Reports

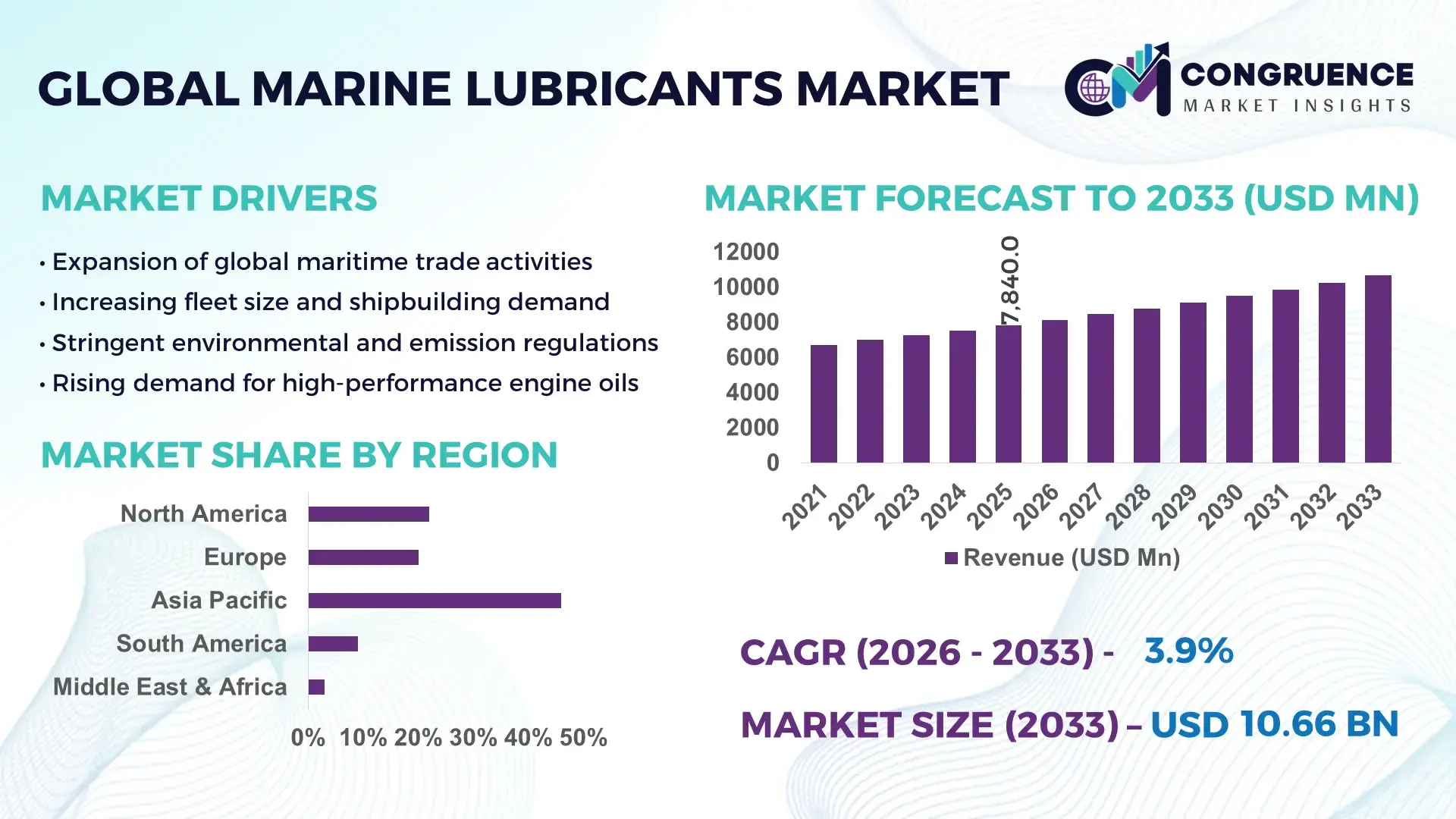

The Global Marine Lubricants Market was valued at USD 7840 Million in 2025 and is anticipated to reach a value of USD 10655.52 Million by 2033 expanding at a CAGR of 3.91% between 2026 and 2033. Growth is primarily driven by expanding global seaborne trade and increasing demand for fuel-efficient marine engines.

