Reports

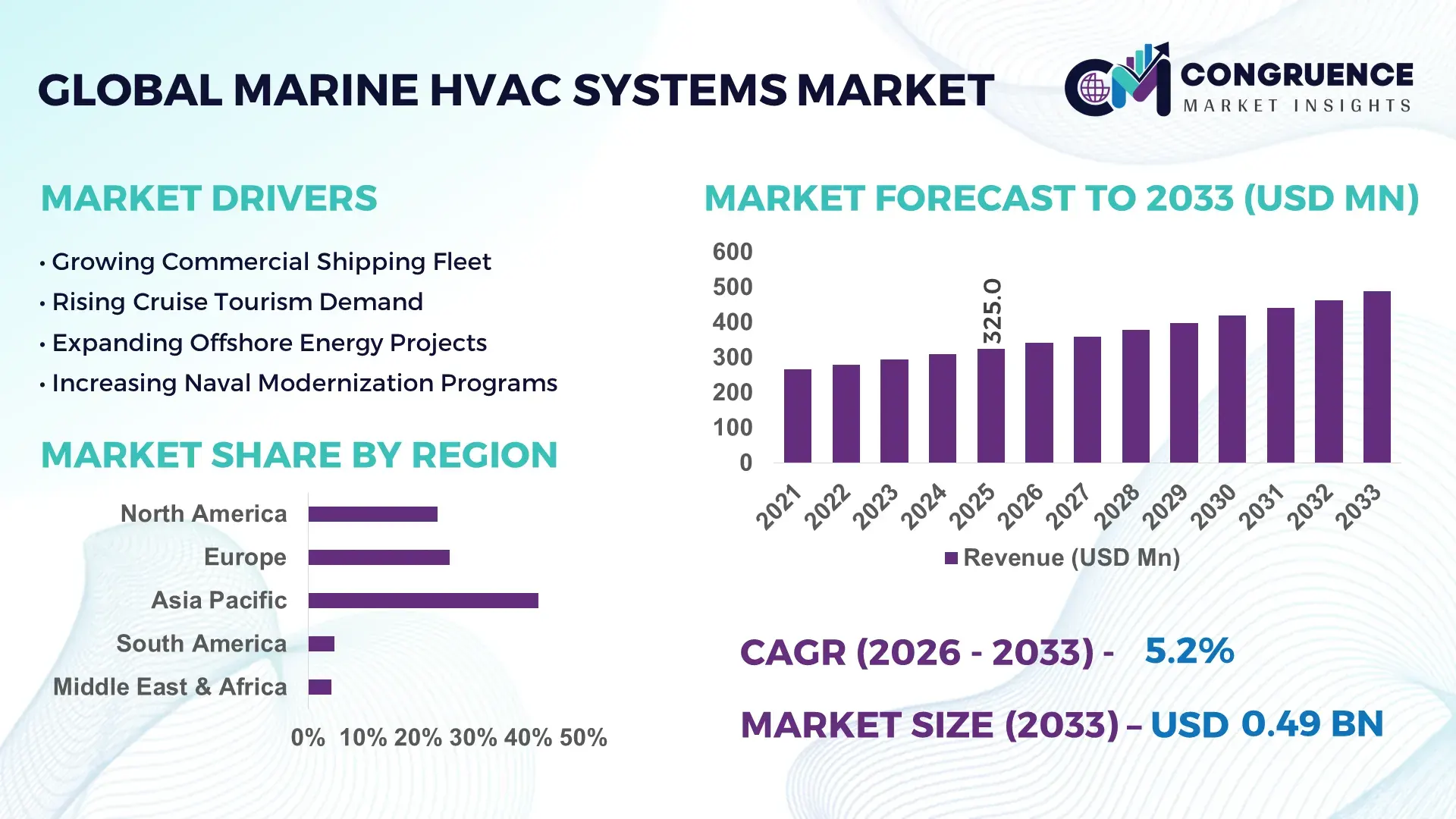

The Global Marine HVAC Systems Market was valued at USD 325.0 Million in 2025 and is anticipated to reach a value of USD 487.5 Million by 2033 expanding at a CAGR of 5.2% between 2026 and 2033. Growth is being propelled by stricter maritime emission regulations, rising cruise fleet modernization programs, and increasing deployment of energy-efficient climate control systems across commercial and naval vessels.

