modules and onboard hardware systems maintain strong complementary roles. Applications span fleet management, port operations, maritime surveillance, and offshore energy logistics. Fleet management solutions account for the largest adoption due to their impact on fuel optimization and cargo visibility. End-users include commercial shipping companies, naval defense authorities, port operators, and offshore energy firms. Commercial operators lead in system adoption owing to large fleet sizes and regulatory reporting mandates. Increasing integration of AI analytics and IoT-based maritime sensors continues to redefine segmentation patterns, supporting both operational efficiency and compliance management objectives.

Software platforms account for approximately 48% of total adoption, driven by real-time vessel tracking, predictive analytics, and regulatory reporting capabilities. Satellite communication systems hold nearly 32% share, supporting offshore connectivity and remote monitoring. However, AI-integrated analytics modules represent the fastest-growing segment, expanding at an estimated 8.5% CAGR due to advanced route optimization and predictive maintenance capabilities. Hardware components, including onboard sensors and AIS transponders, collectively contribute about 20%, maintaining niche importance in compliance and surveillance applications.

Fleet management represents approximately 42% of application deployment, driven by fuel optimization and voyage efficiency tools. Port management systems account for 28%, improving berth allocation and cargo handling accuracy. Maritime surveillance applications contribute 18%, particularly in defense and border security operations. Offshore energy logistics and environmental monitoring collectively hold 12%. However, digital port automation is the fastest-growing application area, expanding at around 7.8% CAGR due to global smart port initiatives. In 2025, more than 40% of global shipping enterprises reported piloting integrated maritime analytics for cargo visibility. Over 65% of large ports deploy automated traffic control dashboards for operational monitoring.

Commercial shipping companies account for approximately 45% of total system adoption due to fleet optimization and compliance needs. Naval defense agencies contribute 27%, utilizing maritime intelligence for surveillance and security operations. Port authorities represent 18%, focusing on traffic and cargo management systems. Offshore energy firms and research institutions together account for 10%. However, offshore renewable energy operators are the fastest-growing end-user group, expanding at approximately 8.2% CAGR as offshore wind installations increase globally. In 2025, over 60% of large maritime enterprises integrated AI-based decision dashboards into daily operations. Nearly 35% of mid-sized shipping firms adopted cloud-based compliance reporting platforms to streamline regulatory audits.

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.4% between 2026 and 2033.

North America’s leadership is supported by over 25,000 active commercial vessels and more than 80% smart port integration across major coastal hubs. Europe held approximately 29% share in 2025, driven by strict emission monitoring mandates and digital maritime compliance frameworks adopted by over 70% of large port authorities. Asia-Pacific represented nearly 24% of global demand, supported by China, Japan, and India collectively managing more than 40% of global container throughput volume. South America contributed 7%, with Brazil handling over 60% of the region’s maritime cargo activity. The Middle East & Africa accounted for 6%, supported by oil & gas shipping corridors and strategic trade routes handling nearly 12% of global seaborne petroleum flows. Regional digitization intensity varies significantly, with developed economies reporting 65%–75% adoption of AI-based maritime analytics platforms compared to 35%–45% in emerging markets.

North America holds approximately 34% of the Maritime Information Market share in 2025, supported by extensive commercial shipping, naval defense modernization, and smart port investments. The region manages over 2 billion metric tons of maritime freight annually, with more than 80% of major ports deploying automated vessel traffic systems. Key industries driving demand include commercial shipping, offshore energy logistics in the Gulf region, and naval surveillance programs. Regulatory frameworks such as mandatory electronic logging and emission reporting standards have increased digital compliance adoption by 25% since 2022. AI-powered route optimization systems reduce fuel usage by 15% across large fleets. A leading regional player, Spire Global, has expanded satellite AIS constellation capacity by over 20% in 2024, strengthening maritime domain awareness. Enterprise adoption patterns show higher uptake among defense and offshore operators, with nearly 70% of large maritime enterprises integrating cloud-based intelligence dashboards.