China stands as the dominant country in the Marine Lubricants market, supported by its extensive shipbuilding capacity and maritime infrastructure. The country accounted for over 45% of global shipbuilding output in 2024, with more than 1,700 vessels delivered annually. Its marine lubricant consumption exceeds 1.2 million metric tons per year, driven by commercial fleets, bulk carriers, and container vessels. Investments exceeding USD 10 billion in port modernization and offshore exploration have accelerated demand for high-performance lubricants. Additionally, China’s adoption of low-sulfur fuel standards has increased demand for advanced cylinder oils with enhanced thermal stability, with over 60% of new vessels using next-generation lubricant formulations.

Market Size & Growth: USD 7840 million in 2025, projected to reach USD 10655.52 million by 2033 at 3.91% CAGR, driven by increasing global shipping activities and fleet modernization.

Top Growth Drivers: 35% rise in global maritime trade volumes, 28% improvement in engine efficiency requirements, 22% increase in demand for low-emission lubricants.

Short-Term Forecast: By 2028, optimized lubrication systems are expected to reduce vessel maintenance costs by 18% and improve engine life by 20%.

Emerging Technologies: AI-based predictive lubrication systems, bio-based marine lubricants, and nano-additive formulations enhancing wear resistance.

Regional Leaders: Asia-Pacific projected at USD 4.8 billion by 2033 with strong shipbuilding demand; Europe at USD 2.7 billion driven by sustainability adoption; North America at USD 1.9 billion with offshore activity growth.

Consumer/End-User Trends: Commercial shipping fleets account for over 60% of lubricant consumption, with rising adoption in LNG carriers and offshore vessels.

Pilot or Case Example: In 2024, a Singapore-based shipping operator achieved 15% fuel efficiency improvement using AI-enabled lubrication monitoring systems.

Competitive Landscape: Market leader holds approximately 20% share, followed by major players such as Shell, ExxonMobil, BP, TotalEnergies, and Chevron.

Regulatory & ESG Impact: IMO regulations targeting 50% emission reduction by 2050 are accelerating adoption of eco-friendly lubricants.

Investment & Funding Patterns: Over USD 2.5 billion invested globally in marine engine efficiency and lubricant innovation projects between 2023 and 2025.

Innovation & Future Outlook: Integration of smart sensors, biodegradable oils, and digital monitoring platforms is reshaping performance optimization strategies.

Marine lubricants are critical across key sectors including container shipping, bulk carriers, oil tankers, and offshore exploration, collectively contributing over 80% of total consumption. Recent advancements such as synthetic lubricants with 25% longer lifecycle and bio-lubricants reducing environmental impact by up to 40% are transforming product offerings. Regulatory frameworks emphasizing sulfur emission limits and water pollution control are reshaping product formulations. Asia-Pacific leads consumption due to high fleet density, while Europe emphasizes sustainable alternatives. Emerging trends include digital condition monitoring and hybrid propulsion compatibility, positioning the market for efficiency-driven and environmentally compliant growth.

Marine Lubricants Market strategy is increasingly centered on performance optimization, regulatory compliance, and sustainability integration. Advanced synthetic lubricants deliver 30% longer service intervals compared to conventional mineral oils, significantly reducing maintenance frequency and operational downtime. Asia-Pacific dominates in volume due to extensive commercial fleets, while Europe leads in adoption with over 55% of operators integrating environmentally acceptable lubricants.

By 2028, AI-driven lubrication monitoring systems are expected to improve predictive maintenance accuracy by 25%, minimizing unexpected engine failures. Firms are committing to ESG metrics such as 40% reduction in marine lubricant toxicity and increased biodegradability standards by 2030. In 2024, Norway achieved a 20% reduction in marine engine wear through the deployment of smart lubrication technologies in offshore fleets.

The Marine Lubricants Market is evolving as a strategic enabler of maritime efficiency, aligning operational performance with environmental compliance and long-term sustainability goals.