China remains the dominant country in the marine HVAC systems landscape, accounting for nearly 47% of global shipbuilding output and over 50% of newly commissioned commercial vessel capacity. Supported by investments exceeding USD 15 billion in shipyard modernization and smart vessel development, Chinese shipbuilders are integrating advanced HVAC automation and heat-recovery technologies at scale. Compared with South Korea's approximately 29% shipbuilding share, China demonstrates broader adoption across cargo, offshore, and passenger fleets. The ongoing Red Sea shipping disruption has further reinforced demand for operationally efficient onboard climate-control infrastructure.

Strategically, manufacturers that align energy-efficient HVAC innovation with vessel digitalization and fleet modernization programs are securing stronger positions across high-volume shipbuilding ecosystems.

Market Size & Growth: USD 325.0 million in 2025, reaching USD 487.5 million by 2033 at 5.2% CAGR, supported by vessel electrification and advanced energy-management integration.

Top Growth Drivers: Cruise fleet upgrades (+18%), smart ship deployment (+24%), and IMO efficiency compliance adoption (+21%) are accelerating procurement activity.

Short-Term Forecast: By 2028, HVAC energy consumption per vessel is projected to decline by 12–15% through intelligent control optimization.

Emerging Technologies: AI-driven monitoring, predictive maintenance platforms, and variable refrigerant flow systems are improving system efficiency by over 20%.

Regional Leaders: Asia Pacific (~USD 185 million), Europe (~USD 98 million), and North America (~USD 72 million) lead through shipbuilding expansion, retrofit demand, and naval modernization.

Consumer/End-User Trends: More than 62% of new cruise and passenger vessel projects prioritize low-emission HVAC integration.

Pilot/Case Example: A 2024 smart-vessel deployment reduced HVAC-related power consumption by 17% through automated load balancing.

Competitive Landscape: Top manufacturers control approximately 45% market share, led by Carrier Marine, Daikin, Johnson Controls, Heinen & Hopman, and Wärtsilä.

Regulatory & ESG Impact: New maritime efficiency requirements are supporting 14% reductions in onboard energy intensity across upgraded fleets.

Investment & Funding: Over USD 2.5 billion has been directed toward shipyard modernization, fleet retrofits, and maritime decarbonization initiatives.

Innovation & Future Outlook: Connected HVAC ecosystems, digital twins, and integrated thermal-management architectures are becoming core competitive differentiators.

Marine HVAC Systems are increasingly deployed across cruise vessels, naval fleets, offshore platforms, and commercial cargo ships where crew comfort, equipment protection, and energy optimization are critical. Recent innovations include AI-enabled thermal controls, low-GWP refrigerants, and predictive maintenance capabilities that improve system uptime by more than 15%. Growing compliance requirements and vessel-efficiency mandates are accelerating retrofit activity, while ongoing maritime supply-chain restructuring is encouraging operators to prioritize resilient, digitally managed onboard climate-control infrastructure, creating a foundation for broader strategic investment decisions.

Marine HVAC systems are becoming strategically important as vessel operators pursue operational efficiency, compliance readiness, and lifecycle cost optimization simultaneously. The sector is increasingly linked to broader maritime modernization programs, particularly as shipping companies invest in digital vessel architectures and energy-management systems. Regulatory pressure surrounding vessel emissions and onboard energy consumption is pushing HVAC systems from a support function to a core operational asset.

Modern intelligent HVAC platforms deliver measurable advantages over conventional fixed-speed systems. Variable-speed compressor technologies can reduce energy consumption by 15–25% while improving thermal control precision and lowering maintenance requirements. South Korea and China are emphasizing large-scale deployment across newly constructed vessels, whereas European operators are concentrating on retrofit programs for existing fleets. Across leading shipbuilding hubs, digital monitoring adoption has surpassed 40% among newly specified HVAC installations, reflecting a shift toward predictive asset management.