Europe accounts for approximately 29% of the Maritime Information Market share in 2025, driven by advanced maritime trade networks across Germany, the UK, France, and the Netherlands. The region operates over 1,200 commercial ports, with more than 70% implementing digital emission monitoring systems aligned with carbon reduction targets. Regulatory pressure under maritime decarbonization frameworks has accelerated adoption of fuel tracking software by nearly 30% since 2023. AI-assisted vessel scheduling platforms have improved berth efficiency by 18% in leading ports such as Rotterdam and Hamburg. Saab AB has expanded its maritime surveillance and traffic management systems across multiple European coastal authorities, strengthening maritime safety infrastructure. Enterprise buyers in the region prioritize explainable analytics and ESG-aligned compliance tools, with over 60% of shipping operators deploying carbon monitoring dashboards.

Asia-Pacific represents approximately 24% of the Maritime Information Market volume in 2025 and ranks as the fastest-growing regional segment. China, Japan, and India collectively handle more than 40% of global container traffic throughput. Infrastructure modernization initiatives have resulted in over 45 major smart ports integrating IoT-based vessel monitoring platforms. Regional manufacturing and export activities have increased maritime data traffic by nearly 35% over the past three years. Japan’s adoption of autonomous vessel trials has expanded by 22%, supporting digital navigation systems. China’s major port operators have integrated AI-powered cargo scheduling platforms reducing turnaround time by 15%. Consumer behavior in the region reflects strong adoption among logistics conglomerates and e-commerce-linked shipping networks, with more than 50% of new fleet acquisitions incorporating digital tracking modules.

South America contributes approximately 7% of global Maritime Information Market demand, with Brazil and Argentina serving as primary maritime trade hubs. Brazil accounts for over 60% of regional container throughput, supported by agricultural exports and offshore energy shipments. Digital port modernization projects have increased adoption of automated traffic management systems by 20% since 2023. Government-backed trade facilitation programs have accelerated electronic documentation implementation across 55% of major terminals. Offshore oil exploration activities in Brazil drive demand for satellite-based vessel tracking systems. Regional adoption patterns are closely linked to commodity exports and multilingual logistics coordination, with nearly 40% of large exporters deploying integrated maritime visibility platforms.

The Middle East & Africa accounts for approximately 6% of the Maritime Information Market in 2025, driven primarily by oil & gas shipping corridors and international trade transit routes. The UAE and Saudi Arabia collectively manage more than 15% of global crude oil maritime exports. Smart port investments in the Gulf region have expanded by 25% between 2022 and 2025. South Africa’s major ports have introduced AI-enabled cargo scheduling platforms improving operational throughput by 12%. Regional trade partnerships have encouraged digitized customs documentation adoption across 50% of high-volume terminals. Enterprise demand is strongest among energy logistics operators, with over 55% integrating emission tracking and vessel monitoring dashboards to meet international compliance standards.

United States – 31% Market Share: Strong maritime defense infrastructure, over 80% smart port integration, and high enterprise-level AI deployment in commercial shipping.

China – 22% Market Share: Controls more than 30% of global container throughput and rapidly expanding smart port and AI-based maritime logistics platforms.

The Maritime Information Market demonstrates a moderately fragmented structure with over 120 active competitors globally. The top five companies collectively hold approximately 48% of total market share, reflecting strong but competitive consolidation. Strategic initiatives include satellite constellation expansion, AI-based analytics launches, and maritime cybersecurity partnerships. Over 35% of competitive differentiation is technology-driven, particularly in predictive analytics and satellite AIS enhancements. Partnerships between maritime data providers and port authorities have increased by 28% since 2023. Mergers and acquisitions activity has grown steadily, with at least 12 notable strategic acquisitions recorded between 2023 and 2025 to enhance data integration capabilities. Product innovation cycles have shortened to 12–18 months as firms prioritize real-time analytics and emission tracking features. Competition intensity is highest in North America and Europe, while Asia-Pacific remains a strong expansion target for multinational maritime intelligence providers.

ORBCOMM

exactEarth

Kongsberg Gruppen

Wärtsilä Corporation

Thales Group

L3Harris Technologies

Leonardo S.p.A.

Hexagon AB

MarineTraffic

FleetMon

HawkEye 360

The Maritime Information Market is undergoing rapid technological transformation driven by AI, satellite IoT, big data analytics, and cloud computing integration. Satellite AIS coverage now exceeds 95% of major global shipping lanes, enabling near real-time vessel tracking accuracy within 5–10 meters. AI-driven predictive maintenance systems reduce unexpected engine failure incidents by approximately 25%, enhancing fleet reliability. Digital twin port modeling platforms are deployed in over 40 advanced ports globally, simulating berth allocation and cargo flows to improve efficiency by 15%–20%.