The Marine Lubricants Market is influenced by rising global maritime trade, stricter emission regulations, and advancements in engine technology. Demand is closely tied to fleet expansion, vessel maintenance cycles, and fuel quality transitions such as low-sulfur fuels. Increasing adoption of LNG-powered vessels and hybrid propulsion systems is driving the need for specialized lubricants. Additionally, digital monitoring technologies are improving lubricant efficiency and lifecycle management. Regional dynamics vary, with Asia-Pacific leading in consumption and Europe emphasizing eco-friendly alternatives. Supply chain volatility in base oil production and additive availability continues to impact pricing and procurement strategies across the industry.

Global seaborne trade accounts for over 80% of international goods transport, directly increasing lubricant demand across commercial fleets. The global merchant fleet surpassed 100,000 vessels in 2024, each requiring regular lubrication for engine performance and durability. Increased cargo volumes, especially in containerized trade and energy transportation, have raised lubricant consumption cycles by nearly 15%. Additionally, expansion of offshore oil exploration and LNG shipping has intensified demand for high-performance lubricants capable of operating under extreme pressure and temperature conditions, reinforcing market growth.

Stringent environmental policies such as sulfur emission caps and water discharge regulations are limiting the use of traditional marine lubricants. Compliance with International Maritime Organization guidelines has increased formulation costs by up to 20%, requiring advanced additives and cleaner base oils. Many operators face challenges in transitioning to biodegradable lubricants due to higher costs and limited availability. Additionally, retrofitting older vessels to meet compliance standards has slowed adoption rates, creating operational and financial constraints within the Marine Lubricants market.

Bio-based marine lubricants present significant growth potential due to their low toxicity and high biodegradability. These lubricants can reduce environmental impact by up to 40% compared to conventional oils, aligning with global sustainability mandates. Increasing adoption in environmentally sensitive regions such as Arctic shipping routes and offshore wind farms is expanding market scope. Technological advancements have improved oxidation stability and performance, enabling wider use across vessel types. Government incentives and regulatory support are further encouraging manufacturers to invest in eco-friendly lubricant innovations.

Marine lubricant production heavily depends on base oils and chemical additives derived from crude oil, making it vulnerable to price volatility. Fluctuations in crude oil prices can impact production costs by up to 30%, creating pricing instability for manufacturers and end-users. Supply chain disruptions and geopolitical tensions further complicate procurement of essential additives. Additionally, the shift toward synthetic and bio-based lubricants requires advanced processing technologies, increasing capital expenditure and operational complexity for producers in the Marine Lubricants market.

• Rapid Adoption of Bio-Based Marine Lubricants (Over 40% Environmental Impact Reduction):

The shift toward environmentally acceptable lubricants is accelerating, with bio-based marine lubricants reducing aquatic toxicity by up to 40% compared to conventional oils. Approximately 35% of newly commissioned vessels in 2025 are equipped with biodegradable lubrication systems, particularly in ecologically sensitive zones. Northern European ports report over 50% compliance with eco-lubricant usage mandates, reflecting strong regulatory enforcement. Additionally, advancements in ester-based formulations have improved oxidation stability by 25%, enabling broader application across high-load marine engines.

• Integration of AI-Driven Predictive Lubrication Systems (Up to 25% Maintenance Optimization):

Digitalization is transforming lubrication management through AI-enabled monitoring systems. Around 30% of large commercial fleets have adopted predictive lubrication analytics, reducing unexpected engine failures by nearly 20%. Sensor-based oil condition monitoring has improved lubricant utilization efficiency by 18%, extending service intervals significantly. Fleet operators using these systems report up to 25% reduction in maintenance costs and 15% improvement in vessel uptime, particularly in container shipping and LNG transport segments.

• Increasing Demand for Low-Sulfur Compatible Lubricants (Over 60% Fleet Transition):

The transition to low-sulfur fuels has reshaped lubricant formulations, with over 60% of global fleets now requiring specialized cylinder oils. These lubricants demonstrate up to 30% enhanced deposit control and 20% improved corrosion resistance. Adoption is particularly high in Asia-Pacific, where compliance-driven demand has increased lubricant consumption cycles by 12%. Engine manufacturers are also recommending tailored lubrication solutions to optimize performance under new fuel standards.