A practical example is the integration of sensor-driven ventilation systems on cruise vessels, where automated airflow balancing reduces auxiliary power loads and improves passenger comfort. Manufacturers are expanding partnerships with shipyards, automation providers, and marine engineering firms to secure long-term contracts. Over the next two to three years, fleet modernization, connected-vessel deployment, and energy-efficiency mandates will increasingly determine competitive positioning, making advanced marine HVAC capabilities a critical source of operational advantage and long-term industry relevance.

Global ship operators are accelerating investment in energy-efficient vessel infrastructure as fuel optimization and compliance requirements intensify. HVAC systems account for approximately 20–35% of onboard hotel-load energy consumption, making efficiency upgrades a high-impact investment area. More than 60% of new passenger vessel specifications now include intelligent HVAC controls, while variable-speed technologies can lower energy use by up to 25%. Following recent maritime decarbonization initiatives, shipbuilders in China and South Korea are incorporating integrated thermal-management platforms into new vessel designs. This shift directly reduces operating costs and improves environmental performance. In response, manufacturers are expanding engineering partnerships, increasing R&D spending on smart controls, and introducing low-emission refrigeration technologies. The key strategic insight is that HVAC performance is increasingly influencing vessel efficiency ratings and procurement decisions.

Marine HVAC deployment continues to face pressure from component cost volatility and specialized equipment sourcing challenges. Advanced compressors, marine-grade heat exchangers, and electronic control systems have experienced procurement cost increases ranging from 10–18% in recent years. Lead times for selected maritime HVAC components remain 20–30% longer than pre-disruption levels, particularly for electronically controlled systems. Dependence on globally distributed supplier networks creates additional operational uncertainty for shipbuilders and retrofit contractors. These factors increase project costs and complicate installation schedules for commercial fleets. To mitigate exposure, manufacturers are diversifying supplier bases, localizing selected production activities, and securing multi-year procurement agreements. A critical operational insight is that supply-chain resilience is becoming as important as technological differentiation in large-scale marine projects.

The emergence of connected vessels is creating significant opportunities for next-generation marine HVAC solutions. Smart monitoring platforms can improve maintenance efficiency by 20% while reducing unexpected system downtime by more than 15%. Increasing deployment of digital twins, onboard analytics, and AI-driven thermal optimization enables operators to manage climate-control performance in real time. Singapore and Norway are actively supporting maritime digitalization initiatives that accelerate adoption of intelligent onboard systems. Companies are investing heavily in predictive maintenance software, integrated sensor networks, and cloud-enabled diagnostics to capture this opportunity. A particularly valuable insight is the growing demand for HVAC systems that contribute operational data to broader vessel management ecosystems, transforming climate-control equipment into a strategic source of performance intelligence.

As ships become increasingly digitalized, integrating HVAC systems with navigation, power management, and automation platforms presents growing complexity. More than 40% of advanced vessel projects now require interoperability across multiple onboard digital systems. Cybersecurity requirements have also intensified, with connected maritime assets facing rising exposure to operational technology vulnerabilities. Workforce limitations represent another challenge, as demand for technicians skilled in marine automation and intelligent HVAC controls continues to exceed supply in several shipbuilding markets. These issues affect deployment consistency, maintenance efficiency, and long-term operational reliability. Companies must address these challenges through workforce training, cybersecurity investment, and standardized communication protocols. The strongest competitive performers will be those capable of delivering seamless integration across increasingly sophisticated vessel ecosystems while maintaining operational reliability at scale.

Smart Controls Reshape Operations Marine operators are rapidly deploying AI-enabled HVAC management platforms, with intelligent monitoring adoption exceeding 40% in newly specified passenger vessels and automated diagnostics reducing unplanned maintenance events by nearly 18%. Digital workflows now allow real-time thermal balancing and equipment performance tracking. As skilled labor shortages intensify across major shipbuilding nations, manufacturers are integrating predictive maintenance software and remote support capabilities, improving service responsiveness while lowering onboard engineering workload and operational interruptions.