Blockchain-based electronic bill of lading systems have reduced documentation processing time by nearly 50%, minimizing administrative bottlenecks. Maritime cybersecurity platforms incorporating anomaly detection algorithms shorten incident response time by 35%. Integration of 5G coastal communication networks supports low-latency maritime data exchange, improving vessel-to-port coordination by 18%. Autonomous vessel pilot programs have expanded by 22% globally, with AI navigation systems demonstrating 30% higher situational prediction accuracy compared to legacy radar-only systems.

Cloud-native maritime dashboards are now adopted by over 60% of large shipping enterprises, enabling centralized compliance reporting and performance analytics. Edge computing devices installed onboard vessels process over 40% of operational data locally before satellite transmission, optimizing bandwidth usage. The convergence of satellite analytics, AI, and IoT sensors is positioning maritime intelligence systems as core digital infrastructure for modern global trade operations.

• In November 2025, S&P Global announced the successful completion of its acquisition of ORBCOMM’s Automatic Identification System (AIS) business, integrating ORBCOMM’s satellite-based vessel tracking services into the S&P Global Market Intelligence division to strengthen maritime analytics and global trade intelligence offerings. This marks a strategic expansion of S&P Global’s maritime data capabilities and reinforces its position in maritime supply chain decision support. Source: www.prnewswire.com

• In December 2024, Windward secured long-term AIS data feeds through 2030 via a new data-sharing agreement with S&P Global Market Intelligence, significantly enhancing Windward’s access to one of the largest terrestrial AIS networks. This ensures uninterrupted high-quality vessel tracking data for Windward’s AI-based maritime intelligence platform. Source: www.windward.ai

• In early January 2026, Windward published a corporate blog outlining its 2026 commitment to verified maritime intelligence, highlighting enhanced GNSS spoofing mitigation solutions and a dedicated 60-plus expert DataOps team that reduces the impact of signal manipulation on vessel profiles and ownership data. Source: www.windward.ai

• In April 2025, S&P Global agreed to acquire ORBCOMM’s AIS data services business and take a strategic equity position, creating a long-term alliance to develop differentiated supply chain and maritime data insights. This move underlines broader growth strategies focused on integrated maritime analytics and logistics intelligence.

The Maritime Information Market Report provides a comprehensive evaluation of global maritime data platforms, satellite-based monitoring systems, AI-driven analytics software, and integrated compliance management solutions. The scope covers segmentation across software platforms, satellite communication modules, onboard hardware systems, and AI-enhanced predictive analytics tools. Applications analyzed include fleet management, port traffic optimization, maritime surveillance, offshore energy logistics, and environmental compliance monitoring.

Geographically, the report evaluates five major regions—North America, Europe, Asia-Pacific, South America, and the Middle East & Africa—covering more than 40 key maritime trade countries. It assesses over 120 active market participants and evaluates strategic initiatives such as partnerships, satellite expansions, and smart port digitization programs. The report further examines technology integration trends including blockchain documentation systems, digital twin port modeling, AI-based anomaly detection, and cloud-native maritime dashboards.

Industry focus areas include commercial shipping operators managing over 80% of global trade flows, naval defense authorities overseeing coastal surveillance, offshore renewable energy logistics networks, and port authorities implementing automated vessel traffic systems. Emerging segments such as autonomous vessel trials, emission tracking analytics, and maritime cybersecurity frameworks are also assessed to provide forward-looking industry insight. The scope ensures coverage of operational, technological, regulatory, and strategic factors shaping long-term market evolution for decision-makers and institutional stakeholders.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 3,400.0 Million |

| Market Revenue (2033) | USD 5,257.6 Million |

| CAGR (2026–2033) | 5.6% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Spire Global; Saab AB; Windward; ORBCOMM; exactEarth; Kongsberg Gruppen; Wärtsilä Corporation; Thales Group; L3Harris Technologies; Leonardo S.p.A.; Hexagon AB; MarineTraffic; FleetMon; HawkEye 360 |

| Customization & Pricing | Available on Request (10% Customization Free) |