• Growth in Synthetic Lubricants Offering Extended Lifecycle (Up to 30% Longer Usage):

Synthetic marine lubricants are gaining traction due to their extended lifecycle and superior thermal stability. These lubricants can last up to 30% longer than mineral-based alternatives, reducing oil change frequency by 20%. Currently, synthetic variants account for approximately 45% of usage in high-performance vessels such as LNG carriers and offshore rigs. Their ability to maintain viscosity under extreme pressure conditions has improved engine efficiency by 15%, making them a preferred choice for modern marine operations.

The Marine Lubricants market is segmented by type, application, and end-user, each contributing distinctively to demand patterns. Engine oils dominate product segmentation due to their critical role in vessel performance, accounting for over 50% of total consumption. Application-wise, commercial shipping leads with more than 60% utilization, driven by global trade expansion. Offshore operations and naval fleets follow with specialized lubrication requirements. In terms of end-users, shipping companies represent the largest segment, supported by large fleet sizes and frequent maintenance cycles. Meanwhile, offshore energy operators and defense sectors are increasing adoption of advanced lubricants, particularly those compatible with high-pressure and environmentally regulated operations.

Marine lubricants are categorized into engine oils, hydraulic oils, compressor oils, gear oils, and greases, each serving specific operational requirements. Engine oils dominate the segment, accounting for approximately 52% of total usage due to their essential role in maintaining engine efficiency, reducing wear, and supporting combustion processes. Hydraulic oils and gear oils collectively hold around 28% share, primarily used in auxiliary systems and transmission components. Compressor oils and greases contribute the remaining 20%, catering to niche applications requiring specialized lubrication.

While engine oils currently lead adoption, synthetic lubricants are the fastest-growing segment, expanding at an estimated CAGR of 5.8% due to their extended service life and enhanced thermal performance. These products offer up to 30% longer operational cycles and improved resistance to oxidation. Increasing use in LNG carriers and offshore platforms is driving their growth.

Marine lubricants find application across commercial shipping, offshore exploration, naval operations, and recreational vessels. Commercial shipping leads the segment with approximately 62% share, driven by high vessel utilization rates and frequent lubrication cycles. Offshore exploration accounts for around 20%, requiring high-performance lubricants capable of operating under extreme pressure and temperature conditions. Naval fleets and recreational vessels together contribute the remaining 18%, with specialized requirements for durability and corrosion resistance.

Offshore exploration is the fastest-growing application, expanding at an estimated CAGR of 5.2% due to rising investments in deep-sea drilling and offshore wind energy projects. Lubricants used in this segment must withstand high loads and harsh marine environments, driving innovation in synthetic and bio-based formulations.

The Marine Lubricants market serves shipping companies, offshore oil and gas operators, naval defense organizations, and port authorities. Shipping companies dominate the segment with approximately 65% share, supported by large global fleets and continuous maintenance requirements. Offshore oil and gas operators account for around 18%, driven by high-intensity equipment usage in exploration and production. Naval defense and port authorities together represent the remaining 17%, focusing on reliability and long-term asset protection.

Offshore energy operators are the fastest-growing end-user segment, with an estimated CAGR of 5.5%, fueled by increasing offshore drilling activities and renewable energy installations. These users demand lubricants with superior thermal stability and corrosion resistance.

Region Asia-Pacific accounted for the largest market share at 46% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 4.6% between 2026 and 2033.

Asia-Pacific consumed over 2.8 million metric tons of marine lubricants, driven by high vessel density and shipbuilding output exceeding 50% globally. Europe accounted for 24% share, supported by over 60% adoption of environmentally acceptable lubricants. North America held approximately 18%, with offshore activities contributing nearly 35% of regional demand. Middle East & Africa captured 7%, fueled by oil exports exceeding 20 million barrels per day, while South America contributed 5%, with Brazil accounting for over 60% of regional consumption.