Low-GWP Refrigerant Transition Accelerates Regulatory pressure on vessel emissions and environmental performance is driving a significant refrigerant transition. More than 35% of newly installed marine HVAC systems now utilize lower-global-warming-potential refrigerants, while energy-efficient compressor configurations improve cooling efficiency by approximately 12–20%. Shipowners are increasingly prioritizing lifecycle compliance rather than upfront equipment cost. In response, suppliers are expanding certified product portfolios, restructuring procurement strategies, and forming technology partnerships to ensure compliance readiness across commercial, cruise, and offshore vessel fleets.

Retrofit Demand Gains Momentum Fleet modernization programs are accelerating retrofit activity, particularly among vessels operating beyond 15 years of service life. Retrofit installations now account for nearly 30% of marine HVAC project activity in several established maritime markets. Operators are replacing legacy air-handling units and controls to reduce energy consumption by 10–15% and improve onboard comfort standards. HVAC suppliers are scaling retrofit engineering teams and developing modular upgrade packages that minimize vessel downtime during maintenance windows.

Integrated Vessel Platforms Expand HVAC systems are increasingly connected with broader ship automation ecosystems, with integration rates surpassing 45% among advanced vessel construction projects. Shared operational data improves energy optimization, ventilation control, and equipment coordination across onboard systems. A less obvious shift is the growing use of HVAC-generated performance data within vessel-wide efficiency reporting frameworks. To capitalize on this trend, companies are investing in interoperable software architectures, automation partnerships, and cybersecure communication platforms that support connected maritime operations.

Centralized marine HVAC systems remain the leading segment, accounting for approximately 52% of installations across commercial ships, cruise liners, and naval platforms. Their dominance stems from superior scalability, centralized monitoring capabilities, and lower lifecycle maintenance requirements on large vessels. Operators benefit from integrated airflow management, consistent thermal control, and improved energy utilization across multiple compartments. Manufacturers continue to strengthen this segment through advanced automation integration, modular architecture development, and energy-efficient compressor technologies that improve system performance by nearly 15%. Packaged HVAC systems represent the fastest-growing type as shipowners prioritize simplified installation and reduced deployment complexity. Adoption has increased by nearly 20% across offshore support vessels and medium-sized commercial fleets where space optimization remains critical. Split-system configurations continue serving specialized marine environments requiring flexible zoning control, while portable marine HVAC units maintain strategic relevance for temporary cooling applications and maintenance operations. Investment priorities are gradually shifting toward intelligent packaged systems equipped with predictive diagnostics and remote monitoring capabilities, reflecting broader vessel digitalization trends and evolving operational efficiency objectives.

Commercial shipping continues to represent the leading application segment, contributing approximately 48% of total marine HVAC demand due to the vast global fleet of container ships, bulk carriers, and tanker vessels. Fleet operators increasingly deploy advanced climate-control systems to enhance crew welfare, equipment protection, and operational efficiency during extended voyages. HVAC modernization projects have increased by nearly 16% among large commercial fleets as energy-management requirements become more stringent and vessel operating costs receive greater scrutiny. Cruise ships are emerging as the fastest-growing application segment, supported by rising passenger comfort expectations and extensive fleet renewal programs. Smart ventilation adoption has expanded by approximately 22% within newly constructed cruise vessels, where indoor environmental quality directly influences customer experience. Naval vessels continue investing in resilient HVAC infrastructure for mission-critical reliability, while offshore platforms maintain steady demand for specialized corrosion-resistant climate-control solutions. Manufacturers are responding through customized product development, integrated automation capabilities, and dedicated service agreements tailored to distinct operational environments and performance requirements.

Commercial fleet operators remain the dominant end-user group, accounting for nearly 55% of procurement activity due to their extensive vessel ownership, continuous maintenance requirements, and fleet modernization initiatives. HVAC systems are increasingly viewed as operational assets that influence fuel efficiency, crew productivity, and equipment reliability. More than 40% of large shipping companies have expanded investment in intelligent climate-control technologies to improve onboard energy management and reduce maintenance interventions. Suppliers are strengthening relationships with ship operators through lifecycle service contracts, remote monitoring offerings, and performance-based maintenance programs. Cruise and passenger vessel operators represent the fastest-growing end-user segment, supported by rising comfort standards and expanding tourism-related fleet investments. Adoption of advanced air-quality management technologies has increased by approximately 20% across newly delivered passenger vessels. Naval organizations continue prioritizing resilient and mission-ready HVAC infrastructure, while offshore energy operators maintain demand for durable systems capable of operating in harsh environments. To capture emerging opportunities, manufacturers are developing segment-specific solutions, enhancing aftermarket capabilities, and expanding strategic partnerships with shipyards and marine engineering firms.

Asia-Pacific accounted for the largest market share at 41.8% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 6.4% between 2026 and 2033.

North America represented approximately 23.5% of the global Marine HVAC Systems Market in 2025, supported by naval fleet modernization, cruise vessel refurbishment, and increasing investment in energy-efficient onboard infrastructure. The region demonstrates strong adoption of automated HVAC monitoring systems, particularly across defense and passenger vessel applications. More than 45% of newly specified marine HVAC projects now incorporate predictive maintenance functionality to improve operational reliability. Shipyards and marine engineering contractors are increasingly prioritizing integrated climate-control architectures that support vessel digitalization objectives. Strategic partnerships between HVAC suppliers and maritime technology firms are accelerating deployment of intelligent thermal-management platforms across both commercial and government-operated fleets.

United States Market Outlook: The United States remains the largest contributor within North America due to its extensive naval fleet, advanced shipbuilding capabilities, and cruise vessel operations. More than 30 major naval modernization programs currently incorporate upgraded environmental-control systems as part of broader vessel lifecycle extension initiatives. Strong investment in shipyard modernization and maritime automation continues to support demand for advanced HVAC technologies featuring predictive diagnostics, cybersecurity integration, and energy-efficiency optimization.

Europe accounted for nearly 25.7% of global demand, driven by environmental compliance requirements, maritime sustainability initiatives, and fleet modernization programs. Vessel operators are increasingly replacing conventional HVAC systems with low-emission alternatives to support stricter operational efficiency targets. More than 38% of retrofit projects across European commercial fleets now include HVAC efficiency upgrades. Demand is particularly concentrated within cruise vessels, offshore support ships, and advanced marine engineering projects. Technology providers are expanding partnerships with shipyards to deploy intelligent ventilation systems, energy-recovery technologies, and advanced refrigerant solutions aligned with evolving environmental standards and operational performance objectives.

Norway Market Outlook: Norway maintains a strategically significant position through its leadership in green shipping initiatives and advanced maritime technology deployment. Electrified vessel programs and sustainable marine infrastructure investments are accelerating HVAC modernization efforts. More than 50% of newly commissioned specialized vessels incorporate integrated energy-management systems linked to HVAC operations. Norwegian operators continue emphasizing low-emission technologies and smart vessel architectures, creating favorable conditions for advanced marine climate-control solutions.

Asia-Pacific remains the dominant regional market with a 41.8% share, supported by extensive shipbuilding activity, fleet expansion programs, and large-scale maritime infrastructure investment. The region accounts for over 70% of global commercial shipbuilding output, creating substantial demand for marine HVAC installations across cargo, passenger, and offshore vessel categories. Advanced automation integration is becoming increasingly common, with intelligent HVAC deployment growing by approximately 22% across newly constructed vessels. Strong manufacturing ecosystems, extensive supplier networks, and shipyard expansion projects continue reinforcing the region’s leadership position in marine environmental-control technologies.