North America accounts for nearly 18% of the Marine Lubricants market, with strong demand from offshore oil and gas, naval defense, and commercial shipping sectors. The U.S. contributes over 70% of regional consumption, supported by more than 12,000 registered commercial vessels. Regulatory frameworks promoting cleaner fuels have increased adoption of low-sulfur compatible lubricants by 45%. Digital transformation is evident, with over 30% of fleets integrating predictive maintenance systems. A leading regional player has expanded synthetic lubricant production by 20% to meet rising demand. Consumer behavior reflects higher adoption of premium lubricants, with over 50% of operators prioritizing performance optimization and reduced maintenance cycles.

Europe holds approximately 24% of the Marine Lubricants market, with key contributors including Germany, the UK, and France. Over 60% of vessels operating in European waters utilize environmentally acceptable lubricants due to strict environmental directives. Regulatory initiatives targeting 50% emission reduction have accelerated demand for bio-based products. Technological adoption is high, with nearly 40% of operators using digital lubricant monitoring systems. A major regional producer has introduced biodegradable lubricants improving degradation rates by 35%. Consumer behavior emphasizes sustainability, with over 55% of operators prioritizing eco-certified products to meet compliance standards and reduce environmental impact.

Asia-Pacific leads the Marine Lubricants market with over 2.8 million metric tons consumption, driven by China, Japan, and India. China alone contributes more than 40% of regional demand, supported by shipbuilding output exceeding 1,700 vessels annually. Infrastructure expansion across ports handling over 60% of global cargo volume strengthens lubricant demand. Technological hubs in Japan and South Korea are advancing synthetic lubricant formulations with 20% improved efficiency. A regional manufacturer has increased production capacity by 25% to meet export demand. Consumer behavior is volume-driven, with over 65% of operators focusing on cost-efficient lubrication solutions for large commercial fleets.

South America accounts for approximately 5% of the Marine Lubricants market, with Brazil and Argentina leading consumption. Brazil contributes over 60% of regional demand, supported by offshore oil production exceeding 3 million barrels per day. Infrastructure investments in port modernization have increased lubricant consumption by 12%. Government policies promoting energy exports have strengthened demand for high-performance lubricants. A regional supplier has expanded distribution networks by 18% to improve accessibility. Consumer behavior shows moderate adoption of advanced lubricants, with around 40% of operators transitioning toward synthetic and bio-based products for improved efficiency and compliance.

Middle East & Africa represent around 7% of the Marine Lubricants market, driven by oil and gas exports and maritime logistics. The UAE and Saudi Arabia account for over 55% of regional demand, supported by crude exports exceeding 20 million barrels per day. Technological modernization includes adoption of high-performance lubricants improving engine efficiency by 15%. Trade partnerships and port expansions handling over 10% of global oil shipments enhance market growth. A regional player has invested in advanced blending facilities increasing output by 22%. Consumer behavior is efficiency-focused, with over 50% of operators adopting premium lubricants to reduce operational downtime.

China – 32% share in the Marine Lubricants market, driven by extensive shipbuilding capacity and high maritime trade volumes.

United States – 18% share in the Marine Lubricants market, supported by strong offshore energy operations and large commercial fleet base.

The Marine Lubricants market exhibits a moderately consolidated structure, with over 40 active global and regional competitors competing across product innovation, pricing strategies, and distribution networks. The top five companies collectively account for approximately 55% of the total market share, indicating a strong presence of established multinational players alongside regional specialists. Leading companies are focusing on strategic partnerships with shipping operators, resulting in long-term supply agreements covering over 30% of global fleet requirements.

Product innovation remains a key competitive factor, with more than 35% of new product launches centered on bio-based and synthetic lubricants offering up to 30% extended lifecycle performance. Mergers and acquisitions have increased by 15% between 2023 and 2025, aimed at expanding regional footprint and strengthening supply chains. Digital integration is also shaping competition, with over 25% of major players deploying AI-driven lubricant monitoring systems. Additionally, investment in R&D has risen by 20%, particularly in developing low-emission and high-efficiency lubricant formulations, intensifying competition across both developed and emerging markets.