China Market Outlook: China serves as the most influential market due to its unmatched shipbuilding capacity, extensive maritime manufacturing ecosystem, and ongoing smart-vessel development initiatives. The country contributes nearly 47% of global shipbuilding output and continues investing heavily in digital shipyard modernization. Large commercial vessel projects increasingly specify automated HVAC systems equipped with remote monitoring and energy-optimization capabilities. Government-backed maritime modernization programs and export-focused shipbuilding strategies further strengthen demand for advanced onboard environmental-management solutions.

South America accounted for approximately 4.8% of global market activity, with demand primarily concentrated around offshore energy operations, commercial shipping routes, and vessel maintenance programs. Marine HVAC deployment is increasingly linked to offshore platform support vessels requiring durable climate-control systems capable of operating in demanding marine environments. Nearly 28% of specialized offshore vessel upgrades now include HVAC modernization components designed to improve crew comfort and equipment reliability. While infrastructure limitations and uneven shipbuilding capacity constrain market scale, growing offshore investment continues creating targeted opportunities for advanced marine environmental-control technologies.

Brazil Market Outlook: Brazil leads regional demand through its extensive offshore oil and gas sector, maritime logistics network, and fleet maintenance requirements. Offshore support vessels operating in deepwater energy projects increasingly require high-performance HVAC systems with corrosion-resistant designs. National port modernization initiatives and expanding offshore operations continue supporting procurement activity. Operators are also adopting advanced monitoring technologies to reduce maintenance downtime and improve environmental control across long-duration offshore deployments.

Middle East & Africa represented approximately 4.2% of the global market in 2025 and is emerging as the fastest-expanding regional opportunity. Large-scale port infrastructure projects, maritime logistics investments, and fleet modernization programs are strengthening demand for advanced HVAC systems. More than 20 major maritime infrastructure initiatives are currently underway across the Gulf region, supporting deployment of modern vessel technologies. Demand is also increasing for energy-efficient cooling solutions capable of operating under extreme climatic conditions. Marine equipment suppliers are expanding regional partnerships and service capabilities to support rising vessel activity and long-term infrastructure development.

Saudi Arabia Market Outlook: Saudi Arabia is becoming the region’s most strategically important market due to extensive maritime infrastructure investments, logistics diversification initiatives, and industrial development programs. Major port expansion projects and shipyard development efforts are creating sustained demand for advanced vessel-support technologies. Maritime modernization activities linked to national economic diversification strategies are encouraging adoption of intelligent HVAC systems with enhanced energy-management capabilities. Increasing commercial vessel traffic and marine infrastructure investment continue positioning the country as a key future demand center for marine environmental-control solutions.

The Marine HVAC Systems Market is characterized by competition between global marine HVAC leaders such as Heinen & Hopman, Johnson Controls, Daikin Industries, Wärtsilä, and Carrier Marine, versus regional marine engineering contractors and vessel-specific HVAC integrators. The top five players collectively control approximately 42–48% of market activity, particularly across cruise ships, naval vessels, and large commercial fleets. Competition is centered on energy efficiency, lifecycle service capability, customization, and shipyard relationships rather than equipment pricing alone. Advanced HVAC systems offering 15–25% lower energy consumption and predictive maintenance capabilities are increasingly winning contracts. More than 40% of new vessel projects now require integration with digital vessel management platforms, creating an advantage for technology-focused suppliers. Leading companies are expanding through long-term shipyard agreements, retrofit service networks, automation partnerships, and vertically integrated engineering capabilities. The competitive shift is moving from standalone equipment supply toward full-lifecycle environmental management solutions. High certification requirements, vessel-specific engineering expertise, and global service coverage remain significant entry barriers. Winning increasingly requires digital integration, proven marine deployment experience, and strong aftermarket support rather than cost leadership alone.

Johnson Controls International plc

Heinen & Hopman Engineering B.V.

Wärtsilä Corporation

Carrier Marine & Offshore Systems

Trane Technologies plc

GEA Group AG

Dometic Group AB

Frigomar S.r.l.

Novenco Marine & Offshore A/S

Horn International AS

AF Group ASA

Bronswerk Marine Inc.

Drews Marine GmbH

Marine HVAC technology is rapidly shifting from conventional standalone cooling systems toward intelligent, connected environmental-control platforms. AI-enabled monitoring, predictive diagnostics, and smart ventilation controls are now being deployed in more than 40% of advanced vessel projects. These technologies reduce unplanned maintenance events by approximately 18% while improving equipment utilization and onboard thermal stability. Integration with vessel automation systems is becoming a key differentiator for commercial operators and naval fleets seeking higher operational reliability.

Emerging technologies include low-GWP refrigerants, variable-speed compressors, digital twin modeling, and cloud-based performance monitoring. Compared with traditional fixed-speed HVAC systems, modern variable-speed platforms can reduce energy consumption by 15–25% while improving cooling precision and lowering maintenance intervention frequency. Adoption is particularly strong among cruise operators and large commercial fleets where HVAC systems account for a significant share of auxiliary energy demand. Companies with advanced controls expertise are gaining competitive advantages through improved lifecycle performance and regulatory readiness.

Between 2026 and 2028, disruptive innovation will increasingly focus on autonomous optimization, cybersecure HVAC connectivity, and integrated thermal-management ecosystems. Deployment of predictive analytics is expected to exceed 50% among newly specified premium marine HVAC installations. Companies that invest early in software-enabled HVAC architectures will benefit from stronger service revenues, improved customer retention, and greater influence over vessel digitalization strategies.

February 2025 – Johnson Controls International announced leadership restructuring with the appointment of a new CEO while continuing expansion of intelligent HVAC and lifecycle service capabilities supporting more than 10,000 marine installations worldwide. The move strengthens operational focus and long-term maritime service competitiveness. Source: www.reuters.com

January 2025 – Heinen & Hopman Engineering expanded deployment of custom-built marine HVAC systems across commercial, naval, offshore, and cruise vessels, surpassing 15,000 vessel installations globally. The milestone reinforces its position in high-specification marine environmental-control projects.

December 2024 – Daikin Industries strengthened HVAC manufacturing strategy through a compressor-focused joint venture initiative, supporting localized supply-chain development and advanced HVAC equipment production. The expansion is designed to improve component availability and support long-term maritime HVAC deployment requirements.

March 2026 – Johnson Controls Marine Services expanded predictive maintenance and remote diagnostics capabilities supporting vessels equipped with its systems, which are installed on more than 20% of ocean-going vessels. The initiative improves uptime, maintenance planning, and operational efficiency for fleet operators.

This report provides comprehensive coverage of the Marine HVAC Systems Market across key system types, applications, end-user categories, and major geographic regions. The analysis evaluates centralized systems, packaged systems, split systems, and specialized marine climate-control solutions used across commercial shipping, cruise vessels, naval platforms, offshore assets, and other marine environments. Regional assessments cover North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting deployment concentration, technology adoption patterns, and competitive positioning trends.

The report further examines intelligent HVAC controls, predictive maintenance platforms, low-GWP refrigerants, automation integration, and digital vessel-management connectivity. More than 40% of advanced vessel projects now incorporate connected environmental-control technologies, while retrofit activity represents an increasingly important demand segment. Strategic insights support investment planning, product development, expansion prioritization, partnership evaluation, competitive benchmarking, and long-term positioning decisions across the evolving marine HVAC ecosystem between 2026 and 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 325.0 Million |

| Market Revenue (2033) | USD 487.5 Million |

| CAGR (2026–2033) | 5.2% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Daikin Industries, Ltd.; Johnson Controls International plc; Heinen & Hopman Engineering B.V.; Wärtsilä Corporation; Carrier Marine & Offshore Systems; Trane Technologies plc; GEA Group AG; Dometic Group AB; Frigomar S.r.l.; Novenco Marine & Offshore A/S; Horn International AS; AF Group ASA; Bronswerk Marine Inc.; Drews Marine GmbH |

| Customization & Pricing | Available on Request (10% Customization Free) |