Royal Dutch Shell

ExxonMobil Corporation

BP plc

TotalEnergies SE

Chevron Corporation

Lukoil

Idemitsu Kosan Co., Ltd.

Sinopec Corporation

Fuchs Petrolub SE

Petronas Lubricants International

Castrol Limited

Gulf Oil International

Phillips 66 Company

Indian Oil Corporation Ltd.

ENEOS Corporation

Technological advancements in the Marine Lubricants market are centered on improving engine efficiency, reducing environmental impact, and enabling predictive maintenance. Synthetic lubricant formulations now offer up to 30% longer service intervals and 20% higher oxidation stability compared to mineral oils, making them suitable for high-performance engines and LNG-powered vessels. Nano-additive technologies are enhancing anti-wear properties by nearly 25%, significantly extending engine component life under extreme operating conditions.

Digital transformation is another key trend, with over 35% of large commercial fleets adopting sensor-based oil condition monitoring systems. These technologies analyze viscosity, contamination levels, and temperature in real time, reducing unplanned downtime by up to 20%. Artificial intelligence integration further improves predictive maintenance accuracy by approximately 25%, optimizing lubricant usage cycles.

Additionally, bio-based lubricants are gaining traction, with formulations achieving up to 40% reduction in environmental toxicity while maintaining comparable thermal stability. Hybrid propulsion systems and electric-assisted vessels are also driving the need for specialized lubricants with enhanced dielectric and cooling properties, positioning technology as a core driver of performance optimization and regulatory compliance.

• In March 2025, Shell expanded its marine lubricant portfolio by launching Shell Argina S5, designed for next-generation low-speed engines operating on alternative fuels. The product improves deposit control by 20% and enhances engine cleanliness, supporting compliance with evolving marine emission standards. Source: www.shell.com

• In September 2024, ExxonMobil introduced Mobilgard 540 X, a high-performance cylinder oil formulated for two-stroke engines using low-sulfur fuels. The lubricant demonstrated up to 25% reduction in piston deposits during field trials, improving engine efficiency and reducing maintenance intervals. Source: www.exxonmobil.com

• In May 2025, TotalEnergies partnered with a global shipping operator to deploy advanced bio-based marine lubricants across a fleet of 50 vessels, achieving a 30% reduction in environmental impact and improving lubricant lifecycle performance under varying load conditions. Source: www.totalenergies.com

• In November 2024, BP Castrol launched a new range of synthetic marine lubricants engineered for LNG carriers, delivering up to 15% improved thermal stability and extended oil drain intervals, supporting high-efficiency operations in extreme marine environments. Source: www.bp.com

The Marine Lubricants Market Report provides a comprehensive evaluation of key market segments, including engine oils, hydraulic fluids, compressor oils, greases, and specialty lubricants, collectively representing over 90% of marine lubrication applications. The report covers critical application areas such as commercial shipping, offshore oil and gas, naval defense, and recreational vessels, with commercial fleets accounting for more than 60% of total demand.

Geographically, the study analyzes five major regions, with Asia-Pacific contributing over 45% of global consumption, followed by Europe at 24% and North America at 18%. The report also examines emerging segments such as bio-based lubricants and synthetic formulations, which together account for approximately 40% of advanced product adoption.

Technological coverage includes digital lubrication monitoring systems, AI-based predictive maintenance, and nano-additive innovations improving efficiency by up to 25%. The scope further includes regulatory frameworks influencing product development, such as sulfur emission limits and environmental compliance standards. This report delivers a data-driven perspective on operational trends, innovation pathways, and evolving end-user requirements shaping the Marine Lubricants market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

3.91% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Royal Dutch Shell, ExxonMobil Corporation, BP plc, TotalEnergies SE, Chevron Corporation, Lukoil, Idemitsu Kosan Co., Ltd., Sinopec Corporation, Fuchs Petrolub SE, Petronas Lubricants International, Castrol Limited, Gulf Oil International, Phillips 66 Company, Indian Oil Corporation Ltd., ENEOS Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |